|

|

市場調査レポート

商品コード

1692145

電気自動車用高電圧DC-DCコンバータ:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Electric Vehicle High-Voltage DC-DC Converter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 電気自動車用高電圧DC-DCコンバータ:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

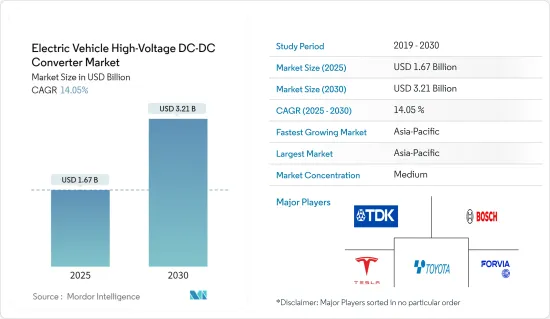

電気自動車用高電圧DC-DCコンバータの市場規模は、2025年に16億7,000万米ドルと推計され、予測期間(2025-2030年)のCAGRは14.05%で、2030年には32億1,000万米ドルに達すると予測されます。

長期的には、電気自動車へのシフトの増加、厳しい排ガス規制、電気自動車の販売を促進するための政府の取り組み、充電インフラの拡大、バッテリー技術やEVコンポーネントの進歩などの要因が市場の成長に寄与しています。例えば、

国際エネルギー機関(IEA)によると、2024年第1四半期の電気自動車販売台数は2023年第1四半期に比べて約25%増加し、電気自動車販売台数では中国が45%と最大のシェアを占め、次いで欧州(25%)が続いた。

世界の電気自動車販売の増加に伴い、最近の高電圧DC-DCコンバータ技術の進歩は、効率の向上、小型軽量化、信頼性の向上に重点を置いています。炭化ケイ素(SiC)や窒化ガリウム(GaN)半導体などの技術革新により、より高い周波数で動作する効率的なコンバータが開発され、受動部品の小型化が進んでいます。

このシナリオを考慮し、さまざまなメーカーが電気自動車とその部品(コンバーターなど)の技術向上に注力しています。

サムスン電機は2024年6月、DC-DCコンバータなどの電気自動車用途に合わせた高電圧積層セラミックコンデンサ(MLCC)「CL32B104KHU6PN#」を発表しました。CL32B104KHU6PN#は、小型化、高耐圧、安定性、高容量といった特長を持ち、自動車におけるMLCCの使用を促進しています。

クラウド・コンピューティングやIoT(モノのインターネット)のような技術が電気自動車のバッテリー管理システムに導入され、安定した出力電圧を保証するDC-DCコンバータと相まって、電気自動車でのコンバータの使用が増加しています。

電気自動車用高電圧DC-DCコンバータ市場では、インドや中国のような国がEV販売で最大のシェアを占めているため、アジア太平洋地域が突出したシェアを占めると推定されます。北米と欧州も、電気自動車の普及が進んでいることと、政府が将来的な排ガス目標の達成に力を入れるようになっていることから、急成長が見込まれています。

これらの要因は、予測期間中の市場成長にプラスの影響を与えると予想されます。

電気自動車用高電圧DC-DCコンバータ市場動向

乗用車が市場で最も高いシェアを占める

長期的には、運転体験の向上、快適性、安全性を提供する自動車に対する需要の高まりにより、低燃費エンジンの需要が増加する可能性があります。さまざまな国が厳しい規制、補助金、税額控除、その他の優遇措置を通じて電気自動車の普及を促進しているため、電気自動車の販売台数の増加が乗用車の販売をさらに押し上げています。

国際エネルギー機関(IEA)によると、欧州における電気自動車の新規登録台数は2023年に320万台近くに達し、2022年比で20%近く増加し、同年の電気自動車ストックの70%をバッテリー電気自動車が占める。

世界各国の政府も、従来型自動車よりも電気自動車を購入するよう奨励するため、さまざまな制度や政策を打ち出しています。電気自動車の購入を促進するそのような取り組みのひとつが、カリフォルニア州のゼロ・エミッション・ビークル(ZEV)プログラムで、2025年までに150万台の電気自動車を普及させることを目指しています。その他にも、インド、中国、英国、韓国、フランス、ドイツ、ノルウェー、オランダなどがさまざまな優遇措置を提供しています。

同様に、2025年12月31日までに欧州で登録された車両は10年間所有税が免除され、この免除は2030年12月31日まで有効です。こうした政策が電気乗用車の販売を後押ししています。

電気乗用車の販売台数の伸びを受けて、EV用コネクタを製造する企業は、EVセグメントにおける成長機会を見出しており、新製品を開発するためにさまざまな技術的進歩に注力しています。

2024年5月、イートンは低電圧48ボルトDC-DCコンバータの高出力バージョンを発売しました。新しく発売されたコンバーターは、48ボルトのシステムから電力を取り、アクセサリーや他の低電力システムを動かすために12ボルトに降圧します。

このような要因に加え、可処分所得の高さ、ブランド認知度の上昇、高電力の購買平準化が、このセグメントの成長に寄与しています。

アジア太平洋が市場を独占している

電気自動車用高電圧DC-DCコンバータ市場では、アジア太平洋地域が大半のシェアを占めています。中国のような国がEV販売をリードしているため、予測期間中に市場は大きく成長すると予想されます。

中国と日本は技術革新、テクノロジー、先進的な電気自動車の開発に傾倒しています。さらに、インドネシアなどは大規模な電動モビリティ・プロジェクトに取り組んでいます。

中国は、世界の電気自動車産業における主要企業です。同国政府は国民に電気自動車の導入を奨励しています。中国は2040年までにモビリティを完全に電気自動車に切り替える計画です。中国の電気乗用車市場も世界最大級であり、ここ数年で急成長しています。予測期間中にさらに成長することが予想され、電気自動車用高電圧DC-DCコンバータ市場にプラスの影響を与える可能性があります。同市場の主要企業数社は、他のプレーヤーと提携してパワーエレクトロニクス部品を開発しています。

自動車会社による多額の投資は、電気自動車の需要増に対応し、自動車の販売台数の増加に貢献すると予想されます。OEMは、MG Comet EVのようなハッチバックからTesla Model 3のような高級セダンまで、さまざまなセグメントで電気自動車を提供しています。

電気自動車への移行には多額の投資が必要で、自動車メーカーは製造拠点のアップグレードに注力しており、これは企業が電動化目標を達成する上で重要です。

インドの電気自動車市場は成長段階にあります。TATA、Mahindra、MGといったインドの自動車メーカーは、手頃な価格の電気自動車を提供するための取り組みを行っています。政府も、国内の温室効果ガスの排出を削減するため、電気モビリティを支援しています。

2024年3月、インド政府はEV政策を承認しました。この政策では、最低投資額5億米ドルで国内に製造ユニットを設立する企業に輸入関税の譲許が与えられます。

インドの自動車メーカーも、インドで手頃な価格の電気自動車を提供するための取り組みや研究開発への投資を行っています。例えば、現代自動車は2021年2月、手頃な価格の新型EVを開発するために1億2,000万米ドルを投資すると発表しました。車両は現地で製造される予定で、同社は部品を調達するために現地ベンダーと交渉中です。現代自動車はまた、インドでEVをポートフォリオに加える計画であるため、姉妹ブランドの起亜自動車との戦略的提携を模索する可能性もあります。起亜自動車は、2024年に発売を予定していたインド向けの大衆向け、より手頃な価格の電気自動車の開発に取り組んでいます。

このような要因から、自動車用DC-DCコンバータの需要は増加し、予測期間中の市場の成長を押し上げる可能性が高いです。

電気自動車用高電圧DC-DCコンバータ産業概要

電気自動車用高電圧DC-DCコンバータ市場は、世界および地域で確立されたプレーヤーによって統合され、主導されています。各社は市場での地位を維持するため、新製品の発売、提携、合併などの戦略を採用しています。

- 2024年6月、TDKはTDK-Lambdaブランドの300W定格i7C非絶縁型DC-DCコンバータシリーズに電流制限調整可能モデルを追加すると発表しました。新モデルは、医療、無人搬送車(AGV)、その他の産業において、12V、24V、48Vのシステム電圧からさらにハイパワーのDC出力を生成するのに適しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 電気自動車の普及拡大

- その他の促進要因

- 市場抑制要因

- コンバーターは動作時にノイズを発生するため、ターゲット市場の妨げになる可能性があります。

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 自動車タイプ

- 乗用車

- 商用車

- 推進タイプ

- プラグインハイブリッド車

- バッテリー電気自動車

- 燃料電池電気自動車

- 冷却方式

- 液冷式

- 空冷

- 入力電圧

- 200 V-450 V

- 450 V-800 V

- 800 V-1000 V

- 出力電圧

- 12 V-24 V

- 24 V-48 V

- 出力電力

- 2kW未満

- 2 kW以上

- 地域

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ノルウェー

- ポーランド

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他の国

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Continental AG

- Robert Bosch GmbH

- Valeo Group

- ABB Ltd

- DENSO Corporation

- Hella GmbH & Co. KGaA

- Toyota Industries Corporation

- Infineon Technologies AG

- Texas Instruments

- STMicroelectronics

- TDK-Lambda Corporation

- Shinry Technologies

- Delta Electronics

- Vicor Corporation

- Hyundai Mobis Ltd

第7章 市場機会と今後の動向

The Electric Vehicle High-Voltage DC-DC Converter Market size is estimated at USD 1.67 billion in 2025, and is expected to reach USD 3.21 billion by 2030, at a CAGR of 14.05% during the forecast period (2025-2030).

Over the long term, factors such as the increasing shift toward electric vehicles, stringent emission regulations, government initiatives to promote sales of electric vehicles, expansions in charging infrastructure, and advancements in battery technology and EV components contribute to the market's growth. For instance,

According to the International Energy Agency, in Q1 2024, electric car sales grew by around 25% compared to Q1 2023, with China holding the largest share of 45% in terms of electric car sales, followed by Europe (25%).

With the rise in EV sales worldwide, recent advancements in high-voltage DC-DC converter technology have focused on increasing efficiency, reducing size and weight, and enhancing reliability. Innovations such as silicon carbide (SiC) and gallium nitride (GaN) semiconductors are leading to more efficient converters that operate at higher frequencies, thus reducing the size of passive components.

Considering the scenario, various manufacturers are focusing on upgrading their technologies for electric vehicles and their components, such as converters.

In June 2024, Samsung Electro-Mechanics introduced the CL32B104KHU6PN#, a high-voltage multi-layer ceramic capacitor (MLCC) tailored for EV applications, such as DC-DC converters. The features include miniaturization, high voltage, stability, and higher capacitance, which are driving the usage of MLCCs in vehicles.

The deployment of technologies like cloud computing and IoT (Internet of Things) in battery management systems of electric cars, coupled with a DC-DC converter to ensure a regulated output voltage, have increased the use of converters in electric vehicles.

Asia-Pacific is estimated to hold a prominent share in the electric vehicle high voltage DC-DC converter market, as countries like India and China hold the largest share in EV sales. North America and Europe are also expected to grow rapidly due to the increasing adoption of electric vehicles and the government's increasing focus on achieving emission goals in the future.

These factors are expected to positively impact the market's growth during the forecast period.

Electric Vehicle High-Voltage DC-DC Converter Market Trends

Passenger Cars Hold the Highest Share in the Market

Over the long term, the growing demand for automobiles that provide enhanced driving experiences, comfort, and safety may increase the demand for fuel-efficient engines. The increasing sales of electric vehicles have further boosted the sales of passenger cars as various countries promote their adoption through strict regulations, subsidies, tax credits, and other incentives.

According to the International Energy Agency, new electric car registrations in Europe reached nearly 3.2 million in 2023, increasing by almost 20% compared to 2022, with battery electric cars accounting for 70% of the electric car stock in the same year.

Governments worldwide have also launched various schemes and policies to encourage buyers to opt for electric vehicles over conventional ones. One such initiative that promotes the purchase of electric vehicles is the California Zero Emission Vehicle (ZEV) program, which aims to have 1.5 million electric vehicles on the road by 2025. Other countries offering various incentives include India, China, the United Kingdom, South Korea, France, Germany, Norway, and the Netherlands.

Similarly, vehicles registered in Europe until December 31, 2025, are exempted from the ownership tax for 10 years, and this exemption is valid until December 31, 2030. Such policies are boosting the sales of electric passenger cars.

Owing to the growth of electric passenger car sales, companies manufacturing EV connectors are seeing a growing opportunity in the EV segment and are focusing on various technological advancements to develop new products.

In May 2024, Eaton launched the higher-power version of its low-voltage 48-volt DC-DC converter. The newly released converter takes power from a 48-volt system and steps it down to 12 volts to run accessories and other low-power systems.

Such factors, along with high disposable income, rising brand awareness, and high-power purchase parity, contribute to the segment's growth.

Asia-Pacific is Dominating the Market

Asia-Pacific holds the majority share in the electric vehicle high voltage DC-DC converter market. With countries like China leading the EV sales, the market is expected to grow significantly during the forecast period.

China and Japan are inclined toward innovation, technology, and the development of advanced electric vehicles. Moreover, countries such as Indonesia are engaged in large electric mobility projects.

China is a key player in the electric vehicle industry worldwide. The country's government is encouraging people to adopt electric vehicles. China plans to switch to electric mobility entirely by 2040. The Chinese electric passenger cars market is also one of the largest worldwide, and it has been growing rapidly over the last few years. It is expected to grow further during the forecast period, which may positively impact the electric vehicle high voltage DC-DC converter market. Several key players in the market are partnering with other players to develop power electronics components.

Heavy investments made by automotive companies are expected to cater to the growing demand for electric vehicles and contribute to the high sales of vehicles. OEMs offer electric vehicles in different segments, ranging from hatchbacks like the MG Comet EV to high-end sedans like Tesla Model 3.

The transition to electric vehicles requires significant investments as carmakers focus on upgrading manufacturing sites, which is important in companies fulfilling electrification targets.

The Indian electric vehicle market is in its growing stage. Automobile manufacturers in India, such as TATA, Mahindra, and MG, are taking initiatives to provide affordable electric driving options. The government is also supporting electric mobility to reduce the exhaust emissions of greenhouse gases in the country.

In March 2024, the Indian government approved an EV policy under which import duty concessions will be given to companies setting up manufacturing units in the country with a minimum investment of USD 500 million, a strategic move to attract major global players like US-based Tesla.

Automobile manufacturers in India are also taking initiatives and investing in R&D practices to provide affordable electric cars in India. For instance, in February 2021, Hyundai announced an investment of USD 0.12 billion to develop new affordable EVs. The vehicles would be manufactured locally, and the company is in talks with local vendors to source the components. Hyundai may also seek a strategic partnership with its sister brand, Kia, as it plans to add EVs to its portfolio in India. The company is working on a mass-market, more affordable electric car for India, which was planned to be launched in 2024.

Due to such factors, the demand for DC-DC converters in vehicles is likely to increase, thus boosting the market's growth over the forecast period.

Electric Vehicle High-Voltage DC-DC Converter Industry Overview

The electric vehicle high voltage DC-DC converter market is consolidated and led by global and regionally established players. The companies adopt strategies such as new product launches, collaborations, and mergers to sustain their market positions.

- In June 2024, TDK announced the addition of adjustable current limit models to the TDK-Lambda brand 300W-rated i7C non-isolated DC-DC converter series. The new models are suitable for generating additional high-power DC outputs from 12 V, 24 V, and 48 V system voltages in medical, automated guided vehicles (AGV), and other industries.

Some of the major players in the market include Robert Bosch GmbH, TDK Corporation, Toyota Industries Corporation, and HELLA GmbH & Co. KGaA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Rising Adoption of Electric Vehicles

- 4.1.2 Other Drivers

- 4.2 Market Restraints

- 4.2.1 Converters Generate Noise During Operation, Which May Hinder the Target Market

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD Million)

- 5.1 Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Commercial Vehicles

- 5.2 Propulsion Type

- 5.2.1 Plug-in Hybrid Vehicles

- 5.2.2 Battery Electric Vehicles

- 5.2.3 Fuel Cell Electric Vehicles

- 5.3 Cooling Method

- 5.3.1 Liquid Cooled

- 5.3.2 Air Cooled

- 5.4 Input Voltage

- 5.4.1 200 V - 450 V

- 5.4.2 450 V - 800 V

- 5.4.3 800 V - 1000 V

- 5.5 Output Voltage

- 5.5.1 12 V - 24 V

- 5.5.2 24 V - 48 V

- 5.6 Output Power

- 5.6.1 Less Than 2 kW

- 5.6.2 2 kW and Above

- 5.7 Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Norway

- 5.7.2.7 Poland

- 5.7.2.8 Russia

- 5.7.2.9 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 Rest of Asia-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Argentina

- 5.7.4.3 Chile

- 5.7.4.4 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 South Africa

- 5.7.5.4 Other Countries

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Continental AG

- 6.2.2 Robert Bosch GmbH

- 6.2.3 Valeo Group

- 6.2.4 ABB Ltd

- 6.2.5 DENSO Corporation

- 6.2.6 Hella GmbH & Co. KGaA

- 6.2.7 Toyota Industries Corporation

- 6.2.8 Infineon Technologies AG

- 6.2.9 Texas Instruments

- 6.2.10 STMicroelectronics

- 6.2.11 TDK-Lambda Corporation

- 6.2.12 Shinry Technologies

- 6.2.13 Delta Electronics

- 6.2.14 Vicor Corporation

- 6.2.15 Hyundai Mobis Ltd