|

市場調査レポート

商品コード

1440376

ウェアラブル心臓モニタリングデバイス:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Wearable Heart Monitoring Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ウェアラブル心臓モニタリングデバイス:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 111 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

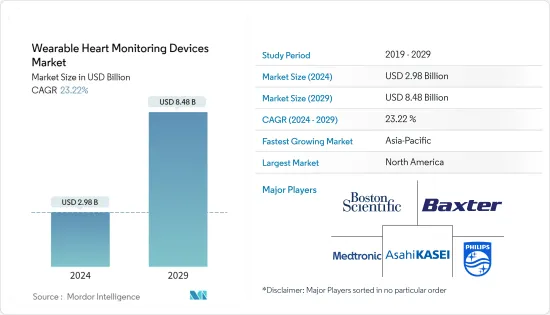

ウェアラブル心臓モニタリングデバイスの市場規模は、2024年に29億8,000万米ドルと推定され、2029年までに84億8,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に23.22%のCAGRで成長します。

COVID-19感染症のパンデミック中、コロナウイルスに感染した患者は心臓疾患を発症する可能性が高く、逆もまた同様で、リスクが増大しました。これは、心血管疾患のリアルタイムモニタリングによりCOVID-19感染症による死亡率が効果的に低下したため、ウェアラブル心臓モニタリングデバイスの需要が高まったことによるものです。たとえば、2021年 2月にJMIR出版物に掲載された記事によると、ウェアラブルデバイスは従来の診断方法よりも早く新型COVID-19を特定でき、病気の管理を追跡および改善するのに役立ちます。鼻腔 PCRによるCOVID-19の同定前に、心拍数変動(HRV)の有意な変化が見られ、これは、鼻腔 PCRがCOVID-19感染症を診断する予測能力があることを示唆しています。しかし、一部の患者では、COVID-19感染症の影響後も心臓の問題が長く続いた。たとえば、2022年2月にNatureジャーナルに掲載された論文によると、COVID-19症から回復した人々は、感染後1年間で心血管系の問題が顕著に増加したことが示されています。したがって、心臓病患者の間でウェアラブル技術に対する意識は常に高まっており、ウェアラブル心臓モニタリングデバイス市場は近い将来急速に拡大すると予想されます。

市場の成長を促進する特定の要因には、心不全率の増加、ウェアラブルベースの心臓モニタリングに対する意識の高まり、ウェアラブルデバイスの技術進歩などが含まれます。 2022年10月に発表されたCDCの最新情報では、冠状動脈性心疾患は最も一般的なタイプの心疾患であり、20歳以上の成人約2,010万人(約7.2%)が冠状動脈疾患を患っていると述べられています。したがって、冠動脈疾患の高い負担が市場の成長を推進しています。さらに、「2022 Spotlight on Heart Failure」レポートによると、毎年10万人以上のカナダ人が心不全と診断されています。同じ情報源によると、心不全によるカナダの損失は年間28億米ドルを超える可能性があります。したがって、心不全の増加とヘルスケア費の増加により、コストを削減し心臓モニタリングを改善するウェアラブル技術に基づく心臓モニタリング装置が求められています。

さらに、2021年 1月、ボストンサイエンティフィックはPreventice Solutionsを9億2,500万米ドルで買収しました。 Preventice Solutionsは、遠隔患者モニタリングに使用されるいくつかのウェアラブル心臓センサー(BodyGuardian)のメーカーです。これらの装置は成人患者だけでなく小児患者向けにも開発されています。したがって、この買収により、ボストンサイエンティフィックは中核となる心調律管理と電気生理学の事業部門を拡大し、この魅力的な市場での地位を強化しました。

さらに、リズムメディックスは2021年2月に、「RhythmStar」という名前の最新世代のウェアラブル心電図モニターを発売しました。このデバイスには携帯電話接続が組み込まれており、それ自体でECG記録を収集し、電話を使用せずに医師にデータをワイヤレスで送信できます。この簡素化され時間の節約されたアプローチにより、より多くの顧客を魅了し、市場の可能性を高めることができます。したがって、ウェアラブルデバイスにおける先進技術の採用の増加は、患者と医師がより良い方法で心臓の問題を管理するのに役立つ利点を含み、それによって市場の成長に貢献します。

したがって、心臓合併症の増加と心臓監視ウェアラブル製品の発売の増加により、ウェアラブル心臓監視デバイス市場は予測期間中に成長すると予想されます。ただし、ウェアラブルデバイスのプライバシーとセキュリティの問題、厳格な規則と規制政策は、ウェアラブル心臓モニタリングデバイス市場の成長を妨げる主要な要因です。

ウェアラブル心臓モニタリングデバイスの市場動向

光学技術ベースの製品は、予測期間中にウェアラブル心臓モニタリングデバイス市場で顕著な成長率を示すと予測されています。

光学技術ベースの製品セグメントは、心血管疾患(CVD)の有病率の上昇、高齢者人口の増加、製品承認の増加などの要因により、予測期間中に大幅な成長率を記録すると予想されます。ベースの製品は、フォトプレチスモグラフィー(PPG)と呼ばれる方法に基づいています。皮膚に光を当て、血流によって散乱される光の量を測定することで心拍数を測定します。最近では、心拍数を継続的にモニタリングするために、光学技術をベースにしたウェアラブルデバイスが広く関心を集めています。機能が単純であるため、消費者に直接入手でき、医療スタッフとの直接接触が減り、電気パルスベースの製品と比較して安価です。

さらに、英国政府の健康改善・格差局によると、2020~21年のNHSバーキングとダゲナムCCGにおける慢性心疾患による入院率は、人口10万人当たり427.9人(入院数580人)だった。これはイングランドの割合(10万人あたり368人)よりも大幅に高かったです。したがって、心血管合併症の増加により心臓モニタリングの需要が増加し、それによって予測期間中のセグメントの成長が促進されます。ほとんどのCVDは心拍数をリアルタイムでモニタリングすることで抑制でき、これは死亡率と治療費の削減に重要な役割を果たします。たとえば、2021年 11月に米国心臓協会(AHA)が発表したデータによると、ECGパッチモニターで確認されたとおり、Fitbit PPG検出は98%の確率で心房細動(AF)イベントを特定しました。したがって、PPGアルゴリズムの効率の向上により、今後数年間で光学技術ベースの製品の需要が増加し、それによって市場の成長に貢献すると予想されます。

さらに、多くの市場プレーヤーが戦略的取り組みの実行に焦点を当てており、それによってウェアラブル心臓モニタリングデバイス市場の成長に貢献しています。たとえば、2022年 4月に、Google所有のFitbitは、AFを識別するための「AFib」という新しい光電脈波計(PPG)アルゴリズムの製品承認をFDAから受け取りました。このアルゴリズムは、Fitbitデバイス上の新しい不規則な心拍リズム通知機能を強化する可能性があります。したがって、ウェアラブル心臓モニタリングデバイス用の光学技術ベースの製品の主要企業が提供する進歩により、この市場セグメントは予測期間中に大幅な成長を遂げると予想されます。

したがって、心臓病の増加と光学技術ベースの心臓モニタリングウェアラブル製品の発売の急増により、市場の調査対象セグメントは予測期間中に成長すると予想されます。

北米は予測期間中に市場でかなりのシェアを握る可能性が高い

北米はウェアラブル心臓モニタリングデバイス市場で大きなシェアを握ると考えられます。これは、CVDの発生率の増加、主要な市場プレーヤーの存在とその戦略的取り組みなどの要因によるものです。たとえば、CARES 2021年次報告書によると、米国では男性の62.5%が院外心停止(OHCA)を起こしたと報告されています。同じ情報源によると、2021年に米国で成人の97.6%と子供の2.4%がOHCAを経験しました。したがって、心臓合併症の数が増加するにつれて、ウェアラブル心臓モニタリングデバイスの需要が高まり、予測期間中の市場の成長を推進します。

政府の取り組みとウェアラブル心臓モニタリング装置市場の成長により、大手企業はこの業界に焦点を移し、戦略的取り組みの実施に取り組んでいます。たとえば、医療診断および消費者向けヘルスケア技術会社であるBiotricity Inc.は、2022年 3月に、FDAの認可を受けたワイヤレスウェアラブル心臓モニタリングデバイス Biotresを発売しました。同製品は2022年2月下旬から医師、診療所、病院、個人向けに提供を開始しました。

さらに、2022年 8月に、Samsung Canadaは、デジタルヘルスの次の時代を推進するSamsung独自のBioActive Sensorテクノロジーを搭載したGalaxy Watch5およびGalaxy Watch5 Proを発売しました。 Samsung BioActiveセンサー(光学心拍数+ 電気心臓信号+ 生体電気インピーダンス分析)、温度センサー、加速度計、気圧計、ジャイロセンサー、地磁気センサー、光センサーが付属しています。

したがって、心臓病の増加と心臓モニタリングウェアラブル製品の発売の急増により、北米は予測期間中に大幅な成長を遂げると予想されます。

ウェアラブル心臓モニタリングデバイス業界の概要

ウェアラブル心臓モニタリングデバイス市場は非常に細分化されており、いくつかの主要企業で構成されています。市場シェアの点では、現在、いくつかの大手企業が市場を独占しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 心不全の増加率

- ウェアラブルベースの心臓モニタリングに対する意識の高まり

- ウェアラブルデバイスの技術進歩

- 市場抑制要因

- ウェアラブルデバイスのプライバシーとセキュリティの問題

- 厳格な規則と規制方針

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 製品別

- 電気パルスベースの製品

- 光学技術ベースの製品

- デバイスの種類別

- 診断および監視デバイス

- 治療機器

- 用途別

- スポーツ&フィットネス

- 遠隔患者モニタリング

- 在宅ヘルスケア

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Medtronic plc

- Koninklijke Philips NV(BioTelemetry, Inc.)

- Boston Scientific(Preventice Solutions, Inc.)

- Asahi Kasei Corporation(ZOLL Medical Corporation)

- Baxter

- iRhythm Technologies, Inc.

- ACS Diagnostics, Inc.

- General Electric Company(GE Healthcare, Inc.)

- Hemodynamics Company LLC

- Heartbit Holdings Plc.

- Qardio, Inc.

- Vital Connect, Inc.

第7章 市場機会と将来の動向

The Wearable Heart Monitoring Devices Market size is estimated at USD 2.98 billion in 2024, and is expected to reach USD 8.48 billion by 2029, growing at a CAGR of 23.22% during the forecast period (2024-2029).

During the COVID-19 pandemic, coronavirus-infected patients were more likely to develop heart problems and vice-versa, which increased the risk. This was attributed to the rising demand for wearable heart monitoring devices, as the real-time monitoring of cardiovascular disease effectively reduced COVID-19 mortality rates. For instance, as per the article published in February 2021 in JMIR publications, wearable devices can identify COVID-19 cases earlier than traditional diagnostic methods and can help track and improve the management of the disease. Significant changes in heart rate variability (HRV) were seen before the identification of COVID-19 by nasal PCR, suggesting its predictive capacity to diagnose COVID-19 infection. However, for some patients, heart problems persisted long after the impact of COVID-19 infection. For instance, as per the article published in February 2022 in Nature journal, people who had recovered from COVID-19 showed stark increases in cardiovascular problems over the year after infection. Therefore, the awareness of wearable technology among cardiac patients is constantly rising, and the wearable heart monitoring devices market will see rapid expansion in the near future.

Certain factors that are driving the market growth include the increasing rate of heart failure, rising awareness of wearables-based cardiac monitoring, and technological advancements in wearable devices. The CDC update published in October 2022 stated that coronary heart disease is the most common type of heart disease, and around 20.1 million adults aged 20 and older have coronary artery disease (approximately 7.2%). Thus, the high burden of coronary artery disease is driving the growth of the market. Further, as per the 2022 Spotlight on Heart Failure report, more than 100,000 Canadians are diagnosed with heart failure each year. As per the same source, Heart failure is likely to cost Canada more than USD 2.8 billion a year. Therefore, the rising cases of heart failure and increasing healthcare cost demands heart monitoring devices based on wearable technology to reduce the cost and improves heart monitoring.

In addition, in January 2021, Boston Scientific acquired Preventice Solutions for USD 925 million. Preventice Solutions is a manufacturer of several wearable cardiac sensors (BodyGuardian) used for remote patient monitoring. These devices are developed for adult as well as pediatric patients. Therefore, from this acquisition, Boston Scientific expanded its business segment of core cardiac rhythm management and electrophysiology which in turn strengthened its position in this attractive market.

Moreover, in February 2021, RhythMedix launched the newest-generation wearable ECG monitor named 'RhythmStar'. This device has built-in cellular connectivity which can collect ECG recordings by itself and send data wirelessly to physicians without the use of a phone. This simplified and time-saving approach may entice more customers and raise their market potential. Thus, the rise in the adoption of advanced technology in wearable devices comprises benefits that help patients and physicians to manage heart problems in a better way, thereby contributing to market growth.

Thus, due to the rise in cardiac complications, and the increase in heart-monitoring wearable product launches, the wearable heart-monitoring devices market is anticipated to witness growth over the forecast period. However, privacy & security issues of wearable devices and stringent rules and regulatory policies are major factors hindering the wearable heart monitoring devices market's growth.

Wearable Heart Monitoring Devices Market Trends

The Optical Technology-based Product is Projected to Have a Notable Growth Rate in the Wearable Heart Monitoring Devices Market Over the Forecast Period

The optical technology-based product segment is anticipated to register a significant growth rate during the forecast period owing to the factors such as the rise in the prevalence of cardiovascular diseases (CVDs), the growing geriatric population, and the rising product approvals This optical technology-based product is based on a method called photoplethysmography (PPG). It measures heart rate by shining light into the skin and measuring the amount of light that is scattered by blood flow. These days, wearable devices based on optical technology are gaining wide interest for continuous monitoring of the heart rate. Attributable to its uncomplicated features, available direct-to-consumer, reduce direct contact with clinical staff, and is inexpensive as compared to electric pulse-based products.

Further, according to the Government of the UK, Office of Health Improvement & Disparities, in 2020-21 the admission rate for chronic heart disease in NHS Barking and Dagenham CCG was 427.9 for every 100,000 people in the population (580 admissions). This was significantly higher than the England rate (368 per 100,000). Thus, the rise in cardiovascular complications increases the demand for heart monitoring thereby driving the segment growth over the forecast period. Most CVDs can be inhibited by real-time monitoring of heart rate, which plays a vital role in reducing the mortality and cost of treatment. For instance, data published by American Heart Association (AHA) in November 2021 found that the Fitbit PPG detections identified atrial fibrillation (AF) events 98% of the time, as confirmed by ECG patch monitors. Thus, the rising efficiency of the PPG algorithm is expected to increase the demand for optical technology-based products in the coming years, thereby contributing to market growth.

In addition, numerous market players are focused on the execution of strategic initiatives, thereby contributing to the growth of the wearable heart monitoring devices market. For instance, in April 2022, Google-owned Fitbit received product approval from the FDA for a new photoplethysmography (PPG) algorithm named 'AFib' to identify AF. This algorithm is likely to power a new irregular heart rhythm notification feature on the Fitbit device. Therefore, due to the advancements offered by the key players in optical technology-based products for wearable heart monitoring devices, this market segment is expected to witness significant growth during the forecast period.

Hence, due to the increase in cardiac diseases, and the surge in optical technology-based cardiac monitoring wearable product launches, the studied segment in the market is anticipated to witness growth over the forecast period.

North America is Likely to Hold a Significant Share in the Market Over the Forecast Period

North America is likely to hold a significant share of the wearable heart monitoring devices market. This is due to factors such as the rising incidences of CVDs and the presence of major market players and their strategic initiatives. For instance, as per the CARES 2021 annual report, 62.5% of males were reported with out-of-hospital cardiac arrest (OHCA) in the United States. As per the same source, 97.6% of adults and 2.4% of children experienced OHCA in 2021 in the United States. Thus, as the number of cardiac complications increases, the demand for wearable heart monitoring devices rises and drives the market growth over the forecast period.

Due to government initiatives and the growing nature of the wearable heart monitoring device market, the major players have shifted their focus in this industry and engaged in the implementation of strategic initiatives. For instance, in March 2022, Biotricity Inc., a medical diagnostic and consumer healthcare technology company, launched its FDA-cleared, wireless wearable cardiac monitoring device, Biotres. The product was available for physicians, medical offices, hospitals, and individual use since late-February 2022.

Furthermore, in August 2022, Samsung Canada launched the Galaxy Watch5 and Galaxy Watch5 Pro equipped with a unique BioActive Sensor technology from Samsung that drives the next era of digital health. It comes with Samsung BioActive Sensor (Optical Heart Rate + Electrical Heart Signal + Bioelectrical Impedance Analysis), Temperature Sensor, Accelerometer, Barometer, Gyro Sensor, Geomagnetic Sensor, and Light Sensor.

Hence, due to the increase in cardiac diseases, and the surge in cardiac monitoring wearable product launches, North America is anticipated to witness significant growth over the forecast period.

Wearable Heart Monitoring Devices Industry Overview

The wearable heart monitoring devices market is highly fragmented and consists of several major players. In terms of market share, a few of the major players are currently dominating the market. Some of the companies which are currently dominating the market are Medtronic plc, iRhythm Technologies, Inc., Baxter, Vital Connect, Inc., Asahi Kasei Corporation (ZOLL Medical Corporation), Koninklijke Philips N.V. (BioTelemetry, Inc.), Hemodynamics Company LLC, ACS Diagnostics, Inc., General Electric Company (GE Healthcare, Inc.), Boston Scientific (Preventice Solutions, Inc.), Qardio, Inc., Heartbit Holdings Plc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Defination

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Rate of Heart Failure

- 4.2.2 Rising Awareness of Wearables-based Cardiac Monitoring

- 4.2.3 Technological advancements in Wearable Devices

- 4.3 Market Restraints

- 4.3.1 Privacy and Security Issue of Wearable Devices

- 4.3.2 Stringent Rules & Regulatory Policy

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Product

- 5.1.1 Electric Pulse-based Product

- 5.1.2 Optical Technology-based Product

- 5.2 By Device Type

- 5.2.1 Diagnostic & Monitoring Devices

- 5.2.2 Therapeutic Devices

- 5.3 By Application

- 5.3.1 Sports & Fitness

- 5.3.2 Remote Patient Monitoring

- 5.3.3 Home Healthcare

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Medtronic plc

- 6.1.2 Koninklijke Philips N.V. (BioTelemetry, Inc.)

- 6.1.3 Boston Scientific (Preventice Solutions, Inc.)

- 6.1.4 Asahi Kasei Corporation (ZOLL Medical Corporation)

- 6.1.5 Baxter

- 6.1.6 iRhythm Technologies, Inc.

- 6.1.7 ACS Diagnostics, Inc.

- 6.1.8 General Electric Company (GE Healthcare, Inc.)

- 6.1.9 Hemodynamics Company LLC

- 6.1.10 Heartbit Holdings Plc.

- 6.1.11 Qardio, Inc.

- 6.1.12 Vital Connect, Inc.