|

市場調査レポート

商品コード

1444558

ユーティリティトラクター:市場シェア分析、業界動向と統計、成長予測(2024-2029)Utility Tractor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ユーティリティトラクター:市場シェア分析、業界動向と統計、成長予測(2024-2029) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

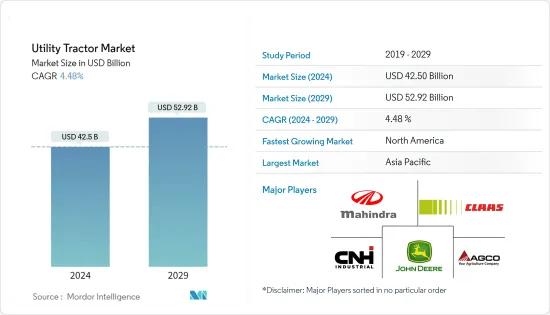

ユーティリティトラクター市場規模は、2024年に425億米ドルと推定され、2029年までに529億2,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に4.48%のCAGRで成長します。

主なハイライト

- ユーティリティトラクターは、フロントローダー作業、土づくり、運搬などさまざまな作業に使用できるように設計されています。このタイプのトラクターは、耕耘や重量物を牽引するなどの農業作業に使用されます。食糧需要の増加と農業機械化の普及により、世界的に農業における機械の使用が増加しています。ユーティリティトラクターは、農家が農業プロセスを簡単に実行できるように支援します。

- ユーティリティトラクターは、35馬力から100馬力の範囲のセグメントで構成されており、小規模から中規模の農業作業向けの多くのコンパクトなユーティリティタイプのトラクターが含まれます。小規模農家は、平均的な農業用トラクターよりもはるかに小さく、価格がはるかに安いため、コンパクトユーティリティトラクター(40HP~70HP)を採用することが増えています。低コストにもかかわらず、コンパクトなトラクターは、農家がバックホーやフロントエンドローダーなどの農機具を使って多くの作業を実行し、人件費を節約するのに役立ちます。大型(41~50馬力)トラクターの需要増加の主な理由は硬い土壌条件ですが、インフラストラクチャーや建設分野などの非農業分野での使用の増加もこのカテゴリーの需要の増加に貢献しています。これにより、ユーティリティトラクター業界は今後数年間で成長するでしょう。

- ユーティリティトラクターは、フロントエンドローダーやバックホーなどの重要な前部または後部のアタッチメントを使用して、積み込みや掘削を行うことができます。それでも、造園、種まき、干し草の栽培、除雪にも使用できるため、この分野の市場を世界的に牽引しています。インドの農業機械化レベルは、2019年に40.0%~45.0%と記録されました。小規模かつ限界的な農家のほぼ80.0%が国内に5ヘクタール未満の土地を所有しているため、農機具の普及は遅れています。インドの農業部門では、動物の力や人間の力の使用が大幅に減少しています。これらの多くは、トラクターやディーゼルエンジンなどの化石燃料を燃料とする車両によって駆動されます。これにより、伝統的な農業プロセスからより機械化された農業プロセスに移行しました。

- インドの機械化のレベルは、中国やブラジルなどの他の新興諸国に比べて低いもの、確実に成長段階にあります。機械化レベルを高めるために、インド政府はさまざまな機器に補助金を提供し、フロントエンド代理店を通じた大量購入をサポートすることにより「バランスの取れた農業機械化」を推進しており、予測期間中にユーティリティトラクター市場が強化されることが予想されます。

ユーティリティトラクター市場動向

農場機械化への関心の高まり

- 精密農業と、生産量を増やすための農業技術の採用の増加により、世界中の最小限の耕地所有地で多用途トラクターの需要が高まっています。農業機械の使用を大規模に促進する農業研修プログラムの増加も、トラクター業界を後押ししています。さらに、いくつかの発展途上国の政府は、主要な農業プロセスの自動化を支援するために補助金や財政援助を提供しています。

- さらに、さまざまな技術的進歩により、GPSおよびテレマティクスシステムが事前にインストールされた最新のトラクターが登場しています。世界の農業用トラクター市場は、自動トラクターの人気の高まりと、農業目的で使用できる遠隔監視のための無線接続の普及によって牽引されると考えられます。

- 現代の農業において農民の収入を増やすためには、農業の機械化が不可欠です。しかし、中国での作物生産における機械の使用は非効率的です。北京の中国農業大学(CAU)が2020年に実施した調査によると、全国の作物の作付けと収穫の機械化率は71%に達しました。

- 作付けと収穫の合計の機械化率は、小麦、米、トウモロコシでそれぞれ95%、85%、90%を超えました。農業の機械化を加速するために、中国政府は、機械の購入や機械の運用に対する財政的補助金や、個々の農民に機械を提供する協同組合への支援など、農民に機械の使用を奨励する一連の政策を打ち出しました。

- アジア太平洋地域の農家も、効率的な農業のニーズを満たすためにカスタマイズされた機能を備えたユーティリティトラクターを求めています。そのため、消費者の需要に応えるために、多くの国内外の農業機械メーカーは、将来の市場の成長を後押しするために、さまざまな農業用途に対応できる、技術的に高度な新しいユーティリティトラクターを開発しています。

- 2022年、John Deere米国は農家向けGtaorユーティリティトラクターを発売しました。 AutoTrac支援ステアリングシステムは、車両が圃場を移動する際に一貫した再現可能な精度と効率を維持することで、オペレータの生産性を向上させます。 AutoTracを利用すると、農家は常に警戒を怠らず、機械の設定やさまざまな圃場条件の制御に集中できます。農家はユーティリティトラクターを使用して、正確なグリッドのサンプリング、散布、圃場の境界作成を行います。

アジア太平洋が市場を独占

- インドでは安価な労働力が豊富にあるにもかかわらず、食料需要が高まっており、特にトラクターなどの農業機械化の導入が増加しています。これは中国にも当てはまり、中国でも同様に農業の機械化傾向が見られます。いくつかの理由から、インドと中国の農家は機械化への関心を高めています。その理由の1つは、人口増加と都市化による食料需要の増大であり、これにより農業の生産性向上の必要性が生じています。もう1つの理由は、人件費の上昇により、機械への投資の費用対効果が高まっていることです。

- 国内における多用途トラクターの普及率は、北インド、特にパンジャブ州、ウッタルプラデーシュ州、ハリヤナ州で高いです。インドでは、インド政府による農業マクロ管理計画の機械化部分に基づき、農業機械化を促進するための補助金が提供されており、これには最大35出力のトラクターの購入に対して30,000インドルピーを上限としてコストの25%が含まれます。-離陸(PTO)HP。インドでは、カスタム雇用サービスが小規模農家に利益をもたらし、小規模地主の利益のために多目的トラクターを操作する新しい種類の起業家が出現しました。これらの要因は、予測期間中にこの地域の市場の成長につながります。

- 中国における農業機械化の増加の背後にある傾向は、農業投資の増加と政府による農業機械化への推進です。農業機械化への投資により、アジア太平洋地域で多用途トラクターの需要が生まれています。中国国家統計局のデータによると、中国は2019年に61万7,700台のトラクターを生産しました。大型および中型のトラクターが徐々に小型トラクターに取って代わられました。

- 2019年末までに、中国は444万台の大型および中型トラクターを含む2,224万台の農業用トラクターを誇っていました。中国はまた、農業用トラクターなどの農業機械の90%をハイエンド機械で生産することに重点を置く「中国製造2025」計画を導入し、2020年までに中国セグメントのシェアの3分の1を占めることになります。国産トラクターを後押しし、国内の農業用トラクター市場を推進します。

- 多用途トラクターは農業プロセスに使用されており、Mahindra &MahindraやJohn Deereなどの国内の大手企業が製品の助けを借りて、この地域で行われる農業慣行に多大な貢献をしています。今後数年間で市場の成長を促進します。新興諸国では、農民の可処分所得が低く、人件費が高いため、35馬力~100馬力のトラクターの需要が高まっています。農家は、農地のサイズが小さいため、農業用にカスタマイズされた小型のコンパクト/ユーティリティトラクターを好みます。さらに、小型トラクターによる燃料消費量の削減は、小規模で限界のある農家に力を与えるのに役立ちます。

ユーティリティトラクター業界の概要

ユーティリティトラクター市場は高度に統合されており、少数のプレーヤーが市場シェアの大部分を占めています。 Deere &Company、CNH Industrial、AGCO Corporation、CLAAS KGaA mbH、Mahindra &Mahindra Corporationがこの市場の主要企業です。新製品の発売、提携、買収は、大手世界企業が採用する主要な戦略です。イノベーションと拡張に加えて、研究開発への投資と新しい製品ポートフォリオの開発は、今後数年間で重要な戦略となる可能性があります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 地域

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- その他アジア太平洋地域

- 世界のその他の地域

- ブラジル

- 南アフリカ

- その他

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- Deere and Company

- CNH Global NV

- AGCO Corporation

- CLAAS KGaA mbH

- Mahindra and Mahindra Corporation

- Kubota Corporation

- Escorts Group

- Tractors and Farm Equipment Limited(TAFE)

- Kuhn Group

- Yanmar Company Limited

第7章 市場機会と将来の動向

The Utility Tractor Market size is estimated at USD 42.5 billion in 2024, and is expected to reach USD 52.92 billion by 2029, growing at a CAGR of 4.48% during the forecast period (2024-2029).

Key Highlights

- Utility tractor is designed for various tasks such as front loader work, soil cultivation, and transportation. This type of tractor is used for farming operations such as plowing and pulling heavy implements. Globally the use of machinery in agriculture is increasing due to increased demand for food and higher penetration of farm mechanization. Utility tractors help the farmer carry out the agriculture process with ease.

- The utility tractors comprise a range of 35 HP to 100 HP segments, including many compact and utility-type tractors meant for small- to mid-sized farming tasks. Small-scale farmers are increasingly adopting compact utility tractors (40HP-70HP) as they are much smaller than the average agricultural tractors and priced much lower. Despite the low-cost, compact tractors can help farmers perform many tasks with the help of farm equipment, such as backhoes and front-end loaders, and save labor wage expenses. Although a key reason for the increasing demand for larger (41-50 HP) tractors is the hard soil condition, increased use in non-agricultural segments, such as infrastructure and construction fields, has also contributed to the increase in demand in this category, which will boost the utility tractors industry to grow in the coming years.

- Utility tractors can work with significant front or rear attachments, like front-end loaders and backhoes, for loading and digging. Still, they can also be used for landscaping, seeding, hay cultivation, and snow removal, which drives the market for this segment globally. The farm mechanization level in India was recorded at 40.0%-45.0% in 2019. The penetration of farm equipment is slow, as almost 80.0% of small and marginal farmers own less than five hectares of land in the country. The agriculture sector in India has witnessed a substantial decline in the use of animal and human power in the agriculture sector. Many of these are driven by fossil fuel-operated vehicles, such as tractors and diesel engines. This has shifted from the traditional agriculture process to a more mechanized one.

- Though the level of mechanization in India is lower than in other developing countries, like China and Brazil, it is certainly in a growing phase. To increase the mechanization level, the Indian government has been promoting 'Balanced Farm Mechanization' by providing subsidies on various equipment and supporting bulk buying through front-end agencies, which is expected to strengthen the utility tractors market during the forecast period.

Utility Tractor Market Trends

Growing Preference For Farm Mechanization

- Precision farming and the increasing adoption of farm technology to boost production are driving up demand for utility tractors in minimum arable landholdings across the globe. The growing number of farm training programs promoting the use of agricultural machinery on a wide scale is also driving the tractor industry. Moreover, governments in several developing nations are providing subsidies and financial aid to help automate key agricultural processes.

- Furthermore, modern tractors with pre-installed GPS and telematics systems have emerged due to different technical breakthroughs. The global agriculture tractor market is likely to be driven by the rising popularity of automated tractors and the widespread use of wireless connectivity for remote monitoring, which can be used for agriculture purposes.

- Agricultural mechanization is essential to increase farmers' income in modern agriculture. However, the use of machinery for crop production in China is inefficient. According to a study conducted by China Agricultural University (CAU), Beijing, in 2020, the national crop planting and harvesting mechanization rate reached 71%.

- The total mechanization rate of planting and harvesting exceeded 95%, 85%, and 90% for wheat, rice, and maize, respectively. To accelerate agricultural mechanization, the Chinese government issued a series of policies to encourage farmers to use machinery, including financial subsidies for machine purchases and machine operations and support for cooperatives to provide machinery for individual farmers.

- Farmers in the Asia-Pacific region also seek utility tractors with tailored features to fulfill their needs for effective farming. So, to meet consumer demand, many international and domestic agriculture machinery manufacturers are developing new technologically advanced utility tractors which can handle various farming applications to push the market to grow in the future.

- In 2022, John Deere US launched Gtaor Utility Tractor for Farmers. The AutoTrac-assisted steering system increases operator productivity by maintaining consistent, repeatable accuracy and efficiency as the vehicle moves across the field. With AutoTrac engaged, farmers can remain alert and focused on controlling machine settings and varying field conditions. Farmers use the utility tractor for precise grid sampling, spraying, and field boundary creation.

Asia-Pacific Dominates the Market

- Despite abundant and cheap labor in India, there has been a growing demand for food, which has led to an increase in the adoption of farm mechanization, particularly in the form of tractors. This is also true for China, where there has been a similar trend toward mechanization in agriculture. For several reasons, farmers in India and China are increasingly turning to mechanization. One reason is the growing demand for food due to population growth and urbanization, which has led to a need for increased productivity in agriculture. Another reason is the rising cost of labor, which has made it more cost-effective to invest in machinery.

- The penetration of utility tractors in the country is higher in North India, particularly in Punjab, Uttar Pradesh, and Haryana. In India, under the mechanization component of the Macro-Management of Agriculture Scheme, by the Indian government, there is a provision of subsidy to promote agricultural mechanization, including 25% of the cost limited to INR 30,000 for buying tractors of up to 35 Power-take-off (PTO) HP. In India, custom hiring services have benefitted smaller farmers, and a new breed of entrepreneurs who operate utility tractors for the benefit of small landholders has emerged. These factors will lead the market to grow in the region during the forecasting period.

- The trend behind the increase in farm mechanization in China has been increased agricultural investments and the government's push toward farm mechanization. The investments in farm mechanization create the demand for utility tractors in the Asia Pacific. According to data from the National Bureau of Statistics of China, China produced 617,700 tractors in 2019. Large and medium-sized tractors gradually replaced small tractors.

- By the end of 2019, China boasted of 22.24 million agricultural tractors, including 4.44 million large- and medium-sized tractors. China has also introduced the 'Made in China 2025' scheme, which focuses on producing 90% of its agricultural equipment with high-end machines, like agricultural tractors, holding a one-third share of their segments by 2020. This, in turn, boosts indigenously produced tractors and propels the country's agricultural tractor market.

- Utility Tractors are being used for the agricultural process, and major players in the country are contributing to it, such as Mahindra & Mahindra and John Deere, with the help of their products, are contributing a lot to the agricultural practices carried out in the region to increase the market growth in the coming years. In developing countries, the demand for 35HP - 100HP tractors is high due to the low disposable income of farmers and high labor costs. Farmers prefer small and customized compact/utility tractors for agricultural purposes due to small farmland sizes. Moreover, lesser fuel consumption by small tractors helps to empower small and marginal farmers.

Utility Tractor Industry Overview

The utility tractors market is highly consolidated, with few players cornering most of the market share. Deere & Company, CNH Industrial, AGCO Corporation, CLAAS KGaA mbH, and Mahindra & Mahindra Corporation are major players in this market. New product launches, partnerships, and acquisitions are the major strategies the leading global companies adopt. Along with innovations and expansions, investments in R&D and developing novel product portfolios will likely be crucial strategies in the coming years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Geography

- 5.1.1 North America

- 5.1.1.1 United States

- 5.1.1.2 Canada

- 5.1.1.3 Rest of North America

- 5.1.2 Europe

- 5.1.2.1 Germany

- 5.1.2.2 United Kingdom

- 5.1.2.3 France

- 5.1.2.4 Spain

- 5.1.2.5 Italy

- 5.1.2.6 Rest of Europe

- 5.1.3 Asia-Pacific

- 5.1.3.1 China

- 5.1.3.2 Japan

- 5.1.3.3 India

- 5.1.3.4 Rest of Asia-Pacific

- 5.1.4 Rest of the World

- 5.1.4.1 Brazil

- 5.1.4.2 South Africa

- 5.1.4.3 Other Countries

- 5.1.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Deere and Company

- 6.3.2 CNH Global NV

- 6.3.3 AGCO Corporation

- 6.3.4 CLAAS KGaA mbH

- 6.3.5 Mahindra and Mahindra Corporation

- 6.3.6 Kubota Corporation

- 6.3.7 Escorts Group

- 6.3.8 Tractors and Farm Equipment Limited (TAFE)

- 6.3.9 Kuhn Group

- 6.3.10 Yanmar Company Limited