|

市場調査レポート

商品コード

1440418

ホームヘルスハブ:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年)Global Home Health Hub - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ホームヘルスハブ:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

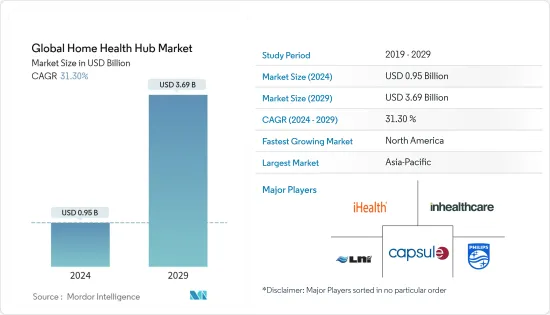

世界のホームヘルスハブ市場規模は、2024年に9億5,000万米ドルと推定され、2029年までに36億9,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に31.30%のCAGRで成長します。

世界的に、新型コロナウイルス感染症(COVID-19)のパンデミックは、人員不足で過重労働となっている病院やヘルスケアシステムに多大な圧力をかけています。ホームヘルスハブテクノロジーは、パンデミック中に病院、救急治療室、最前線のヘルスケア従事者のストレスを軽減しながら、患者が自宅内で安全を保つのに役立ち、市場にプラスの影響を与えています。 2021年8月に『Lancet Regional Health』誌に掲載された「在宅医療サービス、介護者、患者に対する新型コロナウイルス感染症の影響:フランスの経験からの教訓」と題された研究によると、COVID-19感染症のパンデミックが始まって以来、在宅医療は減少しています。病院の混雑を緩和し、慢性疾患や重症ではない新型COVID-19の患者を自宅でケア、監視できるようにするための需要が高まっています。したがって、ホームヘルスハブ市場はCOVID-19感染症によってプラスの影響を受けました。

ホームヘルスハブ市場は、慢性疾患の数が増加し、高齢者人口が増加するにつれて発展すると予測されています。さらに、スマートフォンの使用の拡大とヘルスケア費を削減したいという欲求の高まりが市場を前進させています。世界保健機関による2021年 7月の最新情報によると、心血管疾患は世界中で主な死因となっており、これには冠状動脈性心疾患、脳血管疾患、リウマチ性心疾患、先天性心疾患などが含まれます。同じ情報源によると、2019年には世界中で1,790万人が心血管疾患で死亡しており、これは全世界の死亡者数の約32%に相当します。さらに、Global Cancer Observatoryが発行したGlobocan 2020レポートでは、185か国における36のがんの発生率と死亡率を推定しました。 2020年に世界では、推定1,929万2,789人が新たにがんと診断され、約9,958,133人ががんにより死亡しました。さらに、同じ情報源によると、新たながん症例数は2030年までに24,044,406人に達すると予想されており、世界中でがんの罹患率が増加していることがわかります。

65歳以上の人々は慢性疾患にかかりやすいため、高齢者人口は調査対象の市場に大きな影響を与えると予想されます。世界保健機関の2021年の事実によると、世界人口に占める60歳以上の人口の割合は、2015年から2050年の間に12%から22%へとほぼ2倍に増加します。2050年までに、世界の高齢者の80%は低中流域で暮らすことになります。-所得国。人口の高齢化は過去に比べてはるかに速いスピードで進んでいます。どの国も、この人口動態の変化を活用するための医療および社会システムの準備を確保する上で、重大な課題に直面しています。

ただし、市場参加者によるさまざまな重要な戦略的活動が、予測期間中に市場を押し上げると予想されます。たとえば、2022年 3月、接続およびインターネットサービスの世界のプロバイダーであるVEON Ltd.は、バングラデシュのBanglalink移動体通信事業者として、同国初の統合デジタルヘルスプラットフォームであるHealth Hubを立ち上げたと発表しました。

したがって、前述のすべての要因が予測期間中に市場を牽引すると予想されます。ただし、セキュリティとプライバシーの懸念、償還の問題が市場の成長を制限する可能性のある要因です。

ホームヘルスハブ市場動向

スマートフォンベースのセグメントが予測期間中に市場を独占すると予想される

デジタルプラットフォームのスマートフォンの人気の高まりにより、スマートフォンベースのハブセクターの成長が促進され、現在最大の市場シェアを占めています。スマートフォンベースのハブには、専用のスマートフォンやタブレットにダウンロードできるモバイルプログラム(Android、iOS、Linux、Windows)が必要です。スマートフォンとタブレットは先進国におけるインターネット接続の主要な手段となりつつあり、新興諸国でもその使用が増加しています。

スマートフォンの使用量の増加と高速モバイルネットワークの継続的な成長により、患者情報へのアクセシビリティを向上させるためのモバイルプラットフォームの使用が増加しています。スマートフォン対応のホームヘルスハブは、認知度とアクセシビリティの向上に伴い、人気が高まることが予想されます。スマートフォンテクノロジーとインターネットに対する嗜好の高まりと、スマートフォンベースの健康ハブに対する需要の高まりにより、市場の成長が促進されると予想されます。ユーロスタットのデータによれば、2022年12月の最新情報によると、インターネットにアクセスできるEU世帯の割合は2021年までに92%に上昇し、2011年(72%)よりも約20ポイント高くなっています。さらに、2021年にはEU内の世帯の90%がブロードバンドインターネットアクセスを使用しており、2011年(65%)よりも25ポイント増加しました。

さらに、主要な市場プレーヤーによる製品の発売は、予測期間中に市場を押し上げると予想されます。たとえば、2022年 3月、GRS Indiaの新興企業は、災害や医療緊急事態時に安定した酸素供給を提供できる、新しいスマートフォンベースのポータブル酸素キットを発売しました。

したがって、前述のすべての要因が予測期間中に市場を押し上げると予想されます。

北米が市場を独占しており、予測期間中も同様に成長すると予想されます。

高度なテクノロジーの高度な導入、慢性疾患や生活習慣病の蔓延、ヘルスケア支出の増加、医師不足、より良いヘルスケアサービスに対する需要の増加などの要因が、北米が世界市場で大きなシェアを占める要因となっています。グロボカン2020年報告書によると、2020年に米国で推定2,281,658人が新たにがんと診断され、約612,390人が死亡しました。 2020年に米国で最も多かったがんは、乳がん(25万3,465件)、肺がん(22万7,875件)、前立腺がん(20万9,512件)、結腸がん(10万1,809件)でした。

さらに、ヘルスケア支出の増加と可処分所得の増加も、世界中の在宅医療ハブ市場を推進しています。 2022年 2月に発表されたPETERSON-KFF Health System Trackerデータによると、米国の医療支出は9.7%増加して2020年に4兆1,000億米ドルに達しました。これは2019年の4.3%増加よりもはるかに速いペースです。2020年の加速はこれは主にCOVID-19感染症のパンデミックに対応して発生した医療に対する連邦支出の36.0%増加によるものです。 2010年から2019年までの医療支出の年間平均成長率は4.2%でした。総医療費に占める最大の割合は連邦政府(36.3%)と家計(26.1%)によるものでした。医療支出に占める民間企業の割合は総医療支出の16.7%、州および地方政府は14.3%、その他の民間収入は6.5%を占めました。

さらに、2020年10月に国立医学図書館で発表された「腫瘍学人材による質の高いがんケアの確保:21世紀におけるケアの持続:ワークショップの概要」と題された研究によると、米国は100万人以上のがん患者の潜在的な不足に直面しています。そのため、国内のヘルスケア従事者の不足が深刻化しており、在宅医療ハブの導入が増加しています。したがって、前述のすべての要因により、予測期間中のセグメントの成長が促進されると予想されます。

ホームヘルスハブ業界の概要

競争力のある性格は、技術的な進歩と、より良い治療のための新しい機器の迅速な導入によって影響を受けます。さらに、重要な競合他社が今後数年間で世界の開発、戦略的提携、パートナーシップ、製品リリースにさらに注力するにつれて、それらの間の競合は激化するでしょう。主要なプレーヤーには、OnKol、INSUNG INFORMATION、IDEAL LIFE INC.、iHealth Labs Inc.、Honeywell International Inc.、Vivify Health, Inc.が含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 高齢者人口の増加とそれに伴う慢性疾患有病率の増加

- ヘルスケア費を削減する必要がある

- ヘルスケア専門家の不足

- 市場抑制要因

- セキュリティとプライバシーの問題

- 償還の問題

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 製品およびサービス別

- スマートフォンベースのハブ

- スタンドアロンハブ

- サービス

- 患者モニタリングタイプ別

- 緊急度の高い患者モニタリング

- 中等度の患者のモニタリング

- 緊急度の低い患者のモニタリング

- エンドユーザー別

- 病院

- 在宅介護機関

- ヘルスケア支払者

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Honeywell International,

- Lamprey Networks,

- iHealth Lab

- Capsule Technologies Inc.,

- Pfizer Inc.,

- Inhealthcare,

- Qualcomm Technologies, Inc.,

- Encompass Health Corporation,

- OceanWP,

- MyVitalz LLC,

- Koninklijke Philips NV,

- HiCare Pvt. Ltd,

- Health Hub Vienna,

- Technologies Inc.,

- Vivify Health, Inc.,

- OnKOI

第7章 市場機会と将来の動向

The Global Home Health Hub Market size is estimated at USD 0.95 billion in 2024, and is expected to reach USD 3.69 billion by 2029, growing at a CAGR of 31.30% during the forecast period (2024-2029).

Globally, the COVID-19 pandemic put enormous pressure on hospitals and healthcare systems that were understaffed and overworked. Home health hub technology helped patients to remain safe within their homes while reducing stress on hospitals, emergency rooms, and front-line healthcare workers during the pandemic, which shows a positive impact on the market. According to the study titled "COVID-19's impact on home health services, caregivers and patients: lessons from the French experience," published in the Lancet Regional Health in August 2021, Since the start of the Covid-19 pandemic, home-based care has been in high demand to relieve hospital overcrowding and allow patients with chronic diseases or non-severe Covid-19 to be cared for and monitored at home. Thus, the home health hub market was positively impacted by COVID-19.

The Home Health Hub Market is predicted to develop as the number of chronic diseases rises, and the geriatric population grows. Additionally, the expanding use of smartphones, as well as the growing desire to cut healthcare costs, are both driving the market forward. According to the July 2021 update by the World Health Organization, cardiovascular diseases are the leading cause of death around the world, including diseases like coronary heart disease, cerebrovascular disease, rheumatic heart disease, congenital heart disease, and others. As per the same source, in 2019, 17.9 million people around the world died from cardiovascular diseases, which amounted to about 32% of all global deaths. Additionally, The Globocan 2020 report published by Global Cancer Observatory estimated the incidence and mortality of 36 cancer in 185 countries. Globally, there were an estimated 19,292,789 new cases of cancer diagnosed in 2020, and about 9,958,133 people died due to cancer all over the world. Further, as per the same source, the number of new cancer cases is expected to reach 24,044,406 by 2030, which shows an increasing prevalence of cancer around the globe.

The geriatric population is expected to have a significant impact on the market studied as people aged above 65 are more prone to chronic diseases. According to the World Health Organization Facts of 2021, the proportion of the global population aged 60 and up will nearly double from 12% to 22% between 2015 and 2050. By 2050, 80% of the world's elderly will live in low- and middle-income countries. The population is aging at a much faster rate than in the past. Every country faces significant challenges in ensuring that its health and social systems are prepared to take advantage of this demographic shift.

However, various key strategic activities by the market players are anticipated to boost the market over the forecast period. For instance, in March 2022, VEON Ltd., a global provider of connectivity and internet services, announced that it is Banglalink mobile operator in Bangladesh had launched Health Hub, the country's first integrated digital health platform.

Thus, all aforementioned factors are expected to drive the market over the forecast period. However, security and privacy concerns and reimbursement issues are the factors that might restrict the growth of the market.

Home Health Hub Market Trends

Smartphone-based Segment is Expected to Dominate the Market Over the Forecast Period

The growing popularity of digital platform smartphones has fueled the growth of the Smartphone-Based Hubs sector, which now has the largest market share. Mobile programs (Android, iOS, Linux, and Windows) that can be downloaded to dedicated smartphones and tablets are required for smartphone-based hubs. Smartphones and tablets are becoming the primary means of internet connectivity in developed nations, and their use is increasing in developing countries.

Increased use of mobile platforms to improve patient information accessibility is being driven by increased smartphone usage and the continuous growth of high-speed mobile networks. Smartphone-enabled home health hubs are expected to rise in popularity as awareness and accessibility grow. A growing preference for smartphone technology and the internet and mounting demand for smartphone-based health hub is expected to boost the market growth. As per Eurostat data, by updates from December 2022, by 2021, the share of EU households with internet access had risen to 92%, some 20 percentage points higher than in 2011 (72%). Moreover, broadband internet access was used by 90% of the households in the EU in 2021, 25 percentage points higher than in 2011 (65%).

Furthermore, product launches by the key market players are anticipated to boost the market over the forecast period. For instance, in March 2022, the GRS India startup launched a new smartphone-based portable oxygen kit that can provide consistent oxygen supply during disasters and medical emergencies.

Thus, all aforementioned factors are expected to boost the market over the forecast period.

North America Dominates the Market and Expected to do Same in the Forecast Period.

Factors such as the high adoption of sophisticated technology, the prevalence of chronic and lifestyle diseases, rising healthcare spending, physician shortages, and increasing demand for better healthcare services are all contributing to North America's big share of the worldwide market. According to the Globocan 2020 report, an estimated 2,281,658 new cancer cases were diagnosed in the United States in 2020, with nearly 612,390 deaths. In 2020, The most common cancers were breast (253,465), lung (227,875), prostate (209,512), and colon (101,809) in the United States.

Additionally, the rise in healthcare expenditure and growth in disposable income also drive the market for home health hubs across the globe. According to the PETERSON-KFF Health System Tracker data published in February 2022, the United States health care spending increased 9.7% to reach USD 4.1 trillion in 2020, a much faster rate than the 4.3% increase seen in 2019. The acceleration in 2020 was due to a 36.0% increase in federal expenditures for health care that occurred largely in response to the COVID-19 pandemic. The average annual growth in health spending from 2010-2019 was 4.2%. The largest shares of total health spending were sponsored by the federal government (36.3%) and the households (26.1%). The private business share of health spending accounted for 16.7% of total health care spending, state and local governments accounted for 14.3%, and other private revenues accounted for 6.5%.

Furthermore, according to the study titled "Ensuring Quality Cancer Care through the Oncology Workforce: Sustaining Care in the 21st Century: Workshop Summary," published in the National Library of Medicine in October 2020, the United States faces a potential shortage of more than 1 million nurses by 2020. Thus increasing shortage of healthcare workforce in the country increases the adoption of home health hubs. Thus, all aforementioned factors are anticipated to boost the segment growth over the forecast period.

Home Health Hub Industry Overview

The competitive character is influenced by technical breakthroughs and the quick adoption of new devices for better treatment. Furthermore, as important competitors focus more on global development, strategic collaborations, partnerships, and product releases in the future years, competition amongst them will heat up. Major players include OnKol, INSUNG INFORMATION CO, LTD., IDEAL LIFE INC., iHealth Labs Inc., Honeywell International Inc., Vivify Health, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth In the Geriatric Population and The Subsequent Increase In The Prevalence Of Chronic Diseases

- 4.2.2 Need To Reduce Healthcare Costs

- 4.2.3 Shortage Of Healthcare Professionals

- 4.3 Market Restraints

- 4.3.1 Security and Privacy Concerns

- 4.3.2 Reimbursement Issues

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Product and Services

- 5.1.1 Smartphone-Based Hubs

- 5.1.2 Standalone Hubs

- 5.1.3 Services

- 5.2 By Type of Patients Monitoring

- 5.2.1 High-Acuity Patient Monitoring

- 5.2.2 Moderate-Acuity Patient Monitoring

- 5.2.3 Low-Acuity Patient Monitoring

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Home Care Agencies

- 5.3.3 Healthcare Payers

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Honeywell International,

- 6.1.2 Lamprey Networks,

- 6.1.3 iHealth Lab

- 6.1.4 Capsule Technologies Inc.,

- 6.1.5 Pfizer Inc.,

- 6.1.6 Inhealthcare,

- 6.1.7 Qualcomm Technologies, Inc.,

- 6.1.8 Encompass Health Corporation,

- 6.1.9 OceanWP,

- 6.1.10 MyVitalz LLC,

- 6.1.11 Koninklijke Philips N.V.,

- 6.1.12 HiCare Pvt. Ltd,

- 6.1.13 Health Hub Vienna,

- 6.1.14 Technologies Inc.,

- 6.1.15 Vivify Health, Inc.,

- 6.1.16 OnKOI