|

市場調査レポート

商品コード

1444352

ディスティラーズグレイン(DDGS)飼料:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Distiller's Dried Grains with Solubles (DDGS) Feed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ディスティラーズグレイン(DDGS)飼料:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 159 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

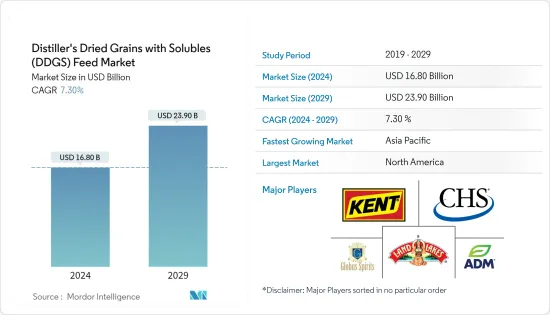

ディスティラーズグレイン(DDGS)飼料の市場規模は、2024年に168億米ドルと推定され、2029年までに239億米ドルに達すると予測されており、予測期間(2024年から2029年)中に7.30%のCAGRで成長します。

主なハイライト

- DDGS飼料市場は、その栄養価、畜産業からの需要、費用対効果の高い栄養素の必要性により成長しています。蒸留穀物は優れたエネルギー源であり、多くの場合、総可消化栄養素(TDN)の85%~95%をテストします。エネルギーの形態も、放牧牛にとって蒸留穀物を魅力的なものにします。でんぷんが除去されるため、蒸留穀物から得られるエネルギーは主に消化可能な繊維と脂肪になります。

- トウモロコシは世界中でDDGSの主な供給源です。一般に、トウモロコシの凝縮した蒸留器可溶分は、可溶分を含む湿式または乾式蒸留器グレインを製造するプロセス中に粗粒に加え戻されます。トウモロコシの凝縮蒸留可溶物の栄養プロファイルは、低品質の飼料を与えられた肉牛にとって有用なサプリメントとなります。 DDGSは主に肉牛、乳牛、豚、家禽に与えられます。

- さらに、飼料コストは総生産コストの60%から70%を占めており、ブロイラー食における代替飼料成分の評価が正当化されます。蒸留乾燥穀物可溶物(DDGS)は、特に家禽の飼料における代替成分です。このDDGS飼料の低コストが市場の原動力となっています。 DDGS市場の主な制約には、一部の新興諸国における知識不足、穀物の価格変動、過剰消費による悪影響などがあります。

ディスティラーズグレイン(DDGS)市場動向

家畜からの需要の増加

DDGSが経済的な動物飼料原料であるかどうかを決定する主な要因の1つは、トウモロコシや大豆粕などの代替オプションの価格と入手可能性です。DDGSはこれらの代替オプションの部分的な代替品であるためです。 DDGSミールは、栄養価と価格の点でトウモロコシに似ています。さらに、健康上の利点と飼料栄養素の改善により、可溶性成分を含む蒸留乾燥穀物の需要が世界市場で増加しました。牛の配合飼料中のDDGSは、乳量の増加とそれに含まれる脂肪とタンパク質の含有量に影響を与えます。コーンミールの価格が高い国は、DDGSにとって理想的な市場となる可能性があります。

DDGSの主なユーザーは乳製品業界と牛肉業界です。最近、養豚産業におけるDDGSの使用が劇的に増加し始め、程度は低いですが養鶏産業でも使用されています。米国穀物評議会によると、授乳期の牛の飼料に20~30%のDDGSを添加すると、DDGSを含まない飼料を与えた場合と同等以上の乳生産量が得られます。米国、中国、インドは、多くの牛やその他の反芻動物の個体群が存在するため、反芻動物の飼料の最大の生産国です。たとえば、農務省によると、2021年の牛と子牛の頭数は9,380万頭で、2017年の9,370万頭から増加しました。これは頭数の増加を示しており、それによって飼料消費量が増加しています。米国などの家畜生産が多い地域では、ここ数年 DDGSの需要が見られます。したがって、動物の個体数が多いことによる牛乳と肉の供給量の増加には、DDGS市場の成長を助ける高い飼料比率が必要です。

北米がDDGS市場を独占

北米は引き続き、トウモロコシをベースとしたディスティラーズグレイン(DDGS)飼料の最大の市場を有しています。 DDGSは蒸留所業界の共同産物です。北米のDDGSの大部分(約98%)は、バイオ燃料産業用のエタノールを生産する乾式粉砕プラントから来ています。米国は国内でバイオ燃料が大量に生産されているため、市場を独占しています。米国穀物評議会によると、米国のエタノール工場は150億ガロン以上のエタノールと4,400万トンのDDGSを生産する能力を有しており、これと並行してDDGS市場の拡大を推進しています。これは、エタノール工場が食品安全近代化法(FSMA)で義務付けられている予防管理要件に確実に準拠していることを保証する米国食品医薬品局の規制監督のおかげであると考えられます。この連邦規則は、施設が動物用食品の生産において危険のない安全な製造慣行に従うことを義務付けています。これらの予防管理は、米国のエタノール製品別が引き続き安全な飼料原料であることを世界中の購入者に正式に保証するものです。

米国はDDGSの生産だけでなく輸出でもリードしています。メキシコは、2021年にそれぞれ4,400万トンと1,100万トンで、生産と輸出の大きなシェアを占めていました。メキシコは現在、米国DDGSの最大の買い手となっており、これは北米自由貿易協定(NAFTA)によって可能になったものです。市場開拓措置と貿易相互関係を通じて。

ディスティラーズグレイン(DDGS)業界の概要

DDGS飼料市場は統合されており、数社が市場シェアの大部分を占めています。米国とブラジルがDDGSの主要生産国ですが、他のほとんどの国は輸入しています。したがって、主要企業はより安価な輸送戦略に焦点を当てています。 DDGS飼料市場の主要企業は、Archer Daniels Midland Company、CHS Nutrition Inc.、Globus Spirits、Kent Nutrition Group、Land O'Lakes Inc.です。これらの主要企業は、新製品の発売と即興、および事業拡大のための買収に投資しています。もう1つの主要な投資分野は、新製品を低価格で発売するための研究開発に重点を置くことです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- タイプ

- トウモロコシ

- 小麦

- 米

- アミノ酸

- ブレンド穀物

- その他のタイプ

- 動物タイプ

- 乳牛

- 肉牛

- 豚

- 家禽

- その他動物タイプ

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- タイ

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東とアフリカ

- 南アフリカ

- その他中東およびアフリカ

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- Archer Daniels Midland Company

- Globus Spirits

- Nugen Feeds and Foods

- Crop Energies

- CHS Nutrition Inc.

- Kent Nutrition Group

- Land O'Lakes Inc.

第7章 市場機会と将来の動向

The Distiller's Dried Grains with Solubles Feed Market size is estimated at USD 16.80 billion in 2024, and is expected to reach USD 23.90 billion by 2029, growing at a CAGR of 7.30% during the forecast period (2024-2029).

Key Highlights

- The DDGS feed market is growing due to its nutrient value, demand from the livestock industry, and the need for cost-effective nutrients. Distiller grains are an excellent energy source, often testing between 85% and 95% of total digestible nutrients (TDN). The form of energy also makes distiller grains attractive for grazing cattle. Since the starch is removed, the energy derived from the distiller's grains is primarily digestible fiber and fat.

- Corn is the primary source of DDGS worldwide. Generally, corn condensed distiller solubles are added back to the coarse grains during the process to produce wet or dry distiller grains with solubles. The nutrient profile of corn condensed distiller solubles makes them a useful supplement for beef cattle fed low-quality forage diets. DDGS is primarily fed to beef cattle, dairy cattle, swine, and poultry.

- Moreover, feed cost represents between 60% and 70% of the total production costs, which warrants the assessment of alternative feed ingredients in broiler diets. Distiller's dried grains with solubles (DDGS) are an alternative ingredient, especially in poultry diets. This low cost of the DDGS feed is a driving factor for the market. Some of the major constraints of the DDGS market are lack of knowledge in some developing countries, price volatility of the grains, and ill effects of excess consumption.

Distiller's Dried Grains with Solubles (DDGS) Market Trends

Increasing Demand from Livestock

One of the prime factors determining whether DDGS is an economical animal feed ingredient is the price and the availability of alternate options, like corn and soybean meal, as DDGS is a partial replacement for those alternate options. DDGS meal is more like corn in terms of nutritional value and price. Additionally, the demand for distiller's dried grains with solubles increased in the global market due to the health benefits and improvement in feed nutrients. DDGS in compound feeds for cattle influences the growth of milk yield and the fat and protein content in it. Countries with high prices of cornmeal may act as ideal markets for DDGS.

The primary users of DDGS are the dairy and beef industries. Recently, the usage of DDGS in the swine industry began to increase dramatically and, to a lesser extent, in the poultry industry. According to the US Grains Council, adding 20-30% DDGS to a lactating cow diet results in milk production equal to or greater than when diets containing no DDGS are fed. The United States, China, and India are the largest producers of ruminant feed due to the presence of many cattle and other ruminant populations in these countries. For instance, according to USDA the population of cattle and calves in 2021 is 93.8 million which increased from 93.7 million in 2017. This showed an increase in the population, thereby increasing feed consumption. Regions with high livestock production, such as the United States, have been witnessing demand for DDGS for the last few years. Therefore, the increased supply of milk and meat due to the high populations of animals needs high feed ratios which aid the growth of the DDGS market.

North America Dominates the DDGS Market

North America continues to have the largest market for corn-based distillers' dried grains with solubles. DDGS is a co-product of the distillery industries. The majority (~98%) of the DDGS in North America comes from dry-grind plants that produce ethanol for the biofuel industry. The United States dominates the market due to the extensive biofuel production in the country. According to the US Grain council, the United States ethanol plants possess the capacity to produce more than 15 billion gallons of ethanol and 44 million metric tons of DDGS driving the parallel expansion of the DDGS market. This can be attributed to the regulatory oversight of the US Food and Drug Administration, which ensures that ethanol plants comply with preventive control requirements as mandated by the Food Safety Modernization Act (FSMA). This federal rule requires facilities to follow hazard-free and safe manufacturing practices for animal food production. These preventive controls provide a formal assurance to buyers worldwide that American ethanol co-products continue to be safe feed ingredients.

The United States leads in the production as well as exports of DDGS. It had a major share of production and export with 44 million metric ton and 11 million metric ton, respectively, in 2021. Mexico is now the top buyer of US DDGS, which has been made possible by the North American Free Trade Agreement (NAFTA) through its market development measures and trade interrelationships.

Distiller's Dried Grains with Solubles (DDGS) Industry Overview

The DDGS feed market is consolidated, with a few companies accounting for most market share. The United States and Brazil are the major producers of DDGS, while most of the other countries are importing. Thus, the focus of the main players is on a cheaper transportation strategy. The major players in the DDGS feed market are Archer Daniels Midland Company, CHS Nutrition Inc., Globus Spirits, Kent Nutrition Group, and Land O' Lakes Inc. These major players are investing in new product launches and improvisations, and acquisitions for business expansions. Another major area of investment is the focus on R&D to launch new products at lower prices.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Corn

- 5.1.2 Wheat

- 5.1.3 Rice

- 5.1.4 Amino Acids

- 5.1.5 Blended Grains

- 5.1.6 Other Types

- 5.2 Animal Type

- 5.2.1 Dairy Cattle

- 5.2.2 Beef Cattle

- 5.2.3 Swine

- 5.2.4 Poultry

- 5.2.5 Other Animal Types

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Thailand

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Archer Daniels Midland Company

- 6.3.2 Globus Spirits

- 6.3.3 Nugen Feeds and Foods

- 6.3.4 Crop Energies

- 6.3.5 CHS Nutrition Inc.

- 6.3.6 Kent Nutrition Group

- 6.3.7 Land O' Lakes Inc.