|

市場調査レポート

商品コード

1444136

携帯型医療機器:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Portable Medical Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 携帯型医療機器:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 153 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

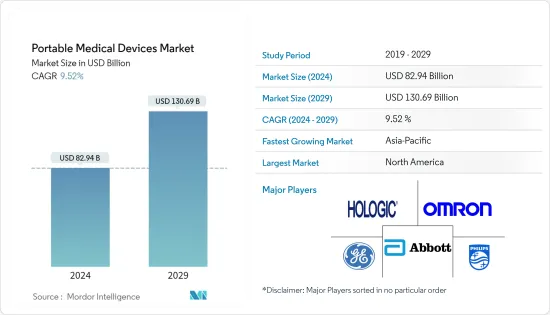

携帯型医療機器市場規模は、2024年に829億4,000万米ドルと推定され、2029年までに1,306億9,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に9.52%のCAGRで成長します。

COVID-19のパンデミックの発生により、ヘルスケア業界におけるポータブル医療機器の役割が拡大しました。ポータブルテクノロジーは、患者と専門家の両方にとって、遠隔地で健康を効果的に管理する上で常に重要です。COVID-19の影響で健康管理への注目が高まる中、家庭環境でのポータブル医療機器の需要が高まっています。たとえば、2021年 3月に発表された「COVID-19と慢性疾患の監視に向けたウェアラブル遠隔医療システム」というタイトルの研究によると、遠隔監視できるシンプルでウェアラブルで目立たないセンサーデバイスにより、入院や入院を減らすことができるとのことです。訪問。このような研究は、ポータブル医療機器の重要性を示しており、市場の成長にプラスの影響を与えます。

さまざまな企業が革新的なポータブル製品を開発してこの情勢に参入しています。 2021年6月、モハリに本拠を置くウォルナット・メディカル社は、インドで圧力スイング吸着(PSA)技術に基づき、55~75kpaの圧力で酸素純度が96%を超える5Lおよび10Lのポータブル医療グレード酸素濃縮器を開発しました。これはパンデミックの最中にユニークな機会をもたらしました。

携帯型医療機器市場は、携帯型医療機器やウェアラブル電子機器に対する需要の高まり、技術の進歩、高齢者人口の増加により、急速な成長が見込まれています。ポータブル医療機器の技術進歩の高まり(実用性、精度、アクセスのしやすさ、ワークフローを向上させるための機器への新技術の組み込みなど)は、ポータブル機器の採用の増加につながり、市場を牽引しています。 2022年 8月、SmartCardiaは7誘導心臓モニタリングパッチである7Lパッチを発売しました。この最先端のパッチモニターは、人工知能(AI)を使用してウェアラブル医療技術と遠隔患者モニタリングを統合し、患者に合わせて予測された洞察を提供します。

さらに、GEヘルスケアは2022年 6月に、患者の滞在中の継続的なモニタリングを可能にするワイヤレス患者モニタリング技術であるPortrait Mobileを発売しました。この技術は、医師が患者の衰弱を特定するのに役立ちます。モバイルモニターは、Portrait Mobileで患者が装着するワイヤレスセンサーと通信できます。したがって、技術的に先進的なポータブル医療機器の発売の増加により、市場は予測期間中に成長すると予想されます。

さらに、高齢者人口の増加により、市場の成長が促進されると予想されます。国連経済社会局が発行した2022年世界人口予測報告書によると、2022年には世界中で7億7,100万人が65歳以上になるとのこと。さらに、同じ情報源によると、2030年までに9億9,400万人が高齢者になるといいます。世界中の成人の数は2050年までに16億人に達すると予想されます。したがって、前述のすべての要因が予測期間中に市場を押し上げると予想されます。

ただし、セキュリティ上の懸念と医療機器の高コストにより、予測期間中に市場が抑制される可能性があります。

携帯型医療機器市場の動向

画像診断セグメントは予測期間中にかなりの市場シェアを保持すると予想される

画像診断装置セグメントは、超音波、X線、MRIなどの診断目的で使用される医療機器を幅広くカバーしています。腫瘍学、整形外科、胃腸、婦人科の分野で広範囲に応用されています。画像診断部門を強化する主な要因は、慢性疾患の負担の増大(これらの機器は病気の診断に使用されるため)と画像診断における技術の進歩です。米国がん協会2022によると、米国では、2022年に約190万人の新たながん症例と609,360人のがん関連死亡が確認されると予想されています。したがって、がんの発生率の増加により、画像診断装置や画像診断装置の需要が増大しています。市場の成長を促進すると予想されています。

画像診断における技術の進歩と製品の発売により、画像診断装置部門が世界的に推進されています。たとえば、2022年 7月に、富士フイルム欧州は、新しい柔軟なハイブリッド CアームとポータブルX線装置を発売しました。 FDR Crossと呼ばれるこの装置は、手術やその他の医療処置中に高品質の透視画像と静的X線画像を提供するように設計されています。

さらに、2022年 1月に、ClariusMobile Healthは、すべての医療専門家向けの高性能ハンドヘルドワイヤレス超音波スキャナーの第3世代製品ラインを発売しました。同様に、2021年 12月に、EagleViewultrasoundはワイヤレスポータブル超音波デバイスを導入しました。これにより、超音波イメージングに大きな自由が提供され、ポイントオブケアソリューションがより手頃な価格になります。したがって、上記の要因が予測期間にわたってこのセグメントを推進すると予想されます。

北米は携帯型医療機器市場をリードしており、予測期間中も同様の成長が見込まれる

北米は、携帯型医療機器市場で最大の金額シェアを保持していると推定されています。技術的に先進的な機器の高い導入率、高い治療率、病気の早期診断に対する政府の支援的な取り組みは、市場を牽引する数少ない要因の一つです。イメージング分野における政府の取り組みの一例としては、国立がん研究所が開始したがんイメージングプログラムがあります。このプログラムは、イメージングおよびテクノロジーにおけるがん関連の基礎研究、臨床研究、橋渡し調査を促進および支援することを目的としています。また、がんの臨床管理のためにこれらの画像技術革新を開発、統合、および応用することも目的としています。

疾病管理のためのモニタリング、診断、治療システムの導入が進んでいることは、地域の成長にとって良い前兆となると予想されます。高齢者人口の増加と、それに伴う慢性疾患の負担の増加も市場を推進しています。 2022年 7月の疾病管理予防センター(CDC)によると、2030年までに1,210万人のアメリカ人が心房細動(AFib)を患うと予想されています。したがって、AFibの有病率の増加により、これらの患者が増加するにつれて市場の成長が期待されています。継続的な監視が必要です。

さらに、国立がん研究所が発表したデータによると、2021年に米国では約1,806,590人が新たにがんと診断され、606,520人ががんにより死亡しました。したがって、国内ではがんや心血管疾患などの慢性疾患の負担が増大しているため、ポータブル医療機器の需要が増加し、その後市場を牽引すると予想されます。

さらに、この国での技術的に先進的な製品の発売は、市場の成長をさらに促進すると予想されます。たとえば、2022年 3月、MobvoiInc.は世界のヘルステック企業CardieXと提携して、同社初の心臓の健康状態をモニタリングするスマートウォッチであるTicWatchGTH Proを発売しました。この時計はセンサーも利用しており、手首と指の両方から追跡する高忠実度のセンシングポイントを通じて、全身および動脈の健康状態に関する洞察を提供します。さらに、GEヘルスケアは2021年 9月に、揚力を最大70%削減することを目的とした、この種初の電動補助フリーモーション伸縮コラムを備えて設計された新しいポータブルデジタルX線システムであるAMX Navigateを発売しました。技術者の怪我を減らします。したがって、上記の要因により、調査対象の市場は国内で大幅に成長すると予想されます。

携帯型医療機器業界の概要

携帯型医療機器市場は、多数の企業が存在し、競争が激しいです。この市場には、その成長に大きく貢献している企業が数多く存在します。製品の革新と高度な技術を開発するための継続的な研究開発活動が市場の成長を促進しました。市場シェアを維持するために、主要企業はさまざまな戦略とコラボレーションを採用しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- ポータブル医療機器とウェアラブル電子機器の需要の高まり

- テクノロジーの進歩の増加

- 高齢者人口の増加

- 市場抑制要因

- セキュリティ上の懸念

- 携帯型医療機器の高コスト

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 製品別

- 画像診断

- 監視デバイス

- 心臓モニタリング

- 神経モニタリング

- 呼吸モニタリング

- その他の監視デバイス

- その他の製品

- エンドユーザー別

- 病院

- 医師の診察室

- ホームケア設定

- その他のエンドユーザー

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Becton, Dickinson and Company

- General Electric(GE Healthcare)

- Hologic Inc.

- Abbott Laboratories

- Samsung Electronics Co. Ltd(Samsung Healthcare)

- Fujifilm Holdings Corporation

- Koninklijke Philips NV

- Omron Healthcare

- Medtronic Inc.

- Siemens Healthcare

第7章 市場機会と将来の動向

The Portable Medical Devices Market size is estimated at USD 82.94 billion in 2024, and is expected to reach USD 130.69 billion by 2029, growing at a CAGR of 9.52% during the forecast period (2024-2029).

The outbreak of the COVID-19 pandemic extended the role of portable medical devices in the healthcare trade. Portable technologies have always been crucial for both patients and professionals in effectively managing health in remote settings. With increasing focus on health management during COVID-19, portable medical devices have experienced increased demand in home settings. For example, according to the study titled 'A Wearable Tele-Health System towards Monitoring COVID-19 and Chronic Diseases' published in March 2021, simple, wearable, non-obtrusive sensor devices that can be monitored remotely can cut down on hospital admissions and visits. Such studies show the importance of portable medical devices, positively impacting the market growth.

Various companies are entering the landscape with innovative portable products. In June 2021, Mohali-based Walnut Medical developed 5L and 10L portable medical-grade oxygen concentrators based on pressure swing adsorption (PSA) technology in India with an oxygen purity of above 96% at a pressure of 55-75 kpa. This offered a unique opportunity during pandemic.

The portable medical devices market is expected to witness rapid growth due to the escalating demand for portable medical devices and wearable electronics, increased technological advancements, and a rise in the geriatric population. The rise in technological advancements in portable medical devices (such as the incorporation of new technology in the device to enhance its utility, accuracy, ease of access, and workflow) will lead to an increase in the adoption of the portable devices, driving the market growth. In August 2022, SmartCardia launched their 7L patch, a 7-lead cardiac monitoring patch. With the use of artificial intelligence (AI), this cutting-edge patch monitor integrates wearable medical technology with remote patient monitoring to deliver tailored and predicted patient insights.

Additionally, in June 2022, GE Healthcare launched Portrait Mobile, a wireless patient monitoring technology that allows for constant monitoring throughout a patient's stay. The technique aids doctors in identifying patient decline. A mobile monitor can communicate with patient-worn wireless sensors in Portrait Mobile. Therefore, owing to the rise in the launch of technologically advanced portable medical devices, the market is expected to grow over the forecast period.

Moreover, the growing geriatric population is expected to propel the growth of the market. According to the World Population Prospects 2022 report published by the United Nations Department of Economic and Social Affairs, 771 million people worldwide will be 65 years or above in 2022. Furthermore, according to the same source, by 2030, there will be 994 million older adults in the world, and by 2050, the number will hit 1.6 billion. Thus, all aforementioned factors are expected to boost the market over the forecast period.

However, security concerns and high cost of medical devices may restrain the market over the forecast period.

Portable Medical Devices Market Trends

Diagnostic Imaging Segment Expected to Hold Significant Market Share Over the Forecast Period

The diagnostic imaging equipment segment covers a wide array of medical devices used for diagnostic purposes like ultrasound, X-ray, and MRI, among others. It has a vast range of applications in the oncology, orthopedic, gastro, and gynecological fields. The key factors bolstering the diagnostic imaging segment are the rising burden of chronic diseases (as these devices are used in diagnosing diseases) and technological advancements in diagnostic imaging. According to the American Cancer Society 2022, in the United States, around 1.9 million new cancer cases and 609,360 cancer-related deaths are anticipated to be identified in 2022. Thus, a rise in the incidence of cancer escalates the demand for diagnostics imaging devices and is expected to drive market growth.

Technological advancements and product launches in diagnostic imaging are driving the diagnostic imaging equipment segment globally. For instance, in July 2022, Fujifilm Europe launched a new flexible, hybrid C-arm and portable X-ray machine. The device, called FDR Cross, is designed to offer high-quality fluoroscopic and static X-ray images during surgery and other medical procedures.

Additionally, in January 2022, ClariusMobile Health launched a third-generation product line of high-performance handheld wireless ultrasound scanners for all medical specialists. Similarly, in December 2021, EagleViewultrasound introduced its wireless portable ultrasound device, which provides much freedom for ultrasound imaging and makes the point-of-care solution more affordable. Thus, the abovementioned factors are expected to drive the segment over the forecast period.

North America Leading the Portable Medical Devices Market and Expected to do the Same Over the Forecast Period

North America is estimated to hold the largest value share in the portable medical devices market. High adoption of technologically advanced devices, high treatment rates, and supportive government initiatives for early diagnosis of diseases are among the few factors driving the market. An example of government initiatives in the area of imaging is the Cancer Imaging Program initiated by the National Cancer Institute. This program is aimed at promoting and supporting cancer-related basic, clinical, and translational research in imaging and technology. It is also aimed at developing, integrating, and applying these imaging innovations for the clinical management of cancer.

High adoption of monitoring, diagnostic, and therapeutic systems for disease management is anticipated to bode well for regional growth. The growing geriatric population and a subsequently rising burden of chronic diseases are also propelling the market. According to the Centers for Disease Control and Prevention (CDC), in July 2022, 12.1 million Americans were expected to have atrial fibrillation (AFib) by the year 2030. Thus, the increasing prevalence of AFib is expected to increase market growth as these patients require constant monitoring.

In addition, as per data published by the National Cancer Institute, in 2021, there were around 1,806,590 new cases of cancer diagnosed in the United States, and 606,520 people died from the disease. Therefore, due to the rising burden of chronic diseases such as cancer and cardiovascular diseases in the country, the demand for portable medical devices is expected to increase and subsequently drive the market.

Moreover, the launch of technologically advanced products in the country is expected to further drive market growth. For instance, in March 2022, MobvoiInc., in partnership with the global health tech company CardieX, launched its first heart health monitoring smartwatch, the TicWatchGTH Pro. The watch also utilizes sensors to provide insights into general and arterial health through high-fidelity sensing points that track both from the wrist and through the finger. Additionally, in September 2021, GE Healthcare launched the AMX Navigate, a new portable, digital X-ray system designed with a first-of-its-kind power-assisted Free Motion telescoping column that aims to reduce lift force by up to 70% and decrease technologist injury. Thus, due to the abovementioned factors, the market studied is expected to grow significantly in the country.

Portable Medical Devices Industry Overview

The portable medical devices market is highly competitive with the presence of a large number of players. The market has a considerable number of companies that are significantly contributing to its growth. Product innovation and ongoing R&D activities to develop advanced technologies have helped boost the market's growth. Various strategies and collaborations are being adopted by key players to maintain their market share.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Demand for Portable Medical Devices and Wearable Electronics

- 4.2.2 Increase in Technological Advancements

- 4.2.3 Rise in Geriatric Population

- 4.3 Market Restraints

- 4.3.1 Security Concerns

- 4.3.2 High Cost of Portable Medical Devices

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Million)

- 5.1 By Products

- 5.1.1 Diagnostic Imaging

- 5.1.2 Monitoring Devices

- 5.1.2.1 Cardiac Monitoring

- 5.1.2.2 Neuro Monitoring

- 5.1.2.3 Respiratory Monitoring

- 5.1.2.4 Other Monitoring Devices

- 5.1.3 Other Products

- 5.2 By End User

- 5.2.1 Hospitals

- 5.2.2 Physician Offices

- 5.2.3 Homecare Settings

- 5.2.4 Other End Users

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East & Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East & Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Becton, Dickinson and Company

- 6.1.2 General Electric (GE Healthcare)

- 6.1.3 Hologic Inc.

- 6.1.4 Abbott Laboratories

- 6.1.5 Samsung Electronics Co. Ltd (Samsung Healthcare)

- 6.1.6 Fujifilm Holdings Corporation

- 6.1.7 Koninklijke Philips N.V.

- 6.1.8 Omron Healthcare

- 6.1.9 Medtronic Inc.

- 6.1.10 Siemens Healthcare