|

|

市場調査レポート

商品コード

1690731

真空遮断器:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Vacuum Interrupter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 真空遮断器:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 121 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

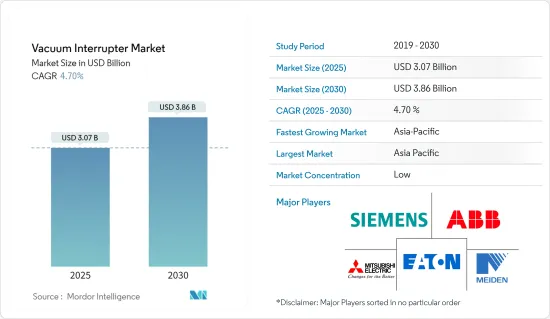

真空遮断器の市場規模は2025年に30億7,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは4.7%で、2030年には38億6,000万米ドルに達すると予測されます。

主なハイライト

- 安全・安心な配電への需要の高まりが、老朽化したインフラのアップグレードにつながり、真空遮断器市場の需要を押し上げています。また、技術の進歩により既存のインフラの近代化工事も増加しており、先進国、新興諸国ともに電力需要の増加に対応するためにインフラのアップグレードに多額の投資を行っています。さらに、エネルギー分野における環境問題や持続可能性に関する規制が、市場の成長をさらに後押ししています。

- 真空遮断器は環境に優しく、良質の材料で構成されており、メンテナンスや廃棄時の取り扱いも安全です。しかし、真空遮断器の製造には高度な技術が必要であり、市場成長の妨げとなっています。輸送中の損傷や故障は真空喪失の原因となり、インターラプタは使い物にならなくなり、現場での修理も不可能となります。さらに、高電圧用途の真空遮断器のコストが高いことも、市場の成長をさらに制限しています。

- こうした課題にもかかわらず、インダストリー4.0開発の触媒として作用するCOVID-19の大流行は、真空遮断器の技術革新をもたらし、高効率レベルでエネルギー消費を改善しました。世界の主要ベンダーは、真空遮断器のニーズの高まりに対応するため、製品の技術革新に取り組んでおり、電気流通業者もウェブサイトでこれらの新製品を紹介しています。

真空遮断器市場の動向

スマート電力網インフラの成長が市場を牽引

- 多くの国々で電力インフラは老朽化しており、本来設計された以上の性能を求められています。世界の発電・送電部門では、先進技術、機器、制御を駆使してグリッドをよりスマートで強靭なものにするため、グリッドの近代化が進んでいます。スマートグリッドは、より効率的かつ確実に電力を供給するために通信し、連携することができます。これらの送電網は、停電の期間と頻度を大幅に削減し、暴風雨の影響を軽減し、停電が発生した場合にサービスを迅速に復旧させることができます。

- 例えば、米国エネルギー省は数年前にグリッド近代化イニシアチブ(GMI)を立ち上げました。これは米国の送電網インフラの将来を形作るための包括的な取り組みです。

- 世界中の先進国・新興国政府は、スマートグリッド技術を、持続可能な長期的経済繁栄を可能にし、二酸化炭素排出削減目標の達成を支援する戦略的インフラ投資と見なすようになっています。この動向は、近い将来、スマートグリッドネットワーク市場に携わる企業にビジネスチャンスをもたらすと期待されています。

- 真空遮断技術は、反復スイッチング、故障保護、過電流、短絡保護に使用されるため、より大きな制御が可能です。このような制御は自動化され、より高い効率を実現します。

- さらに、より多くの再生可能エネルギー源や分散型エネルギー源がスマートグリッドに統合されるにつれて、需要と供給のバランスをとるために監視と測定が不可欠になります。真空遮断器産業は、重要なインフラの拡張とグリッドの自動化の増加に依存しています。したがって、スマートグリッドが市場成長を促進すると予想されます。

- さらに、米国エネルギー省は2022年9月、同国の電力網を強化するため、スマートグリッドやその他のアップグレードのための105億米ドルのプログラムを発表しました。送電網強靭化資金は、異常気象や自然災害による影響を軽減するために送電網を近代化する活動を支援する補助金の形で提供されます。

著しい成長を遂げるアジア太平洋地域

- アジア太平洋地域は、特にインド、日本、中国などの主要国において、発電所設置プロジェクトが大きく伸びています。しかし、同地域の多くの電力会社は、特に都市部における送電線敷設の新たな方法を獲得するという課題に直面しています。

- 電力容量を最適化し、再生可能エネルギーの統合を可能にするためには、新しい負荷開閉器を設置する必要があるが、ガス絶縁型はライフサイクルが長く、開閉器システムのサイズが小さいことから人気を集めています。この地域の国々が大規模な再生可能エネルギー・プロジェクトに注力するにつれ、さまざまなタイプの遮断器スイッチの中でもガス絶縁タイプの人気が高まると予想されます。

- 例えば、フィリピンは最近、第3回オープン・競合選定プロセス(OCSP3)の下で再生可能エネルギープロジェクトの申請を開始し、大規模な地熱探査・開発・利用プロジェクトに100%外国企業が参加できるようになりました。同様にインドネシアは、国営電力会社(PLN)の電力供給事業計画(RUPTL)草案によれば、2021年から2030年の間に、再生可能エネルギーを利用した新規発電所の割合を30%から48%に引き上げる計画です。

- この地域の変革が進むにつれて、分散型発電や公益事業のIT・分析市場への支出の増加とともに、スマートグリッドのロードマップが普及すると予想されます。インドには安定した電力供給が受けられない農村地域がいくつかあり、最近の電化イニシアチブは、こうした地域への電力供給を重視する傾向を強め、サーキットブレーカー・スイッチの需要に貢献すると予想されます。

- また、電力会社は、停電時に回路遮断スイッチやヒューズスイッチを開くために遠隔地を訪問する人員を確保できないため、主要課題として遠隔地へのグリッドアクセスを展開する必要に迫られています。遠隔地発電プロジェクトも回路開閉器市場の成長に寄与しています。

真空遮断器産業の概要

真空遮断器市場は競争が激しく、製品に多額の投資を行っている老舗企業が存在します。市場に新規参入するプレーヤーは、競争に打ち勝つために高額の投資を必要とします。企業は強力な競争戦略によって市場での地位を維持することができます。市場の主要企業には、Eaton Corporation PLC、Meidensha Corporation、三菱電機株式会社、Siemens AG、ABB、Shaanxi Baoguang Vacuum Electric Deviceなどがあります。これらの企業は、競争上の優位性を獲得するために、いくつかの拡大戦略にも取り組んでいます。

2023年2月、武漢飛特電器が生産した15.5KV、630A、31.5KAの真空遮断器と海外顧客の自動リクローザがオランダのKEMA研究所で行われた型式試験に合格しました。5.5KV、630A、31.5KAはFeite社のもう一つの真空遮断器で、有名な国際研究所の試験に合格しました。試験規格はIEC 62271-111:2019/IEEE Std C37.60:2018規格です。このような認証は、同社の製品に対する顧客の信頼を維持することになります。

2023年2月、ABBはELECRAMA 2023でConVac Hoover Contractorを発表し、電化事業とモーション事業のイノベーションを紹介しました。送電の安全性、インテリジェンス、持続可能性を確保するため、ABBの電化事業は、電柱からソケットに至るまで、幅広い電気機器、技術ソリューション、サービスを提供します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- スマート電力網インフラの成長

- 既存インフラの近代化とアップグレードの増加

- 市場抑制要因/課題

- 高電圧での過大なコスト

第6章 市場セグメンテーション

- 用途別

- サーキットブレーカー

- 接触器

- リクローザー

- ロードブレークスイッチ

- その他の用途

- 地域別

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- ラテンアメリカ

第7章 競合情勢

- 企業プロファイル

- Eaton Corporation PLC

- Meidensha Corporation

- Mitsubishi Electric Corporation

- Siemens AG

- ABB Ltd

- Wuhan Feite Electric Co. Ltd

- Toshiba Corporation

- Shaanxi Joyelectric International Co. Ltd

- Kirloskar Electric Company Ltd

- Zhejiang Xuhong Vacuum Electricappiliance Co. Ltd

第8章 市場機会と今後の動向

The Vacuum Interrupter Market size is estimated at USD 3.07 billion in 2025, and is expected to reach USD 3.86 billion by 2030, at a CAGR of 4.7% during the forecast period (2025-2030).

Key Highlights

- The increasing demand for safe and secure electrical distribution has led to the upgradation of outdated infrastructure, boosting the market demand for vacuum interrupters. Modernization work is also increasing in existing infrastructure due to technological advancements, with both developed and developing countries investing heavily in infrastructure upgrades to meet rising electricity demands. Additionally, environmental concerns and sustainability regulations in the energy sector are further driving the market growth.

- Vacuum interrupters are highly environmentally friendly, comprised of benign materials, and safe to handle during maintenance and disposal. However, the production of vacuum interrupters requires high technology, hindering the market growth. Transit damage or failure can cause a loss of vacuum, rendering the interrupter useless and impossible to repair on-site. Moreover, the high cost of vacuum interrupters for high-voltage applications further limits the market growth.

- Despite these challenges, the COVID-19 pandemic acting as a catalyst for Industry 4.0 developments led to innovations in vacuum interrupters, improving energy consumption with high-efficiency levels. Major global vendors are innovating their products, and electrical distributors are showcasing these new products on their websites to meet the growing need for vacuum interrupters.

Vacuum Interrupter Market Trends

Growth of Smart Electricity Grid Infrastructure to Drive the Market

- In many countries, electric infrastructure is aging, and it is being pushed to do more than it was originally designed for. Globally, the power generation and transmission sectors are witnessing a trend of modernizing the grid to make it smarter and more resilient using advanced technologies, equipment, and controls. Smart grids are able to communicate and work together to deliver electricity more efficiently and reliably. These grids can vastly reduce the duration and frequency of power outages, reduce storm impacts, and restore service at a faster rate when outages occur.

- For instance, the United States Department of Energy launched the Grid Modernization Initiative (GMI) a few years back. It is a comprehensive effort to help shape the future of the US grid infrastructure.

- Governments of both developed and emerging countries across the world are increasingly seeing smart grid technology as a strategic infrastructural investment that will enable sustainable long-term economic prosperity and aid them in achieving carbon emission reduction targets. This trend is expected to provide opportunities to the companies involved in the smart grid network market in the near future.

- Vacuum interrupter technology is used for repetitive switching, fault protection, overcurrent, and short-circuit protection; hence, it allows greater control. Such controls are automated for greater efficiency.

- Moreover, as more renewable and distributed energy sources are integrated into smart grids, monitoring and measurement become essential to balancing supply and demand. The vacuum interrupter industry depends on the extension of crucial infrastructures and the increase in grid automation. Therefore, smart grids are expected to drive market growth.

- Moreover, in September 2022, the US Department of Energy announced a USD 10.5 billion program for smart grids and other upgrades to strengthen the country's electricity grid. The grid resilience funding will be in the form of grants to support activities to modernize the grid to reduce the impacts due to extreme weather and natural disasters.

Asia-Pacific to Witness Significant Growth

- The Asia-Pacific region has experienced significant growth in power plant installation projects, particularly in major countries such as India, Japan, and China. However, many utilities in the region are facing challenges in acquiring new ways to install transmission lines, especially within urban areas.

- To optimize power capacity and enable the integration of renewable energy, new load break switches need to be installed, with the gas-insulated type gaining popularity due to its longer life cycles and smaller size of the switchgear system. As countries in the region focus on large-scale renewable energy projects, the gas-insulated type is expected to grow in popularity among the different types of circuit breaker switches.

- For example, the Philippines recently opened applications for renewable energy projects under the third Open and Competitive Selection Process (OCSP3), allowing for 100% foreign participation in large-scale geothermal exploration, development, and utilization projects. Similarly, Indonesia plans to increase the portion of new and renewable energy-based power plants from 30% to 48% within 2021-2030, according to a draft electric power supply business plan (RUPTL) of the state electricity company (PLN).

- As the region's transformation continues, smart grid roadmaps are expected to become more popular, along with increased spending in distributed generation and utility IT and analytics markets. The presence of several rural areas in India without a stable power supply and recent electrification initiatives are expected to increase the emphasis on providing power to these areas, contributing to the demand for circuit breaker switches.

- In addition, utilities face pressure to deploy remote grid access as a major agenda, as they cannot afford personnel to visit remote sites to open circuit break switches and fuse switches during outages. Remote power generation projects also contribute to the growth of the circuit switch markets.

Vacuum Interrupter Industry Overview

The vacuum interrupter market is highly competitive, with well-established players who have invested significantly in the product. New players entering the market require high investments to compete. Companies can sustain their position in the market through powerful competitive strategies. Some of the leading companies in the market include Eaton Corporation PLC, Meidensha Corporation, Mitsubishi Electric Corporation, Siemens AG, ABB, Shaanxi Baoguang Vacuum Electric Device Co., Ltd., and many others. These companies are also involved in several expansion strategies to gain a competitive advantage.

In February 2023, the 15.5 KV, 630 A, 31.5 KA vacuum interrupter produced by Wuhan Feite Electric Co. Ltd with the automatic recloser of overseas customers passed the type test in KEMA Laboratories in the Netherlands. 5.5 KV, 630 A, 31.5 KA is another vacuum interrupter from Feite company that has passed the test in the famous international laboratory. The test standard is IEC 62271-111: 2019/IEEE Std C37.60:2018 standard. Such type of certification would maintain the customer's trust in the company's products.

In February 2023, ABB introduced the ConVac Hoover Contractor at ELECRAMA 2023, showcasing innovations from its Electrification and Motion businesses. In order to ensure the safety, intelligence, and sustainability of electricity transmission, ABB's Electrification will offer a wide range of electrical equipment, technology solutions, and services ranging from poles to sockets.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Buyers

- 4.3.2 Bargaining Power of Suppliers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes of Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth of Smart Electricity Grid Infrastructure

- 5.1.2 Increasing Modernization and Upgrading of Existing Infrastructure

- 5.2 Market Restraint/Challenge

- 5.2.1 Excessive Cost at Higher Voltage

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Circuit Breaker

- 6.1.2 Contactor

- 6.1.3 Recloser

- 6.1.4 Load Break Switch

- 6.1.5 Other Applications

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia Pacific

- 6.2.4 Middle East and Africa

- 6.2.5 Latin America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Eaton Corporation PLC

- 7.1.2 Meidensha Corporation

- 7.1.3 Mitsubishi Electric Corporation

- 7.1.4 Siemens AG

- 7.1.5 ABB Ltd

- 7.1.6 Wuhan Feite Electric Co. Ltd

- 7.1.7 Toshiba Corporation

- 7.1.8 Shaanxi Joyelectric International Co. Ltd

- 7.1.9 Kirloskar Electric Company Ltd

- 7.1.10 Zhejiang Xuhong Vacuum Electricappiliance Co. Ltd