|

市場調査レポート

商品コード

1444905

医療画像管理: 市場シェア分析、業界動向と統計、成長予測(2024年~2029年)Medical Imaging Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 医療画像管理: 市場シェア分析、業界動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 114 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

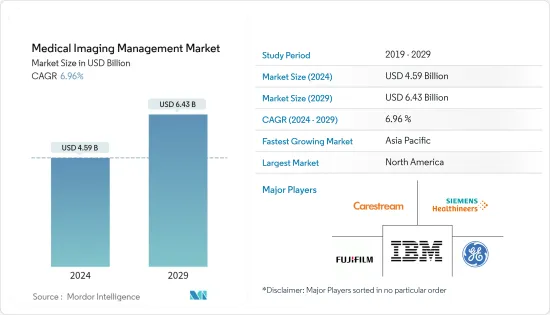

医療画像管理市場規模は、2024年に45億9,000万米ドルと推定され、2029年までに64億3,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に6.96%のCAGRで成長します。

COVID-19は、パンデミック期間中の市場の成長に大きな影響を与えました。これは主に、COVID-19感染症の診断における医用画像の需要が高く、それが医療画像管理の需要に影響を与えたためです。たとえば、2021年 5月に発行された欧州 PMCの記事では、医療画像がCOVID-19感染症の診断、管理、疾患進行監視において重要な役割を果たしていると述べられています。報告書はまた、胸部X線撮影とコンピューター断層撮影がパンデミック中に世界中で一般的に使用されている画像技術であるとも述べた。このように、COVID-19感染症の流行は、病気の診断のための医用画像処理と管理の利用が増加したため、医療画像管理に顕著な影響を及ぼしました。さらに、SARS-CoV-2の変異株の出現と効果的な診断と管理に対する需要の高まりにより、医療画像管理の需要は維持されると予想され、それが市場の成長に貢献します。

高齢者人口の増加は、世界人口における慢性疾患の有病率の上昇と相まって、医療画像管理の需要を促進し、それによって市場の成長を推進すると予想されます。

たとえば、2022年 1月に発表された英国心臓財団(BHF)のデータによると、2021年に世界中で影響を受けた最も一般的な心臓病は、冠状動脈(虚血性)心疾患(世界有病率は2億人と推定)、末梢動脈(血管)疾患(1億1,000万人)、脳卒中(1億人)、心房細動(6,000万人)。この報告書はまた、北米での心臓および循環器疾患の有病者数が4,600万人、欧州で9,900万人、アフリカで5,800万人、南米で3,200万人、アジアとオーストラリアで3億1,000万人であると述べた。 2022年 2月に発表された世界保健機関のファクトシートによると、2021年に米国で新たにがんと診断された患者数は推定190万人でした。報告書はまた、世界中で毎年約40万人の子供ががんを発症していることにも言及しました。子宮頸がんは、エスワティニ、インド、南アフリカ、ラテンアメリカなどの23か国で最も一般的です。世界人口におけるこのようなさまざまな慢性疾患の有病率の増加により、効果的な医療画像処理の需要が高まり、それによって市場の成長が促進されると予想されます。

さらに、国連が2022年に発表した報告書では、世界人口に占める65歳以上の人口の割合が2022年の10%から2050年には16%に上昇すると予測されていると述べています。慢性疾患を発症しやすい高齢者人口はこのように増加しています。また、医療画像管理の需要も高まり、それによって市場の成長が促進されると予想されます。

一方で、さまざまな主要市場企業による製品開発の増加も市場の成長に貢献すると予想されます。たとえば、2021年 8月にRamSoftは、ヘルスケア企業全体で画像と画像データのシームレスな交換を可能にするベンダー中立のアーカイブであるOmega AI VNAを立ち上げました。 Omega AI VNAは、あらゆるシステムからの画像とデータを統合し、臨床医が患者の病歴の全体像を確認できるようにします。

ただし、医療画像管理ソリューションの実装に関連するコストや、放射性同位元素の不足によるSPECTおよびPETシステムの供給の減少などの要因により、予測期間中の市場の成長が抑制されると予想されます。

医療画像管理市場動向

画像アーカイブおよび通信システム(PACS)は、予測期間中に市場で顕著なCAGRで推移すると予想されます

画像アーカイブおよび通信システム(PACS)は、主にヘルスケア機関で電子画像や臨床関連レポートを安全に保存し、デジタル送信するために使用される医療画像技術です。 PACSを使用すると、機密情報、フィルム、レポートを手動でファイルして保存、取得、送信する必要がなくなります。代わりに、医療文書と画像はオフサイトのサーバーに安全に保管され、PACSソフトウェア、ワークステーション、モバイルデバイスを使用して基本的に世界中のどこからでも安全にアクセスできます。

ヘルスケアにおける技術的に高度なソリューションの使用の増加、電子医療記録の使用の増加、慢性疾患の有病率の上昇、PACSの発売などの要因が、予測期間中に市場セグメントの成長を推進しています。また、PACSの有効性を実証する研究により、将来的にはその使用が拡大し、市場の成長が促進されると予想されます。たとえば、2021年 3月に発行されたJournal of Multidisciplinaryヘルスケアの記事では、PACSが臨床医の効率を高め、診断の有効性を高め、放射線科レポートの平均所要時間を短縮することが示されたと報告しています。また、複数の場所からPACS画像とレポートにアクセスすることで、臨床医の迅速かつ適切な意思決定が可能になり、患者情報の正確性、関連性、タイムリー性が向上して患者情報の質が向上し、患者ケアプロセスの継続性が向上すると報告しました。したがって、PACSの使用はワークフローを維持する効果的な方法です。 PACSの利点を実証するこのような研究は需要を促進し、それによって研究分野の成長に貢献すると予想されます。

慢性疾患の有病率の増加も、効果的な医療画像管理のためのPACSの成長に貢献すると予想されます。たとえば、国立乳がん財団によると、2022年 6月に発表されたデータによると、2022年には米国の女性で推定287,500人の新たな浸潤性乳がん症例が診断され、同様に51,400人の新たな非浸潤性乳がん症例が診断されるとのことです。浸潤性乳がん。この報告書はまた、2022年に米国で推定2,170人の男性が乳がんと診断されると述べています。このようながんの有病率の増加により、効果的な診断手順や医用画像処理のためのPACSの需要が高まり、研究分野の成長が促進されると予想されます。

また、さまざまな主要市場企業による高度な製品開発の増加も、調査対象セグメントの成長に貢献すると予想されます。たとえば、2021年 11月、GEヘルスケアは、ヘルスケア機関が急速に進化するテクノロジーに常に対応できるよう支援することを目的として、次世代のクラウドベースの画像アーカイブおよび通信システム(PACS)を開発しました。 Edison True PACS1と呼ばれるサブスクリプションベースの画像診断ソリューションには、読影、検査ワークフロー、AIアプリケーション、3D後処理、エンタープライズビジュアライゼーション、アーカイブが1つのプラットフォームに含まれています。

したがって、慢性疾患の有病率の上昇、高度な製品開発に伴うPACSの需要の増加が、調査対象のセグメントの成長を促進すると予想されます。

北米は予測期間中に市場でかなりのシェアを保持すると予想される

北米では、医療画像アーカイブの汎用化、データストレージコストの削減、VNAと古いデータアーカイブシステムとの互換性などの需要の増加により、有利な成長が見込まれています。

また、北米での医療画像管理の臨床使用の開始により、その需要が増加しており、市場の成長を推進しています。たとえば、2021年 11月にChangeヘルスケアは、同社のStratus Imaging PACSが臨床で使用されていると報告しました。これは、クラウドネイティブでフットプリントがゼロの画像アーカイブおよび通信システムです。このスケーラブルなクラウドネイティブプラットフォームは、米国のStatRadによって使用されています。このような医療画像管理システムの使用の開始も、この地域で調査対象となっている市場の成長を推進しています。

さらに、市場関係者とサービスプロバイダー間のパートナーシップにより、イメージング機能とワークフローが容易になり、市場の成長が促進されます。たとえば、2022年 4月、Sectraはカナダのノースヨーク総合病院(NYGH)と契約を締結しました。 NYGHは、Sectraのエンタープライズ画像ソリューションの放射線学および乳房画像モジュールとベンダー中立アーカイブ(VNA)を利用して、画像をレビューおよび保存します。これにより、NYGHは放射線読影の効率を高め、現在のワークフローを強化して、スタッフの仕事量を増やすことなく、より多くのことを行うことで患者ケアを改善できるようになります。同様に、2021年 1月、Canadian Teleradiology Services, Inc.(CTS)は、RamSoftのクラウド Power Server PACSと連携して、クライアントの病院にリモート放射線学サービスを提供しました。 CTSはLevel Jumpヘルスケア Corpの子会社です。

さらに、高度な製品のマーケティング、使用、開発のための合併、買収、パートナーシップなど、市場関係者がとった戦略的取り組みも市場の成長を推進しています。たとえば、2022年 4月に、ロイヤルフィリップスとプリズマヘルス、およびサウスカロライナ州最大の非営利ヘルスケアシステムの1つが、医療システムが企業の相互運用性を実現し、患者のモニタリングを標準化し、企業画像処理の革新を促進することを目的とした複数年契約を締結しました。患者ケアを強化し、臨床パフォーマンスを向上させるソリューション。合意に従い、企業は企業全体でヘルスケアを革新し、患者データの力を解き放つことになります。

したがって、北米における主要な市場企業と先進的なヘルスケアインフラの存在に加え、先進的な製品の発売の増加が、この地域の市場の成長に貢献すると予想されます。

医療画像管理業界の概要

医療画像管理市場は適度な競争があり、世界の企業によって大部分が支配されています。主要な市場企業には、Carestream Health, Inc.、富士フイルムホールディングス株式会社、IBM Corporation、Siemens Healthineers、GEヘルスケアなどが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 画像診断と画像管理における技術革新

- 慢性疾患の有病率の上昇

- ヘルスケアにおけるビッグデータの出現

- 市場抑制要因

- 医療画像管理ソリューションの導入に関連するコスト

- 放射性同位元素不足によるSPECT・PET装置の供給減少

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- システム別

- ベンダー中立のアーカイブ

- 画像アーカイブおよび通信システム(PACS)

- その他のシステム

- エンドユーザー別

- 病院

- 診断センター

- 外来手術センター

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Agfa-Gevaert Group

- BridgeHead Software

- Carestream Health Inc.(Onex Corporation)

- Fujifilm Holdings Corporation

- GE Healthcare

- IBM Corporation

- Novarad Corporation

- Koninklijke Philips NV

- Siemens Healthineers

- Lexmark International Inc.

- McKesson Corporation

- Dell Technologies Inc.

第7章 市場機会と将来の動向

The Medical Imaging Management Market size is estimated at USD 4.59 billion in 2024, and is expected to reach USD 6.43 billion by 2029, growing at a CAGR of 6.96% during the forecast period (2024-2029).

COVID-19 had a significant impact on the growth of the market over the pandemic period. This was mainly due to the high demand for medical imaging in the diagnosis of COVID-19, which in turn impacted the demand for medical imaging management. For instance, the Europe PMC article published in May 2021 mentioned that medical imaging played an essential role in the diagnosis, management, and disease progression surveillance of COVID-19 disease. The report also mentioned that chest radiography and computed tomography are commonly used imaging techniques globally during the pandemic. Thus, the COVID-19 outbreak had a notable impact on medical imaging management owing to the increased usage of medical imaging and management for the diagnosis of the disease. In addition, the demand for medical imaging management is expected to remain intact due to the emergence of mutant strains of SARS-CoV-2 and the rising demand for effective diagnosis and management, thereby contributing to the market's growth.

The increasing geriatric population, coupled with the rising prevalence of chronic diseases among the global population, is expected to drive the demand for medical imaging management, thereby propelling the market's growth.

For instance, the British Heart Foundation (BHF) data published in January 2022 reported that in 2021, the most common heart conditions affected globally were coronary (ischemic) heart disease (global prevalence estimated at 200 million), peripheral arterial (vascular) disease (110 million), stroke (100 million) and atrial fibrillation (60 million). The report also mentioned that the prevalence of heart and circulatory diseases in North America was 46 million, in Europe 99 million, in Africa 58 million, in South America 32 million, in Asia and Australia 310 million. As per the World Health Organization factsheet published in February 2022, in 2021, there were an estimated 1.9 million new cancer cases diagnosed in the United States. The report also mentioned that each year, approximately 400,000 children develop cancer globally. Cervical cancer is the most common in 23 countries, such as Eswatini, India, South Africa, Latin America, and others. Such increasing prevalence of various chronic diseases among the global population is expected to drive the demand for effective medical imaging, thereby driving the growth of the market.

Additionally, the report published by the UN in 2022 mentioned that the share of the global population aged 65 years or above is projected to rise from 10% in 2022 to 16% in 2050. Such an increasing geriatric population who are susceptible to developing chronic disorders is also expected to boost the demand for medical imaging management, thereby propelling the growth of the market.

On the other hand, the increasing product developments by various key market players are also expected to contribute to the market's growth. For instance, in August 2021, RamSoft, launched Omega AI VNA, a vendor-neutral archive that enables the seamless exchange of images and imaging data across healthcare enterprises. Omega AI VNA consolidates images and data from any system to allow clinicians to see the complete picture of a patient's medical history.

However, factors such as the cost associated with the implementation of medical imaging management solutions and a decrease in the supply of SPECT and PET systems due to the shortage of radioisotopes are expected to restrain the growth of the market over the forecast period.

Medical Image Management Market Trends

Picture Archiving and Communications Systems (PACS) is Expected to Record Notable CAGR in the Market During the Forecast Period

Picture Archiving and Communication Systems (PACS) is a medical imaging technology used primarily in healthcare organizations to securely store and digitally transmit electronic images and clinically-relevant reports. The use of PACS eliminates the need to manually file and store, retrieve, and send sensitive information, films, and reports. Instead, medical documentation and images can be securely housed in off-site servers and safely accessed essentially from anywhere in the world using PACS software, workstations, and mobile devices.

Factors such as the increasing usage of technologically advanced solutions in healthcare, increased usage of electronic health records, rising prevalence of chronic diseases, and the launch of PACS are propelling the growth of the market segment over the forecast period. Also, the studies demonstrating the effectiveness of the PACS are expected to augment its usage in the future and thus propel the growth of the market. For instance, the Journal of Multidisciplinary Healthcare article published in March 2021 reported that PACS had been shown to increase clinicians' efficiency, enhance diagnostic efficacy, and shorten the average turnaround time for radiology reports. It also reported that access to PACS images and reports from multiple locations allows immediate and better clinician decision-making and increases the quality of patient information by making it more accurate, relevant, and timely, improving the continuity of the patient care process. Thus, the use of PACS is an effective way of maintaining workflow. Such studies demonstrating the advantages of PACS are expected to drive the demand, thereby contributing to the growth of the studied segment.

The increasing prevalence of chronic diseases is also expected to contribute to the growth of the PACS for effective medical image management. For instance, as per the National Breast Cancer Foundation Inc., data published in June 2022 mentioned that in 2022, an estimated 287,500 new cases of invasive breast cancer is diagnosed in women in the United States and as well as 51,400 new cases of non-invasive breast cancer. The report also mentioned that an estimated 2,170 men are diagnosed with breast cancer in 2022 in the United States. Such increasing prevalence of cancer is expected to drive the demand for PACS for effective diagnostic procedures and medical imaging, thereby fueling the growth of the studied segment.

Also, the increasing advanced product developments by various key market players are expected to contribute to the growth of the studied segment. For instance, in November 2021, GE Healthcare developed a next-generation, cloud-based Picture Archiving and Communication System (PACS) aiming to help healthcare organizations keep current with rapidly evolving technology. The subscription-based diagnostic imaging solution called Edison True PACS1 encompasses diagnostic reading, exam workflow, AI Applications, 3D post-processing, enterprise visualization, and archiving in a single platform.

Thus, the rising prevalence of chronic diseases, increasing demand for PACS along with advanced product developments are expected to fuel the studied segment growth.

North America is Expected to Hold Significant Share in the Market over the Forecast Period

North America is expected to show lucrative growth owing to the factors such as increasing demand for the Universalization of medical image archiving, reducing data storage costs, and compatibility of VNA with older data archival systems.

Also, the initiation of the clinical use of medical imaging management in North America is increasing the demand for it and thus driving the market's growth. For instance, in November 2021, Change Healthcare reported that its Stratus Imaging PACS was live in clinical use. It is a cloud-native, zero-footprint Picture Archiving and Communication System. This scalable, cloud-native platform is used by StatRad in the United States. Such initiation of the use of medical imaging management systems is also propelling the growth of the studied market in this region.

Furthermore, the partnership among the market players and service providers to ease the imaging capabilities and workflow bolsters the market's growth. For instance, in April 2022, Sectra signed a contract with North York General Hospital (NYGH) in Canada. NYGH will utilize the radiology and breast imaging modules and vendor-neutral archive (VNA) of Sectra's enterprise imaging solution to review and store images. This will enable NYGH to boost radiology reading efficiency and enhance current workflows to improve patient care by doing more without increasing the workload on staff. Similarly, in January 2021, Canadian Teleradiology Services, Inc. (CTS) collaborated with RamSoft's cloud Power Server PACS to provide remote radiology services to their client hospitals. CTS is a subsidiary of Level jump Healthcare Corp.

Additionally, the strategic initiatives taken by the market players, such as mergers, acquisitions, and partnerships for the marketing, usage, or development of advanced products, are also driving the market's growth. For instance, in April 2022, Royal Philips and Prisma Health and South Carolina's one of largest non-profit healthcare systems, entered into a multi-year agreement to help the health system achieve enterprise interoperability, standardize patient monitoring, and drive innovation in enterprise imaging solutions to enhance patient care and improve clinical performance. As per the agreement, companies will innovate healthcare across the enterprise and unlock the power of patient data.

Thus, the increasing launches of advanced products, along with the presence of key market players and advanced healthcare infrastructure in North America, is expected to contribute to the growth of the market in this region.

Medical Image Management Industry Overview

The Medical Imaging Management Market is moderately competitive and is majorly dominated by global players. Some of the major market players include Carestream Health, Inc., Fujifilm Holdings Corporation, IBM Corporation, Siemens Healthineers, GE Healthcare, and others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Technological Innovations in the Diagnostic Imaging and Image Management

- 4.2.2 Rising Prevalence of Chronic Diseases

- 4.2.3 Emergence of Big Data in Healthcare

- 4.3 Market Restraints

- 4.3.1 Cost Associated With Implementation of Medical Imaging Management Solutions

- 4.3.2 Decrease In the Supply of SPECT and PET Systems due to the Shortage of Radioisotopes

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By System

- 5.1.1 Vendor Neutral Archive

- 5.1.2 Picture Archiving and Communications System (PACS)

- 5.1.3 Other Systems

- 5.2 By End-User

- 5.2.1 Hospitals

- 5.2.2 Diagnostic Centers

- 5.2.3 Ambulatory Surgery Centers

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Agfa-Gevaert Group

- 6.1.2 BridgeHead Software

- 6.1.3 Carestream Health Inc. (Onex Corporation)

- 6.1.4 Fujifilm Holdings Corporation

- 6.1.5 GE Healthcare

- 6.1.6 IBM Corporation

- 6.1.7 Novarad Corporation

- 6.1.8 Koninklijke Philips NV

- 6.1.9 Siemens Healthineers

- 6.1.10 Lexmark International Inc.

- 6.1.11 McKesson Corporation

- 6.1.12 Dell Technologies Inc.