|

市場調査レポート

商品コード

1444274

心臓血管デバイス:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Cardiovascular Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 心臓血管デバイス:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 143 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

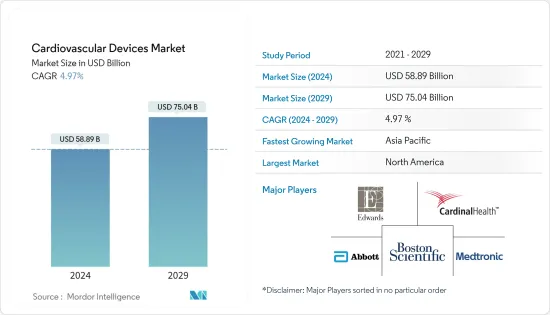

心臓血管デバイス市場規模は、2024年に588億9,000万米ドルと推定され、2029年までに750億4,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に4.97%のCAGRで成長します。

COVID-19のパンデミックの出現は、当初、心臓血管デバイス市場に打撃を与えました。ヘルスケア資源がCOVID-19感染症患者のために確保されているために心血管疾患の診断が減少し、市場に悪影響を及ぼしました。多くの医療機器企業はパンデミックにより心臓血管デバイス事業で損失を経験しています。しかし、生産施設とヘルスケア施設は再開され、市場にプラスの影響を与えることが期待されています。例えば、メドトロニックの2022年の年次報告書によると、心血管ポートフォリオからの収益の大部分を占めるテクノロジー企業は、世界の手術件数が1年目のCOVID-19感染症のパンデミックによる減少から回復したことにより収益を増加させたといいます。および2021会計年度の第2四半期。

市場を牽引する主な要因は、急速な技術進歩、さまざまな心血管疾患による世界の負担の増加、および低侵襲処置への嗜好の高まりです。心臓関連の死亡率は、心筋症や脳卒中などの心臓疾患の有病率の上昇によって引き起こされています。世界で最も一般的な病気は心血管系に関連する病気です。たとえば、カナダ心臓脳卒中財団が2022年 2月に発表した報告書によると、心不全と診断された患者数は75万人であり、この数は毎年増加しています。したがって、心臓関連疾患の適切な診断と治療のために、心臓血管デバイスは研究期間中の市場の成長を促進する重要な役割を果たします。

さらに、心臓病学用機器の開発に使用される技術は過去10年間で大幅に向上し、これらの機器の適応範囲は拡大しました。これにより、心臓病学機器で管理される患者の数が増加し、その結果、治療効果やモニタリング効果が飛躍的に向上しました。人工知能は、特定の心臓の状態を監視する機能が向上し、心臓病学に大きなプラスの影響を与える進歩の1つです。たとえば、2021年 7月にメドトロニックは、LINQ II挿入型心臓モニター(ICM)で使用する2つのAccuRhythm AIアルゴリズムについて米国FDAの認可を取得しました。 AccuRhythm AIは、LINQ IIによって収集された心拍リズムイベントデータに人工知能(AI)を適用し、医師が受け取る情報の精度を向上させ、異常な心拍リズムの診断と治療を向上させます。

しかし、厳格な規制政策と機器および処置の高コストが、心臓血管装置市場の成長を抑制する要因となっています。

心臓血管デバイスの市場動向

診断・監視機器部門の心電図(ECG)は市場で大きなシェアを握ると予想される

最新世代の軽量でコンパクトなデバイスのおかげで、診断やモニタリングの目的でECGを使用する人が増えており、ホームヘルスケア市場で特に人気があります。心血管疾患(CVD)の発生率が上昇しているため、継続的なECGモニタリングが必要です。さらに、ワイヤレス ECGの開発により、リアルタイムでの患者の監視と診断が可能になり、市場の成長に貢献しました。たとえば、フィリップスは2022年 1月に、患者の自宅で快適に実施できる分散型臨床試験で使用する12誘導心電図(ECG)ソリューションの提供を開始しました。

心臓デバイスの新技術の中でも、バンド、時計、指輪などの心臓監視機能を備えたウェアラブルスマートデバイスは、世界中の多くの人々にとって標準となっています。 2021年 2月、VivaLNKは、6分間の歩行テスト(6MWT)中にECGと心拍数をワイヤレスでキャプチャするように設計されたウェアラブルECGモニタリングソリューションを発売しました。したがって、新製品の発売と承認により、ECGの使用範囲が拡大し、調査期間を通じて市場セグメントを推進します。

さらに、心臓血管市場の主要企業間の協力により、調査期間中のこのセグメントの成長が促進されます。たとえば、2022年 10月に、AccurKardiaは、心臓領域で医療グレードのウェアラブルを提供する医療技術プロバイダーであるMawiと協力し、独自のECG分析をMawiの新しい心臓モニタリングウォッチに統合する予定です。この提携は、遠隔患者モニタリングソリューションを通じて世界クラスの心臓ケアを実現するというAccurKardiaの取り組みを強調しています。

したがって、前述の要因により、この市場セグメントは予測期間中に大幅な成長を遂げると予想されます。

北米は予測期間中に市場でかなりのシェアを握ると予想される

心血管疾患の有病率の高さ、低侵襲処置の高い採用率、償還制度の存在、高齢者人口の増加、継続的な在宅モニタリングに対する高い需要により、北米が心臓血管デバイス市場を独占すると予想されています。

2022年 10月に発行されたCDCの最新報告書によると、米国では40秒ごとに心臓発作が発生しており、毎年約805,000人のアメリカ人が心臓発作を経験しています。したがって、今後数年間で心血管疾患の負担が増大するため、心血管の診断および治療装置の需要が増加します。さらに、国内の主要な市場プレーヤーのいくつかは、既存の製品と競合する新しい製品や技術を開発しており、その他の企業は、市場で動向になっている他の企業を買収して提携しています。

たとえば、アボットは2022年 4月に、米国で心拍リズムが遅い患者の治療を目的としたAveir単腔(VR)リードレスペースメーカーの承認を米国FDAから取得しました。これは患者ケアの大幅な進歩を示し、これまでにない新しい機能を患者と医師にもたらします。同様に、2022年 2月にアボットは、心不全の初期段階に苦しむ患者のケアをサポートするCardioMEMS HFシステムの適応拡大承認を米国FDAから取得しました。これらの新製品の承認により、この地域の市場を牽引するデバイスの使用範囲が広がります。

さらに、疾患に対する意識を高めるための支援的な啓発活動が、北米地域の心臓血管デバイスの市場をサポートすると予測されています。たとえば、2022年 2月、フィリップスは、専門分野を超えた意識を高め、心臓血管植込み型電子機器(CIED)感染症からの生存率を向上させるための米国心臓協会の複数年にわたる取り組みを支援しています。したがって、上記の要因により、調査対象となった北米地域の市場は、予測期間中に大幅な成長を記録すると予想されます。

心臓血管デバイス業界の概要

心臓血管デバイス市場は適度に統合されており、競争が激しいです。大手企業は市場の特定のセグメントで地位を確立しています。さらに、企業は新興地域で世界的企業や既存の地元企業と競争しています。主要企業は、既存の製品と競合するために新しい製品や技術を開発および発売していますが、他の企業は市場で動向になっている他の企業を買収して提携しています。主要なプレーヤーには、Abbott、General Electric(GEヘルスケア)、WL Gore &Associates, Inc.、Siemensヘルスケア GmbH、Biotronik、Canon Medical Systems Corporation、B. Braun SE、LivaNova PLC、Boston Scientific Corporation、Cardinal Health、Edwardsなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 急速な技術の進歩

- 心血管疾患の負担の増大

- 低侵襲手術に対する嗜好の増加

- 市場抑制要因

- 厳格な規制政策と製品リコール

- 器具や処置にかかる費用が高い

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- デバイスタイプ

- 診断およびモニタリングデバイス

- 心電図(ECG)

- 遠隔心臓モニタリング

- その他の診断およびモニタリングデバイス

- 治療および外科用機器

- 心臓補助装置

- 心拍リズム管理デバイス

- カテーテル

- 移植片

- 心臓弁

- ステント

- その他の治療用および外科用機器

- 診断およびモニタリングデバイス

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Abbott

- Boston Scientific Corporation

- Cardinal Health

- General Electric(GE Healthcare)

- WL Gore &Associates, Inc.

- Medtronic

- Biotronik

- Siemens Healthcare GmbH

- Canon Medical Systems Corporation

- Edwards Lifesciences Corporation

- B. Braun SE

- LivaNova PLC

第7章 市場機会と将来の動向

The Cardiovascular Devices Market size is estimated at USD 58.89 billion in 2024, and is expected to reach USD 75.04 billion by 2029, growing at a CAGR of 4.97% during the forecast period (2024-2029).

The emergence of the COVID-19 pandemic hurt the cardiovascular devices market in the beginning. It had a detrimental effect on the market due to the reduction in the diagnosis of cardiovascular diseases due to healthcare resources being reserved for COVID-19 patients. Many medical device companies have experienced losses in their cardiovascular device businesses due to the pandemic. However, production and healthcare facilities got resumed which is expected to have a positive impact on the market. For instance, as per the 2022 annual report of Medtronic, a technology company having a major share of the revenue from the cardiovascular portfolio has increased revenue due to the global procedure volumes recovering from the decline brought on by the COVID-19 pandemic in the first and second quarters of the fiscal year 2021.

The major factors driving the market are rapid technological advancements, the rising global burden of various cardiovascular diseases, and increased preference for minimally invasive procedures. Heart-related mortality is caused by the rising prevalence of heart disorders such as cardiomyopathy and stroke. The most common diseases in the world are those related to the cardiovascular system. For instance, per the report published by the Heart and Stroke Foundation of Canada in February 2022, there are 750,000 patients diagnosed with heart failure and this is increasing every year. Hence for proper diagnosis and treatment of heart-related diseases cardiovascular devices play an important role that drives the market growth over the study period.

Moreover, technologies used in the development of cardiology devices have improved significantly over the past decade, and indications for these devices have expanded. This has led to an increasing number of patients being managed with cardiology devices, resulting in exponential therapeutical and monitoring outcomes. Artificial intelligence is one such advancement that has a significant positive impact on cardiology with improved capabilities for monitoring certain heart conditions. For instance, in July 2021, Medtronic received United States FDA clearance for two AccuRhythm AI algorithms for use with the LINQ II insertable cardiac monitor (ICM). AccuRhythm AI applies artificial intelligence (AI) to heart rhythm event data collected by LINQ II, improving the accuracy of information physicians receive so they can better diagnose and treat abnormal heart rhythms.

However, the stringent regulatory policies and high cost of instruments and procedures are the factors restraining the growth of the cardiovascular devices market.

Cardiovascular Devices Market Trends

The Electrocardiogram (ECG) Under Diagnostic and Monitoring Devices Segment is Expected to Hold a Significant Share in the Market

More people are using ECGs for diagnostic and monitoring purposes thanks to the latest generation of lightweight and compact devices, which are especially popular in the home healthcare market. Rising rates of cardiovascular disease (CVD) necessitate continuous ECG monitoring. In addition, the development of wireless ECG has allowed for real-time patient monitoring and diagnosis, which has contributed to the growth of the market. In January 2022, Philips, for instance, began offering a 12-lead electrocardiogram (ECG) solution for use in decentralized clinical trials that could be performed in the comfort of a patient's own home.

Among the new technologies in cardiac devices, wearable smart devices equipped with heart-monitoring capabilities, such as bands, watches, and rings, have become the norm for many people globally. In February 2021, VivaLNK launched a wearable ECG monitoring solution designed to wirelessly capture ECG and heart rate during a six-minute walk test (6MWT). Thus the new product launches and approvals increase the scope for the usage of ECG which drives the market segment over the study period.

Additionally, the collaborations among the major players in the cardiovascular market help the segment to grow over the study period. For instance, in October 2022, AccurKardia is going to collaborate with Mawi, a medtech provider of medical-grade wearables in the cardiac space, to integrate its proprietary ECG analytics into Mawi's new cardiac monitoring watch. This collaboration highlights AccurKardia's commitment to enabling world-class cardiac care through remote patient monitoring solutions.

Therefore, due to the aforementioned factors, this market segment is expected to witness significant growth during the forecast period.

North America is Expected to Hold a Significant Share in the Market During the Forecast Period

North America is expected to dominate the cardiovascular devices market due to the high prevalence of cardiovascular diseases, the high adoption rate of minimally invasive procedures, the presence of reimbursements, the rising geriatric population, and the high demand for continuous and home-based monitoring.

According to the CDC updated report published in October 2022, for every 40 seconds, a heart attack occurs in the United States, and also about 805,000 Americans experience a heart attack each year. Hence the rising burden of cardiovascular diseases in coming years increases the demand for cardiovascular diagnostics and treatment devices. Additionally, a few of the key market players in the country are developing novel products and technologies to compete with the existing products, while others are acquiring and partnering with other companies trending in the market.

For instance, in April 2022, Abbott received approval from the United States FDA for its Aveir single-chamber (VR) leadless pacemaker for the treatment of patients in the United States with slow heart rhythms. This marks a significant advancement in patient care and brings new, never-before-seen features to patients and their physicians. Similarly, in February 2022, Abbott received expanded indication approval from the United States FDA for the CardioMEMS HF System to support the care of patients suffering from earlier stages of heart failure. These new product approvals increase the scope for the usage of devices that drive the market in the region.

Furthermore, supportive awareness initiatives to create disease awareness are projected to support the market for cardiovascular devices in the North American region. For instance, in February 2022, Philips is supporting the American Heart Association's multi-year effort to generate awareness among cross-disciplinary specialties and improve survival rates from cardiovascular implantable electronic device (CIED) infections. Thus, owing to the abovementioned factors, the studied market in the North American region is expected to register significant growth over the forecast period.

Cardiovascular Devices Industry Overview

The cardiovascular devices market is moderately consolidated and competitive. The major players have established themselves in specific segments of the market. Furthermore, the companies are competing in emerging regions with global players and with established local players. Key players are developing and launching novel products and technologies to compete with existing products, while others are acquiring and partnering with other companies trending in the market. Some of the major players include Abbott, General Electric (GE Healthcare), W. L. Gore & Associates, Inc., Siemens Healthcare GmbH, Biotronik, Canon Medical Systems Corporation, B. Braun SE, LivaNova PLC, Boston Scientific Corporation, Cardinal Health, Edwards Lifesciences Corporation, and Medtronic.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Technological Advancements

- 4.2.2 Increasing Burden of Cardiovascular Diseases

- 4.2.3 Increased Preference for Minimally Invasive Procedures

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Policies and Product Recalls

- 4.3.2 High Cost of Instruments and Procedures

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 Device Type

- 5.1.1 Diagnostic and Monitoring Devices

- 5.1.1.1 Electrocardiogram (ECG)

- 5.1.1.2 Remote Cardiac Monitoring

- 5.1.1.3 Other Diagnostic and Monitoring Devices

- 5.1.2 Therapeutic and Surgical Devices

- 5.1.2.1 Cardiac Assist Devices

- 5.1.2.2 Cardiac Rhythm Management Devices

- 5.1.2.3 Catheters

- 5.1.2.4 Grafts

- 5.1.2.5 Heart Valves

- 5.1.2.6 Stents

- 5.1.2.7 Other Therapeutic and Surgical Devices

- 5.1.1 Diagnostic and Monitoring Devices

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Australia

- 5.2.3.5 South Korea

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Middle East and Africa

- 5.2.4.1 GCC

- 5.2.4.2 South Africa

- 5.2.4.3 Rest of Middle East and Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Rest of South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott

- 6.1.2 Boston Scientific Corporation

- 6.1.3 Cardinal Health

- 6.1.4 General Electric (GE Healthcare)

- 6.1.5 W. L. Gore & Associates, Inc.

- 6.1.6 Medtronic

- 6.1.7 Biotronik

- 6.1.8 Siemens Healthcare GmbH

- 6.1.9 Canon Medical Systems Corporation

- 6.1.10 Edwards Lifesciences Corporation

- 6.1.11 B. Braun SE

- 6.1.12 LivaNova PLC