|

市場調査レポート

商品コード

1687276

サイバーセキュリティ保険- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Cybersecurity Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| サイバーセキュリティ保険- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

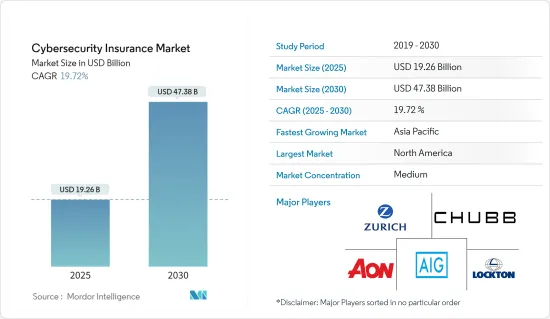

サイバーセキュリティ保険市場規模は、2025年に192億6,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは19.72%で、2030年には473億8,000万米ドルに達すると予測されます。

ビジネスや社会におけるクラウド、ビッグデータ、IoT、人工知能(AI)のデジタル化と急速な開発が進み、あらゆるものが接続されるようになったことで、すでに疲弊しているITチームの仕事量が増加しています。

主要ハイライト

- ITの進歩、通信技術、スマートエネルギーグリッドは、あらゆる国の重要インフラやビジネスネットワークの状況を変えつつあります。しかし、技術の急速な進化には、脅威の急速な進化も伴います。個人情報は貴重であるため、サイバー犯罪者は、クレジットカード番号、ID、医療記録など、個人情報がダークウェブで販売されるような犯罪を犯すようになります。これは、サイバーセキュリティの需要が高まっている数少ない要因のひとつです。

- クラウドコンピューティングは、ITの伝統的境界をなくし、新たな市場を創造し、モビリティの動向に拍車をかけ、ユニファイドコミュニケーションの進歩を可能にする、最近最も急速に成長している技術のひとつです。さまざまなハイテク関係者や組織が、現代のサイバーセキュリティの状況下で機密データを保管するリスクを軽減するために、新たな保険モデルに目を向けています。

- サイバーセキュリティ保険のセグメントが成熟し続けるにつれ、保険会社は査定においてより広範なセキュリティ管理と技術を考慮するようになると考えられます。したがって、組織のデータの機密レベルとそれを適切に隠蔽する能力が、リスク全体を判断する上で重要な役割を果たすことになり、これがマイクロシェーディングのような新技術の採用を後押ししています。マイクロシェーディング技術は、データを1桁バイト程度の断片に分割してから汚染し、その断片を複数の場所に分散させることで、攻撃対象領域を減らし、データの機密性を排除します。

- サイバー保険契約とビジネスは幅広いリスクをカバーしており、保険会社はどの損害事象をカバーするかについて必ずしも合意していないです。サイバー事象には、限定的な損害履歴、将来の事象を予測する際の過去のデータの信頼性の低さ、企業や業種間で相関性の高い損害を伴う大規模攻撃の可能性など、包括的な保険契約を結ぶことを困難にする特徴があります。

- さらに、保険会社は、サイバー攻撃やモノのインターネットのような新技術の影響に関する正確で的確な基準の作成に取り組んでいる最中です。明確な危険定義や保険会社への影響についての理解がないまま大規模なサイバー攻撃が発生した場合、サイバー保険の補償は効果がなく、企業は多大な損害を被る可能性があります。

サイバーセキュリティ保険市場の動向

BFSIセグメントが大きなシェアを占めると予測

- BFSI産業は、多数のデータ漏洩やサイバー攻撃に直面している重要インフラセグメントの1つです。サイバー犯罪者は、金融産業を動けなくするために無数の極悪非道なサイバー攻撃を最適化しています。なぜなら、金融産業は非常に有利な営業モデルであり、驚くほどの利益を上げることができ、また比較的リスクが少なく発見しやすいという利点があるからです。

- トロイの木馬、ATM、ランサムウェア、データ侵害、組織侵入、データ窃盗、財政侵害、その他の脅威はすべて、こうした攻撃の脅威環境の一部であり、BFSIセクターにおけるサイバーセキュリティ保険の需要をさらに高めています。

- 例えば、オレンジのデータによると、2021年10月から2022年9月の間に金融・保険組織で最も頻発したサイバー攻撃はマルウェアでした。この攻撃ベクトルは世界の組織の40%以上を標的にしていました。2位はネットワークとアプリケーションの異常で、23%の組織がこのようなサイバー攻撃を報告しており、次いでシステムの異常が20%でした。

- サイバーセキュリティ保険は、銀行や金融機関にとって不可欠なものとなりつつあります。予測期間中、この産業は世界市場で大きなシェアを占めると予想されます。同産業は高度に規制され、管理された産業のひとつであり、また個人情報詐欺の被害も受けやすいため、BFSIセクターにおけるサイバーセキュリティ保険市場の需要がさらに高まっています。

- セキュリティ侵害の増加に伴い、銀行や金融機関は顧客のデータを保護し、経済的損失を防ぐためにサイバーセキュリティ保険を導入する必要があります。例えば、2021年12月、暗号取引プラットフォームのBitmartで大規模なセキュリティ侵害が発生し、ハッカーが約2億米ドルの資産を持ち去りました。盗まれた秘密鍵がセキュリティ侵害の一次情報であり、イーサリアムとバイナンスの革新的なチェーンのホットウォレットの2つに影響を与えました。

米国が北米地域の主要シェアを占めると予想される

- 米国は世界で最も著名なサイバーセキュリティ保険市場と考えられています。また、同国には同市場で事業を展開する主要企業が多数存在し、これも同国のシェアが高い理由となっています。

- 米国におけるサイバー攻撃は急増しており、過去最高水準に達しています。これは主に、同地域で接続デバイスの数が急速に増加していることに起因しています。米国では、消費者がパブリッククラウドを利用し、バンキング、ショッピング、コミュニケーションなどの利便性を高めるために、モバイルアプリケーションの多くに個人情報がプリインストールされています。

- ホワイトハウスの経済諮問委員会によると、米国経済は有害なサイバー活動によって年間約570億~1,090億米ドルを失っています。サイバー攻撃によるこの損失を最小限に抑えるためには、サイバーセキュリティ保険プロバイダーが提供するソリューションが不可欠であり、この地域ではサイバーセキュリティ保険の需要が高まっている

- 同地域ではここ数年、相当数のデータ漏洩が発生しています。Identity Theft Resource Centerが2022年に発表した報告書によると、1,789件のデータ漏洩事件が記録されています。データ漏えいの多発は、さまざまな業種の組織にサイバーセキュリティ保険を選択することを促し、市場の成長を促進しています。

- 米国政府は、サイバー攻撃に対する防御を強化するため、サイバーセキュリティインフラ安全保障局(CISA)を設立する法律に署名しました。CISAは連邦政府と協力し、サイバーセキュリティツール、インシデント対応サービス、評価能力を提供し、提携する省庁の重要業務を支える政府系ネットワークを保護します。その結果、新規と既存の企業が、この産業向けに設計された適切なサイバーセキュリティスイートに投資するための新たな道が開かれることになります。

サイバーセキュリティ保険産業概要

サイバーセキュリティ保険市場は適度に統合されており、重要な参入企業が優れた技術を提供し、既存の流通チャネルを通じて成長を促進しています。これらの技術・リーダーは、市場での競合を維持するために、イノベーション、合併、買収、パートナーシップ活動に投資しています。

- 2023年2月-CloudCover Reは保険ブローカーであるHylant Global Captive Solutions(Hylant)と提携し、サイバーセキュリティの「レンタル・ア・キャプティブ」保険プログラムであるCloudCover CyberCellを立ち上げました。団体、アフィニティ・グループ、大企業が利用できるこのプログラムにより、利用者は管理可能なコストで自己保険付きサイバー・リスクに資金を提供することができます。これにより、サイバー攻撃による潜在的な賠償責任が軽減され、企業にとっては、より低コストで幅広い補償範囲のサイバー保険を提供できるため、より大きな収益を生み出すことが容易になります。

- 2022年11月-サイバーセキュリティ企業であるアジリカスと大手総合保険代理店の1つであるRidge Canada Cyber Solutions Inc.(RCCS)は、カナダの中堅・中小企業(SMB)がサイバーセキュリティ保険の資格を取得し、保険に加入するのを支援するために協力しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 産業のガイドラインと施策

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- クラウドベースのサービス採用の増加

- データセキュリティ侵害の増加

- 市場抑制要因

- サイバー保険導入の難しさと高コスト

第6章 市場セグメンテーション

- 組織規模

- 中小企業(SME)

- 大企業

- エンドユーザー産業

- 医療

- 小売

- BFSI

- IT・通信

- 製造業

- その他

- 地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- アジア

- インド

- 中国

- 日本

- シンガポール

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- American International Group Inc.

- Zurich Insurance Co. Ltd

- Aon PLC

- Lockton Companies Inc.

- The Chubb Corporation

- AXA XL

- Berkshire Hathaway Inc.

- Insureon

- Security Scorecard Inc.

- Allianz Global Corporate & Specialty(AGCS)

- Munich Re Group

第8章 投資分析

第9章 市場機会と今後の動向

The Cybersecurity Insurance Market size is estimated at USD 19.26 billion in 2025, and is expected to reach USD 47.38 billion by 2030, at a CAGR of 19.72% during the forecast period (2025-2030).

Increasing digitalization and rapid development in the cloud, Big Data, IoT, and artificial intelligence (AI) in business and society and the growing connectivity of everything have increased the workload of already strained IT teams.

Key Highlights

- IT advances, communication technologies, and the smart energy grid are changing the landscape of all every country's critical infrastructure and business networks. However, with rapidly evolving technology comes rapidly advancing threats. Personal data is valuable, which prompts cybercriminals to commit crimes, where personal information will be sold on the dark web, like a credit card number, identity, medical records, etc. It is among the few factors that have led to an increased demand for cybersecurity.

- Cloud computing is one of the most rapidly growing recent technologies, eliminating the traditional boundaries of IT, creating new markets, spurring the mobility trend, and enabling advances in unified communications. Various tech stakeholders and organizations are turning to new insurance models to mitigate the risks of storing sensitive data in the modern cybersecurity landscape.

- As the cybersecurity insurance space continues to mature, insurers will consider a broader range of security controls and technologies in their assessments. Hence, the sensitivity level of an organization's data and its ability to adequately obscure it will play a key role in determining the overall risk, which is driving the adoption of new technologies like micro shading. Microsharding technology breaks data into fragments that can be as small as single-digit bytes before polluting and distributing shards to multiple locations to reduce the attack surface and eliminate data sensitivity.

- Cyber insurance policies and businesses cover a wide range of risks, and insurers do not always agree on which loss events are covered. Cyber events have characteristics that make it challenging to write comprehensive policies, such as limited loss history, the unreliability of past data when predicting future events, and the possibility of a large-scale attack with highly correlated losses across companies and industries.

- Furthermore, insurers are still working on precise and accurate criteria for cyberattacks and the impact of new technologies like the Internet of Things. Cyber insurance coverage could be ineffective and expose firms to considerable damage if big cyberattacks occur without well-defined dangers and an understanding of how they affect insurers.

Cybersecurity Insurance Market Trends

The BFSI Segment is Estimated to Hold a Significant Share

- The BFSI industry is one of the critical infrastructure segments facing multiple data breaches and cyberattacks, owing to the massive client base that the sector serves and the financial information at stake. Cybercriminals are optimizing myriad diabolical cyberattacks to immobilize the financial industry since it is a highly lucrative operating model with amazing profits and the bonus of relatively little risk and detectability.

- Trojans, ATMs, ransomware, data breaches, institutional invasion, data thefts, fiscal breaches, and other threats are all part of the threat environment for these attacks, which further necessitated the demand for cybersecurity insurance in the BFSI sector.

- For instance, according to the data from Orange, the malware was the most frequent form of cyber attack in financial and insurance organizations between October 2021 and September 2022. The attack vector targeted over 40% of the world's organizations. Network and application anomalies came in second, with 23% of organizations reporting such cyberattacks, followed by System anomalies with 20%.

- Cybersecurity Insurance is increasingly becoming a vital part of banking and financial institutions. The industry is expected to command a significant global market share during the forecast period. It is one of the highly regulated, governed industries and is also prone to identity frauds that augment demand, thus further proliferating the demand for the cybersecurity insurance market in the BFSI sector.

- With increased security breaches, banks and financial institutes should adopt cybersecurity insurance to safeguard their customers' data and prevent economic losses. For instance, in December 2021, a huge security breach at Bitmart, a crypto trading platform, resulted in hackers removing about USD 200 million in assets. A stolen private key was the primary source of the security compromise, which affected two of its Ethereum and Binance innovative chain hot wallets.

The United States is Expected to Hold the Major Share in the North American Region

- The United States is considered the world's most prominent cybersecurity insurance market. The country is also home to a significant number of key players operating in the market, which is another reason for the country's high share.

- Cyberattacks in the United States are rising rapidly and have reached an all-time high, primarily owing to the rapidly increasing number of connected devices in the region. In the United States, consumers are using public clouds, and many of their mobile applications are preloaded with their personal information for the convenience of banking, shopping, communication, etc.

- According to the White House Council of Economic Advisers, the US economy loses approximately USD 57 billion to USD 109 billion per year to harmful cyber activity. To minimize this loss due to cyber attacks, the solutions offered by cyber security insurance providers are essential, and the demand for cyber security insurance is increasing in the region.

- The region has been witnessing a significant number of data breaches over the years. According to the report published in 2022 by the Identity Theft Resource Center, 1,789 data breach incidents have been recorded. The high number of data breaches encourages organizations across various industries to opt for cybersecurity insurance, driving the market's growth.

- The United States government signed the law to establish Cybersecurity and Infrastructure Security Agency (CISA) to enhance the defense against cyber attacks. It works with the federal government to provide cybersecurity tools, incident response services, and assessment capabilities to safeguard the governmental networks that support essential operations of the partner departments and agencies. As a result, it will open new avenues for the new and existing companies to invest in suitable cyber security suite designed for this industry.

Cybersecurity Insurance Industry Overview

The cybersecurity insurance market is moderately consolidated, with significant players offering superior technology and fostering growth through their existing distribution channels. These technology leaders are investing in innovations, mergers, acquisitions, and partnership activities to maintain a competitive edge in the market.

- February 2023 - CloudCover Re collaborated with insurance brokerage Hylant Global Captive Solutions (Hylant) to launch CloudCover CyberCell, a cybersecurity 'rent-a-captive' insurance program. Available to associations, affinity groups, and large enterprises, the program allows users to finance self-insured cyber risks at a manageable cost. This reduces the potential liability of cyber attacks and facilitates more significant revenue generation for companies, as they can provide cyber insurance at a lower cost and broader coverage.

- November 2022 - Agilicus, a cybersecurity firm, and Ridge Canada Cyber Solutions Inc.(RCCS), one of the leading managing general insurance agencies, collaborated to assist Canadian small to midsize businesses (SMBs) qualify for and obtain cybersecurity insurance.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Industry Guidelines and Policies

- 4.5 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Cloud-based Services

- 5.1.2 Rising Data Security Breaches

- 5.2 Market Restraints

- 5.2.1 Difficulties in Implementing Cyber Insurance and High Costs

6 MARKET SEGMENTATION

- 6.1 Organization Size

- 6.1.1 Small and Medium Enterprises (SMEs)

- 6.1.2 Large Enterprises

- 6.2 End-user Industry

- 6.2.1 Healthcare

- 6.2.2 Retail

- 6.2.3 BFSI

- 6.2.4 IT and Telecom

- 6.2.5 Manufacturing

- 6.2.6 Other End-user Industries

- 6.3 Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 United Kingdom

- 6.3.2.3 France

- 6.3.3 Asia

- 6.3.3.1 India

- 6.3.3.2 China

- 6.3.3.3 Japan

- 6.3.3.4 Singapore

- 6.3.3.5 Australia and New Zealand

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 American International Group Inc.

- 7.1.2 Zurich Insurance Co. Ltd

- 7.1.3 Aon PLC

- 7.1.4 Lockton Companies Inc.

- 7.1.5 The Chubb Corporation

- 7.1.6 AXA XL

- 7.1.7 Berkshire Hathaway Inc.

- 7.1.8 Insureon

- 7.1.9 Security Scorecard Inc.

- 7.1.10 Allianz Global Corporate & Specialty (AGCS)

- 7.1.11 Munich Re Group