|

市場調査レポート

商品コード

1940817

システムオンチップ(SoC):市場シェア分析、業界動向と統計、成長予測(2026年~2031年)System On Chip (SoC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| システムオンチップ(SoC):市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 156 Pages

納期: 2~3営業日

|

概要

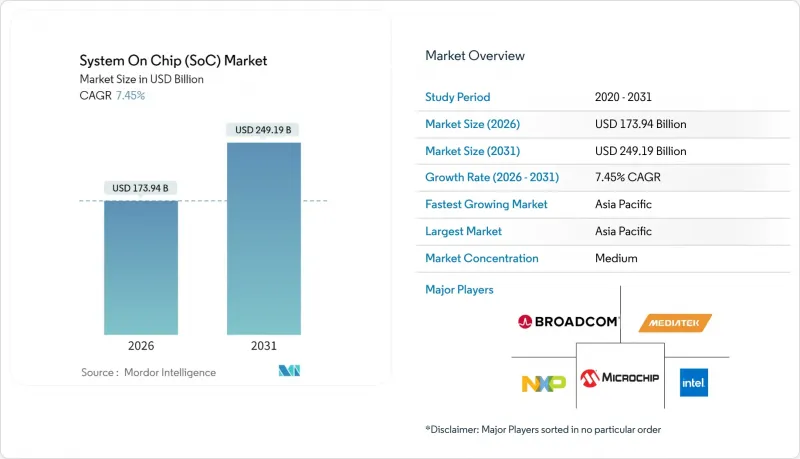

システムオンチップ(SoC)市場は、2025年の1,618億8,000万米ドルから2026年には1,739億4,000万米ドルへ成長し、2026年から2031年にかけてCAGR7.45%で推移し、2031年までに2,491億9,000万米ドルに達すると予測されています。

スマートフォンの更新サイクルの鈍化は、エッジネイティブAI推論と5Gクライアントデバイスの急速な普及によって相殺され、出荷台数は安定し、平均ダイサイズは拡大しました。ティア1自動車メーカーは数十の制御ユニットを集中型コンピューティングドメインに統合し、マルチコアでASIL-D対応のSoCに対する需要を高めました。ハイパースケーラーは自社設計で市販シリコンを置き換え続け、先進的パッケージングプロバイダーの潜在市場を拡大しました。米国、日本、欧州連合における地域別のファブ奨励策が生産能力の拡大を後押しし、サプライチェーンリスクを緩和するとともに、現地生産を前提とした設計戦略を促進しました。

世界のシステムオンチップ(SoC)市場の動向と洞察

5G対応デバイスの需要急増

スタンドアロン方式の5Gネットワーク第一波は、アップリンク予算の厳格化とベースバンドの複雑化をもたらし、スマートフォンOEMメーカーはモデムサブシステム内にAIチューニングエンジンを組み込む必要に迫られました。クアルコムのSnapdragon 8 Eliteは、Release 17クラスのモデムと45 TOPSのニューラルエンジンを組み合わせ、前世代比でワット当たりの性能を45%向上させました。MediaTekのDimensity 9400も同様の階層構造を採用し、2025年初頭に発売されたプレミアムスマートフォン向けインライン動画強化機能を加速させました。産業用ルーター向けコンパニオンモジュールもこの統合を再現し、クラウド経由の往復通信なしにスマートファクトリーセル内でサブミリ秒単位の作動を実現しました。その結果、スマートフォンと産業用ゲートウェイの更新が、システムオンチップ(SoC)市場全体における短期的な収益の波動を増幅させました。

IoTとAIエッジの急速な普及

分散型推論ワークロードの増加により、設計者は汎用コア、DSP、ニューラルアクセラレータを単一ダイ上に統合する必要に迫られました。EdgeCortix社のSAKURA-IIは、10ワット未満の消費電力で40 TOPSを実現し、ライン上で部品を検査する産業用カメラに採用されました。スマートシティ統合事業者は、交通信号キャビネットにマイクロサーバーを後付けし、メタデータを送信する前にビデオストリームをローカルで圧縮することで、バックホールを80%削減しました。このアーキテクチャ転換により、ノードあたりのシリコン含有量が増加すると同時に設計サイクルが短縮され、その結果、ヘテロジニアス/フュージョンSoCがシステムオンチップ(SoC)市場で最も急成長している分野となりました。

5nm以下の設計およびマスクコストの急騰

TSMCの2nmノードにおけるマスクセット費用は、2024年末にウエハー1枚あたり3万米ドルを超え、3nmノード比で50%高騰しました。これにより複雑なSoCのプロジェクト総予算は1億米ドル規模に膨れ上がりました。このような支出を負担できるファブレス企業はごく一部に限られており、多くの設計者は成熟したノードに留まることを余儀なくされています。これにより機能統合が制限され、最先端のEDAベンダーのTAM成長は鈍化しています。

セグメント分析

デジタルSoCデバイスは2025年の収益の52.45%を占め、スマートフォンや汎用コンピューティング分野での普及度を反映しました。設計者は階層を跨いだスケーラブルなIPライブラリを再利用し、コスト曲線を平準化するとともに、派生製品の迅速な投入を可能としました。しかしながら、チップレットベースの積層技術の登場は、モノリシックデジタルの優位性に対する初の構造的課題をもたらしています。CPU、GPU、NPU、特殊アクセラレータを単一インターポーザ上に統合するヘテロジニアス/フュージョンSoCは、CAGR9.7%の見通しを示し、従来型デジタルフォーマットからシェアを奪い取りました。混合信号バリエーションは、センサーフュージョンと電力管理が交差する領域(例:バッテリーBMSコントローラー)において依然として重要性を維持しました。RF/接続性SoCはWi-Fi 7および5G RedCapの展開拡大を活かし、アナログ中心デバイスはパワートレインおよび産業用ドライブ分野を支えました。その結果、SoC市場はデジタル分野での数量的優位性を維持しつつ、増分的な研究開発をモジュール化されたドメイン特化型ハイブリッドへ方向転換する過渡期を迎えています。

このアーキテクチャの再編はファウンダリの構成にも変化をもたらしました。純粋なデジタルテープアウトは稼働率の高い7/6nmプロセスラインに集中する一方、初期のヘテロジニアスプロトタイプでは5nmロジックダイと16nmアナログチップレットを組み合わせ、TSMCのSoICパッケージングフローに組み込まれました。この分割により、アナログIPを超微細なフィン幅縮小によるペナルティから保護し、リスク低減を図りました。ベンダー各社はユニバーサル・チップレット・インターコネクト・エクスプレス(UCIe)仕様を通じた標準化を推進し、2026年以降のマルチソース・チップレットマーケットプレースの活性化を目指しました。相互運用性が成熟するにつれ、システムオンチップ(SoC)市場では製品タイプの更新が加速し、設計サイクルの短縮とダイからパッケージまでの価値創出の拡大が見込まれます。

2025年には、携帯電話、ウェアラブル機器、ARグラスが予測可能な12~18ヶ月のサイクルで更新されたため、民生用電子機器が収益の45.58%を占めました。コンテンツ面での成長は、生成AIカメラ機能をサポートする大規模なISPクラスターから生じました。しかし、自動車分野が通信インフラ分野を抜き、2031年までCAGR13.85%で最も成長が速い分野となりました。この変化は、限られた車両コンピューティングノード上で知覚処理・領域制御・インフォテインメントワークロードを集中化するソフトウェア定義車両のロードマップに起因します。ティア1サプライヤーは複数年にわたる半導体供給契約を締結し始め、割り当てリスクを抑制するとともに、SoCメーカーに比類のない需要可視性を提供しました。産業用・IoTセグメントは、PLC上に予知保全モデルを実装する既存設備改修の支援を受け、安定した一桁台の成長を維持しました。

医療分野では、体内連続血糖モニターの規制認可が、統合無線機能を備えた超低消費電力バイオメディカルSoCの需要を押し上げました。データセンター需要は、AWSなどのハイパースケーラーが自社開発のGraviton4 CPUを採用したことで変化し、汎用サーバーCPUの総市場規模(TAM)は縮小したもの、ラック内での光コントローラーの共封装需要を促進しました。通信インフラ分野の収益は5G Advancedベースバンドのアップグレードで恩恵を受けましたが、オープンRANの価格設定により利益率は縮小しました。全体として、システムオンチップ(SoC)市場は、消費者向け携帯電話の周期的な変動を緩和するために、自動車およびエッジAI IoTの受注に依存しており、業界を横断した多様な需要構造を浮き彫りにしました。

システムオンチップ(SoC)市場は、製品タイプ(デジタルSoC、アナログSoC、ミックスドシグナルSoC、RF/コネクティビティSoCなど)、エンドユーザー産業(民生用電子機器、通信インフラ、自動車など)、プロセスノード(28nm以上、16/14nm、10/8nm、7/6nmなど)、アプリケーション(スマートフォン・タブレット、エッジAI・IoTデバイス、サーバー・データセンター、自動車用ADAS/インフォテインメントなど)、地域別に分析しております。

地域別分析

アジア太平洋地域は2025年に54.20%の収益を占め、2031年までCAGR9.75%で全地域を上回る成長を継続しました。中国の「リトルジャイアント」補助金プログラムは200社以上の国内SoCスタートアップを支援し、各社が低軌道衛星モデムから自動車用LiDAR信号プロセッサまで垂直分野のニッチ市場をターゲットとしています。韓国のIDM企業は、自社生産のDRAMとHBMを活用し、メモリと演算タイルをバンドルすることでエコシステムの結束力を強化しました。台湾のファウンダリ群はプロセス技術における優位性を維持し、2025年第2四半期には2nmゲートオールアラウンドプロセスによる初のリスクウエハーを出荷しました。一方、日本のファブはEV駆動用インバーター向けワイドバンドギャップパワーSoCに特化しています。

北米では、インテルによるオハイオ州への200億米ドル規模の投資と、2025年4月にパイロット運転を開始したニューメキシコ州の新パッケージング工場が追い風となりました。AWSは2024年7月以降、米国5つのアベイラビリティゾーンにGraviton4ベースのインスタンスを展開し、ウェブ層のパフォーマンスが30%向上したと報告。これにより国内設計サイクルを加速するシリコン・フライホイールを確立しました。政府の輸出規制改正により中国との二国間貿易は制約を受けましたが、堅調なクラウド・防衛支出により、同地域のCAGRは高い一桁台を維持しました。

欧州は自動車用シリコン技術の卓越性を軸に転換を図りました。ドイツの自動車メーカー各社はADASコンピューティングを確保するため、インフィニオンおよびSTマイクロエレクトロニクスと複数世代にわたる供給契約を締結。一方、EUチップ法は2030年までに地域生産能力を倍増させるため430億ユーロ(479億米ドル)を拠出することを約束しました。フランスとイタリアは産業用自動化システム向け3DICモジュール用ウエハーレベルパッケージングラインを共同出資し、インダストリー4.0展開における供給自律性を確保しました。これらの動向は、アジア太平洋地域が数量面で優位性を維持する一方、システムオンチップ(SoC)市場が規模と回復力のバランスを取る三極供給構造へと進化していることを示しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 5G対応デバイスの需要急増

- IoTおよびAIエッジの急速な普及

- 自動車業界における集中型E/Eアーキテクチャへの移行

- 補助金による地域ファブ増設

- チップレットベースのヘテロジニアス統合の勢い

- エッジネイティブAIモデル推論の必要性

- 市場抑制要因

- 5nm未満の設計およびマスクコストの急騰

- 輸出管理によるサプライチェーンの脆弱性

- 未成熟なチップレット相互運用性標準

- ハイエンドSoCにおける熱密度限界

- マクロ経済要因の影響

- バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- チップレット導入と分散化の動向分析

第5章 市場規模と成長予測

- 製品タイプ別

- デジタルSoC

- アナログSoC

- ミックスドシグナルSoC

- RF/接続性SoC

- ヘテロジニアス/フュージョンSoC

- エンドユーザー業界別

- 民生用電子機器

- 通信インフラ

- 自動車

- コンピューティングおよびデータセンター

- 産業用およびIoT

- ヘルスケアおよび医療機器

- プロセスノード別

- 28 nm以上

- 16/14 nm

- 10/8 nm

- 7/6 nm

- 5/4/3 nm

- 2 nm以下/3-DIC

- 用途別

- スマートフォンとタブレット

- エッジAIおよびIoTデバイス

- サーバーおよびデータセンター

- 自動車用ADAS/インフォテインメント

- 産業オートメーション

- ウェアラブル機器とスマートホーム

- 地域別

- 北米

- 米国

- カナダ

- 南米

- ブラジル

- その他南米

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- 韓国

- 台湾

- インド

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Advanced Micro Devices Inc.

- Apple Inc.

- Arm Holdings plc

- Broadcom Inc.

- Rockchip Electronics Co., Ltd.

- Google LLC(Tensor SoC)

- HiSilicon Technologies Co., Ltd.

- Infineon Technologies AG

- Intel Corporation

- Marvell Technology Inc.

- MediaTek Inc.

- Microchip Technology Inc.

- Nvidia Corporation

- NXP Semiconductors N.V.

- Qualcomm Technologies Inc.

- Realtek Semiconductor Corp.

- Renesas Electronics Corporation

- Samsung Electronics Co., Ltd.(System LSI)

- SiFive Inc.

- Silicon Labs Inc.

- STMicroelectronics N.V.

- Taiwan Semiconductor Manufacturing Company Limited

- Texas Instruments Incorporated

- Allwinner Technology Co., Ltd.

- UNISOC Technologies Co., Ltd.