|

|

市場調査レポート

商品コード

1444845

戦闘機の世界市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Fighter Aircraft - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 戦闘機の世界市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 107 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

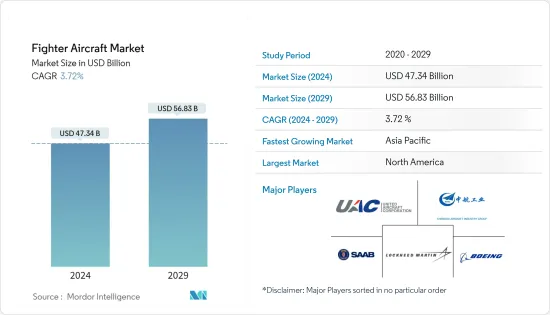

世界の戦闘機の市場規模は、2024年に473億4,000万米ドルと推定され、2029年には568億3,000万米ドルに達し、予測期間中(2024年~2029年)にCAGR3.72%で成長すると予測されています。

主なハイライト

- COVID-19のパンデミックは戦闘機市場に悪影響を及ぼし、納入と生産に影響を及ぼしました。ウイルスの蔓延を抑えることを目的とした厳しい規制により、各国への戦闘機の納入に遅れが生じました。さらに、パンデミックによりさまざまな企業で一時解雇が発生し、生産プロセスが妨げられました。しかし、パンデミックの沈静化に伴い、制限が緩和され、世界中で戦闘機の生産と納入が増加したことにより、市場は成長を遂げました。

- 国家間の地政学的な緊張の高まりにより、既存の艦隊を近代化し、防空能力を強化するために先進的な戦闘機の導入が促されています。各国が戦闘能力を最新の状態に保つよう努める中、ステルス兵器や精密兵器などの技術の進歩が戦闘機市場の発展をさらに支援しています。

- しかし、特に新興諸国では、次世代戦闘機への投資ではなく既存の古い戦闘機のアップグレードを選択してコストを削減する可能性があるため、予算の制約が市場の成長を妨げる可能性があります。

戦闘機市場動向

離着陸セグメントでは従来型離着陸に予測期間中の大幅な成長が見込まれる

- 従来型離着陸セグメントは、武器や装備品のより高い積載能力とより広い戦闘範囲を搭載できるため、予測期間中に大幅な成長が見込まれています。この成長は、中国のJ-20、Su-37、Mig-35、Su57、および老朽化した第4世代戦闘機を第4.5世代、第5世代、第6世代航空機に置き換えるインドのTejasMK2などの新しい戦闘機プログラムの開発によって促進されると予想されます。

- さらに、各国は航空機の能力を向上させ、寿命を延ばすために、F-16、F-15、F/A-18などの近代化プログラムに取り組んでいます。世界中の一部の主要国も、軍艦の老朽化に関する懸念に対処するため、新しい戦闘機の調達を計画しているか、調達を開始しています。

- たとえば、ブラジル空軍は2022年4月、47億米ドルの契約の一環として2014年に購入した36機に加えて、サーブ・エンブラエルF-39Eジェット機4機を発注しました。同国はまた、グリペンNG航空機の現地指定を伴う少なくとも30機のF-39E戦闘機の別のバッチを発注することも検討しています。

- さらに、技術の急速な進歩に伴い、各国は次世代輸送機の調達などにより航空部隊支援能力の強化に努めています。その結果、航空機製造会社と契約を締結しています。たとえば、2021年6月、エアバスはアジア太平洋の非公開国とC-295輸送機の契約を獲得したと報じられました。これらの開発は、予測期間中の従来型離着陸航空機の前向きな見通しに貢献すると予想されます。

北米は予測期間中に大幅な成長が見込まれる

北米は、予測期間中に大幅な成長が見込まれると予想されます。米国の軍事支出は、2020年の7,782億3,000万米ドルから2021年にはほぼ2.9%増加し、8,010億米ドルに達しました。米国は2021年も依然として最大の国防支出国であり、世界支出の38%を占めています。

さらに、米国空軍は、新世代ジェット機の納入に伴い、航空機の老朽化問題に徐々に取り組んでいます。在庫が減少するにつれて、航空機の平均使用年数は過去10年間で増加しました。米国空軍の艦隊の平均年齢は25年を超え、爆撃機の平均年齢は50歳を超えています。さらに、米国国防総省は戦闘機の契約を締結しています。例えば、2022年7月、米国国防総省はロッキード・マーティン社と共同で、3年間で約375機のF-35戦闘機を製造することを約束しています。さらに、国防総省によれば、この協定の対象となる航空機の最終数は、米国議会による2023会計年度予算の変更や外国パートナーによる発注に応じて変更される可能性があります。

固定翼輸送機とは別に、米国軍は多用途ヘリコプターの部隊も近代化しています。米国海軍はCMV-22Bオスプレイの納入を開始しており、2024年までにすべてのC-2航空機を退役させる計画です。米国海軍と海兵隊はここ数年、オスプレイを発注しています。さらに、2022年6月には、米国からH-60Mブラックホークヘリコプター120機の調達と2022年から2026年度の関連支援として、ストラットフォードのシコルスキー・エアクラフト社に22億7,000万米ドルの契約が締結されました。、追加の135機の航空機のオプションがあります。

したがって、そのような開発が、予測期間中の戦闘機を大幅に増加させることにつながります。

戦闘機業界の概要

航空宇宙および防衛産業には、ロッキード・マーチン社、ボーイング社、ユナイテッド・エアクラフト・コーポレーション、成都航空機産業(グループ)、サーブABなど、いくつかの大手企業が存在します。しかし、ロッキード・マーチン社は、F-35戦闘機の納入量が多いため、市場で重要な地位を占めています。同社の継続的な研究開発努力は、空挺部隊、地上部隊、敵対的な海軍部隊と交戦し無力化するための優れた能力を提供する高性能戦闘機と技術の開発に重点を置いた同社の市場支配力をさらに強化しています。

ロッキード・マーチン社の広範な製品ポートフォリオは、いくつかのバリエーションと継続的な製品開発サイクルを特徴としており、航空資産の運用寿命の延長を可能にします。この堅牢な研究開発フレームワークは、航空資産のより高い性能の信頼性とアップグレードの可能性を求める潜在的な購入者も魅了しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

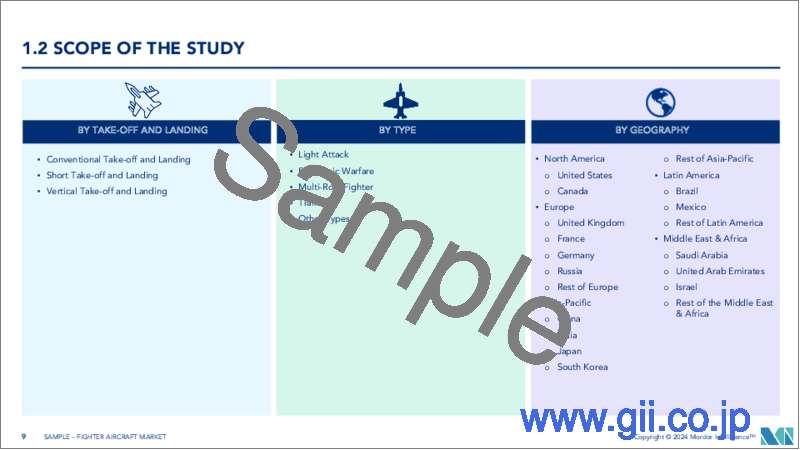

第5章 市場セグメンテーション

- 離着陸

- 従来型離着陸

- 短距離離着陸

- 垂直離着陸

- タイプ

- 弱攻撃

- 電子戦

- マルチロール戦闘機

- 訓練機

- その他のタイプ

- 地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東とアフリカ

- アラブ首長国連邦

- サウジアラビア

- エジプト

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- Lockheed Martin Corporation

- Saab AB

- The Boeing Company

- Airbus SE

- United Aircraft Corporation

- Chengdu Aircraft Industrial(Group)Co. Ltd

- Hindustan Aeronautics Limited

- BAE Systems PLC

- Dassault Aviation SA

- Mitsubishi Heavy Industries

- Aero Vodochody Aerospace AS

- Embraer SA

- Textron Aviation(Textron Systems)

- Korea Aerospace Industries

- Turkish Aerospace Industries

第7章 市場機会と将来の動向

The Fighter Aircraft Market size is estimated at USD 47.34 billion in 2024, and is expected to reach USD 56.83 billion by 2029, growing at a CAGR of 3.72% during the forecast period (2024-2029).

Key Highlights

- The COVID-19 pandemic negatively impacted the fighter aircraft market, affecting delivery and production. Stringent regulations aimed at reducing the spread of the virus caused delays in the delivery of fighter aircraft to various countries. Furthermore, the pandemic led to layoffs in various companies, hampering the production process. However, with the decline in the pandemic, the market witnessed growth due to the ease in restrictions and increased production and delivery of fighter aircraft worldwide.

- The growing geopolitical tensions between nations have prompted the adoption of advanced fighter aircraft to modernize existing fleets and enhance their aerial defense capabilities. Advancements in technology, such as stealth and precision weapons, are further supporting the development of the fighter aircraft market as nations strive to keep their combat capabilities up-to-date.

- However, budget constraints may hinder market growth, particularly for developing countries that may opt for upgrading existing old fighters to cut costs rather than investing in next-generation fighter jets.

Fighter Aircraft Market Trends

By Take-Off and Landing Segmentation, the Conventional Take-Off and Landing is Expected to Witness Significant Growth During the Forecast Period

- The conventional take-off and landing segment is expected to experience significant growth during the forecast period due to its ability to carry a higher payload capacity for weapons and equipment, as well as its greater battle range. This growth is anticipated to be fueled by the development of new fighter aircraft programs such as China's J-20, Su-37, Mig-35, Su57, and India's TejasMK2, which will replace aging fourth-generation fighter aircraft with 4.5th, 5th, and 6th generation aircraft.

- Additionally, countries are engaging in modernization programs such as the F-16, F-15, and F/A-18 to improve aircraft capabilities and life extension. Some prominent countries across the globe are also planning or have started procuring new fighter aircraft to address concerns about their aging military fleets.

- For example, in April 2022, the Brazilian air force ordered four Saab-Embraer F-39E jets in addition to the 36 purchased in 2014 as part of a USD 4.7 billion contract. The country is also considering ordering another batch of at least 30 F-39E fighters with a local designation of Gripen NG aircraft.

- Furthermore, with the rapid advancement of technology, countries are striving to enhance their aerial troop support capabilities by procuring next-generation transport aircraft. As a result, they are awarding contracts to aircraft manufacturing companies. For instance, in June 2021, Airbus reportedly secured a contract with an undisclosed nation in the Asia-Pacific region for its C-295 transport aircraft. These developments are expected to contribute to a positive outlook for conventional take-off and landing aircraft during the forecast period.

The Region of North America is Expected to Witness Significant Growth During the Forecast Period

The region of North America is expected to witness significant growth during the forecast period. The United States military expenditure increased by almost 2.9% in 2021 to reach USD 801 billion from USD 778.23 billion in 2020. The United States remained the largest defense-spending country in 2021 and represented 38% of global spending.

Moreover, the United States Air Force is gradually addressing its aging aircraft problem, as it takes delivery of newer generation jets. As inventories decreased, the average aircraft age increased over the past decade. The average age of the United States Air Force fleet is over 25 years, and bombers have an average age of over 50 years. Moreover, the United States Department of Defense is awarding contracts for fighter aircraft. For instance, in July 2022, The United States Department of Defense is committed to manufacturing around 375 F-35 fighter jets over a three-year period With Lockheed Martin Corp. Additionally, according to the Pentagon, the final number of aircraft covered by this agreement could change depending on any alterations made by the United States Congress to the budget for the Fiscal Year 2023 and any orders put in by foreign partners.

Apart from the fixed-wing transport aircraft, the United States armed forces are also modernizing its fleet of utility helicopters. The United States Navy plans to retire all its C-2 aircraft by 2024, as it has started taking deliveries of CMV-22B Osprey. Both the United States Navy and Marine Corps have placed orders for Ospreys in the past few years. Moreover, in June 2022, a contract of USD 2.27 billion has been awarded to Sikorsky Aircraft Corp., Stratford, by the United States department of defense for procurement of 120 H-60M Black Hawk helicopters and associated support for the fiscal years 2022-2026, with options for an additional 135 aircraft.

Thus, such developments will lead to the fighter aircraft witnessing significant increase during the forecast period.

Fighter Aircraft Industry Overview

The aerospace and defense industry boasts several leading players, including Lockheed Martin Corporation, The Boeing Company, United Aircraft Corporation, Chengdu Aircraft Industrial (Group) Co. Ltd., and Saab AB. However, Lockheed Martin Corporation holds a prominent position in the market due to its high delivery volumes of F-35 fighter aircraft. Its ongoing research and development efforts further reinforce the company's market dominance focus on creating high-performance fighter aircraft and technologies that provide superior capabilities for engaging and neutralizing airborne, ground, and hostile naval forces.

Lockheed Martin Corporation's extensive product portfolio, featuring several variants, and continuous product development cycles, enable enhanced operating life of aerial assets. This robust research and development framework also attracts potential buyers seeking higher performance reliability and upgrade potential from their aerial assets.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 Market Segmentation

- 5.1 Take-off and Landing

- 5.1.1 Conventional Take-off and Landing

- 5.1.2 Short Take-off and Landing

- 5.1.3 Vertical Take-off and Landing

- 5.2 Type

- 5.2.1 Light Attack

- 5.2.2 Electronic Warfare

- 5.2.3 Multi-Role Fighter

- 5.2.4 Trainers

- 5.2.5 Other Types

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Egypt

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Vendor Market Share

- 6.2 Company Profile

- 6.2.1 Lockheed Martin Corporation

- 6.2.2 Saab AB

- 6.2.3 The Boeing Company

- 6.2.4 Airbus SE

- 6.2.5 United Aircraft Corporation

- 6.2.6 Chengdu Aircraft Industrial (Group) Co. Ltd

- 6.2.7 Hindustan Aeronautics Limited

- 6.2.8 BAE Systems PLC

- 6.2.9 Dassault Aviation SA

- 6.2.10 Mitsubishi Heavy Industries

- 6.2.11 Aero Vodochody Aerospace A.S

- 6.2.12 Embraer SA

- 6.2.13 Textron Aviation (Textron Systems)

- 6.2.14 Korea Aerospace Industries

- 6.2.15 Turkish Aerospace Industries