|

|

市場調査レポート

商品コード

1444429

半導体シリコンウエハー:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Semiconductor Silicon Wafer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 半導体シリコンウエハー:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

半導体シリコンウエハー市場規模は、2024年に139億3,000万米ドルと推定され、2029年までに168億1,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に3.82%のCAGRで成長します。

主なハイライト

- 半導体シリコンウエハーは、依然として多くのマイクロ電子デバイスの中核コンポーネントであり、エレクトロニクス産業の基礎を形成しています。デジタル化と電子モビリティが技術情勢における現在の動向であるため、これらの製品は多くのデバイスに応用されています。また、小型ガジェットの需要により、単一デバイスにより多くの機能を求めるニーズが高まっています。これは、より多くの機能をサポートするには、ICチップにさらに多くのトランジスタを搭載する必要があることを意味します。

- 国際半導体製造装置材料協会(SEMI)によると、COVID-19の影響を巡る不確実性が高まる中、シリコンウエハー市場の売上高は低迷する可能性があるとのことです。しかし、チップ売上の回復により需要は増加しました。 SEMIはまた、世界のシリコンウエハー出荷量が2022年に過去最高に達すると予測しています。中国での最初のCOVID-19感染症の発生により、同国のサプライチェーンと生産が混乱しました。過去20~30年で中国が世界の生産拠点となったことにより、主要な半導体製造業界は大きな影響を受けています。

- 半導体産業は、エレクトロニクス、自動車、オートメーションなどの重要な分野における重要なイノベーションの背後にある重要な推進力であり、半導体技術はすべての現代技術の構成要素として台頭しています。この分野の進歩と革新は、すべての下流技術に即座に影響を与えています。

- ファウンドリは、新しい先進パッケージング技術、特にシリコンウエハーベースへの投資を増やしています。ファウンドリベンダーは、モノリシック 3D集積回路を開発するチャネルとしてシリコンの代わりに2次元材料を利用するなどの技術を使用して、トランジスタ密度を向上させる研究を行っています。たとえば、TSMCのチップ・オン・ウエハー・オン・サブストレート技術は、パッケージ内に8個のHBMメモリデバイスと組み合わせた2つの巨大プロセッサ用のスペースを備えた世界最大のシリコンインターポーザを開発しました。

- ウェアラブルデバイスの進歩は、市場ベンダーに大きな成長機会をもたらします。シーメンスによると、産業用ウェアラブルは加工産業の品質と安全性を向上させるため、巨大な市場になる可能性があります。 Zebra Technologies Corporationによると、世界中の製造業者の40~50%が2022年までにウェアラブルを採用すると予想されています。また、小型ガジェットの需要により、単一のデバイスからより多くの機能を求めるニーズが高まっています。これは、より多くの機能をサポートするには、ICチップにさらに多くのトランジスタを搭載する必要があることを示しています。

- 中国のような新興国全体にわたる政府の有利な政策は、半導体業界に多大な機会をもたらし、予測期間中に半導体シリコンウエハー市場が拡大すると予想されています。たとえば、中華人民共和国国務院が発表した政策枠組みは、先進的な半導体パッケージングソリューションを半導体業界全体の技術優先事項にすることを目的としています。

半導体シリコンウエハー市場動向

家庭用電化製品部門はかなりの市場シェアを占めると予想される

- 現在の市場シナリオでは、ラップトップ、スマートフォン、コンピューターなどを含む多くの電子機器は依然としてシリコン物質から製造されたICやその他の半導体デバイスを使用しています。家庭用電化製品市場では依然としてシリコンが主な用途を支配していますが、いくつかの用途では新しい材料が以前の基板やパッケージに取って代わりました。

- Consumer Technology Association(CTA)の「米国消費者技術売上と予測」調査によると、CTAは5G対応スマートフォンデバイスが210万台に達し、売上高が19億米ドルを超え、2021年まで3桁の増加を示すと予想しています。Appleは、 2023年までに米国経済に3,500億米ドルの貢献を約束し、今後5年間で240万人の雇用を約束しており、これには新規投資と供給と製造のための国内企業への既存支出が含まれます。同社は家庭用電化製品業界の著名な企業です。したがって、この発表により半導体シリコンウエハーの需要が促進されることが期待されます。

- 最近、シンガポールのMITの調査企業であるシンガポール-MIT調査技術連合(SMART)は、設計に強力な性能のIII-Vデバイスを挿入した統合シリコンIII-Vチップを製造する商業的に実行可能な方法の開発に成功したと発表しました。

- 現在のほとんどのデバイスでは、シリコンベースのCMOSチップが主にコンピューティングに使用されていますが、通信や照明には効率的ではないため、効率が低くなり、発熱が生じます。したがって、現在市販されている5Gモバイルデバイスは使用中に非常に熱くなり、しばらくするとシャットダウンしてしまいます。しかし、商業的に実行可能な方法でIII-V族半導体デバイスとシリコンを組み合わせるのは、半導体産業が直面する最も複雑な課題の1つです。

北米が大きなシェアを占めると予想される

- 半導体ファウンドリやウエハープレーヤーにとってファブレス半導体企業が主要な顧客であるため、北米は2021年までに市場への収益に大きく貢献すると予想されています。ファブレス企業はチップ設計を独占的に行い、製造工場を持たずに販売します。

- この地域の主要なファブレス企業は、AMD、Broadcom、Apple、Qualcomm、Marvell、NVIDIA、Xilinxです。北米は、先進的な半導体システムの設計と製造において重要な役割を果たしてきました。この地域では、半導体ウエハーファウンドリの設立活動が活発化しています。 TSMCは、先進的な5nmプロセスを使用してチップを製造するための12インチウエハー工場を建設するために、2021年から2029年までに総額120億米ドルを費やすと発表しました。さらに、外国企業に米国への投資と雇用創出を迫ったドナルド・トランプ氏がジョー・バイデン氏に離反された後も、ハイテクサプライチェーンは変化し続けると思われます。

- この地域のエレクトロニクス産業は着実に成長しており、設計およびファブレス分野で活動するいくつかの企業で顕著なシェアを占めています。米国国勢調査局によると、2019年の米国における半導体およびその他の電子部品の業界収益は1,000億8,000万米ドルで、2023年までに1,051億6,000万米ドルに達すると予想されています。スマートフォンは半導体消費に最も大きく貢献しているもの1つです。家庭用電化製品分野で。近年、この地域ではスマートフォンの売上が一貫して増加しています。

- さらに、米国は世界の主要な自動車企業の本拠地であり、高性能ICを必要とする電気自動車や自動車の自動運転の可能性に投資しています。これは、半導体シリコンウエハー市場の需要を促進する主要な要因の1つです。

半導体シリコンウエハー業界の概要

半導体シリコンウエハー市場は非常に競争が激しいです。市場シェアの点では、少数のプレーヤーのみが現在の市場を独占しているため、市場はかなり統合されています。しかし、プレーヤーの今後の技術と実行されたイノベーションが、半導体シリコンウエハー市場の大幅な押し上げの背後にある理由です。市場では、企業が地理的な存在感を拡大するために、複数の合併や提携も行われています。

- 2022年3月-SKシルトロン社は、亀尾国家産業団地3にある300mmウエハー設備の拡張のため、今後3年間で1兆500億ウォンを投資することを決定したと発表しました。同社は2022年に拡張工事を開始、2024年に量産開始する予定です。

- 2022年 1月- 世界有数のシリコンウエハーサプライヤーの1つであるGlobalWafers Co.は、地元の工場から毎月約20,000枚の高度な12インチウエハーを追加しました。世界ウェーファーズは、旺盛な需要を満たすための拡張の結果、韓国、日本、台湾、イタリアの工場の生産能力が10~15%増加すると推定しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場力学

- 市場概要

- 業界のバリューチェーン分析

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

- 市場促進要因

- 非伝統的なエンドユーザー業種からの需要の拡大とウェアラブル売上の着実な増加

- 市場の課題

- 高コストとエンドユーザーの需要の動的な性質により、生産者が直面する運営上の課題

- シリコンウエハーのコストに関する主な考慮事項

- COVID-19による半導体シリコンウエハー業界への影響

第5章 市場セグメンテーション

- 直径別

- 150mm未満

- 200mm

- 300mm以上(450mm等)

- 製品別

- ロジック

- メモリ

- アナログ

- その他の製品

- 用途別

- 家電

- モバイル・スマートフォン

- デスクトップ、ノートブック、サーバーPC

- 産業

- 通信

- 自動車

- その他の用途

- 家電

- 地域別

- 北米

- 欧州

- アジア太平洋地域

第6章 競合情勢

- 企業プロファイル

- Shin-Etsu Handotai

- Siltronic AG

- SUMCO Corporation

- SK Siltron Co. Ltd

- Globalwafers Co.Ltd

- SOITEC SA

- Okmetic Inc.

- Wafer Works Corporation

- Episil-Precision Inc.

第7章 中国の主要ベンダーと利害関係者の分析

- Zing Semiconductor Corporation (Shanghai)

- MCL Electronic Material Limited

- GrinM Semiconductor Materials Limited

- Shanghai Simgui Technology Co. Limited

- Ferrotec (Hangzhou & Shenhe FTS)

- Zhonghuan Semiconductor Corporation

第8章 投資分析

第9章 市場の将来

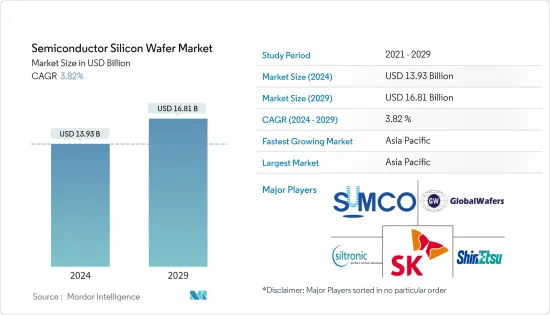

The Semiconductor Silicon Wafer Market size is estimated at USD 13.93 billion in 2024, and is expected to reach USD 16.81 billion by 2029, growing at a CAGR of 3.82% during the forecast period (2024-2029).

Key Highlights

- Semiconductor silicon wafer remains the core component of many microelectronic devices and forms the cornerstone of the electronics industry. With digitization and electronic mobility being the current trends in the technology landscape, these products are finding applications in many devices. Also, the demand for small-sized gadgets has increased the need for more functionalities from a single device. This means that an IC chip should now house more transistors to support more features.

- According to the Semiconductor Equipment and Materials International (SEMI), silicon wafer market sales could witness a dip amidst the looming uncertainty surrounding the impact of COVID-19. However, the demand climbed on the strength of rebounding chip sales. SEMI also estimates that silicon wafer shipments globally will reach a record high in 2022. The initial outbreak of COVID-19 in China disrupted the country's supply chain and production. Major semiconductor manufacturing industries have been significantly affected due to China becoming a world production center over the past two to three decades.

- The semiconductor industry has been a significant driver behind critical innovations in significant sectors like electronics, automobiles, and automation, with semiconductor technology emerging as the building block of all modern technologies. The advancements and innovations in this field are immediately impacting all downstream technologies.

- Foundries are increasingly investing in new advanced packaging techniques, especially silicon wafer-based. Foundry vendors are researching improving transistor density with techniques like utilizing two-dimensional materials instead of silicon as the channel to develop Monolithic 3D Integrated Circuits. For instance, TSMC's chip on wafer on Substrate technology developed the world's largest silicon interposer that featuring room for two massive processors combined with 8 HBM memory devices in a package.

- Advancements in wearable devices will create massive growth opportunities for market vendors. According to Siemens, industrial wearables could be a massive market as these devices enhance quality and safety in the processing industry. According to Zebra Technologies Corporation, 40-50% of manufacturers globally are expected to adopt wearables by 2022. Also, the demand for small-sized gadgets has raised the need for more functionalities from a single device. This indicates that an IC chip should now house more transistors to support more functionalities.

- Favorable government policies across emerging economies like China created enormous opportunities for the semiconductor industry, which is expected to expand the semiconductor silicon wafer market during the forecast period. For instance, the policy framework published by the State Council of the People's Republic of China aims to make advanced semiconductor packaging solutions a technology priority across the semiconductor industry.

Semiconductor Silicon Wafer Market Trends

The Consumer Electronics Segment is Expected to Occupy a Significant Market Share

- In the current market scenario, many electronic devices, including laptops, smartphones, computers, etc., still use ICs and other semiconductor devices manufactured from silicon substances. Although silicon is still dominating primary applications in the consumer electronics market, new materials have replaced the previous substrates and packaging for a few uses.

- According to the Consumer Technology Association's (CTA) 'US Consumer Technology Sales and Forecast' study, CTA expects that 5G-enabled smartphone devices will reach 2.1 million units and cross USD 1.9 billion in revenue with triple-digit increases through 2021. Apple announced a contribution of USD 350 billion to the US economy by 2023 and promised 2.4 million jobs over the next five years, which comprises new investments and its existing spending with domestic companies for supply and manufacturing. The company is a prominent player in the consumer electronics industry. Hence, the announcement is expected to propel the demand for semiconductor silicon wafers.

- Recently, the Singapore-MIT Alliance for Research and Technology (SMART), MIT's research enterprise in Singapore, announced the successful development of a commercially viable way to manufacture integrated silicon III-V chips with powerful performance III-V devices inserted into their design.

- In most devices nowadays, silicon-based CMOS chips are primarily used for computing, but they are not efficient for communications and illumination, resulting in low efficiency and heat generation. Thus, current 5G mobile devices on the market get very hot upon use and shut down after a short time. However, combining III-V semiconductor devices with silicon in a commercially viable way is one of the most complex challenges the semiconductor industry faces.

North America is Expected to Hold a Significant Share

- North America is expected to be a significant revenue contributor to the market by 2021, as fabless semiconductor companies are the prominent customers for semiconductor foundries and wafer players. Fabless companies make chip designs exclusively and market them without a fabrication plant.

- The major fabless companies in the region are AMD, Broadcom, Apple, Qualcomm, Marvell, NVIDIA, and Xilinx. North America has presented a crucial role in advanced semiconductor system design and manufacturing. The region has been witnessing increased activity in establishing semiconductor wafer foundries. TSMC announced that it would spend a total of USD 12 billion from 2021 to 2029 to build a 12-inch wafer plant to manufacture chips using the advanced 5 nm process. Moreover, tech supply chains will continue to shift even after Donald Trump, who pressed foreign companies to invest and create jobs in America, was defected by Joe Biden.

- The electronics industry in the region has been growing steadily and holds a prominent share in several enterprises operating in the design and fabless space. According to the US Census Bureau, the industry revenue of semiconductors and other electronic components in the United States during 2019 stood at USD 100.08 billion, and it is expected to reach USD 105.16 billion by 2023. Smartphones are among the most significant contributors to semiconductor consumption in the consumer electronics sector. In recent years, the region has witnessed consistent growth in smartphone sales.

- Moreover, the United States is home to some of the world's major automotive players, which are investing in electric vehicles and the self-driving potential of cars, which demand high-performance ICs. This is one of the major factors driving the demand for the semiconductor silicon wafers market.

Semiconductor Silicon Wafer Industry Overview

The Semiconductor Silicon Wafer Market is quite competitive. In terms of market share, only a few players dominate the current market, due to which the market is quite consolidated. However, players' upcoming technologies and the innovations carried out are the reason behind the significant boost in the semiconductor silicon wafers market. The market is even witnessing multiple mergers and partnerships so that the companies expand their geographical presence.

- March 2022 - SK Siltron Co. announced that it has decided to invest won 1.05 trillion over the next three years to expand its facilities for 300 mm wafers, which are located in Gumi National Industrial Complex 3. The company will begin the expansion work in 2022 to start mass production in 2024.

- January 2022 - GlobalWafers Co., one of the global leading silicon wafer suppliers, added around 20,000 advanced 12-inch wafers each month from local fabs. GlobalWafers estimates capacity to rise 10-15% at plants in South Korea, Japan, Taiwan, and Italy as a result of the expansions to satisfy strong demand.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Market Drivers

- 4.4.1 Growing Demand from Non-Traditional End-User Verticals and Steady Rise in Wearable Sales

- 4.5 Market Challenges

- 4.5.1 Operational Challenges Faced by the Producers Owing to High Cost and Dynamic Nature of End-User Demand

- 4.6 Key Cost Considerations for Silicon Wafer

- 4.7 Impact of COVID-19 on the Semiconductor Silicon Wafer Industry

5 MARKET SEGMENTATION

- 5.1 By Diameter

- 5.1.1 Less than 150 mm

- 5.1.1.1 By Product (Logic, Memory, Analog, and Other Products)

- 5.1.1.2 Vendor Ranking Analysis

- 5.1.2 200 mm

- 5.1.3 300 mm and above (450mm, etc.)

- 5.1.1 Less than 150 mm

- 5.2 By Product

- 5.2.1 Logic

- 5.2.2 Memory

- 5.2.3 Analog

- 5.2.4 Other Products

- 5.3 By Application

- 5.3.1 Consumer Electronics

- 5.3.1.1 Mobile/Smartphones

- 5.3.1.2 Desktop, Notebook, and Server PCs

- 5.3.2 Industrial

- 5.3.3 Telecommunication

- 5.3.4 Automotive

- 5.3.5 Other Applications

- 5.3.1 Consumer Electronics

- 5.4 By Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Shin-Etsu Handotai

- 6.1.2 Siltronic AG

- 6.1.3 SUMCO Corporation

- 6.1.4 SK Siltron Co. Ltd

- 6.1.5 Globalwafers Co.Ltd

- 6.1.6 SOITEC SA

- 6.1.7 Okmetic Inc.

- 6.1.8 Wafer Works Corporation

- 6.1.9 Episil-Precision Inc.

7 ANALYSIS OF KEY CHINESE VENDORS AND STAKEHOLDERS

- 7.1 Zing Semiconductor Corporation (Shanghai)

- 7.2 MCL Electronic Material Limited

- 7.3 GrinM Semiconductor Materials Limited

- 7.4 Shanghai Simgui Technology Co. Limited

- 7.5 Ferrotec (Hangzhou & Shenhe FTS)

- 7.6 Zhonghuan Semiconductor Corporation