|

市場調査レポート

商品コード

1687056

昆虫飼料:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Insect Feed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 昆虫飼料:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

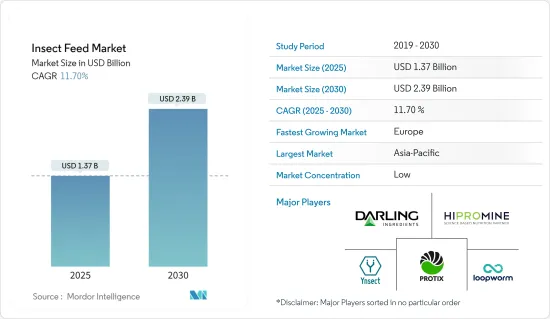

昆虫飼料の市場規模は2025年に13億7,000万米ドルと推計され、2030年には23億9,000万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは11.7%です。

養殖魚に対する世界の需要の増加は、魚粉と魚油の価格上昇につながっています。昆虫飼料は、水産飼料用のタンパク質が豊富な代替品として有効です。魚粉代替としての昆虫飼料の調査は過去20年間続けられており、養殖魚への給餌において有望な結果が得られています。ITC貿易マップによると、2023年の魚の輸入額は2,600万米ドルに達し、2021年の2,390万米ドルから8.6%増加しました。昆虫はその高いエネルギーとタンパク質含有量により、実行可能な動物飼料として認知されつつあります。昆虫飼料は新鮮な昆虫や未加工の乾燥昆虫に比べて、粉砕した穀物や大豆のような他の飼料成分と簡単に混合して希望の組成のペレットを形成できるため、より便利な動物への給餌が可能になるという利点があります。

昆虫飼料の分野は、従来の動物飼料製品に比べ商業的規模の生産が少ないです。しかし、市場の世界の需要の増加により、調査期間中に国際機関による新たな投資を含む大きな要因が観察されました。2024年6月、国際金融公社(IFC)は、コスタリカを拠点とする持続可能な昆虫ベースの動物飼料生産を専門とするProNuvo社に200万米ドルを投資しました。国際機関によるこうした投資の拡大は、市場の拡大に対する自信を示しています。さらに、昆虫の高い飼料化率、低いスペース要件、支持的な規制環境が昆虫飼料市場の成長を後押ししています。

昆虫飼料市場の動向

水産養殖における昆虫タンパク質の需要拡大

ブラックソルジャーフライ幼虫(BSFL)やミールワームなどの昆虫は、高タンパク質、必須アミノ酸、その他の栄養素を含むため、水産養殖において従来の飼料原料に代わる持続可能な選択肢を提供します。さまざまな組織や企業が昆虫ベースの養殖飼料を開発しています。2024年には、インドの中央海洋水産研究所(CMFRI)がBSFLベースの水産飼料の作成に成功し、魚の成長を改善し魚粉依存を減らすという好結果を示しました。この技術革新を進めるため、CMFRIはアマラ・エコクリーン社と提携し、この飼料をさまざまな魚種や養殖環境に適応させ、商業生産を目指しています。

アジアと欧州を中心とした世界の水産物需要の増加により拡大する養殖産業は、それに対応する高品質の飼料原料のニーズを生み出しています。この成長は、国連食糧農業機関(FAO)の「世界の漁業と水産養殖の現状(SOFIA)2024」報告書にも反映されており、それによると、世界の水産動物生産量は2022年に1億8,540万トンに達し、その79%がアジアと欧州からもたらされています。今後については、2032年までに水産動物の生産量は10%増加し、2億500万トンに達し、見かけの消費量は12%増加し、2032年には一人当たり平均21.3kgになると予測しています。これらの予測は、環境への影響を最小限に抑えながら業界の成長を支えるために、昆虫ベースの代替品など持続可能な飼料ソリューションの開発が重要であることを強調しています。

アジア太平洋が市場を独占

アジア太平洋地域では近年、食肉消費の増加が栄養価の高い昆虫飼料の需要を牽引しています。中国がこの地域の昆虫飼料市場をリードしており、食肉消費は一貫した伸びを示しています。2023年の経済協力開発機構(OECD)によると、中国、フィリピン、インドネシアの1人当たりの鶏肉消費量はそれぞれ9.9kg、9.4kg、8kgでした。栄養価の高い肉への需要の高まりに対応するため、家畜にはタンパク質が豊富な昆虫が与えられており、中国では家畜、特に家禽と豚用の昆虫飼料産業の開発が促進されています。

インドは中国に次ぐ昆虫飼料の市場となっています。食肉や食肉を主原料とする製品の需要が徐々に増加しているため、資源を大量に消費する鶏肉製品の栽培にかなりの農地が割り当てられ、栄養不良が懸念されています。この動向に対応して、Arthro Biotechのような企業が昆虫タンパク質業界の主要企業として台頭してきています。2024年、Arthro Biotech社はインド初の黒兵児蝿(BSF)昆虫タンパク質生産業者としてEU TRACES認証を取得し、現在の昆虫タンパク質の生産能力は年間500トンです。

昆虫飼料市場の成長は、この地域における企業の拡大によってさらに促進されています。特筆すべき例は、動物飼料および植物栄養用の機能性昆虫由来成分の持続可能な生産における世界的リーダーであるEntobel社です。2023年、Entobel社はベトナムにアジア最大の昆虫タンパク質生産工場を開設し、業界記録を打ち立てた。この最新鋭の施設では、高度なセンサーとデータ分析を活用し、50段階の垂直飼育でブラックソルジャーフライ(BSF)を生産しており、アジア太平洋地域で拡大する昆虫ベースの飼料需要に対応するため、業界のイノベーションと大規模生産への取り組みを実証しています。

昆虫飼料産業の概要

世界の昆虫飼料市場は断片化が特徴で、多数の新規参入企業が小さな市場シェアを握っています。以下のような主要企業が参入しています。 Hipromine SA, Protix, Loopworm, Ynsect, and Darling Ingredients Inc. dominate the market. These companies employ strategies including acquisitions, partnerships, and expansions to enhance their research capabilities and marketing efforts in the insect feed industry.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 昆虫の高い飼料化率

- 昆虫の養殖と加工における技術革新

- 持続可能な代替蛋白源への需要

- 市場抑制要因

- 規制と法的障壁

- 文化および消費者の受容

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 動物タイプ

- 水産養殖

- 家禽

- 豚

- その他の動物

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- アラブ首長国連邦

- エジプト

- その他中東とアフリカ

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- Hipromine SA

- nextProtein

- Darling Ingredients Inc.

- Protix BV

- InnovaFeed SAS

- Nasekomo AD

- Ynsect

- Beta Hatch Inc.

- Entomo Farms

- Hexafly Enterprises Limited

- Loopworm Private Limited

第7章 市場機会と今後の動向

The Insect Feed Market size is estimated at USD 1.37 billion in 2025, and is expected to reach USD 2.39 billion by 2030, at a CAGR of 11.7% during the forecast period (2025-2030).

The increasing global demand for farmed fish has led to a rise in fishmeal and fish oil prices. Insect feed serves as a viable protein-rich alternative for aquafeed. Research on insect meals as fishmeal alternatives has been ongoing for the past 20 years, with promising results in aquaculture species feeding. According to the ITC Trade Map, the import value of fish in 2023 reached USD 26 million, an 8.6% increase from USD 23.9 million in 2021. Insects are gaining recognition as viable animal feed due to their high energy and protein content. Insect feed offers advantages over fresh or unprocessed dried insects, as it can be easily mixed with other feed components like ground grains and soy to form pellets of the desired composition, enabling more convenient animal feeding.

The insect feed sector has less commercial-scale production compared to conventional animal feed products. However, significant factors, including new investments by international organizations, were observed during the study period due to the market's increasing global demand. In June 2024, the International Finance Corporation (IFC) invested USD 2 million in ProNuvo, a Costa Rica-based company specializing in sustainable insect-based animal feed production. These growing investments by international organizations demonstrate confidence in the market's expansion. Additionally, insects' high feed conversion ratio, low space requirements, and supportive regulatory environment drive the insect feed market growth.

Insect Feed Market Trends

Growing Demand for Insect Protein in Aquaculture

Insects like black soldier fly larvae (BSFL) and mealworms offer a sustainable alternative to traditional feed ingredients in aquaculture due to their high protein content, essential amino acids, and other nutrients. Various organizations and companies are developing insect-based aquaculture feeds. In 2024, India's Central Marine Fisheries Research Institute (CMFRI) successfully created a BSFL-based aquafeed, which has shown positive results in improving fish growth and reducing fishmeal dependency. To advance this innovation, CMFRI has partnered with Amala Ecoclean to adapt the feed for different fish species and farming environments, aiming for commercial production.

The expanding aquaculture industry, driven by increasing global seafood demand, particularly in Asia and Europe, is creating a corresponding need for high-quality feed ingredients. This growth is reflected in the Food and Agriculture Organization of the United Nations (FAO) State of World Fisheries and Aquaculture (SOFIA) 2024 report, which states that global aquatic animal production reached 185.4 million metric tons in 2022, with 79% originating from Asia and Europe. Looking ahead, the report forecasts a 10% increase in aquatic animal production by 2032, reaching 205 million tonnes, and a 12% rise in apparent consumption, providing an average of 21.3 kg per capita in 2032. These projections underscore the importance of developing sustainable feed solutions, such as insect-based alternatives, to support the industry's growth while minimizing environmental impact.

Asia-Pacific Dominates the Market

In Asia-Pacific, increasing meat consumption has driven demand for nutritious insect feed in recent years. China leads the region's insect feed market, with meat consumption showing consistent growth. According to the Organization for Economic Co-operation and Development (OECD) in 2023, the per capita consumption of poultry meat in China, the Philippines, and Indonesia was 9.9 kg, 9.4 kg, and 8 kg respectively. To meet the growing demand for nutritious meat, livestock is being fed protein-rich insects, fostering the development of the insect feed industry for livestock, particularly poultry and swine, in China.

India ranks as the second-largest market for insect feed after China. The gradual increase in demand for meat and meat-based products has raised concerns about malnutrition, as significant areas of farmland are allocated to grow resource-intensive poultry products. In response to this trend, companies like Arthro Biotech are emerging as key players in the insect protein industry. In 2024, Arthro Biotech became the first Indian black soldier fly (BSF) insect protein producer to receive EU TRACES Certification, with a current production capacity of 500 metric tons of insect protein per annum.

The growth of the insect feed market is further propelled by the expansion of companies in the region. A notable example is Entobel, a global leader in the sustainable production of functional insect-based ingredients for animal feed and plant nutrition. In 2023, Entobel set an industry record by opening the largest insect protein production plant in Asia, located in Vietnam. This state-of-the-art facility produces black soldier fly (BSF) in 50 levels of vertical rearing, utilizing advanced sensors and data analytics, demonstrating the industry's commitment to innovation and large-scale production to meet the growing demand for insect-based feed in the Asia-Pacific region.

Insect Feed Industry Overview

The global insect feed market is characterized by fragmentation, with numerous new entrants holding small market shares. Key players such as Hipromine SA, Protix, Loopworm, Ynsect, and Darling Ingredients Inc. dominate the market. These companies employ strategies including acquisitions, partnerships, and expansions to enhance their research capabilities and marketing efforts in the insect feed industry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Feed Conversion Ratio of Insects

- 4.2.2 Innovations in Insect Farming and Processing

- 4.2.3 Demand for Sustainable and Alternative Protein Source

- 4.3 Market Restraints

- 4.3.1 Regulatory and Legislative Barriers

- 4.3.2 Cultural and Consumer Acceptance

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Animal Type

- 5.1.1 Aquaculture

- 5.1.2 Poultry

- 5.1.3 Swine

- 5.1.4 Other Animal Types

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.1.4 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Russia

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 Egypt

- 5.2.5.3 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Hipromine SA

- 6.3.2 nextProtein

- 6.3.3 Darling Ingredients Inc.

- 6.3.4 Protix BV

- 6.3.5 InnovaFeed SAS

- 6.3.6 Nasekomo AD

- 6.3.7 Ynsect

- 6.3.8 Beta Hatch Inc.

- 6.3.9 Entomo Farms

- 6.3.10 Hexafly Enterprises Limited

- 6.3.11 Loopworm Private Limited