|

|

市場調査レポート

商品コード

1444571

皮膚治療薬:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Dermatological Therapeutics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 皮膚治療薬:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 114 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

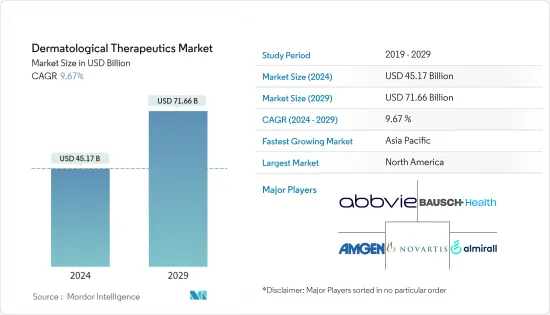

皮膚治療薬の市場規模は、2024年に451億7,000万米ドルと推定され、2029年までに716億6,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に9.67%のCAGRで成長します。

世界的に見て、COVID-19感染症の感染率の高さにより、世界中の多くの国が経済とヘルスケアシステムに大きな負担を被っており、現在も被り続けています。COVID-19のパンデミック中、すべてのヘルスケア関連企業の製造部門が影響を受け、すべての先進市場と新興市場で交通機関が大きな影響を受けました。皮膚科市場はパンデミック中に間接的および直接的な影響をいくつか観察しました。たとえば、2021年1月にPubMed Centralが発表した論文によると、COVID-19の流行がほとんどの皮膚科サービスに悪影響を及ぼし、慢性患者の診察時間が大幅に減少したことが研究で示されました。したがって、パンデミックは市場の成長に大きな影響を与えました。ただし、パンデミックが沈静化しているため、調査対象の市場は予測期間中に安定した成長を遂げると予想されます。

市場の成長を促進する要因としては、皮膚科疾患の負担の増大、疾患の進行と病因に対する意識レベルの向上、高齢者人口の増加などが挙げられます。高齢化の進展に伴い、皮膚科診療は今後ますます注目を集めることになるでしょう。加齢に伴い、結合組織の変化、皮膚の強度と弾力性の低下、皮脂腺からの分泌物の減少などの要因により、皮膚関連疾患を発症するリスクが増加します。

たとえば、2022年に発行された「世界人口予測2022年報告書」によると、世界人口に占める65歳以上の人口の割合は、2022年の10%から2050年には16%に上昇すると予測されています。2050年までに、65歳の人口は世界中の高齢者人口は、5歳未満の子供の数の2倍以上、12歳未満の子供の数とほぼ同じになると予測されています。したがって、高齢者人口の増加が市場の成長を促進すると予想されます。

皮膚疾患は人々の生活の質に深刻な影響を及ぼし、職場やその他の場所での生産性の低下や、外観の損傷による差別を引き起こしています。 2022年に国際湿疹評議会が発行した2022年アトピー性皮膚炎に関する世界報告書によると、2022年には約2億2,300万人がアトピー性皮膚炎を抱えており、そのうち約4,300万人が1~4歳でした。これは、幼児における有病率が驚くほど高いことを示しています。アトピー性皮膚炎は、子どもとその保護者にとって病気の負担となるだけでなく、子どもの発育、教育、仕事にも悪影響を与える可能性があります。したがって、このような皮膚疾患の高い有病率と負担の増加により、市場の成長が促進されると予想されます。

皮膚治療薬市場は、コラボレーション、買収、新製品の発売により、大きな成長の機会が見込まれると予想されています。たとえば、2021年12月、LEO Pharma Inc.は、局所処方療法では疾患が適切にコントロールされていない18歳以上の成人の中等度から重度のアトピー性皮膚炎の治療薬として、米国FDAがアドブリー(トラロキヌマブ-ldrm)を承認したと発表しました。またはそれらの治療法がお勧めできない場合。

したがって、皮膚疾患の負担の増大、高齢者人口の増加、主要な市場プレーヤーによる開発の増加が、予測期間中に市場を牽引すると予想されます。しかし、特定の種類の治療薬の重篤な副作用により、近い将来市場が抑制されることが予想されます。

皮膚治療薬市場動向

乾癬セグメントは予測期間中にかなりの市場シェアを保持すると予想される

乾癬は、皮膚細胞の成長サイクルを加速させる慢性の自己免疫性皮膚疾患です。肘、顔、手のひら、膝、頭皮、腰、足の裏に分厚い赤い皮膚と銀色の鱗の斑点が生じます。最も一般的なタイプの乾癬は尋常性乾癬であり、皮膚に対する誤ったT細胞攻撃が原因となります。乾癬の有病率の上昇、乾癬治療薬開発の臨床試験数の増加、主要市場プレーヤーによる開発の増加により、この部門の成長が促進されると予想されます。

乾癬の有病率の上昇がこのセグメントを推進する主な要因です。たとえば、国立乾癬財団が2022年 12月に更新したデータによると、2022年には世界中で約1億2,500万人が乾癬を患っており、これは総人口の2~3%にほぼ相当します。この情報筋はまた、2022年には800万人以上のアメリカ人が乾癬を患っていると述べました。したがって、乾癬の有病率の高さにより、皮膚科治療の採用が促進されると予想されます。乾癬は高齢者に関連することが多いため、高齢者人口の増加も部門別の成長を促進すると予想されます。

Clinicaltrials.govが公開したデータによると、2023年 2月に世界中で乾癬の治療を目的とした約325件の臨床試験が進行中です。これらは将来的にこの疾患の治療薬として承認されることが期待されており、それがこの部門の成長を牽引することになります。

新製品の発売、皮膚治療薬市場の拡大における市場関係者の焦点、および提携や買収がこの分野を後押しすると予想されます。たとえば、2021年12月に米国FDAは、軽度から中等度の尋常性乾癬の成人の治療にアムジェン社の医薬品オテズラの使用拡大を承認しました。

したがって、乾癬の有病率の上昇、高齢者人口の増加、主要企業による開発の増加、乾癬の臨床試験数の増加などの要因により、このセグメントは予測期間中に着実な成長を遂げると予想されます。

北米は予測期間中にかなりの市場シェアを持つと予想される

北米は、ヘルスケア費の増加、皮膚疾患に対する意識の高まり、製薬会社の存在感の強さにより、大きな市場シェアを保持すると予想されています。

皮膚科疾患の有病率の上昇は、この地域の市場を押し上げると予想される主要な要因です。たとえば、2022年 8月にアメリカ喘息・アレルギー財団が発表したデータによると、成人約1,650万人がアトピー性皮膚炎(AD)を患っており、2022年には660万人が中等度から重度の症状を報告しています。このような皮膚科疾患により、この地域での皮膚科治療の採用が促進されると予想されます。

高齢者人口の増加も市場の主要な促進要因です。たとえば、カナダ統計局が2022年 7月に発表したデータによると、カナダの65歳以上の人口は約7,330,605人で、総人口の18.8%を占めています。

主要な地域市場プレーヤーによる新製品の発売も、市場の成長を促進すると予想されます。たとえば、2021年7月、Sol-Gel Technologies Ltdは、成人および小児患者の尋常性ざ瘡の治療を適応とする初の独自医薬品製品TWYNEO(トレチノイン/過酸化ベンゾイル)クリーム0.1%/3%をFDAが承認したと発表しました。 9歳以上。同様に、2021年 9月、インサイトは、米国FDAが、12歳以上の非免疫不全患者における軽度から中等度のアトピー性皮膚炎(AD)の短期的かつ非継続的な慢性治療としてオプゼルラ(ルキソリチニブ)クリームを承認したと発表しました。局所処方療法では疾患が適切にコントロールされない場合、またはそれらの療法が推奨されない場合。したがって、主要な市場プレーヤーによる製品発売の増加が主に北米市場を牽引しています。

したがって、皮膚科疾患の有病率の上昇、高齢者人口の増加、主要な市場プレーヤーによる開発の増加などの要因により、市場は予測期間中にこの地域で着実な成長を遂げると予想されます。

皮膚治療薬業界の概要

皮膚治療薬市場は適度に細分化されています。成長機会により、皮膚治療薬市場には多くの新規プレーヤーが出現しています。主要医薬品の今後の特許失効により競合が激化し、特にジェネリック分野での市場調査がさらに促進されています。皮膚科の診断および治療産業は、発展途上地域での大きな市場シェアをいくつかのジェネリック企業が支配しており、大幅に成長すると予想されています。市場参加者には、Amgen Inc.、Bausch Health Companies Inc.、Novartis AG、AbbVie Inc.、Almirall SAなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 増大する皮膚科疾患の負担

- 病気の進行と病因についての意識レベルの向上

- 高齢者人口の増加

- 市場抑制要因

- 特定の種類の治療薬における重篤な副作用

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 用途別

- 脱毛症

- ヘルペス

- 乾癬

- 酒さ様皮膚炎

- アトピー性皮膚炎

- その他の用途

- 薬剤クラス別

- 抗感染症薬

- コルチコステロイド

- ニキビ対策

- カルシニューリン阻害剤

- レチノイド

- その他の薬剤クラス

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Abbvie Inc.(Allergan PLC)

- Almirall SA

- Amgen Inc.

- Bausch Health Companies Inc.

- Galderma SA

- GlaxoSmithKline PLC

- Johnson &Johnson

- Novartis AG

- Pfizer Inc.

- Bristol-Myers Squibb Company

- LEO Pharma AS

- Eli Lilly and Company

- Sun Pharmaceuticals Ltd

- Aclaris Therapeutics Inc.

- Aurobindo Pharma Ltd

第7章 市場機会と将来の動向

The Dermatological Therapeutics Market size is estimated at USD 45.17 billion in 2024, and is expected to reach USD 71.66 billion by 2029, growing at a CAGR of 9.67% during the forecast period (2024-2029).

Globally, due to the high transmission rate of COVID-19, many countries worldwide have suffered and are continuing to suffer a major burden on their economy and healthcare systems. The manufacturing units of all healthcare-based companies were affected, and the transport was impacted badly across all developed and emerging markets during the COVID-19 pandemic. The dermatology market observed some indirect and direct impacts during the pandemic. For instance, according to an article published by PubMed Central in January 2021, a study showed that the COVID-19 outbreak had an adverse effect on most dermatology services, with a significant reduction in consultation time spent for chronic patients. Thus, the pandemic had a significant impact on the market growth. However, as the pandemic has subsided, the studied market is expected to have stable growth during the forecast period.

Some factors driving the market's growth include the growing burden of dermatology diseases, increased awareness levels of disease progression and etiology, and a rise in the elderly population. With the rise in the aging population, dermatological care is likely to receive particular attention. As people age, the risk of developing skin-related disorders increases due to factors such as changes in the connective tissue, reduction in the skin's strength and elasticity, and reduction in secretions from sebaceous glands.

For instance, according to the World Population Prospects 2022 Report published in 2022, the share of the global population aged 65 years or above is projected to rise from 10% in 2022 to 16% in 2050. By 2050, the number of people aged 65 years or over worldwide is projected to be more than twice the number of children under age five and about the same as that of children under age 12. Thus, the rising geriatric population is expected to enhance market growth.

Skin diseases have seriously impacted people's quality of life, causing productivity loss at work and other places and discrimination due to disfigurement. According to the Global Report on Atopic Dermatitis 2022 published by the International Eczema Council in 2022, about 223 million people were living with atopic dermatitis in 2022, of which around 43 million were aged 1-4. This shows the strikingly high prevalence in young children. In addition to the disease burden for the children and their caregivers, atopic dermatitis can also negatively affect the children's development, education, and work. Thus, the high prevalence and the rising burden of such dermatological diseases are expected to boost the market's growth.

The dermatological therapeutics market is anticipated to witness a lucrative growth opportunity due to collaborations, acquisitions, and new product launches. For instance, in December 2021, LEO Pharma Inc. announced that the US FDA approved Adbry (tralokinumab-ldrm) for the treatment of moderate-to-severe atopic dermatitis in adults 18 years or older whose disease is not adequately controlled with topical prescription therapies or when those therapies are not advisable.

Thus, the increasing burden of dermatological diseases, the rising geriatric population, and the increasing developments by key market players are expected to drive the market over the forecast period. However, serious side effects of certain classes of therapeutic drugs are expected to restrain the market in the near future.

Dermatological Therapeutics Market Trends

Psoriasis Segment is Expected to Hold a Significant Market Share Over the Forecast Period

Psoriasis is a chronic autoimmune skin disease that speeds up the growth cycle of skin cells. It causes patches of thick red skin and silvery scales on the elbows, face, palms, knees, scalp, lower back, and soles of feet. The most common type of psoriasis is plaque psoriasis, and misguided T-cell attacks on the skin cause it. The rising prevalence of psoriasis, the increasing number of clinical trials for psoriasis drug development, and the rising developments by major market players are expected to boost the segment's growth.

The rising prevalence of psoriasis is a major factor driving the segment. For instance, according to the data updated by the National Psoriasis Foundation in December 2022, around 125 million people worldwide had psoriasis in 2022, almost equal to 2-3% of the total population. The source also stated that more than 8 million Americans had psoriasis in 2022. Thus, the high prevalence of psoriasis is expected to boost the adoption of dermatological therapeutics. As psoriasis is often associated with the elderly, the rising geriatric population is also expected to drive segmental growth.

As per the data published by clinicaltrials.gov, in February 2023, globally, approximately 325 ongoing clinical trials were being conducted for the treatment of psoriasis. These are expected to receive approvals for the treatment of the disease in the future, thus driving the segment's growth.

The new product launches, the focus of market players in expanding their market for dermatology therapeutics, and collaborations and acquisitions are anticipated to boost the segment. For instance, in December 2021, the US FDA approved the expanded use of Amgen Inc.'s drug Otezla to treat adults with mild to moderate plaque psoriasis.

Thus, due to factors such as the rising prevalence of psoriasis, the rising geriatric population, the increasing developments by key players, and the rising number of psoriasis clinical trials, the segment is expected to witness steady growth over the forecast period.

North America is Expected to Have a Significant Market Share Over the Forecast Period

North America is expected to hold a significant market share due to increasing healthcare expenditure, growing awareness about skin diseases, and the strong presence of pharmaceutical companies.

The rising prevalence of dermatological diseases is a major factor that is expected to boost the market in the region. For instance, according to the data published by the Asthma and Allergy Foundation of America in August 2022, around 16.5 million adults had atopic dermatitis (AD), with 6.6 million reporting moderate-to-severe symptoms in 2022. Thus, the high prevalence of such dermatological diseases is expected to boost the adoption of dermatological therapeutics in the region.

The rising geriatric population is also a major driver of the market. For instance, according to the data published by Statistics Canada in July 2022, around 7,330,605 people are 65 years of age or older in Canada, accounting for 18.8% of the total population.

The new product launches by key regional market players are also anticipated to boost the market's growth. For instance, in July 2021, Sol-Gel Technologies Ltd announced that the FDA approved its first proprietary drug product, TWYNEO (tretinoin/benzoyl peroxide) cream, 0.1%/3%, indicated for the treatment of acne vulgaris in adults and pediatric patients nine years of age and older. Similarly, in September 2021, Incyte announced that the US FDA approved Opzelura (ruxolitinib) cream for the short-term and non-continuous chronic treatment of mild to moderate atopic dermatitis (AD) in non-immunocompromised patients 12 years of age and older whose disease is not adequately controlled with topical prescription therapies, or when those therapies are not advisable. Thus, the rising product launches by key market players are mainly driving the North American market.

Thus, due to factors such as the rising prevalence of dermatological diseases, the rising geriatric population, and the increasing developments by key market players, the market is expected to witness steady growth in the region over the forecast period.

Dermatological Therapeutics Industry Overview

The dermatological therapeutics market is moderately fragmented. Due to the growth opportunities, many new players are emerging in the dermatological therapeutics market. Forthcoming patent expiries of major drugs are leading to increased competition, further driving the market studied, especially in the generic sector. The dermatological diagnostics and therapeutics industry is expected to grow tremendously, with several generic players controlling significant market share in the developing regions. Some of the market players include Amgen Inc., Bausch Health Companies Inc., Novartis AG, AbbVie Inc., and Almirall SA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Burden of Dermatology Diseases

- 4.2.2 Increasing Awareness Levels of Disease Progression and Etiology

- 4.2.3 Increasing Elderly Population

- 4.3 Market Restraints

- 4.3.1 Serious Side Effects for Certain Classes of Therapeutic Drugs

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Application

- 5.1.1 Alopecia

- 5.1.2 Herpes

- 5.1.3 Psoriasis

- 5.1.4 Rosacea

- 5.1.5 Atopic Dermatitis

- 5.1.6 Other Applications

- 5.2 By Drug Class

- 5.2.1 Anti-infectives

- 5.2.2 Corticosteroids

- 5.2.3 Anti-acne

- 5.2.4 Calcineurin Inhibitors

- 5.2.5 Retinoids

- 5.2.6 Other Drug Classes

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbvie Inc. (Allergan PLC)

- 6.1.2 Almirall SA

- 6.1.3 Amgen Inc.

- 6.1.4 Bausch Health Companies Inc.

- 6.1.5 Galderma SA

- 6.1.6 GlaxoSmithKline PLC

- 6.1.7 Johnson & Johnson

- 6.1.8 Novartis AG

- 6.1.9 Pfizer Inc.

- 6.1.10 Bristol-Myers Squibb Company

- 6.1.11 LEO Pharma AS

- 6.1.12 Eli Lilly and Company

- 6.1.13 Sun Pharmaceuticals Ltd

- 6.1.14 Aclaris Therapeutics Inc.

- 6.1.15 Aurobindo Pharma Ltd