造影剤:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

Contrast Media - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1850001

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

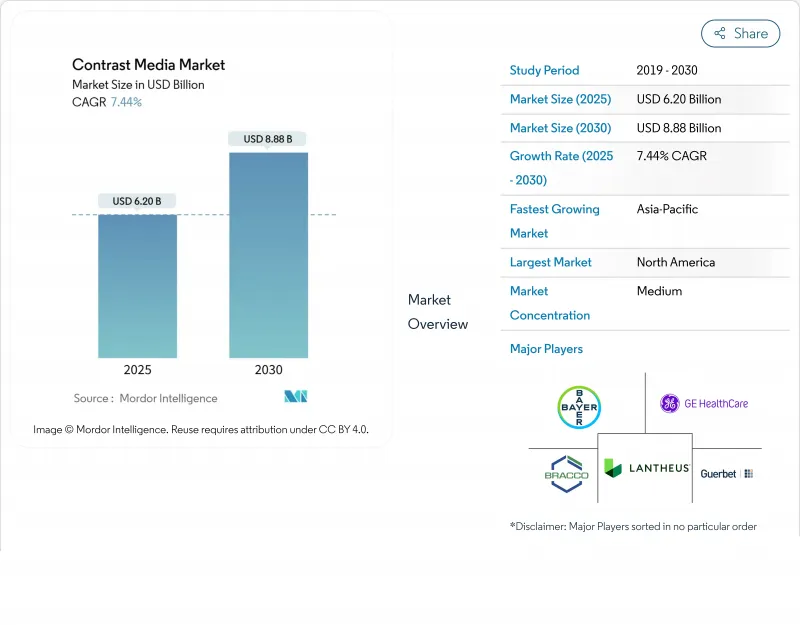

造影剤市場は2025年に62億米ドルに達し、2030年には88億8,000万米ドルに達すると予測され、予測期間のCAGRは7.44%です。

拡大の背景には、画像診断の着実な増加、大環状ガドリニウム製剤に対する規制当局の承認の迅速化、供給を確保するための製造能力への継続的な投資があります。病院は、より安全な大環状製剤を優先してプロトコルを合理化する一方、有害事象を抑制するために低用量ヨード剤の使用を拡大しています。ベンダーは、無駄を省き、画像診断センターが患者の滞留を解消するのに役立つAI対応注射器による投与の自動化を急いでいます。持続可能性は現在、安全性と並ぶ購買基準の中核となっており、生分解性またはマンガンをベースとする代替品の研究を促しています。同時に、日常的な画像診断の外来へのシフトは、より少量のパッケージングと単一患者への送達システムへと需要を再分配しています。

世界の造影剤市場の動向と洞察

大環状ガドブトロールとガドピクレノール:迅速な承認取得が需要を後押し

ガドブトロールやガドピクレノールなどの大環状化合物は、直鎖状化合物に比べて体内組織におけるガドリニウムの残存量が少ないため、世界の規制当局は承認取得を急ピッチで進めています。欧州医薬品庁はすでにいくつかの直鎖型製剤を市場から排除しており、病院がMRIプロトコルを変更するのに拍車をかけています。ドイツがん研究センターのデータでは、大環状製剤の組織滞留性が低いことが確認されており、この保証は、繰り返しフォローアップ検査を行う神経科医や循環器科医の共感を呼んでいます。ガドリニウムの投与は毎年約4億回行われるため、プロトコルの切り替えは大きな交換サイクルを生み出し、単位需要と平均販売価格の両方を押し上げます。初期段階の承認を獲得したベンダーは、現在、拡張された独占権を活用し、さらに強固な分子ケージを持つ次世代キレートに資金を供給しています。北米の支払機関も、大環状化合物に有利な償還スケジュールを更新しており、採用曲線が加速し、造影剤市場がマージンを犠牲にすることなく数量を増やすのに貢献しています。

無駄を省くAI主導の自動注射システム

スマートインジェクターは、患者の体重、糸球体濾過率、スキャンタイプを組み合わせて、リアルタイムで流量を調節します。2024年に発表されたEuropean Congress of Radiologyの調査では、診断の明瞭さを犠牲にすることなく、CTスキャン1回あたり平均30%の造影剤節約が示されました。画像保存通信システム(PACS)と統合すると、バッチ番号が自動的に記録され、ファーマコビジランスデータの追跡に役立ちます。画像処理室では、1回の検査につき最大3分の時間短縮が報告されており、スキャン枠の拡大や病室の利用率向上に繋がっています。パンデミックによる医薬品不足から回復しつつある市場では、廃棄物削減機能は事業継続のテコにもなります。メーカーは独自のアルゴリズムをクローズド・ループ・ハードウェアに組み込むことで、高いスイッチング・コストを生み出し、市場競争力を強化しています。

OEMのマージンを圧迫する世界のヨウ素価格変動

ヨウ素のスポット価格は2021年から2023年にかけて3倍に上昇し、イオヘキソールおよびヨウジキサノール製造業者のコスト構造に打撃を与えました。2022年の上海封鎖は、GEヘルスケアの生産量を80%削減し、病院が最大85%の使用量削減を余儀なくされたことで、その脆弱性を浮き彫りにしました。メーカーは現在、原料となるヨウ素をチリと日本から二重に調達しているが、輸送コストと地政学的リスクは依然として残っています。低ヨウ素製剤を試行しているベンダーもあるが、投与量が増える可能性があり、節約効果は中和されます。保険会社は、突然の投入量の高騰をカバーできるほど迅速に償還額を調整することはほとんどないため、粗利益率は圧迫され、新プラントへの資本支出は鈍化します。価格の乱高下が収まるまでは、調達担当者は多様な供給を行うベンダーを支持し、造影剤市場におけるバイヤーの選好を微妙に変化させると思われます。

セグメント分析

2024年の造影剤市場の62.1%はヨード溶液で占められており、これはCTが救急診断や腫瘍診断で中心的な役割を果たしていることに支えられています。このリーダーシップは、供給ショックによって二重調達や低濃度製剤の必要性が浮き彫りになっても続いています。ベンダーは、40%少ないヨウ素で高解像度画像を提供するフォトンカウンティングCTスキャナーと組み合わせるために、粘度と浸透圧を最適化しています。ヨード製剤はまた、OECD加盟国の多くで保険償還経路が確立されていることも利点となっています。しかし、環境と腎臓の安全性への配慮から、代替化学物質の実験が推進され、成長率は緩やかになっています。

マイクロバブル分野は、ポイントオブケア超音波検査に後押しされ、2030年までのCAGRは14.8%となる見込みです。マイクロバブルが電離放射線被曝なしに5分以内に心筋灌流画像を増幅することを救急医が知れば、採用は急増します。新興企業は、保存期間を2年に延長する凍結乾燥製剤に取り組んでおり、マイクロバブルを低資源環境での採用に位置づけています。日本では、小児肝臓の適応について規制上の許可が下り、対処可能な範囲がさらに広がっています。その結果、マイクロバブルはセグメントレベルで造影剤市場規模を最も大きく押し上げることになります。

X線/CTは2024年に造影剤市場全体の69.2%を占めるが、これはCTが依然として外傷、脳卒中、がんの病期分類の第一選択モダリティであるためです。フォトンカウンティング検出器は、低線量でより鮮明な画像が得られるため、成熟した地域でも台数の伸びを維持できる可能性があります。しかし、モダリティに特化した線量最適化ソフトウェアが、スキャン1ミリリットルあたりの使用量を低下させており、出来高のみによる収益の伸びを抑えています。一方、ベンダーは造影剤の売上を長期的な機器サービス契約に結びつけ、病院のロイヤリティを固定しています。

2030年までのCAGRが11.5%になると予測される超音波検査は、解剖学的画像診断の枠を超え、リアルタイムの組織灌流評価にまで発展するマイクロバブルのブレークスルーにかかっています。VEGFを発現する腫瘍をターゲットとする分子標的マイクロバブルは初期の臨床試験段階にあり、特定の腫瘍学ワークフローにおいて将来的にMRIから代替されることを示唆しています。産科や救急外来で超音波が広く使用されるようになったことで、造影機能に対する認識が広まり、使用者の裾野が広がっています。これらの開発により、造影剤市場の拡大における超音波の役割が強化されます。

造影剤市場は、タイプ(ヨード化造影剤、ガドリニウムベース造影剤、マイクロバブル造影剤、その他)、イメージングモダリティ(X線/コンピュータ断層撮影(CT)、磁気共鳴画像法(MRI)、その他)、適応症(心血管疾患、腫瘍、その他)、エンドユーザー(病院、その他)、地域(北米、欧州、アジア太平洋、その他)。

地域分析

北米は2024年に造影剤市場の36.18%を占めたが、これは広範なイメージングインフラと高度なモダリティに報いる償還制度を背景にしたものです。大環状GBCAの使用量はMRI造影剤投与量の90%を超え、安全性勧告への迅速な対応を示します。アルツハイマー病や多発性硬化症のモニタリングに関連する神経カメラは安定したベースライン需要に貢献し、心臓CTプログラムは慢性冠疾患ガイドラインの更新に対応して拡大します。AIを活用した注射器は、ベンチャーキャピタルの医療技術への強力な支援により迅速に展開され、米国の施設は原材料価格ショックから身を守る無駄削減イノベーションをいち早く利用できるようになります。

アジア太平洋地域は2030年まで最も急速に成長する地域であり、中国の大規模な手術件数、インドの拡大する放射線科のフットプリント、日本の継続的な技術アップグレードがその要因です。中国の低ヨウ素剤国家調達政策は、ヨウ素消費量に比例することなく量の増加を促進し、弾力的なサプライチェーンを強化します。2024年10月、富士フイルムは小児用マイクロバブル製剤の国内承認を取得し、新規製剤に対する規制当局の寛容さを示すとともに、対応可能な患者プールを拡大します。インドでは官民パートナーシップによりTier2都市にCTが新たに設置され、これまで十分なサービスを受けられなかった人々に造影剤を用いた画像診断が提供され、造影剤市場全体の成長を後押ししています。

欧州は安定した基本需要を維持しつつ、持続可能性に傾注しています。いくつかの国の医療サービスでは、大環状GBCAを導入する病院や廃水回収を実施する病院に対して財政的ボーナスを提供しています。2025年4月、スウェーデンのスパゴ・ナノメディカル社によるナノ粒子MRI薬剤の前臨床試験結果が、グリーンケミストリーのイノベーションに対する同地域の貢献を示します。EUの大規模病院が、将来のガドリニウム廃棄規制を見越して、マンガン造影剤を評価するコンソーシアムに参加します。規制が強化されるにつれ、欧州の購買方針は明確な環境ロードマップを持つベンダーに有利に働く可能性が高く、造影剤市場の競争力学に影響を与えます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 世界中で大環状化合物ガドブトロールとガドピクレノールの承認が加速し、代替需要が高まる

- ヨウ素供給制約に対処するため、中国における低用量ヨウ素剤の迅速な導入

- AI駆動型自動注入システムにより造影剤の無駄を削減し、スキャンスループットを向上

- 救急部門におけるポイントオブケア超音波の普及がマイクロバブル剤の普及を促進

- EU5カ国における造影マンモグラフィーの保険償還拡大により検査件数が増加

- CMS OPPS更新に伴う米国における外来心臓CTへの移行

- 市場抑制要因

- 世界のヨウ素供給価格の変動がOEMの利益率を圧迫

- ガドリニウム廃水排出に対する環境監視の強化

- 副作用訴訟が医師による新薬採用を阻む

- 近々施行されるEUのMDR規制により、線形ガドリニウム製剤の製品ポートフォリオが厳格化

- バリューチェーン分析

- 規制の見通し

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- タイプ別

- ヨウ素化造影剤

- ガドリニウムベース造影剤

- マイクロバブル造影剤

- バリウム系造影剤

- その他

- 画像診断法別

- X線/コンピュータ断層撮影(CT)

- 磁気共鳴画像法(MRI)

- 超音波

- 核イメージング(SPECT/PET)

- 適応症別

- 心血管疾患

- 腫瘍学

- 胃腸障害

- 神経疾患

- 腎臓疾患

- 筋骨格系障害

- その他の適応症

- エンドユーザー別

- 病院

- 診断画像センター

- 外来手術センター

- 学術研究機関

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他のアジア

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- Bayer AG

- GE HealthCare

- Bracco Imaging S.p.A

- Guerbet Group

- Lantheus Medical Imaging Inc.

- FUJIFILM Corporation

- Beijing Beilu Pharmaceutical Co. Ltd.

- Taejoon Pharm Co. Ltd.

- Spago Nanomedical AB

- Nano Therapeutics(NTI Ltd.)

- Jiangsu Hengrui Medicine Co. Ltd.

- Fresenius Kabi AG

- NanoPET Pharm GmbH

- Starry Pharma Group Co. Ltd.

- Guerbet U.S. Holdings Inc.

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日