|

|

市場調査レポート

商品コード

1445723

原薬CDMO:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年)Global Active Pharmaceutical Ingredients CDMO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 原薬CDMO:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

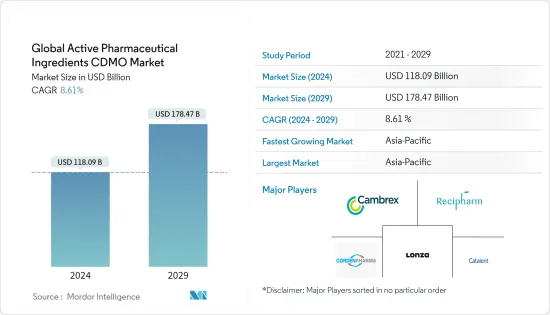

世界の原薬CDMO市場規模は、2024年に1,180億9,000万米ドルと推定され、2029年までに1,784億7,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に8.61%のCAGRで成長します。

COVID-19のパンデミックはAPI CDMO市場に大きな影響を与えました。コロナウイルスのワクチンと治療薬が世界的に展開されるにつれ、CDMOサービスの需要が急増しました。 CDMOは危機の間、製薬会社の顧客のニーズを満たすために多大な努力を払ってきました。 CDMOは、医薬品開発とサプライチェーン、商用 APIと医薬品の製造、パッケージングなどの幅広いサービスを製薬会社に提供します。これらのサービスにより、製薬会社は最先端のテクノロジーの恩恵を受けながら、開発および製造のコスト、資本投資およびスケジュールを削減できます。

たとえば、2021年上半期には、CDMOのCOVID-19ワクチン製造への参加や、強力な合併・買収活動が目立った。また、バイオ/医薬品業界におけるCDMOの不可欠性も強調しました。これは、COVID-19ウイルスと戦うワクチンや治療法の発売を成功させるために不可欠でした。

Drug, Chemical &Associated Technologies Association Inc.(DCAT)の「年央CDMOレビュー:COVID-19ワクチン製造とM&A」に関するバリューチェーンインサイトによると、パンデミックの最初の数か月間、公に知られているCDMOは10社未満でした。CDMOはワクチンの有効成分と主要な賦形剤の生産に従事していました。ワクチン生産能力の需要により、以前は古い製品やジェネリックに依存していた多くのCDMOの地位とプロファイルが高まりました。たとえば、Rovi Contract Manufacturingなどの一部の企業は、原薬と医薬品の両方の契約を結んでいます。

さらに、2021年上半期には、投資家が業界への参入を目指し、既存企業が自社の能力を拡大、深化させようとして、多数の合併・買収活動も見られました。 2021年の最初の5か月間で合計 32件の取引が発表または完了しました。このうち、5件の取引は低分子 APIビジネスに関するもので、4件は大分子 API資産に関するものでした。

CDMOへのアウトソーシングにより、企業は高度に専門化された専門家を含む柔軟な労働力へのアクセスを得ることができます。最近では、製薬会社からバイオ医薬品会社まで、中小企業から大企業まで、また初期段階から後期段階の開発プロジェクトまで、製薬会社によるCDMOへのアウトソーシングの増加が見られます。

APIの品質は、医薬品の有効性と安全性に顕著な影響を与えます。したがって、必要な強度、純度、品質で正確なAPIを提供できるCDMOを選択することは、医薬品開発会社にとって重要な決定です。

原薬CDMO市場動向

商業セグメントが主要な市場シェアを保持すると予想される

COVID-19のパンデミックにより医薬品の需要が増加し、生産中断を受けて一部の国が供給を買いだめしたことで輸出が増加しました。COVID-19の症例が急速に増加したとき、新しいCOVID-19のワクチンと治療薬が必要になりました。十分な量の治療薬が国内で生産されることを保証するために、一部の政府は現地化規制を検討し始めています。

その結果、多くの製薬会社が製造拠点を拡大し始め、一部の製薬会社は今後数年間の計画を立てるために製造拠点を再考し始めました。追加容量の最大の供給源はCDMOでした。

さらに、製薬会社は契約製造業者とかなりのスペースを予約し、場合によっては二重予約することもありました。アストラゼネカ、モデルナ、ファイザーは、Lonza、Catalent、Emergent Biosolutionsを含む多くのCDMOとパートナーシップ契約を結んだことを宣言しました。この機会を最大限に活用して、キャンブレックス、キャタレント、サムスンバイオロジクス、その他多くの発展途上国のCDMOは工場の大規模な拡張を宣言しました。

アジア太平洋は予測期間中に市場で大きなシェアを握ると予想される

中国とインドは米国や欧州と比べて製造コストが大幅に低いです。 Invest Indiaによると、インドでの製造コストは米国よりも約33%低いです。中国とインドはAPI製造サービスの重要なプロバイダーとしての地位を確立していますが、米国は引き続き医薬品開発の主要なアウトソーシングハブです。これは、巨額の資金調達と大学関連の製薬調査拠点の独占的集中の組み合わせによるものです。

従来の医薬品の重要性の拡大と持続性感染症の発生率の急速な増加は、インドのAPI CDMO市場の順調な成長の重要な推進力となっています。 2020年にPHRMABIZ.comに掲載された記事によると、ジェネリックAPIはインドから先進国に輸出されており、インドの総売上高の41.6%を占めるのに対し、中国では24.7%を占めています。 Chemical Pharmaceutical Generic Association調査によると、インドは米国市場へのジェネリック APIの2番目に大きなプロバイダーであり、24.4%のシェアを占めています。同国は西欧への供給も増やしており、同地域の総供給量の19.2%を占める。また、中国は世界の非独占的 APIベンダー市場の30%を占めています。中国に次いで、米国とインドが非独占的 APIの主要生産国です。

原薬CDMO業界の概要

原薬CDMO市場は細分化されており、いくつかの主要企業で構成されています。市場シェアの点では、少数の大手企業が市場を独占しています。そのうちのいくつかは、Cambrex Corporation、Patheon(Themo Fisher Scientific Inc.)、Recipharm AB、CordenPharma International、Samsung Biologics、Lonza、Siegfried、Piramal Pharma Solutions、Abbvie Inc.、Catalent Incです。

医薬品サプライチェーンにおけるAPIメーカーの役割は、顧客からの新たな要求と世界の競合他社からの増大する圧力に応えて進化しています。従来のジェネリック医薬品企業はバルク事業を中国とインドに求めている一方、特殊製薬企業は従来のジェネリック医薬品で必要とされる能力よりも専門的な能力に対する新たな需要を生み出しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 医薬品の研究開発投資の増加

- ジェネリック医薬品の需要の高まり

- 複雑な製造

- 特許の有効期限

- 市場抑制要因

- アウトソーシング時のコンプライアンス問題

- データの品質とセキュリティに関する懸念

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 分子の種類別

- 低分子

- 高分子

- 合成別

- バイオテクノロジー

- 合成

- 薬剤の種類別

- 革新的

- ジェネリック

- ワークフロー別

- 臨床

- 商業

- 用途別

- 心臓病

- 腫瘍学

- 眼科

- 神経内科

- 整形外科

- その他

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Cambrex Corporation

- Patheon(Thermo Fisher Scientific Inc.)

- Recipharm AB

- CordenPharma International

- Samsung Biologics

- Lonza

- Siegfried

- Piramal Pharma Solutions

- AbbVie Inc.

- Catalent Inc.

第7章 市場機会と将来の動向

The Global Active Pharmaceutical Ingredients CDMO Market size is estimated at USD 118.09 billion in 2024, and is expected to reach USD 178.47 billion by 2029, growing at a CAGR of 8.61% during the forecast period (2024-2029).

The COVID-19 pandemic had a huge impact on the API CDMO market. As the vaccines and therapeutics for the coronavirus were rolled out globally, the demand for CDMO services skyrocketed. CDMOs went to great lengths to meet the needs of their pharmaceutical customers during the crisis. CDMOs provide a broad range of services to pharmaceutical companies, such as drug development and supply chain, commercial API and drug manufacturing, and packaging. These services permit pharmaceutical firms to reduce their development and manufacturing costs, along with capital investments and timelines, while benefiting from the most advanced technologies.

For instance, in the first half of 2021, there was marked participation of CDMOs in COVID-19 vaccine manufacturing and robust merger acquisition activities. It also highlighted the indispensability of CDMOs in the bio/pharmaceutical industry. This has been vital to the successful launch of vaccines and therapies to combat the COVID-19 virus.

According to the Drug, Chemical & Associated Technologies Association Inc. (DCAT) Value Chain Insights on "Mid-Year CDMO Review: COVID-19 Vaccine Manufacturing and M&A", in the first months of the pandemic, less than 10 CDMOs were known publicly to be working with the bio/pharma companies and government agencies to develop and manufacture vaccines. Contracts were going to CDMOs that had the accessible capacity or could expand it rapidly, including Catalent and Lonza. CDMOs were engaged in producing the vaccine's active ingredients and key excipients. The demand for vaccine capacity elevated the status and profiles of many CDMOs that were earlier dependent on the older products and generics. Some companies, for instance, Rovi Contract Manufacturing, have got both drug substance and drug product contracts.

Besides, the first half of 2021 also saw a high number of merger and acquisition activities as investors sought to buy their way into the industry and incumbents sought to broaden and deepen their capabilities. A total of 32 deals were announced or closed during the first five months of 2021. Out of these, five deals were for small molecule API businesses and four for large molecule API assets.

Outsourcing to CDMOs can also offer companies access to a flexible workforce, including highly-specialized experts. In recent times, increased outsourcing to CDMOs has been seen for drug owners from pharmaceutical to biopharmaceutical companies, from small to large firms, and for early to late-stage development projects.

The quality of APIs has a noteworthy effect on the efficacy and safety of medications. Hence, selecting a CDMO that can provide the precise API at the required strength, purity, and quality is a vital decision for drug development companies.

Active Pharmaceutical Ingredients CDMO Market Trends

The Commercial Segment is Expected to Hold the Major Market Share

The COVID-19 pandemic led to an increase in the demand for pharmaceutical products, and the hoarding of supplies by some nations in the wake of production disruptions boosted exports. When COVID-19 cases rapidly increased, there was a need for new COVID-19 vaccines and therapeutics. Some governments even started considering localization regulations to ensure that sufficient quantities of therapeutics would be produced domestically.

As a result, many pharmaceutical companies started expanding their manufacturing footprint, and some began to rethink their manufacturing footprint to plan for the years ahead. The largest source of additional capacity was CDMOs.

Additionally, pharmaceutical firms reserved and sometimes even double-booked a considerable space with the contract manufacturers. AstraZeneca, Moderna, and Pfizer have declared their partnership agreements with a number of CDMOs, including Lonza, Catalent, and Emergent Biosolutions. Making the most of the opportunity, Cambrex, Catalent, Samsung Biologics, and many other developing country CDMOs have declared a major expansion of their plants.

Asia-Pacific is Expected to Hold a Significant Share in the Market during the Forecast Period

China and India have a significantly low cost of manufacturing compared to the United States and Europe. As per Invest India, the cost of manufacturing in India is approximately 33% lower than that of the United States. While China and India have established themselves as significant providers of API manufacturing services, the United States continues to be the main outsourcing hub for pharmaceutical development. This is due to the combination of enormous amounts of financing and an exclusive concentration of university-affiliated pharmaceutical research hubs.

The expanding importance of traditional pharmaceuticals and the rapidly rising incidence of persistent infections are critical drivers of the Indian API CDMO market's favorable growth. As per an article published in PHRMABIZ.com in 2020, generic APIs are exported to developed countries from India, accounting for 41.6% of the total sales in India versus 24.7% in China. As per the Chemical Pharmaceutical Generic Association Research, India is the second-largest provider of generic API to the US market, with a 24.4% share. The country is also increasing its supply to Western Europe, which accounts for 19.2% of the region's total supply. Also, China accounts for 30% of the global nonexclusive API vendor market. Following China, the United States and India are the leading producers of nonexclusive APIs.

Active Pharmaceutical Ingredients CDMO Industry Overview

The active pharmaceutical ingredients CDMO market is fragmented and consists of several major players. In terms of market share, a few major players dominate the market. A few of them are Cambrex Corporation, Patheon (Themo Fisher Scientific Inc.), Recipharm AB, CordenPharma International, Samsung Biologics, Lonza, Siegfried, Piramal Pharma Solutions, Abbvie Inc., and Catalent Inc.

The role of API manufacturers in the pharmaceutical supply chain is evolving in response to the newfound demands from customers and increasing pressures from global competitors. Traditional generic firms are looking to China and India for bulk activities, while specialty pharmaceutical companies have generated new demands for more specialized capabilities than those required by traditional generics.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Pharmaceutical R&D Investment

- 4.2.2 Rising Demand for Generic Drugs

- 4.2.3 Complex Manufacturing

- 4.2.4 Patent Expiration

- 4.3 Market Restraints

- 4.3.1 Compliance Issues while Outsourcing

- 4.3.2 Concerns about Data Quality and Security

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Molecule Type

- 5.1.1 Small Molecule

- 5.1.2 Large Molecule

- 5.2 By Synthesis

- 5.2.1 Biotech

- 5.2.2 Synthetic

- 5.3 By Drug Type

- 5.3.1 Innovative

- 5.3.2 Generics

- 5.4 By Workflow

- 5.4.1 Clinical

- 5.4.2 Commercial

- 5.5 By Application

- 5.5.1 Cardiology

- 5.5.2 Oncology

- 5.5.3 Ophthalmology

- 5.5.4 Neurology

- 5.5.5 Orthopedic

- 5.5.6 Other Applications

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Cambrex Corporation

- 6.1.2 Patheon (Thermo Fisher Scientific Inc.)

- 6.1.3 Recipharm AB

- 6.1.4 CordenPharma International

- 6.1.5 Samsung Biologics

- 6.1.6 Lonza

- 6.1.7 Siegfried

- 6.1.8 Piramal Pharma Solutions

- 6.1.9 AbbVie Inc.

- 6.1.10 Catalent Inc.