|

市場調査レポート

商品コード

1686546

超高速レーザー:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Ultrafast Lasers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 超高速レーザー:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 166 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

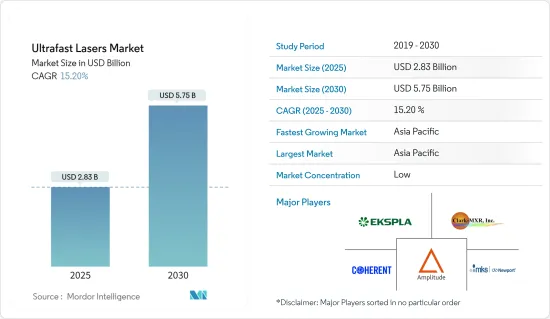

超高速レーザー市場規模は、2025年に28億3,000万米ドルと推計され、予測期間(2025-2030年)のCAGRは15.2%で、2030年には57億5,000万米ドルに達すると予測されています。

超高速レーザーは、1パルスが1ナノ秒以下というパルス列を発振するレーザの一種。超短パルス持続時間と高いピーク強度で知られ、精密で制御された材料加工を可能にします。様々な材料の切断、穴あけ、アブレーション、構造化に使用されます。

超高速レーザーは、材料加工において高い精度を提供し、材料の極めて正確で複雑な加工や修正を可能にします。これらのレーザは、ほとんどすべての種類の材料を加工することができ、様々な用途に対応できる万能ツールとなっています。

超高速レーザーの市場成長は、主に材料加工と半導体産業における需要の増加によって牽引され、自動車、家電、通信技術、ヘルスケアなどのエンドユーザーでの用途が見つかっています。超高速レーザーとマイクロマシニングが可能にする高い寸法精度は、超高速レーザーの需要を押し上げる重要な要因です。これらのレーザは、半導体産業におけるフォトマスク修正に使用されています。また、スライスやダイシングにも使用されています。

より小さく、より複雑なコンポーネントの需要は、より高いレベルの寸法精度を必要とし、超高速レーザーはその超短パルス持続時間と最小の熱影響円錐でそれを実現します。この機能は製品の品質を向上させ、製造時間とコストを削減します。技術の進歩に伴い、超高速レーザーの市場は、優れた寸法精度に対するニーズの高まりに対応するため、さらに拡大すると予想されます。

超高速レーザーの製造には、これらのデバイスを製造するために必要な高度な技術と精度に起因する多くの複雑さが伴います。製造の複雑さを理解するには、これらの高性能デバイスを作る複雑なプロセスを掘り下げる必要があります。

COVID-19パンデミックは世界経済に混乱を引き起こしました。また、エレクトロニクスや半導体市場の生産設備も停止しました。製造能力の鈍化、労働者や原材料の入手不能、渡航禁止、施設の閉鎖などが市場の成長鈍化につながりました。自動化の普及と精密製造の需要増で、レーザーはパンデミック効果後、より高い応用と需要を示しています。

超高速レーザー市場動向

コンシューマエレクトロニクスが大幅成長

- ほとんどの民生用電子機器アプリケーションは、最大限の生産性と精度を得るために、高い繰返し精度のパルスを集光したレーザビームを必要とします。ファイバーレーザーの優れたビーム品質、柔軟性、安定性は、微細加工アプリケーションに最適です。最近の動向として、IPGは製品ポートフォリオを従来の赤外から緑色や紫外へと大幅に拡大し、ピコ秒や高フェムト秒パルス機能を開発しました。

- さらに、民生用電子機器産業は、信頼性、柔軟性、効率性、高出力、ビーム品質、コンパクト性、費用対効果のユニークな組み合わせのために、IPGファイバーレーザーと統合自動化システムを切望しています。

- 研究部門は、主に民生用電子機器部門からの需要の増加と、OEMが継続的にユニークな製品を市場に投入することを余儀なくされる速いペースの技術開発によって牽引されています。コンシューマー・エレクトロニクス・プロバイダーは主に、コスト削減、量産までの時間短縮、品質、市場投入までの時間短縮、柔軟性といったメリットを市場に提供する電子機器メーカーに依存しています。

- 米国消費者技術協会(Consumer Technology Association)によると、米国では消費者技術小売の収益が2022年から2024年にかけて微増し、期間終了時には5,000億米ドルを超えると予測されています。収益の大半はハードウェアが占め、2024年には約3,450億米ドルに達します。

- 現在、市場の電子機器のほとんどは小型化されており、素子がますます小さくなるフォームファクタに収まるように、より厳しい寸法公差が要求され、超高速レーザーの成熟を促しています。電子部品の製造工程では、より小さな部品の特徴を検査し、精度を向上させる必要があります。

- 超高速レーザーは、マイクロプロセッサや半導体など、特定のスマートフォン部品の製造に極めて重要です。スマートフォンの普及拡大は、研究市場の成長を大きく後押しします。

アジア太平洋が主要市場シェアを握る見込み

- アジア太平洋には、中国、日本、韓国、台湾など、世界最大の製造業経済圏があります。自動車、エレクトロニクス、航空宇宙、医療機器などの分野における製造業の継続的な拡大は、様々な加工、切断、溶接、マーキングアプリケーションをサポートする産業用レーザの大きな需要を生み出しています。

- アジア太平洋には、Han's Laser Technology Industry Groupなど、この市場で重要なプレーヤーがいます。この地域は、自動車産業や医療産業における能力で知られており、市場成長の原動力になると期待されています。また、アジア太平洋地域は市場で最も高い成長率を示すことが期待されているため、様々なプレイヤーが成長と開拓を推進するために投資しています。

- さらに、この地域の自動車産業は、高い剛性、設計の柔軟性、生産性を要求しながら、電動化、小型化に向かっています。光吸収効率の高い青色レーザは、自動車用モータやバッテリの銅加工で高い需要があります。生産性の高い加工には、出力とビーム品質の高いレーザービーム源が必要です。

- この地域は、台湾セミコンダクタマニュファクチャリングカンパニーのような企業の存在により、半導体やエレクトロニクス製品の最大のメーカーです。台湾は、世界の半導体の60%以上、先端半導体の90%以上を生産しています。半導体のほとんどはTSMCによって製造されています。

超高速レーザー市場概要

超高速レーザー市場は、複数のプレーヤーによって断片化され、競争が激しいです。市場は適度に集中しているように見えます。同市場のベンダーは、市場成長を大きく後押しする重要なR&D投資やパートナーシップで新製品展開に参画しています。さらに、企業は成長戦略として買収を行っています。同市場は、Amplitude Laser Group Coherent Inc.、Ekspla(EKSMA group)、MKS Instruments Inc.(Newport Corporation)、Clark-MXR Inc.などのレーザ/フォトニック大手で構成されています。

2024年1月-IPG Photonics Corporationは、サンフランシスコで開催されたフォトニクス・ウエスト(Photonics West)において、新しく革新的なファイバーレーザーソリューションを紹介しました。2,000平方フィートのブースでは、幅広いレーザー光源、統合システム、業界固有のソリューションが展示され、多数のアプリケーションサンプルも展示されました。

2023年6月- コヒレント・コーポレーションは、産業用電子機器、消費財、機器、パッケージングなどの高コントラストマーキング用途向けに、超低コストの次世代ナノ秒パルスUVレーザを発表しました。新しいアレイレーザは出力5Wと10Wがあり、パルス繰り返し周波数は50kHzから300kHzで動作します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19の影響とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- 寸法精度向上へのニーズ

- 超高速レーザーの採用を促進する政府の指令

- 市場抑制要因

- 製造の複雑さが市場成長の課題

第6章 市場セグメンテーション

- レーザータイプ別

- 固体レーザー

- ファイバーレーザー

- パルス時間別

- ピコ秒

- フェムト秒

- 用途別

- 材料加工と微細加工

- 医療およびバイオイメージング

- 研究

- エンドユーザー別

- コンシューマーエレクトロニクス

- 医療

- 自動車

- 航空宇宙・防衛

- 研究

- その他のエンドユーザー

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- Vendor Positioning Analysis

- 企業プロファイル

- Amplitude Laser Group

- Coherent Inc.

- Ekspla(EKSMA group)

- MKS Instruments Inc.(Newport Corporation)

- Clark-MXR Inc.

- TRUMPF Group

- Novanta(Laser Quantum Ltd)

- Lumentum Holdings

- Aisin Seiki(IMRA America Inc.)

- IPG Photonics

- NKT Photonics

- Light Conversion Ltd

第8章 投資分析

第9章 市場の将来

The Ultrafast Lasers Market size is estimated at USD 2.83 billion in 2025, and is expected to reach USD 5.75 billion by 2030, at a CAGR of 15.2% during the forecast period (2025-2030).

Ultrafast lasers are a variety of lasers that emits a series or train of pulses, each lasting less than a nanosecond. They are known for their ultra-short pulse duration and high peak intensity, allowing precise and controlled material processing. They are used for cutting, drilling, ablating, and structuring various materials.

Ultrafast lasers offer high precision in material processing, allowing for extremely accurate and intricate fabrication and modification of materials. These lasers can process almost every type of material, making them versatile tools for various applications.

The market growth for ultrafast lasers is primarily driven by the increasing demand in the materials processing and semiconductor industries, finding applications in several end users like automotive, consumer electronics, communications technology, and healthcare. The high dimensional accuracy enabled by ultrafast lasers and micromachining are significant factors boosting the demand for ultrafast lasers. These lasers are used for photomask repairs in the semiconductor industry. They are also employed for slicing and dicing activities

The demand for smaller, more complex components necessitates a higher level of dimensional accuracy, which ultrafast lasers deliver with their ultrashort pulse durations and minimal heat-affected cones. This capability improves product quality and reduces production time and costs. As technology advances, the market for ultrafast lasers is expected to expand further to meet the growing need for superior dimensional accuracy.

Manufacturing ultrafast lasers involves many complexities stemming from the advanced technology and precision required to produce these devices. Understanding the manufacturing complexities requires delving into the intricate process of creating these high-performance devices.

The COVID-19 pandemic caused disruptions in the global economy. It also halted the production facilities of the electronics and semiconductors markets. The slowdown in manufacturing capacity, unavailability of workers and raw materials, travel bans, and facility closures led to a slowdown in the market's growth. With the proliferation of automation and a growth in the demand for precision manufacturing, lasers are witnessing higher application and demand after the pandemic effect.

Ultrafast Lasers Market Trends

Consumer Electronics to Witness Significant Growth

- Most consumer electronics applications require a focused laser beam delivered in highly repeatable pulses at a rapid repetition rate for maximum productivity and precision. Fiber lasers' outstanding beam quality, flexibility, and stability are ideal for micromachining applications. Recently, IPG significantly expanded its product portfolio from the traditional infrared into the green and ultraviolet wavelengths and developed picosecond and high femtosecond pulse capabilities, which greatly broaden the scope of consumer electronics applications able to benefit from fiber laser technology.

- In addition, the consumer electronics industry covets IPG fiber lasers and integrated automated systems for their unique combination of reliability, flexibility, efficiency, high power, beam quality, compactness, and cost-effectiveness.

- The studied sector is driven primarily by the increasese in demand from the consumer electronics sector and fast-paced technological developments, which force OEMs to introduce unique products continuously in the market. Consumer electronics providers primarily rely on electronic manufacturers who offer benefits like cost savings, reduced time-to-volume, quality, decreased time-to-market, and flexibility to provide their products in the market.

- According to the Consumer Technology Association, in the United States, consumer technology retail revenue is forecast to increase slightly between 2022 and 2024, reaching over USD 500 billion at the end of the period. Hardware accounts for most of the revenue, bringing in around USD 345 billion in 2024.

- Most of the electronic appliances in the market nowadays are downsized and demand tighter dimensional tolerances so that the elements can fit inside ever-smaller form factors, driving the maturation of the ultrafast laser. The electronic manufacturing process needs to inspect the tinier component features and improve accuracy.

- Ultrafast lasers are crucial in manufacturing specific smartphone components, such as microprocessors and semiconductors. The increasing adoption of smartphones is going to to aid the studied market's growth significantly.

Asia-Pacific is Expected to Hold Major Market Share

- The Asia-Pacific is home to some of the world's largest manufacturing economies, including China, Japan, South Korea, and Taiwan. The ongoing expansion of manufacturing industries in sectors such as automotive, electronics, aerospace, and medical devices creates a significant demand for industrial lasers to support various machining, cutting, welding, and marking applications.

- The Asia-Pacific houses some important players in the market, such as Han's Laser Technology Industry Group, among others. The region is known for its capabilities in the automotive and medical industries, which are expected to drive its market growth. Also, various players have invested in driving their growth and development, as the Asia-Pacific is expected to witness the highest growth rate in the market.

- Moreover, the automotive industry in the region is moving toward electrification and miniaturization while requiring high rigidity, design flexibility, and productivity. Blue lasers with high optical absorption efficiency are in high demand in copper fabrication for automotive motors and batteries. The highly productive processing requires a laser beam source with high output power and beam quality.

- The region is the biggest manufacturer of semiconductor and electronics products owing to the presence of companies like Taiwan Semiconductor Manufacturing Company. Taiwan produces more than 60% of the global semiconductors and over 90% of the advanced ones. Most of the semiconductors are manufactured by TSMC.

Ultrafast Lasers Market Overview

The Ultrafast laser market is fragmented and highly competitive due to multiple players. The market appears to be moderately concentrated. Vendors in the market are taking part in new product rollouts with crucial R&D investments and partnerships that significantly boost market growth. Additionally, companies have acquisitions as their growth strategy. The market consists of laser/photonic giants, like Amplitude Laser Group Coherent Inc., Ekspla (EKSMA group), MKS Instruments Inc. (Newport Corporation), and Clark-MXR Inc.

January 2024 -The IPG Photonics Corporation highlighted new and innovative fiber laser solutions at Photonics West January 30 - February 01, 2024, in San Francisco. The 2,000-square-foot booth displays include a wide range of laser sources, integrated systems, and industry-specific solutions, along with numerous showcases of application samples.

June 2023 - Coherent Corporation introduced an ultra-low-cost, next-generation nanosecond pulsed UV laser for high-contrast marking applications in industrial electronics, consumer goods, equipment, and packaging. The new array lasers are available with 5W and 10W output power and operate at pulse repetition rates between 50kHz and 300kHz.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Need for Enhanced Dimensional Accuracy

- 5.1.2 Government Mandates Promoting Adoption of Ultrafast Lasers

- 5.2 Market Restraints

- 5.2.1 Manufacturing Complexities Challenge the Market Growth

6 MARKET SEGMENTATION

- 6.1 By Laser Type

- 6.1.1 Solid State Laser

- 6.1.2 Fiber Laser

- 6.2 By Pulse Duration

- 6.2.1 Picosecond

- 6.2.2 Femtosecond

- 6.3 By Application

- 6.3.1 Material Processing And Micromachining

- 6.3.2 Medical And Bioimaging

- 6.3.3 Research

- 6.4 By End User

- 6.4.1 Consumer Electronics

- 6.4.2 Medical

- 6.4.3 Automotive

- 6.4.4 Aerospace and Defense

- 6.4.5 Research

- 6.4.6 Other End Users

- 6.5 By Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia-Pacific

- 6.5.4 Latin America

- 6.5.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Vendor Positioning Analysis

- 7.2 Company Profiles

- 7.2.1 Amplitude Laser Group

- 7.2.2 Coherent Inc.

- 7.2.3 Ekspla (EKSMA group)

- 7.2.4 MKS Instruments Inc. (Newport Corporation)

- 7.2.5 Clark-MXR Inc.

- 7.2.6 TRUMPF Group

- 7.2.7 Novanta (Laser Quantum Ltd)

- 7.2.8 Lumentum Holdings

- 7.2.9 Aisin Seiki (IMRA America Inc.)

- 7.2.10 IPG Photonics

- 7.2.11 NKT Photonics

- 7.2.12 Light Conversion Ltd