|

市場調査レポート

商品コード

1444478

飼料リン酸塩:市場シェア分析、業界動向と統計、成長予測(2024-2029)Feed Phosphate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 飼料リン酸塩:市場シェア分析、業界動向と統計、成長予測(2024-2029) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

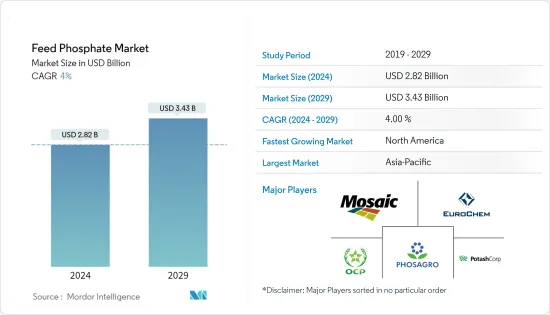

飼料リン酸塩市場規模は2024年に28億2,000万米ドルと推定され、2029年までに34億3,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に4%のCAGRで成長します。

主なハイライト

- 主な要因は、世界中で肉の消費量が増加していることです。 2021年、家禽肉の消費量は1人当たり1キロ当たり76.6%増加し、豚肉は19.7%増加しました。経済協力開発機構(OECD)の2022年報告書によると、家禽肉は全タンパク質の41%を占めると予想されている2030年の食肉源からの摂取量は、基準期間と比較して2パーセントポイント増加しました。他の肉製品の世界シェアはこれより低く、牛肉(20%)、豚肉(34%)、羊肉(5%)です。

- 可処分所得の増加により、消費が大きく飛躍したのは主に中流階級の人々によるものです。政府機関による家畜開発は、動物福祉における動物栄養の重要性を強調することにより、住民、特に貧しい地域の間で畜産を促進するのに役立ちました。食肉産業、特に家禽および豚肉部門の工業化は、その健康上の利点に対する意識の高まりにより赤身の肉の消費が急速に増加し、飼料リン酸塩産業に重要な貢献をしてきました。

- 原材料の価格の上昇と、再生不可能な資源であるリン酸塩埋蔵量の世界の不足が市場を抑制しています。この業界の動向に影響を与える機会には、高製造コストを削減するために動物飼料の製造にブレンドとして使用されるフィターゼなどの天然飼料製品および代替品の需要の増加が含まれます。多くの企業は、リン酸塩の持続可能な利用のための研究開発にも投資しました。家畜の生産は、特に発展途上市場における人口の食生活の変化の需要を満たすために、世界的に、またすべての動物種にわたって増加しています。

- 世界中、特にアジア太平洋で畜産業の工業化が進んでいるにもかかわらず、インドや中国などの国の多くの農家は依然として限界に達しています。アジア太平洋は世界最大の動物飼料の生産国および消費国であり、その結果、飼料リン酸塩の市場に直接影響を与えています。中国やインドを含むこの地域最大の経済大国は、地域の畜産業の拡大もあり、飼料生産能力を増強しています。

飼料リン酸塩の市場動向

産業畜産の増産

- 畜産物の需要の高まりにより、畜産物の収量向上を目指して供給側に大きな変化が生じています。新しい資本集約型技術により、北米、欧州、アジア太平洋などの地域全体、特に土地が限られている国で、工業型生産施設での家禽肉や豚肉の生産が可能になりました。

- 食糧農業機関(FAO)によると、世界の牛の頭数は過去4年間で増加傾向にあります。 2022年の世界の食肉生産量は、2021年比1.2%増の3億6,000万トン(枝肉重量換算)になると予測されました。成長の大部分はアジア、主に中国の豚肉生産量の増加と南米の生産量の増加によるものと予測された他の場所では比較的安定した生産が行われている牛と家禽の肉。欧州の落ち込みがこの成長をほぼ相殺すると予測されていました。

- 食肉生産産業は近年、特に米国や欧州諸国などの先進国で土地利用が減少し、増加傾向にあります。この要因により家畜と肉の生産が増加し、これらの国々で増加する家畜人口のための飼料添加物の需要が加速します。

- 産業規模の家畜生産では、高品質の飼料を最適に利用して、生産プロセスの効率を向上させ、飼料転換率を向上させ、動物の筋肉量とタンパク質含有量を高めます。より多くの農家が産業規模の家畜生産を導入するに伴い、この高品質配合飼料の大規模生産基盤に対応するために飼料添加物の生産を改善する必要があります。これは、予測期間中に世界の飼料添加物市場を押し上げると予想されます。したがって、牛乳と牛の生産量の増加は、飼料添加物市場の成長を促進します。

- さらに、肉の消費は家禽に移りつつあります。低所得の新興諸国では、鶏肉は他の肉に比べて価格が安いのが特徴です。対照的に、高所得国では、調理が簡単でより良い食品の選択肢として認識されている白身の肉に対する嗜好が高まっていることを示しています。家禽肉は、2030年には世界中の肉源からのタンパク質全体の41%を占めると予測されています。米国農務省(USDA)によると、2021年の米国の家禽肉の消費量は1,715万8,000トンでした。鶏肉の最大消費国は中国で、消費量は1,503万2,000トン、次いでブラジルが1,028万トン、カナダが141万1,000トンとなりました。

アジア太平洋が市場を独占

- 急速な経済成長に伴い、アジア、特に中国、インド、マレーシア、ベトナム、タイで肉たんぱく質の需要が高まっています。この肉タンパク質の需要の増加により、この地域での肉生産が活発になり、配合飼料の摂取が増加し、より高い成長率を示すことが予想されています。栄養価の向上とは別に、肉の品質を向上させるために配合飼料の重要性が高まっています。

- 中国の配合飼料産業はここ数年で大きく成長しました。オールテックの調査によると、中国の飼料生産量は昨年大幅に増加し、トン数当たりの飼料生産量が最も増加した国となった。この地域の飼料生産量では中国が2億6,142万トンを占め、次にインドが2021年に4,405万トンを生産しています。

- インドは昨年、牛と水牛の頭数で第1位となった。牛乳と水牛肉の最大の生産国であり、次いでヤギ肉の生産国が2位、家禽肉の生産国が3位でした。インドは2021年に1,220億4,000万個の家禽卵を生産しました。主な成長の促進要因は、品種改良、有機飼料市場の低迷、普及、正式な摂取量の増加などです。

- 米国農務省(USDA)の調査に含まれる業界筋によると、2021年のインドの商業飼料市場はトウモロコシと大豆粕が独占し、数量限定の傷んだ小麦や低品質の小麦などの他の粗穀物も使われたといいます。および他の油糧種子ミールは、比較価格に応じて市場を補完します。したがって、アジア諸国におけるタンパク質ベースの製品の国内消費量の増加、業界によるさまざまなプロモーション活動、および各国でのアフリカ豚コレラ(ASF)の減少は、世界の成長を後押しすると予想される重要な要因の一部です。今後数年間で市場が研究される予定です。

飼料リン酸塩産業の概要

飼料リン酸塩市場は適度に統合されており、The Mosaic Company、Eurochem、Potash Corp、PhosAgro、OCP Groupなどのいくつかの積極的な企業が2022年にはかなりの市場シェアを占めることになります。これらの企業は事業の拡大と合併などの戦略に重点を置いています。そして買収、拡張、そして新しい製品のイノベーション。大手企業は、国内外の市場での事業を拡大するために、飼料工場や小規模製造業の買収に注力しました。これらの企業は、地域全体での事業の拡大と、生産能力と製品ラインを増強するための新工場の設立に重点を置いていました。両社は既存工場の生産能力も増強しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競合企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- フィードの種類

- リン酸一カルシウム

- リン酸二カルシウム

- リン酸二カルシウム

- リン酸三カルシウム

- 脱フッ素リン酸塩

- 他のフィードタイプ

- 家畜の種類

- 家禽

- 豚

- 牛

- 水生動物

- その他の種類の家畜

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- アフリカ

- 南アフリカ

- その他アフリカ

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- The Mosaic Company

- EuroChem

- Simphos

- Fosfitalia

- Timab Industries

- Yara International ASA

- OCP Group

- PhosAgro

- Potash Corporation

第7章 市場機会と将来の動向

The Feed Phosphate Market size is estimated at USD 2.82 billion in 2024, and is expected to reach USD 3.43 billion by 2029, growing at a CAGR of 4% during the forecast period (2024-2029).

Key Highlights

- The main driving factor is the growing consumption of meat worldwide. Poultry meat consumption increased by 76.6% per kilo per capita, and pig meat by 19.7% in 2021. According to the Organisation for Economic Co-operation and Development (OECD) report 2022, poultry meat is expected to represent 41% of all the protein from meat sources in 2030, an increase of 2 percentage points when compared to the base period. The global shares of other meat products are lower: beef (20%), pigmeat (34%), and sheep meat (5%).

- The major leap in consumption is mainly by the middle-class population due to increasing disposable income. Livestock development by government organizations helped promote animal husbandry among the population, especially among the poorer sections, by emphasizing the importance of animal nutrition in animal welfare. Industrialization of the meat industry, specifically the poultry and pork segments, has been an important contributor to the feed phosphate industry, with rapid growth in lean meat consumption due to increased awareness of its health benefits.

- The rising cost of raw materials and the global scarcity of phosphate reserves, as it is a non-renewable resource, are restraining the market. Opportunities that affect the dynamics of this industry include increasing demand for natural feed products and substitutes, such as phytase being used in the manufacture of animal feed as blends to decrease the high cost of manufacture. Many companies also invested in R&D for the sustainable use of phosphate. Livestock production has increased globally and across all animal species to meet the demands of the population's shifting dietary habits, especially in developing markets.

- Even though the livestock industry is becoming more industrialized worldwide, particularly in Asia-Pacific, many farmers in nations like India and China are still marginal. Asia-Pacific is the world's largest producer and consumer of animal feed, and as a result, it directly affects the market for feed phosphates. The region's largest economies, including China and India, have increased their feed production capacities partly due to the region's expanding livestock industry.

Feed Phosphate Market Trends

Increasing Industrial Livestock Production

- The growing demand for livestock products has been driving significant changes on the supply side aimed at improving livestock product yields. New capital-intensive technologies have made poultry and pig meat production in industrial-style production facilities possible across regions, such as North America, Europe, and Asia-Pacific, especially in countries with limited land.

- According to the Food and Agriculture Organisation (FAO), the global cattle population witnessed an upward trend over the past four years. World meat production was forecasted at 360 million tons (in carcass weight equivalent) in 2022, up 1.2% from 2021. A significant portion of the growth was predicted to come from Asia, primarily from China's increasing production of pig meat and South America's increasing production of bovine and poultry meat, with relatively stable production elsewhere. The decline in Europe was predicted to largely offset this growth.

- The meat production industry witnessed an upward trend in the recent past, especially in developed countries, such as the United States and European countries, with reduced land usage. This factor boosts livestock and meat production, thus accelerating the demand for feed additives for the growing livestock population in these countries.

- Industrial-scale livestock production makes optimum use of high-quality feed to improve efficiency in the production process, improve feed conversion ratios, and enhance animal muscle mass and protein content. With the adoption of industrial-scale livestock production by a larger number of farmers, feed additives' production needs to improve to cater to this large production base of high-quality compound feed. This is expected to boost the global feed additives market during the forecast period. Thus, the increasing milk and cattle production drives the feed additives market growth.

- Additionally, meat consumption has been changing toward poultry. In lower-income developing countries, poultry reflects a lower price as compared to other meats. In contrast, in high-income countries, this indicates an enhanced preference for white meats, which are easier to prepare and perceived as a better food choice. Poultry meat is projected to represent 41% of all the protein from meat sources in 2030 across the world. According to the United States Department of Agriculture (USDA), in 2021, the consumption of poultry meat in the United States was 17,158 thousand metric tons. China was the largest consumer of chicken, with a consumption rate of 15,032 thousand metric tons, followed by Brazil at 10,280 thousand metric tons, and Canada at 1,411 thousand metric tons.

Asia-Pacific Dominates the Market

- With rapid economic growth, the demand for meat protein is rising in Asia, especially in China, India, Malaysia, Vietnam, and Thailand. This increased demand for meat protein has triggered meat production in the region, where uptake of compound feed has increased and is expected to show a higher growth rate. Apart from improving nutritional value, compound feed is gaining importance in improving meat quality.

- The compound feed industry in China has risen tremendously over recent years. According to a survey by Alltech, the feed output in China had increased significantly last year, making it the country with the highest increase in feed production by tonnage. China is the leading country in feed production in the region, accounting for 261.42 million metric tons, followed by India, with 44.05 million metric tons during the year 2021.

- India ranked first in cattle and buffalo population last year. It was the largest producer of milk and buffalo meat, followed by the second-largest producer of goat meat and the third-largest poultry producer. India produced 122.04 billion poultry eggs in the year 2021. The major growth drivers are breed improvement, low organic feed market, penetration, increasing formal offtake, etc.

- According to industry sources included in a study by the United States Department of Agriculture (USDA), in the year 2021, corn and soybean meal dominated the commercial feed market in India, with other coarse grains such as limited quantities of spoiled/lower quality wheat and other oilseed meals supplementing the market depending on comparative pricing. Therefore, an increase in domestic consumption of protein-based products in Asian countries, various promotional initiatives by the industries, and the decline of the African swine fever (ASF) in various nations are some of the essential factors expected to boost the growth of the market studied in the coming years.

Feed Phosphate Industry Overview

The feed phosphate market is moderately consolidated, with a few active players, including The Mosaic Company, Eurochem, Potash Corp, PhosAgro, and OCP Group, occupying a considerable market share in 2022. These companies focus on expanding their businesses and undertaking strategies like mergers and acquisitions, expansions, and novel product innovations. Leading companies focused on acquiring feed mills and small manufacturing to expand their business in local and foreign markets. These companies focused on the expansion of the business across regions and setting up a new plant for increasing production capacity as well as a product line. The companies are also increasing the production capacities of their existing plants.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Feed Type

- 5.1.1 Monocalcium Phosphate

- 5.1.2 Dicalcium Phosphate

- 5.1.3 Mono-Dicalcium Phosphate

- 5.1.4 Tricalcium Phosphate

- 5.1.5 Defluorinated Phosphate

- 5.1.6 Other Feed Types

- 5.2 Livestock Type

- 5.2.1 Poultry

- 5.2.2 Swine

- 5.2.3 Cattle

- 5.2.4 Aquatic Animals

- 5.2.5 Other Livestock Types

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Rest of Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 The Mosaic Company

- 6.3.2 EuroChem

- 6.3.3 Simphos

- 6.3.4 Fosfitalia

- 6.3.5 Timab Industries

- 6.3.6 Yara International ASA

- 6.3.7 OCP Group

- 6.3.8 PhosAgro

- 6.3.9 Potash Corporation