航空管制機器:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

Air Traffic Control Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 112 Pages

- 納期

- 2~3営業日

- 商品コード

- 1850123

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

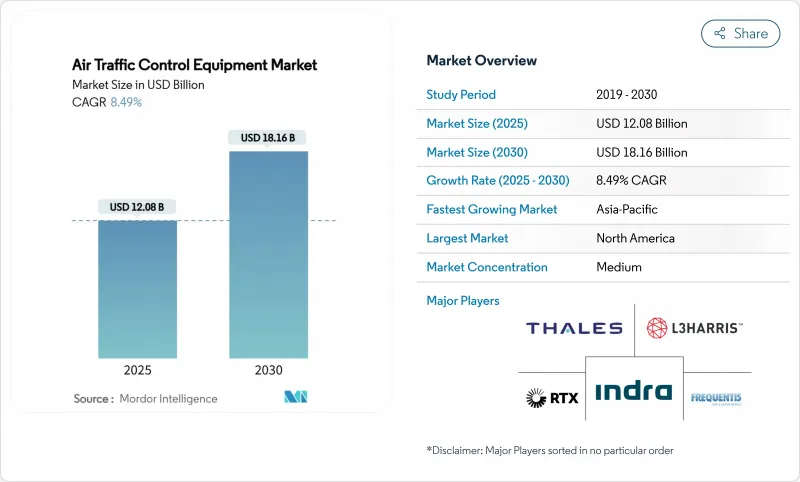

航空管制機器市場規模は2025年に120億8,000万米ドル、2030年には181億6,000万米ドルに達すると予測され、予測期間のCAGRは8.49%です。

航空管制機器市場は、各国がより多くの交通量を処理し、安全性を強化するために空域システムをアップグレードするにつれて勢いを増しています。この変化の中心にあるのが公共投資です。米国連邦航空局は、老朽化したレーダーと無線を交換するために150億米ドルを割り当て、次世代管制ネットワークの基礎を築いた。アジア各地でも、国家プログラムが同様の変化を促しています。インドの「One Airspace」計画は民間と軍事の一体化を目指すもので、中国は増加する飛行需要に対応するため、高度な監視と自動化への支出を増やしています。これらのイニシアチブは、状況認識を向上させ、交通の流れをスムーズにする自動化、デジタル化、統合化された監視に向けた幅広い動きを指し示しています。民間航空機関や防衛機関からの需要は、市場の着実な成長と継続的な技術革新を支えています。

世界の航空管制機器市場の動向と洞察

ネクストジェンとSESARによるデジタル化の波

欧州のATMマスタープランでは、2050年までに投資1単位あたり17ユーロのリターンが得られると試算され、当局がクラウドネイティブで相互運用可能なアーキテクチャに予算を振り向けるよう促しています。米国の並行するNextGenプログラムでは、衛星ベースのナビゲーション、時間ベースのフロー管理、デジタル音声スイッチングが優先され、プラットフォームサプライヤに複数年の発注が確定しました。トップクラスのベンダーは、ソフトウェアのアップデートを簡素化し、リモートメンテナンスを容易にするKubernetes対応のオープンシステムで対応しました。

ADS-B Outの義務化

12カ国が定義された空域帯のADS-Bを施行し、トランスポンダと関連する地上受信機の後付け需要を維持した。FAAはADS-Bデータを滑走路進入を削減するSurface Awareness Initiativeに活用し、450以上の空港でAeroBOSSを展開する権限をIndraに与えました。欧州では、Digital Sky枠組みの下でADS-C共通サービスを進め、監視データのエコシステムを拡大しました。

高いCAPEXと長い認証サイクル

米国政府説明責任局は、FAAシステムの37%が持続不可能であることを明らかにしたが、リプレース・プロジェクトは多くの場合、複数年にわたる認証取得のハードルに直面し、支出の引き延ばしを遅らせていました。欧州のEASA規則2023/1769はATM機器に設計組織の承認を課し、小規模サプライヤーの開発スケジュールを延長しました。

セグメント分析

通信プラットフォームは、ATC機器市場の2024年売上高の42.50%を占め、弾力性のある音声チャネルとデータリンクの重要性を強調しています。インドラがFAAから2億4,430万米ドルを獲得し、4万6,000台のデュアルモードデジタル無線機を供給したことは、老朽化したアナログ無線機の置き換えの勢いを示しています。Frequentisのようなベンダーは、世界の管制官ポジションの30%のシェアを占めており、既存プロバイダーが享受しているスケールメリットを浮き彫りにしています。

リモートタワーモジュールとデジタルタワーモジュールは、2024年の収益に占める割合は5.3%に過ぎないが、空港が複数の空港センターの下に監視を統合するにつれて、11.20%のCAGRで推移すると予測されています。この移行により、北欧の地方空港では人件費が最大30%削減され、投下資本利益率が向上し、規制当局が4Kセンサーを使用した低視認性の運航を認定するようになりました。

民間航空会社は、世界的な旅客需要の回復とADS-B装備の義務化により、ATC機器市場の2024年の収益の66.45%を生み出しました。ボーイングは、アフリカの航空機が2043年までに倍増すると予測しており、管制塔、レーダー、データリンクのアップグレードに対する下流需要が根強いことを示しています。同時に、防衛機関は調達を加速させ、2025年から2030年までのCAGR 9.85%で軍事収入を増加させました。米国空軍が19台のTPY-4レーダーを4億7,200万米ドルで発注したことは、このセグメントに流れ込む近代化契約の規模を浮き彫りにしました。

軍事用途は、重層的な防空優先事項を反映しています。サイバーセキュリティ、人工知能、UTMハードウェアをめぐる民間と防衛の要件間の収束は、サプライヤーの境界を曖昧にし、統合プラットフォームベンダーにクロスセリングの機会を開き続けています。

地域分析

北米は、デジタル音声交換、レーダー交換、管制塔建設に関するFAAの150億米ドルの青写真に支えられ、ATC機器市場の2024年の収益の40.54%を維持した。ナブ・カナダは、孤立した飛行場を遠隔管理するデジタル飛行場航空交通サービスに投資し、運用革新におけるこの地域のリーダーシップを強化しました。

アジア太平洋地域は、CAGR10.50%で最も高い成長を記録しました。インドの「一つの空域」構想は、280万海里2を一つの国家システムに統合し、中国は主要ハブ空港の新しい滑走路と同時にCNS/ATMの展開を加速させました。オーストラリアはオフサイト・タワー技術を早期に採用し、地域の勢いをさらに加速させました。

欧州はSESAR 3計画を予定通り進め、2050年までに4億トンのCO2削減を約束するデジタルスカイ・プロジェクトに300億ユーロを投入しました。中東・アフリカでは、ドバイ、リヤド、ドーハにおける1兆米ドルにのぼる空港拡張に牽引され、活発な支出が見られました。ラテンアメリカは、インドラが同地域の管制センターの70%を近代化したことで恩恵を受けたが、資金制約により成長軌道は緩やかになりました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- NextGenとSESARが資金提供するデジタル化の波

- 義務付けられたADS-B Out期限

- 二次空港におけるリモート/デジタルタワーの導入

- UAS交通管理(UTM)ハードウェアの統合

- AI駆動型予測空域管理プラットフォーム

- 軌道ベースの運用におけるグリーン飛行回廊の需要

- 市場抑制要因

- 高額な設備投資と長い認証サイクル

- レガシーシステムの相互運用性のボトルネック

- IPベースのVCSにおけるサイバーセキュリティ責任の増大

- 都市回廊のRFスペクトルの混雑

- バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 買い手の交渉力/消費者

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 機器別

- 通信機器

- ナビゲーション機器

- 監視/自動化システム

- リモート/デジタルタワーモジュール

- エンドユーザー別

- 商業用

- 軍隊

- 空港の種類別

- ブラウンフィールド空港

- グリーンフィールド空港

- 投資カテゴリー別

- 新規設置

- 近代化とアップグレード

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- その他南米

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Thales Group

- IndraSistemas S.A.

- RTX Corporation

- L3Harris Technologies, Inc.

- SITA N.V.

- Honeywell International Inc.

- Frequentis AG

- ACAMS AS

- Searidge Technologies

- Saab AB

- Rohde & Schwarz USA, Inc.(Rohde & Schwarz GmbH & Co. KG)

- General Dynamics Mission Systems, Inc.(General Dynamics Corporation)

- Leonardo S.p.A

- NEC Corporation

- Intelcan Technosystems Inc.

- Aquila Air Traffic Management Services Limited

- ARTISYS, s.r.o.

- Leidos Holdings, Inc.

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 112 Pages

- 納期

- 2~3営業日