|

市場調査レポート

商品コード

1444266

外科用シーラント・接着剤:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Surgical Sealant and Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 外科用シーラント・接着剤:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

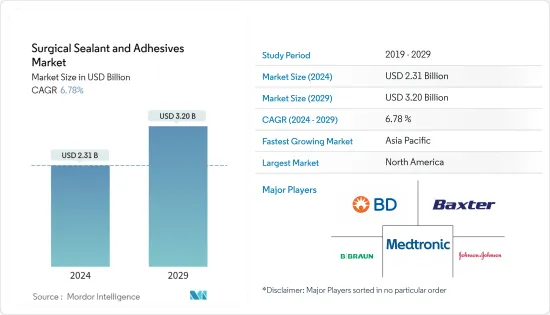

外科用シーラント・接着剤の市場規模は、2024年に23億1,000万米ドルと推定され、2029年までに32億米ドルに達すると予測されており、予測期間(2024年から2029年)中に6.78%のCAGRで成長します。

パンデミックは、さまざまな外科手術の取り組み方に影響を及ぼしました。COVID-19のパンデミック下でも外科医が安全で効果的な治療を提供し続けるために、各専門分野に厳格なガイドラインが導入され、遵守されていました。緊急でない手術はすべて避けるという規制当局の厳しいガイドラインにより、パンデミック中に手術件数は大幅に減少し、外科センターでの外科用シーラント・接着剤の調達に影響を与えました。手術が遅れ、手術件数も減少しました。 2021年10月に国立衛生研究所に掲載された論文によると、世界中で一般外科の入院が42.8%減少したといいます。 British Journal of Surgeryの報告書によると、2020年5月時点でインドでは1週間あたり約4万8,728件の外科手術がキャンセルされ、12週間で約58万5,000件の外科手術がキャンセルされたと推定されています。この外科技術の低下により、外科用シーラント・接着剤の需要が減少しました。ただし、外科治療に対する厳格なロックダウン制限が緩和された後、延期された手術が再開されたことが、予測期間中の市場の成長に貢献しました。

世界中で慢性疾患の罹患率と負担が増加しているため、外科的処置を伴う効果的で高度な治療への需要が高まっています。この要因により、世界中で行われる外科手術の数は増加しており、近いうちにさらに増加すると予想されており、研究の予測期間中に外科用シーラント・接着剤市場の成長に大きな影響を与えると予想されます。

2020年9月に発表されたNCBIの調査研究によると、世界の病気の負担の約11%は外科的治療、麻酔治療、またはその両方を必要とし、インド国民の外科的ニーズを満たすためには、推定で年間3,646件の手術が必要となると推定されています。世界の推計では、人口10万人あたり5,000件の手術が行われています。したがって、世界中で外科手術の需要が高まるにつれて、外科用シーラント・接着剤の必要性が増加し、市場の成長を促進すると予想されます。同様に、2021年 6月に発表されたNCBIの調査研究によると、合計 92,809件の手術が古典的な意味での心臓手術として分類され、そのうち29,444件が単独冠状動脈バイパス移植手術、35,469件が単独心臓弁手術であり、したがって、毎年行われる心臓処置および手術の件数が多いため、外科用シーラント・接着剤市場の成長が促進されると予想されます。

シーラントや接着剤はあらゆる手術に不可欠な部分です。それらは組織の治癒を助けるため、手術において重要な役割を果たします。慢性疾患の有病率の上昇により、ほとんどの慢性疾患の後期では手術が必要となるため、手術が増加しています。 2022年 7月のオーストラリア認知症に関する最新情報によると、2020年には45万9,000人を超えるオーストラリア人が認知症を抱えて暮らしており、約160万人がケアセンターに関わっていました。認知症患者の数は2058年までに110万人に達すると推定されており、今後5年間で認知症は国内の死因の第2位になると思われます。

近年、膝関節および股関節置換手術の件数が増加し、外科用シーラント・接着剤の需要が増加し、調査対象の市場にプラスの影響を与えています。外科手術の増加に伴い、その注文も増加すると予想され、調査対象市場は成長すると予想されます。このような外科手術の増加は、外科用シーラント・接着剤の需要を促進し、それによって市場の成長に貢献すると予想されます。

しかし、外科用シーラント・接着剤を優遇しない償還政策と代替方法の利用可能性により、外科用シーラント・接着剤市場の成長が抑制されることが予想されます。

外科用シーラント・接着剤の市場動向

一般外科セグメントが予測期間中に市場を独占すると予想される

一般外科セグメントは、市場の成長において大きなシェアを占めると予想されます。一般外科は、食道、胃、小腸、大腸、肝臓、膵臓、胆嚢、虫垂、胆管、そして多くの場合、甲状腺を含む腹部領域に焦点を当てます。一般に、皮膚、乳房、軟部組織、末梢血管外科、ヘルニアなどの疾患を扱います。腹部手術は、世界中で最も一般的な種類の手術の1つです。子宮摘出術、胆嚢手術、ヘルニア手術、前立腺摘出術、および胆嚢摘出術は、世界中で大規模な手術です。経済協力開発機構(OECD)によると、2021年にドイツとイタリアでそれぞれ約229.5件と134.6件の胆嚢摘出術が実施されました。

2020年にはドイツとイタリアでそれぞれ約113,862件と32,755件の虫垂切除術が行われました。腹部手術の件数は世界的に増加しており、市場全体の成長にプラスの影響を与えています。接着剤は一般的な手術において重要な役割を果たします。一般手術の件数が増加するにつれて、接着剤やシーラントは手術に不可欠な部分であるため、その需要と調達も増加すると予想されます。したがって、これは市場の成長を促進すると予想されます。

ヘルニア症例の世界の発生率の増加は、病院のケア現場での外科用シーラント・接着剤の需要の増加により、調査対象の市場を押し上げると予想されています。たとえば、米国麻酔科学会によると、2021年 11月に更新されたデータによると、腹壁ヘルニア修復は最も一般的な手術の1つです。米国では毎年 100万件以上のヘルニア修復が行われており、世界中でこれらの手術は年間2,000万件を超えると推定されています。このうち、鼠径ヘルニアは、米国で年間約80万件のヘルニア修復手術を占めています。したがって、このセグメントは、上記の要因により、予測期間中に大幅な成長を遂げると予想されます。

予測期間には北米が市場を独占すると予想される

北米は、予測期間を通じて市場全体を支配すると予想されます。北米地域では、米国が最大の市場シェアを占めています。これは、外科用器具の規制が改善され、怪我や慢性疾患の問題が発生した場合にそのような処置に取り組むという国民の意識が高まっているためです。

国家安全評議会(NSC)によると、2021年7月には個人運動による負傷が52万6,000件、バスケットボールによる負傷が50万人、自転車による負傷が45万7,000人、サッカーによる負傷が34万1,000件報告されました。 NSCはまた、19万9,000件の水泳傷害が緊急治療室で治療されたと述べた。脊椎、肩、頭、膝の損傷がこれらの損傷全体の50%以上を占めました。したがって、医師の診察を必要とする怪我の数が増加すると、調査対象の市場が拡大します。

さらに、疾病管理予防センターによると、2020年には米国で毎年約60万人の女性が子宮摘出術を受け、約46万人の米国居住者が胆嚢摘出術を受け、130万人の妊婦が米国を求めました。米国では外科手術が大量に行われているため、外科用シーラント・接着剤の需要が増加し、それによってこの地域で調査されている市場の成長に貢献すると予想されます。したがって、市場は、前述の要因により、予測期間中に大幅な成長を遂げると予想されます。

外科用シーラント・接着剤業界の概要

調査対象の市場は、地元企業と世界的企業が存在し、適度な競争が見られます。外科用シーラント・接着剤の大部分は国際企業が製造しています。主要なプレーヤーには、Becton, Dickinson and Company、B. Braun Melsungen AG、Baxter International Inc、Johnson &Johnson、Medtronic PLCなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 増加する外科手術

- テクノロジーの進歩

- 市場抑制要因

- 外科用シーラント・接着剤を優遇しない償還ポリシー

- 代替方法の利用可能性

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 製品別

- 天然/生物由来シーラント・接着剤

- フィブリンシーラント

- ゼラチンベース接着剤

- コラーゲンベース接着剤

- 合成・半合成接着剤

- シアノアクリレート

- 高分子ヒドロゲル

- ポリエチレングリコールポリマー

- その他

- 天然/生物由来シーラント・接着剤

- 用途別

- 一般外科

- 口腔外科

- 心臓血管外科

- 美容外科

- 脳神経外科

- 整形外科

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- B. Braun Melsungen AG

- Baxter International Inc.

- Becton, Dickinson and Company

- Cardinal Health Inc.

- Cohera Medical Inc.

- CryoLife

- CSL Limited

- Johnson &Johnson

- Medline Industries Inc.

- Medtronic PLC

- Ocular Therapeutix

- Sanofi SA

- Stryker Corporation

- Terumo Corporation

- Vivostat A/S

第7章 市場機会と将来の動向

The Surgical Sealant and Adhesives Market size is estimated at USD 2.31 billion in 2024, and is expected to reach USD 3.20 billion by 2029, growing at a CAGR of 6.78% during the forecast period (2024-2029).

The pandemic had ramifications for ways of working on various surgical procedures. There were strict guidelines for each specialty implemented and followed for surgeons to continue providing safe and effective care during the COVID-19 pandemic. The volume of surgeries significantly declined during the pandemic, owing to the stringent guidelines by regulatory authorities to avoid all non-emergent surgeries, impacting the procurement of surgical sealants and adhesives in surgical centers. The surgical procedures were delayed, and the number of surgical procedures decreased. According to the article published in the National Institute of Health in October 2021, there was a 42.8% decline in general surgery admission across the globe. According to the British Journal of Surgery report, in May 2020, around 48,728 surgical procedures per week were canceled in India, estimating about 585,000 surgical procedures for 12 weeks. This decline in surgical techniques led to decreased demand for surgical sealants and adhesives. However, the resumption of postponed surgeries after the relaxation of strict lockdown restrictions on surgical care contributed to the market's growth over the forecast period.

The increasing prevalence and burden of chronic diseases worldwide drive the demand for effective and advanced treatment involving surgical procedures. Due to this factor, the number of surgical procedures performed worldwide is increasing and further expected to rise shortly, which is expected to significantly impact the growth of the surgical sealant and adhesives market during the forecast period of the study.

As per the NCBI research study published in September 2020, about 11% of the global burden of disease requires surgical, or anesthesia care or both, and an estimated 3,646 surgeries would be required annually to meet the surgical needs of the Indian population as compared to the global estimate which is 5,000 surgeries per 100,000 people. Thus, with the rising demand for surgical procedures worldwide, the need for surgical sealants and adhesives is expected to increase, driving the market's' growth. Similarly, according to the NCBI research study published in June 2021, a total of 92,809 operations were classified as heart surgery procedures in the classical sense, of which 29,444 were isolated coronary artery bypass grafting procedures, 35,469 were isolated heart valve procedures, and the number of isolated heart transplantation increased by 2% to 340. Hence, the high number of heart procedures and surgeries performed yearly is anticipated to boost growth in the surgical sealants and adhesives market.

Sealants and adhesives are an integral part of any surgery. They play a vital role in surgeries as they help the tissues to heal. Due to the rising prevalence of chronic diseases, surgeries have increased as most chronic diseases in later stages demand surgeries. As per Dementia Australia updates from July 2022, more than 459,000 Australians were living with dementia in 2020, and about 1.6 million were involved in their center for care. It is estimated that the number of people with dementia is expected to reach 1.1 million by 2058, and dementia will become the second-leading cause of death in the country in the next five years.

The volume of knee and hip replacement surgeries increased in recent years, increasing the demand for surgical sealants and adhesives and positively impacting the market studied. With the increase in surgical procedures, their order is expected to increase, and the studied market will grow. For instance, as per the June 2021 report of the Canadian Institute of Health Information, 63,496 hip replacements and 75,073 knee replacements were performed in 2020 in Canada, and there was an average increase of about 5% in recent years in the knee and hip replacement procedures in the country. Such an increase in surgical procedures is expected to drive the demand for surgical sealants and adhesives, thereby contributing to the market's growth.

However, reimbursement policies not favoring surgical sealants and adhesives and the availability of alternative methods are expected to restrain the growth of the surgical sealant and adhesives market.

Surgical Sealants and Adhesives Market Trends

The General Surgery Segment is Expected to Dominate the Market in the Forecast Period

The general surgery segment is expected to hold a significant share of the market's growth. General surgery focuses on the abdominal area, including the esophagus, stomach, small intestine, large intestine, liver, pancreas, gall bladder, appendix, bile ducts, and often the thyroid gland. It generally deals with diseases involving the skin, breast, soft tissue, peripheral vascular surgery, and hernias. Abdominal surgery is one of the most common types of surgery worldwide. Hysterectomies, gall bladder surgeries, hernia surgeries, prostatectomies, and cholecystectomies are major surgeries worldwide. According to the Organization for Economic Cooperation and Development (OECD), in 2021, around 229.5 and 134.6 cholecystectomies were performed in Germany and Italy, respectively.

As the same source mentioned, in 2020, around 113,862 and 32,755 appendectomies were performed in Germany and Italy, respectively. The volume of abdominal surgeries is rising globally, positively impacting the overall market's growth. Adhesives play a vital role in general surgeries. Natural and synthetic polymeric materials generate threedimensional networks that physically or chemically bind to target tissues and act as hemostats, sealants, or adhesives. As the number of general surgeries increases, the demand and procurement of adhesives and sealants are expected to increase, considering they are a vital part of the surgery. Hence, this is expected to boost the market's growth.

The growing incidence of hernia cases globally is expected to boost the market studied because of the increasing demand for surgical sealants and adhesives in hospital care settings. For instance, according to the American Society of Anesthesiologists, data updated November 2021, abdominal wall hernia repair is one of the most common types of surgery. More than 1 million hernia repairs are performed each year in the United States, and worldwide these surgeries are estimated to top 20 million annually. Among these, inguinal hernias account for approximately 800,000 annual hernia repair surgeries in the United States. Thus, the segment is expected to witness significant growth over the forecast period due to the abovementioned factors.

North America is Expected to Dominate the Market in the Forecast Period

North America is expected to dominate the overall market throughout the forecast period. In the North American region, the United States holds the largest market share, and this is due to better regulations of surgical devices and growing awareness among the population to approach such procedures in case of injuries and chronic disease problems.

According to the National Safety Council (NSC), in July 2021, 526,000 injuries were reported due to personal exercise, 500,000 players were injured due to basketball, 457,000 due to bicycling, and 341,000 due to football. NSC also said that 199,000 swimming injuries were treated in the emergency room. Spine, shoulder, head, and knee injuries accounted for more than 50% of these total injuries. Thus, increasing the number of injuries requiring medical attention boosts the studied market.

Additionally, according to the Centers for Diseases Control and Prevention, in 2020, about 600,000 women in the United States had a hysterectomy every year, about 460,000 United States residents had a cholecystectomy, and 1.3 million pregnant women sought C-section in the United States. The high volume of surgical procedures in the United States is expected to drive the demand for surgical sealants and adhesives, thereby contributing to the growth of the market studied in this region. Thus, the market is expected to witness significant growth over the forecast period due to the factors mentioned earlier.

Surgical Sealants and Adhesives Industry Overview

The market studied is moderately competitive, with local and global companies. International companies manufacture the majority of surgical sealants and adhesives. Some significant players include Becton, Dickinson and Company, B. Braun Melsungen AG, Baxter International Inc, Johnson & Johnson, and Medtronic PLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Surgical Procedure

- 4.2.2 Advancement in Technology

- 4.3 Market Restraints

- 4.3.1 Reimbursement Policies not Favoring Surgical Sealants and Adhesives

- 4.3.2 Availability of Alternative Methods

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Products

- 5.1.1 Natural or Biological Sealants and Adhesives

- 5.1.1.1 Fibrin Sealant

- 5.1.1.2 Gelatin-based Adhesives

- 5.1.1.3 Collagen-based Adhesive

- 5.1.2 Synthetic and Semi-synthetic Adhesives

- 5.1.2.1 Cyanoacrylates

- 5.1.2.2 Polymeric Hydrogels

- 5.1.2.3 Polyethylene Glycol Polymer

- 5.1.2.4 Other Synthetic and Semi-synthetic Adhesives

- 5.1.1 Natural or Biological Sealants and Adhesives

- 5.2 By Application

- 5.2.1 General Surgery

- 5.2.2 Dental Surgery

- 5.2.3 Cardiovascular Surgery

- 5.2.4 Cosmetic Surgery

- 5.2.5 Neuro-surgery

- 5.2.6 Orthopaedic Surgery

- 5.2.7 Other Applications

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 B. Braun Melsungen AG

- 6.1.2 Baxter International Inc.

- 6.1.3 Becton, Dickinson and Company

- 6.1.4 Cardinal Health Inc.

- 6.1.5 Cohera Medical Inc.

- 6.1.6 CryoLife

- 6.1.7 CSL Limited

- 6.1.8 Johnson & Johnson

- 6.1.9 Medline Industries Inc.

- 6.1.10 Medtronic PLC

- 6.1.11 Ocular Therapeutix

- 6.1.12 Sanofi SA

- 6.1.13 Stryker Corporation

- 6.1.14 Terumo Corporation

- 6.1.15 Vivostat A/S