|

市場調査レポート

商品コード

1444086

網膜剥離診断:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Retinal Detachment Diagnostic - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 網膜剥離診断:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

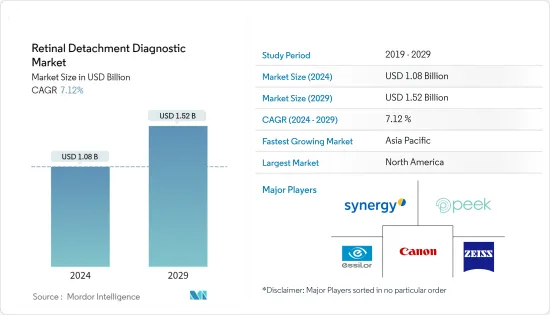

網膜剥離診断市場規模は2024年に10億8,000万米ドルと推定され、2029年までに15億2,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に7.12%のCAGRで成長します。

新型コロナウイルス感染症(COVID-19)のパンデミックにより、不確実な予測、短期的な計画目標の変化、短期的なコスト管理と長期的な複雑さ管理の懸念が焦点になりました。国立医学図書館によると、新型COVID-19ウイルス感染症のパンデミック中、緊急の眼科受診で網膜剥離と診断される割合は大幅に減少し、患者は眼科検査を求めるまでの待ち時間が長くなった。これらの発見はおそらく、病院環境でCOVID-19感染症に感染することへの恐怖によるものと考えられます。したがって、上記の要因により、新型コロナウイルス感染症(COVID-19)は網膜剥離診断市場に大きな影響を与えました。

網膜疾患の有病率の増加が市場の成長を推進しています。 2021年9月のWHOの推計によると、世界では1億8,000万人が視覚障害者で、4,000~4,500万人が視覚障害者となっています。同情報筋は、世界の失明の約80%は予防可能である、つまり、必要な知識と医療介入が適切なタイミングで提供されるか、予防可能な特定の症状に起因する場合には、その症状に対処できると述べた。世界保健機関やその加盟国、非政府組織(NGO)、民間部門、その他の国連機関などの組織を含む国際社会によって、協調した啓発活動が行われています。

技術の急速な進歩により、効率的な診断装置に対する需要も高まっています。新しい技術プラットフォームは間違いなく非常に効率的です。ただし、最初は高額で入手できます。レーザー装置の価格が高いため、眼科レーザー治療の費用はかなり高額であり、低所得層や中所得層には手が届きません。さらに、設置およびサービスのコストも高くなります。眼科用レーザーの平均価格は20,000米ドルから75,000米ドルの範囲になると考えられますが、レーシック屈折矯正手術の治療費は片目あたり2,077米ドルを超えます。これは、予測期間中に市場に悪影響を与えると予想されます。

網膜剥離診断市場動向

裂孔原性網膜剥離の診断薬が市場を独占すると予想される

裂孔原性網膜剥離(RRD)は、最も一般的な種類の網膜剥離疾患です。患者の網膜に穴、裂傷、または亀裂が生じ、硝子体ゲルが網膜の下に漏れます。液体が沈降すると、網膜はその下の層から剥がれます。状況によっては、RRDは部分的または完全な視力喪失を引き起こす可能性があります。 Journal of Clinical &Experimental Opharmology 2020に掲載されたレポートによると、RRDの発生率は年齢とともに増加します。世界保健機関によると、世界中で60歳以上の人口は2050年までに21億人に増加すると予想されています。世界の高齢者人口の増加により、RRD患者の数が増加すると予想されます。これにより、予測期間中の市場の成長が刺激されます。

裂孔原性網膜剥離疾患の早期発見は、患者が経済的困難を回避するのに役立ちます。 WHOによると、白内障は世界中で約6,520万人が罹患しており、症例の80%以上で中等度から重度の視力喪失を引き起こしています。世界中で人口の高齢化が進み、平均寿命が延びると、白内障を患う人の数も増加します。これにより、これらの障害の診断に対する需要が増加し、予測期間中の市場の成長を促進すると予想されます。

北米が網膜剥離の診断市場を独占すると予想される

北米は、一貫した新製品の承認を通じて成長の基盤を提供する広範な研究開発活動により、市場を独占すると予想されています。対象疾患と高齢者人口の増加は、予測期間中の市場の成長を支えると予想されます。北米が最も大きな市場シェアを占めており、これは定期的な新製品の承認を通じて成長のプラットフォームを提供する広範な研究開発活動によるものです。さらに、疾病管理予防センターによると、2020年5月時点で40歳以上のアメリカ人の約17%(約2,050万人)が少なくとも片目に白内障を患っていました。同じ情報筋は、2028年までに約3,000万人が白内障に罹患すると述べています。

米国疾病管理予防センターは、2020年には410万人のアメリカ人が糖尿病性網膜症を患っており、90万人近くが視力障害網膜症のリスクにさらされていると推定しました。視覚障害の増加、白内障の症例の増加、および糖尿病網膜症の頻度の増加が寄与しています。セグメントの成長に貢献します。たとえば、米国では40歳以上の約1,200万人が視覚障害を抱えており、2020年には約100万人が視覚障害者となっています。さらに、北米における多くの主要企業の存在は、市場の成長を促進する主要な要因です。

網膜剥離診断業界の概要

世界の主要企業は、ほとんどの網膜剥離診断機器およびデバイスを製造しています。より多くの調査資金とより優れた流通システムを持つ市場リーダーは、市場での地位を確立しています。さらに、アジア太平洋では、意識の高まりにより、いくつかの小規模プレーヤーの台頭が見られます。これも市場の成長に貢献しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 低侵襲手術の需要の増加

- 高齢者人口の増加

- 白内障手術件数の増加

- 市場抑制要因

- 網膜手術用機器の価格が高い

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 疾患タイプ別

- 裂孔原性網膜剥離

- 滲出性、漿液性、または続発性網膜剥離

- 牽引性網膜剥離

- 診断別

- 眼底撮影

- 検眼鏡検査

- デジタル眼底カメラ

- 蛍光網膜血管造影

- その他

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Canon Medical Systems Corporation

- Carl Zeiss Meditec Inc.

- Revenio Group Corporation(Centervue SpA)

- Eyenuk Inc.

- Essilor International SA

- HealPros LLC

- Millennium Surgical Corp.

- ONL Therapeutics

- Peek Vision Ltd

- Parata Systems(Synergy Medical)

第7章 市場機会と将来の動向

The Retinal Detachment Diagnostic Market size is estimated at USD 1.08 billion in 2024, and is expected to reach USD 1.52 billion by 2029, growing at a CAGR of 7.12% during the forecast period (2024-2029).

The COVID-19 pandemic caused uncertain forecasts, shifts in short-term planning goals, and a focus on near-term cost management and long-term complexity management concerns. According to the National Library of Medicine, the rate of retinal detachment diagnosed in its emergent ophthalmology consultation decreased significantly during the COVID-19 pandemic, and patients waited longer before asking for an ophthalmologic examination. These findings were probably due to the fear of contracting the COVID-19 infection attending hospital environments. Hence, COVID-19 significantly impacted the retinal detachment diagnostic market due to the abovementioned factors.

The increasing prevalence of retinal disorders is driving the growth of the market. According to WHO estimates of September 2021, globally, 180 million people were visually disabled, and 40-45 million people were blind. The same source stated that around 80% of global blindness is preventable, i.e., the condition can be addressed if the requisite knowledge and medical interventions are provided at the right time or result from certain conditions that can be prevented. Concerted awareness efforts are being made by the international community, including organizations such as World Health Organization and its member states, nongovernmental organizations (NGOs), the private sector, and other UN agencies.

The demand for efficient diagnostic devices is also increasing owing to rapid technological advances. Novel technological platforms are no doubt highly efficient. However, they are available at high prices initially. The cost of ophthalmic laser treatment is considerably high owing to the high cost of the laser devices, which makes them unaffordable for low- and middle-income groups. In addition, installation and service costs are high. The average price of ophthalmic lasers is likely to be valued in the range of USD 20,000-USD 75,000, while treatments are priced at over USD 2,077 per eye for LASIK refractive correction surgery. This is expected to have a negative impact on the market during the forecast period.

Retinal Detachment Diagnostic Market Trends

Rhegmatogenous Retinal Detachment Diagnostics is Expected to Dominate the Market

Rhegmatogenous retinal detachment (RRD) is the most prevalent kind of retinal detachment disorder. The patient's retina develops a hole, tear, or crack, and the vitreous gel leaks beneath the retina. The retina peels away from the layer beneath it when the liquid settles. In some circumstances, RRD can cause partial or complete visual loss. According to a report published in the Journal of Clinical & Experimental Ophthalmology 2020, the incidence of RRD increases with age. According to the World Health Organization, globally, people aged 60 years and above are expected to increase to 2.1 billion by 2050. The rising geriatric population globally is expected to increase the number of patients with RRD. This will stimulate market growth over the forecast period.

The early detection of the rhegmatogenous retinal detachment illness helps patients avoid financial hardship. According to the WHO, cataracts affect approximately 65.2 million people worldwide, causing moderate to severe vision loss in more than 80% of cases. When populations age and average life expectancy rises worldwide, so will the number of people with cataracts. This is expected to increase the demand for the diagnosis of these disorders, driving the growth of the market over the forecast period.

North America is Expected to Dominate the Retinal Detachment Diagnostic Market

North America is expected to dominate the market due to the extensive research & development activities that provide a platform for growth through consistent new product approvals. The increasing target disease and geriatric population are expected to support the market growth during the forecast period. North America has the most significant market share, ascribed to extensive research & development operations that provide a platform for growth through new product approvals regularly. Furthermore, according to the Centers for Disease Control and Prevention, in May 2020, around 17% of Americans over 40 had a cataract in at least one eye (about 20.5 million people). The same source stated that cataracts would affect around 30 million people by 2028.

The Centre for Disease Control and Prevention estimated that 4.1 million Americans had diabetic retinopathy, and nearly 900,000 was at risk of vision-damaging retinopathy in 2020. The rising number of vision disorders, increasing cases of cataracts, and the rising frequency of diabetes retinopathy contribute to the growth of the segment. For example, approximately 12 million people aged 40 and up had vision impairment in the United States, with approximately a million blind in 2020. Furthermore, the presence of many key players in North America is a major factor driving the growth of the market.

Retinal Detachment Diagnostic Industry Overview

Global key players manufacture most retinal detachment diagnostic equipment and devices. Market leaders with more funds for research and better distribution system have established their position in the market. Moreover, Asia-pacific is witnessing an emergence of some small players due to the rise of awareness. This has also helped the market grow. The key players operating in the market are Revenio Group Corporation (Centervue SpA), Parata Systems (Synergy Medical), Canon Medical Systems Corporation, Peek Vision Ltd, Carl Zeiss Meditec Inc., Eyenuk Inc., Essilor International SA, HealPros LLC, Millennium Surgical Corp, ONL Therapeutics, and Peek Vision Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in the Demand of Minimally Invasive Procedures

- 4.2.2 Rising Geriatric Population

- 4.2.3 Increase in the Number of Cataract Surgeries

- 4.3 Market Restraints

- 4.3.1 High Price of Retinal Surgery Equipments

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Disease Type

- 5.1.1 Rhegmatogenous Retinal Detachment

- 5.1.2 Exudative, Serous or Secondary Retinal Detachment

- 5.1.3 Tractional Retinal Detachment

- 5.2 By Diagnostics

- 5.2.1 Fundus Photography

- 5.2.2 Ophthalmoscopy

- 5.2.3 Digital Retinal Camera

- 5.2.4 Fluorescent Retinal Angiography

- 5.2.5 Others

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Canon Medical Systems Corporation

- 6.1.2 Carl Zeiss Meditec Inc.

- 6.1.3 Revenio Group Corporation (Centervue SpA)

- 6.1.4 Eyenuk Inc.

- 6.1.5 Essilor International SA

- 6.1.6 HealPros LLC

- 6.1.7 Millennium Surgical Corp.

- 6.1.8 ONL Therapeutics

- 6.1.9 Peek Vision Ltd

- 6.1.10 Parata Systems (Synergy Medical)