|

|

市場調査レポート

商品コード

1440436

ステンレス鋼:市場シェア分析、業界動向と統計、成長予測(2024-2029)Stainless Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ステンレス鋼:市場シェア分析、業界動向と統計、成長予測(2024-2029) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

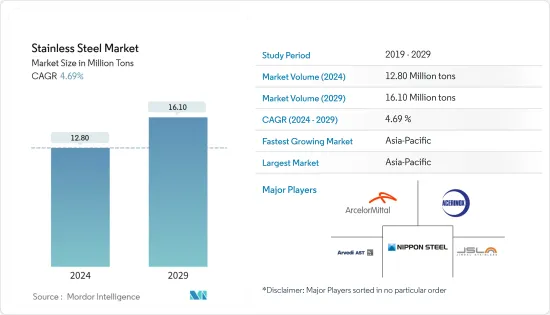

ステンレス鋼市場規模は2024年に1,280万トンと推定され、2029年までに1,610万トンに達すると予測されており、予測期間(2024年から2029年)中に4.69%のCAGRで成長します。

主なハイライト

- 新型コロナウイルス感染症(COVID-19)のパンデミックは市場に悪影響を及ぼしました。ロックダウンや制限措置により製造施設や工場が停止したためです。サプライチェーンと輸送の混乱により、さらに市場に障害が生じました。しかし、業界は2021年に回復を見せ、調査対象市場の需要が回復しました。

- 短期的には、建築・建設業界および自動車業界からの需要の増加が、調査対象市場の成長を促進する要因の一部です。

- 一方で、生産コストの高さと原材料価格の変動の上昇により、調査対象の市場の成長が妨げられる可能性があります。

- しかし、アジア太平洋の産業とインフラの発展は、調査対象市場にとってチャンスとなる可能性が高いです。

- アジア太平洋地域は市場を独占すると予想されており、予測期間中に最高のCAGRを示す可能性もあります。

ステンレス鋼市場動向

建設業界での使用の増加

- ステンレス鋼は、アーキテクチャ、建設、建築のあらゆる面で使用されています。耐食性が優れているため、ほとんどの建築設計および構造エンジニアリング会社は、より腐食しやすい場所には、より高合金化されたモリブデン含有ステンレス鋼を好みます。

- ステンレス鋼は建設業界で最も急速に成長している分野です。ステンレス鋼製品は、梁、柱などの構造用途や一般建築用途に使用されます。手すり、屋根、エレベーター、階段、プールのシェード、アトリウムなど、さまざまな用途に使用されています。

- 人口増加と都市化により、世界中で住宅、商業ビル、病院の建設需要が高まっています。都市化が進むと、より多くの建物やインフラの開発が必要になります。例えば、インドは今後もG20諸国の中で最も急成長を遂げると予想されています。インド政府は、27の産業クラスター開発に1,205億米ドル、道路、鉄道、港湾接続プロジェクトに753億米ドルを含む、3年間(2023~2025年)のインフラ投資目標を3,765億米ドルと発表しました。したがって、インフラプロジェクトへの投資の増加は、ステンレス鋼市場に上向きの需要を生み出すと予想されます。

- さらに、サウジアラビアは多くの商業プロジェクトに取り組んでおり、国内でさらに多くの商業ビルが建設される可能性があります。 5,000億米ドルの未来的巨大都市「ネオム」プロジェクト、紅海プロジェクト-フェーズ1は2025年までに完了予定で、5つの島と2つの内陸リゾートに3,000室の高級および超高級ホテル14軒が建設されます。キディヤエンターテイメントシティ、超高級ウェルネス観光地アマーラ、アルウラーにあるジャンヌーヴェルのシャランリゾート。したがって、商業建設プロジェクトへの投資の増加は、ステンレス鋼市場に上向きの需要を生み出すと予想されます。

- 米国には世界最大の建設産業があり、その価値は2022年に1兆7,920億米ドル、2021年には1兆6,265億米ドルに達します。さらに、2022年には、建設産業による米国の国内総生産(GDP)への付加価値は、約1兆米ドルでした。これは、GDPに9,588億米ドルが追加された前年に比べて大幅な増加でした。

- 米国国勢調査局によると、2008年の景気後退中に米国の商業建設市場が著しく低下した後、導入された商業建設の金額は景気後退前の数字に回復し、2022年には1,150億米ドルに達しました。 2021年と比較して21.4%の増加を示しました。2022年の米国の商業建設着工額は、不動産の種類によって大きく異なりました。学校および大学の建設着工は、製造業と並んで市場シェアが最も高いカテゴリーでした。倉庫の着工額は2022年に270億米ドルを超えました。したがって、この国のステンレス鋼市場は、国内の商業建設業界からの需要が上向くと予想されています。

- さらに、米国建築家協会(AIA)の建設コンセンサス予測委員会によると、米国の非住宅建築の建設支出は2023年に5.8%の成長を遂げると予想されています。2023年までに、すべての主要な商業および施設のカテゴリーは、少なくともかなり健全な利益を得ることができます。その後の増加により、予測期間におけるステンレス鋼市場の成長が促進されると予想されます。

- これらすべての要因により、ステンレス鋼市場は予測期間中に世界的に成長する可能性があります。

アジア太平洋地域が市場を独占

- アジア太平洋地域ではステンレス鋼産業が大幅に成長しています。中国やインドなどの国が消費の大きなシェアを占めています。アジア太平洋地域における外国企業の存在感の増大により、新しいオフィスやビルの建設需要も生まれています。

- 自動車産業からの需要の高まりにより、予測期間中にこの地域のステンレス鋼市場がさらに押し上げられました。

- 中国の自動車産業は、バッテリー駆動の電気自動車に対する消費者の嗜好が高まるにつれ、動向の変化を経験しています。中国の自動車部門の拡大はステンレス鋼の需要に恩恵をもたらすと予想されています。国際自動車工業機構(OICA)によると、中国は世界最大の自動車生産国であり、世界の自動車生産台数のほぼ34%を占めています。 2022年にこの国は2,702万615台の自動車を生産し、2021年の2,612万1,712台と比較して24%の増加を記録しました。したがって、自動車生産の増加はステンレス鋼の需要の上振れを引き起こすと予想されます。市場。

- さらに、中国はステンレス鋼市場においてアジア太平洋で最大の市場シェアを保持しています。国内の投資と建設活動の増加により、ステンレス市場の需要は予測期間を通じて増加すると予想されます。中国は過去数年間、世界のインフラへの主要な投資国の一つであり、多大な貢献をしています。たとえば、中国国家統計局(NBS)によると、2022年の中国の建設工事の生産額は27兆6,300億人民元( 4兆1,085億8,100万米ドル)に達し、2021年と比較して6.6%増加しました。建設業界への投資の増加により、国内のステンレス鋼市場の需要が上向きになることが予想されます。

- さらに、インドにおける自動車産業への投資の増加と進歩により、高張力鋼の消費が増加すると予想されます。たとえば、タタモーターズは2022年4月、今後5年間で乗用車事業に30億8,000万米ドルを投資する計画を発表しました。これは、国内のステンレス鋼市場にプラスの影響を与えることが期待されます。

- インフラ部門はインド経済の重要な推進力です。この部門はインド全体の発展を推進することに大きな責任を負っています。例えば、インド・ブランド・エクイティ財団(IBEF)によると、2022年12月にAAIと他の空港開発業者は約2億ルピーの資本支出を目標としています。今後5年間で空港部門に9万8000億米ドル(118億米ドル)が投じられ、既存ターミナルの拡張と改造、新しいターミナル、滑走路の強化その他の活動。したがって、この拡大はステンレス鋼市場に上向きの需要を生み出すと予想されます。

- OECによると、2022年2月から2023年2月の間に、日本のステンレス鋼線の輸出は17億5,000万円(1,340万米ドル)から16億5,000万円(1,270万米ドル)へと9,680万円(-5.54%)[74万5,000米ドル]減少しました。輸入は12億3,000万円(947万1,000米ドル)から12億4,000万円(954万8,000米ドル)へと1,340万円(+1.09%)[10万3,000米ドル]増加しました。したがって、同国からのステンレス鋼線の減少は、同国のステンレス鋼市場に影響を与えることが予想されます。

- このようなすべての要因により、この地域のステンレス鋼市場は予測期間中に着実に成長すると予想されます。

ステンレス鋼業界の概要

ステンレス鋼市場は本質的に部分的に統合されています。この市場の主要企業には(順不同)、日本製鉄株式会社、Acerinox、ArcelorMittal、Jindalステンレス Limited、およびAcciai Speciali Terni SpAなどが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 建設業界からの需要の拡大

- 自動車業界からの需要の増加

- その他の 促進要因

- 抑制要因

- 代替要員の確保

- その他の拘束具

- 業界のバリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替製品やサービスの脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模(数量))

- 製品

- コールドフラット

- ホットコイル

- コールドバー

- ホットバー

- ホットプレートとシート

- その他の製品

- 用途

- 自動車および輸送

- 建築と建設

- 金属製品

- 電気機械

- 機械工学

- その他の用途

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東とアフリカ

- サウジアラビア

- 南アフリカ

- その他中東およびアフリカ

- アジア太平洋

第6章 競合情勢

- 合併と買収、合弁事業、コラボレーション、および契約

- 市場シェア(%)**/ランキング分析

- 有力企業が採用した戦略

- 企業プロファイル

- Acciai Speciali Terni SpA

- Acerinox

- Aperam

- ArcelorMittal

- Baosteel Group

- China Baowu Steel

- JFE Steel Corporation

- Jindal Stainless Limited

- NIPPON STEEL CORPORATION

- Outokumpu

- POSCO

- thyssenkrupp Stainless GmbH

- TSINGSHAN HOLDING GROUP

第7章 市場機会と将来の動向

- アジア太平洋の産業およびインフラ開発

- その他の機会

目次

Product Code: 91424

The Stainless Steel Market size is estimated at 12.80 Million tons in 2024, and is expected to reach 16.10 Million tons by 2029, growing at a CAGR of 4.69% during the forecast period (2024-2029).

Key Highlights

- The COVID-19 pandemic negatively impacted the market. This was because of the shutdown of the manufacturing facilities and plants due to the lockdown and restrictions. Supply chain and transportation disruptions further created hindrances for the market. However, the industry witnessed a recovery in 2021, thus rebounding the demand for the market studied.

- Over the short term, increasing demand from the building and construction and automotive industries are some of the factors driving the growth of the market studied.

- On the flip side, high production costs and rising fluctuations in raw material prices is likely to hinder the growth of the market studied.

- However, industrial and infrastructure development in Asia-Pacific is likely to act as an opportunity for the studied market.

- The Asia-Pacific region is expected to dominate the market and is also likely to witness the highest CAGR during the forecast period.

Stainless Steel Market Trends

Increasing Usage in the Construction Industry

- Stainless steel is used in all aspects of architecture, construction, and building. Due to the better corrosion resistance, most architectural design and structural engineering firms prefer more highly alloyed molybdenum-containing stainless steels for more corrosive locations.

- Stainless Steel is the fastest-growing sector in the construction industry. Stainless Steel products are used in structural applications such as beams, columns, and general architectural applications. It is used in a variety of applications, including railings, roofing, lifts, staircases, swimming pool shades, and atriums.

- Due to rising population and urbanization, there is a growing demand for the construction of residential and commercial buildings, as well as hospitals, all over the world. Increased urbanization necessitates the development of more buildings and infrastructure. For instance, India is anticipated to remain the fastest-growing G20 economy. The Indian government announced a target of USD 376.5 billion in infrastructure investment over three years (2023-2025), including USD 120.5 billion for developing 27 industrial clusters and USD 75.3 billion for road, railway, and port connectivity projects. Therefore, the increasing investments in infrastructure projects are expected to create an upside demand for the stainless steel market.

- Moreover, Saudi Arabia is working on a lot of commercial projects, which will likely lead to more commercial buildings in the country. The USD 500 billion futuristic mega-city "Neom" project, the Red Sea Project - Phase 1, which is expected to be completed by 2025 and has 14 luxury and hyper-luxury hotels with 3,000 rooms spread across five islands and two inland resorts, Qiddiya Entertainment City, Amaala - the uber-luxury wellness tourism destination, and Jean Nouvel's Sharaan resort in Al-Ula. Therefore, the increasing investments in commercial construction projects are expected to create an upside demand for the stainless steel market.

- The United States has one of the world's largest construction industries, valued at USD 1,792 billion in 2022 and USD 1,626.5 billion in 2021. Furthermore, in 2022, the value added to the gross domestic product (GDP) of the United States by the construction industry was around USD 1 trillion. This was a large increase from the previous year when USD 958.8 billion were added to the GDP.

- According to the US Census Bureau, after a noticeable drop in the United States commercial construction market during the 2008 recession, the value of commercial construction that has been put in place has recovered to pre-recession figures, reaching USD 115 billion in 2022, which showed an increase of 21.4% compared to 2021. The value of commercial construction starts in the United States in 2022 varied significantly depending on the property type. School and college construction starts were the categories, along with manufacturing, with the highest market share. The construction starts of warehouses amounted to over USD 27 billion in 2022. Therefore, the stainless steel market in the country is expected to have an upside demand from the country's commercial construction industry.

- Furthermore, according to the American Institute of Architects (AIA) Construction Consensus Forecast Panel, nonresidential building construction spending in the United States is likely to witness a growth of 5.8% in 2023. By 2023, all the major commercial and institutional categories are projected to witness at least reasonably healthy gains. The subsequent increase is expected to enhance the growth of the stainless steel market in the forecast period.

- Owing to all these factors, the market for stainless steel is likely to grow globally during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region has seen significant growth in the stainless steel industry; countries such as China and India account for significant consumption shares. The growing presence of foreign companies in the Asia-Pacific region has also created a demand for the construction of new offices and buildings.

- The growing demand from the automotive industry further boosted the market for stainless steel in the region during the forecast period.

- The automobile industry in China is experiencing shifting trends as consumer preference for battery-powered electric vehicles rises. The expansion of China's automotive sector is expected to benefit stainless steel demand. According to the International Organization of Motor Vehicle Manufacturers (OICA), China is the world's largest automobile producer, accounting for nearly 34% of global volume. In 2022, the country produced 2,70,20,615 units of automobiles, registering an increase of 24% compared to 2,61,21,712 units in 2021. Therefore, increasing in the production of automobiles is expected to create an upside demand for stainless steel market.

- Moreover, China holds the largest Asia-Pacific market share for stainless steel market. The demand for the stainless market is expected to rise throughout the forecast period due to rising investments and construction activity in the country. China is a huge contributor, as it has been one of the leading investors in infrastructure worldwide over the past few years. For instance, according to the National Bureau of Statistics (NBS) of China, in 2022, the output value of construction works in China amounted to CNY 27.63 trillion (USD 4108.581 billion), an increase of 6.6% compared with 2021. Therefore, the rising investments in the construction industry is expected to create an upside demand for stainless steel market in the country.

- Furthermore, increased investments and advancements in the automobile industry in India is expected to increase the consumption of high strength steel. For instance, in April 2022, Tata Motors announced plans to invest USD 3.08 billion in its passenger vehicle business over the next five years. This is expected to have a positive impact on the stainless steel market in the country.

- Infrastructure sector is a key driver for the Indian economy. The sector is highly responsible for propelling India's overall development. For instance, according to India Brand Equity Foundation (IBEF), in December 2022, AAI and other Airport Developers have targeted capital outlay of approximately Rs. 98,000 crore (USD 11.8 billion) in airport sector in the next five years for expansion and modification of existing terminals, new terminals and strengthening of runways, among other activities. Therefore, this expansion is expected to create an upside demand for stainless steel market.

- According to OEC, between February 2022 and February 2023 the exports of Japan's Stainless Steel Wire have decreased by JPY 96.8 million (-5.54%) [USD 0.745 million] from JPY 1.75 billion (USD 0.0134 billion) to JPY 1.65 billon (USD 0.0127 billion), while imports increased by JPY 13.4 million (+1.09%) [USD 0.103 million] from JPY 1.23 billion (USD 0.009471 billion) to JPY 1.24 billion (USD 0.009548 billion). Therefore, decrease in the stainless steel wires from the country is expected to affect the stainless steel market in the country.

- Due to all such factors, the market for Stainless Steel in the region is expected to have a steady growth during the forecast period.

Stainless Steel Industry Overview

The Stainless Steel Market is partially consolidated in nature. The major players in this market (not in a particular order) include NIPPON STEEL CORPORATION, Acerinox, ArcelorMittal, Jindal Stainless Limited, and Acciai Speciali Terni S.p.A., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from Construction Industry

- 4.1.2 Increasing Demand from Automotive Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Availability of Substitutes

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product

- 5.1.1 Cold Flat

- 5.1.2 Hot Coils

- 5.1.3 Cold Bars

- 5.1.4 Hot Bars

- 5.1.5 Hot Plate and Sheet

- 5.1.6 Other Products

- 5.2 Application

- 5.2.1 Automtoive and Transportation

- 5.2.2 Building and Construction

- 5.2.3 Metal Products

- 5.2.4 Electrical Machinery

- 5.2.5 Mechanical Engineering

- 5.2.6 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Acciai Speciali Terni S.p.A.

- 6.4.2 Acerinox

- 6.4.3 Aperam

- 6.4.4 ArcelorMittal

- 6.4.5 Baosteel Group

- 6.4.6 China Baowu Steel

- 6.4.7 JFE Steel Corporation

- 6.4.8 Jindal Stainless Limited

- 6.4.9 NIPPON STEEL CORPORATION

- 6.4.10 Outokumpu

- 6.4.11 POSCO

- 6.4.12 thyssenkrupp Stainless GmbH

- 6.4.13 TSINGSHAN HOLDING GROUP

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Industrial and Infrastructural Development in Asia-Pacific

- 7.2 Other Opportunities