|

市場調査レポート

商品コード

1689775

小児用医薬品:世界の市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Global Pediatric Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 小児用医薬品:世界の市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 119 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

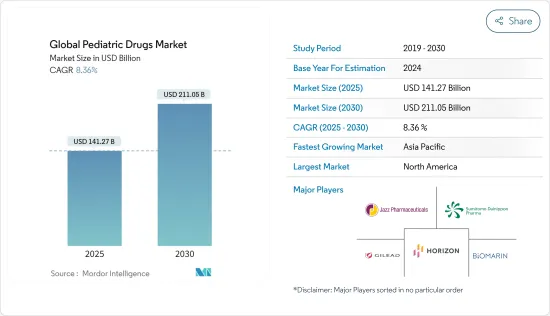

世界の小児用医薬品市場規模は、2025年に1,412億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは8.36%で、2030年には2,110億5,000万米ドルに達すると予測されます。

COVID-19パンデミックは世界の小児用医薬品市場に影響を与えました。ビジネスの世界では、COVID-19パンデミックはかつてない経済的不確実性をもたらしました。一部の企業は被爆量が少ないため比較的影響を受けずに済んでいるが、他の多くの企業はパンデミックの影響を回避できず、財政難に見舞われています。COVID-19の大流行と、その後の感染拡大を抑えるための公衆衛生指導は、子どもたちの健康と福祉に広範な影響を及ぼしています。小児科救急部門(ED)は、パンデミックに対応するため、ケアの提供を急速に適応させてきました。

小児用医薬品市場の成長をもたらしている主な要因は、以前に比べて出生率が上昇していることと、小児の致死的症例が増加していることであり、様々な疾患、ウイルス感染症、消化器疾患、肺がん、栄養不良が原因で死亡することさえあります。国連国際児童緊急基金(ユニセフ)の2020年報告によると、2020年までに5歳未満の子ども500万人が死亡すると予想されています。2020年には、毎日13,800人の5歳未満児が死亡することになります。肺炎、下痢、マラリアなどの感染症、早産や分娩内合併症は、依然として世界の5歳未満児の主な死因となっています。したがって、5歳未満の子どもの死亡は、効率的な治療を必要としています。免疫不全や免疫低下による造血幹細胞移植(HSCT)後の腎機能障害や肺機能障害の有病率の上昇が、世界の小児用医薬品市場の成長をもたらしています。

小児用医薬品市場の動向

小児用医薬品市場では、呼吸器疾患治療薬の適応症別セグメントが大きな市場シェアを占める見通し

免疫力の低下、公害の増加、さまざまなアレルゲンへの曝露により、慢性閉塞性肺疾患(COPD)などの慢性呼吸器疾患が引き起こされるため、呼吸器疾患治療薬セグメントが小児用医薬品市場で最大のシェアを占めると予想されます。COPDは世界の小児ヘルスケア負担の主な原因であり、疾患の効率的な治療に対する需要の増加につながり、ひいては市場の活性化につながっています。世界保健機関2021によると、慢性閉塞性肺疾患(COPD)は世界第3位の死因であり、2019年には323万人の死亡を引き起こしました。したがって、小児のCOPD有病率の増加は、予測期間中の市場成長を押し上げると予想されます。

一方、希少自己免疫疾患治療薬セグメントは、予測期間中に最も速いCAGRを記録し、市場を独占すると予測されます。同分野の優位性は、様々ながん、遺伝性疾患、その他の自己免疫疾患患者間の一致率の上昇に起因するこれらの疾患の有病率の上昇に起因すると考えられ、希少疾患治療薬の開発を支援・奨励するインセンティブを提供しています。例えば、2019年5月、ヤコブス製薬は、ルズルギ(アミファンプリジン)錠剤について、米国食品医薬品局(FDA)から優先審査およびファストトラック指定による承認を取得しました。ルズルギはまた、小児におけるランバート・イートン筋無力症候群(LEMS)の治療薬として希少疾病用医薬品の指定も受けています。これらの処方薬は高コストであることも急成長の要因となっており、予測期間中の世界の小児用医薬品市場を牽引しています。

北米が市場を独占、予測期間中も同様と予測

様々な自己免疫疾患、呼吸器疾患、脳性麻痺、筋萎縮症などを患う小児患者の増加に加え、米国における先端技術の採用が急増していることから、北米が小児用医薬品市場を独占すると予想され、北米市場の主要な収益シェアを占めています。

例えば、Luyu Xieが2020年にJAMA Networkに発表した論文によると、喘息は世界で最も一般的な小児の慢性疾患のひとつです。米国では、600万人の子ども(人口の約8%)が喘息と診断されており、年間医療費は819億米ドルに上り、小児用医薬品の需要が高いです。

この地域の主要企業が小児患者向けに新製品を発売していること、小児用医薬品に対する人々の意識を高めるための政府の取り組みが増加していること、希少疾患治療薬の開発を奨励し、小児医療負担の増加を軽減するために米国食品医薬品局(USFDA)が医薬品承認加速化イニシアチブを導入して早期承認を行っていることなどが、市場にさらなる機会を生み出すと考えられます。例えば、2020年には、抗ウイルス薬であるVeklury(remdesivir)が米国食品医薬品局から成人および12歳以上の小児への使用が認可されました。

また、可処分所得の増加やヘルスケアインフラの改善も、予測期間における世界の小児ヘルスケア市場の成長を後押しするとみられます。

小児用医薬品業界の概要

小児用医薬品市場の競争は中程度で、複数の大手企業が参入しています。現在、数社の大手企業が市場シェアで市場を独占しています。市場の満たされていない課題に対処するために新製品を発売している有力企業もあれば、製品を流通させている企業もあります。例えば、2019年4月、GSKは米国食品医薬品局(FDA)から、わずか5歳からの全身性エリテマトーデス(SLE)の小児の頭蓋欠損に対する米国初の医薬品として承認された静注用(IV)Benlysta(belimumab)の承認を取得しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 糖尿病、呼吸器疾患など小児疾患の負担増と可処分所得の増加

- 研究開発活動の活発化と一般市民の小児医療に対する意識の高まり

- 市場抑制要因

- 研究対象集団の小規模化と小児科研究における倫理的問題

- 死に至る可能性のある重篤な合併症のリスク

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 医薬品タイプ

- 呼吸器疾患薬

- 自己免疫疾患薬

- 胃腸薬

- 循環器系薬

- その他の医薬品

- 投与経路

- 経口

- 局所

- 非経口

- その他の投与経路

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- PTC Therapeutics Inc.

- BioMarin Pharmaceutical Inc.

- Horizon Therapeutics PLC

- Sumitomo Dainippon Pharma Co. Ltd

- Gilead Sciences Inc.

- Jazz Pharmaceuticals Inc.

- Pfizer Inc.

- Glaxosmithkline PLC

- Johnson & Johnson

- Boehringer Ingelheim International GmbH

- Sanofi SA

- Novartis AG

第7章 市場機会と今後の動向

The Global Pediatric Drugs Market size is estimated at USD 141.27 billion in 2025, and is expected to reach USD 211.05 billion by 2030, at a CAGR of 8.36% during the forecast period (2025-2030).

The COVID-19 pandemic impacted the global pediatric drug market. In the business world, the COVID-19 pandemic has created unprecedented economic uncertainty. While some businesses are relatively insulated due to low exposure, many others have been unable to avoid the pandemic's effects and are experiencing financial hardship. The COVID-19 pandemic and subsequent public health guidance to reduce the spread of the disease have wide-reaching implications for children's health and wellbeing. Pediatric emergency departments (EDs) have rapidly adapted the provision of care in response to the pandemic.

The major factors attributing to the growth of the pediatric drugs market are a rise in the birth rate compared to previous years and the increased volume of fatal pediatric cases, which are leading to even deaths due to various diseases, viral infections, GI disorders, lung cancers, and malnutrition. According to the United Nations International Children's Emergency Fund (UNICEF) 2020 Report, 5.0 million children under five were expected to die by 2020. In 2020, this translated to 13,800 children under five dying each day. Infectious diseases such as pneumonia, diarrhea, and malaria, and preterm birth and intrapartum complications continue to be the leading causes of death among children under the age of five worldwide. Hence, deaths among children under age five demand efficient treatment. The rise in prevalence of renal or pulmonary dysfunctions following hematopoietic stem-cell transplantations (HSCT) due to defective or low immunity results in the growth of the global pediatric drugs market.

Pediatric Drugs Market Trends

Respiratory Disorder Drugs Segment By Indication is Expected to Hold the Major Market Share in the Pediatric Drugs Market

The respiratory disorder drugs segment is expected to account for the largest share of the pediatric drugs market due to lower immunity, increased pollution, and exposure to various allergens, resulting in chronic respiratory disorders such as Chronic obstructive pulmonary disease (COPD). COPD is a major cause of the global pediatric healthcare burden, leading to an increased demand for the efficient treatment of the diseases, in turn fueling the market. According to the World Health Organization 2021, Chronic Obstructive Pulmonary Disease (COPD) was the third leading cause of death worldwide, causing 3.23 million deaths in 2019. Thus, the increasing prevalence of COPD among children is expected to boost the market growth over the forecast period.

On the other hand, the rare autoimmune disorders drugs segment is anticipated to witness the fastest CAGR and dominate the market during the forecast period. The segment's dominance can be attributed to the increased prevalence of these disorders due to rising coincidences among the patients with various cancers, genetic disorders, and other autoimmune disorders, which provides incentives to assist and encourage the development of drugs for rare diseases. For instance, in May 2019, the Jacobus pharmaceutical company received approval from the US Food and Drug Administration (FDA) under Priority Review and Fast Track designations for its RUZURGI (amifampridine) tablets. Ruzurgi also received orphan drug designation for the treatment of Lambert-Eaton myasthenic syndrome (LEMS) in pediatric patients. These prescription drugs' high cost may also attribute to the fastest growth, propelling the global pediatric drugs market during the forecast period.

North America Dominates the Market and Expected to do Same in the Forecast Period.

North America is expected to dominate the pediatric drugs market due to the rise in the volume of pediatric patient cases with kids suffering from various autoimmune disorders, respiratory disorders, cerebral palsy, and muscular atrophy, along with a steep rise in the adoption of advanced technologies in the US, which holds the major revenue share of the market in North America.

For instance, according to the article published in the JAMA Network in 2020 by Luyu Xie, asthma was one of the world's most common chronic diseases in children. In the United States, 6 million children (roughly 8% of the population) have been diagnosed with asthma, costing USD 81.9 billion in annual health care costs and resulting in high demand for pediatric drugs.

The launch of new products by key players in the region for pediatric patients, rise in government initiatives to create awareness in people for pediatric medicines, and early approvals with accelerated drug approval initiative by the USFDA to encourage the development of drugs for rare diseases and to decrease the rising pediatric burden are likely to create more opportunities in the market. For instance, in 2020, Veklury (remdesivir), an antiviral medication, was licensed by the US Food and Drug Administration for use in adults and children aged 12 and above.

Also, the rise in disposable income and improvements in healthcare infrastructure are likely to help the global pediatric healthcare market's growth over the forecast period.

Pediatric Drugs Industry Overview

The pediatric drugs market is moderately competitive and consists of several major players. A few major players are currently dominating the market in terms of market share. Some prominent players are launching new products to address the unmet challenges in the market, while others are distributing the products. For instance, in April 2019, GSK received approval from the US Food and Drug Administration (FDA) for its intravenous (IV) Benlysta (belimumab), the first medicine approved in the US for children with systemic lupus erythematosus (SLE) from as young as five years of age cranial defects. Some companies currently dominating the market include BioMarin Pharmaceutical Inc., Horizon Therapeutics PLC, Sumitomo Dainippon Pharma Co. Ltd, Gilead Sciences Inc., and Jazz Pharmaceuticals Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market defination

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Burden of Pediatric Diseases such as Diabetes, Respiratory Disorders, and Rise in Affordability with Disposable Income

- 4.2.2 Increased R&D Activities and Awareness of Pediatric Medicine Among Public

- 4.3 Market Restraints

- 4.3.1 Small Size of Study Population and Ethical Issues in Pediatric Research

- 4.3.2 Risk of Severe Complications Associated with Medicines that may lead to Death

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 Drug Type

- 5.1.1 Respiratory Disorder Drugs

- 5.1.2 Autoimmune Disorder Drugs

- 5.1.3 Gastrointestinal Drugs

- 5.1.4 Cardiovascular Drugs

- 5.1.5 Other Drug Types

- 5.2 Route of Administration

- 5.2.1 Oral

- 5.2.2 Topical

- 5.2.3 Parenteral

- 5.2.4 Other Routes of Administration

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle-East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle-East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 PTC Therapeutics Inc.

- 6.1.2 BioMarin Pharmaceutical Inc.

- 6.1.3 Horizon Therapeutics PLC

- 6.1.4 Sumitomo Dainippon Pharma Co. Ltd

- 6.1.5 Gilead Sciences Inc.

- 6.1.6 Jazz Pharmaceuticals Inc.

- 6.1.7 Pfizer Inc.

- 6.1.8 Glaxosmithkline PLC

- 6.1.9 Johnson & Johnson

- 6.1.10 Boehringer Ingelheim International GmbH

- 6.1.11 Sanofi SA

- 6.1.12 Novartis AG