|

市場調査レポート

商品コード

1687982

スパッタリング装置カソード:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Sputtering Equipment Cathode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| スパッタリング装置カソード:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

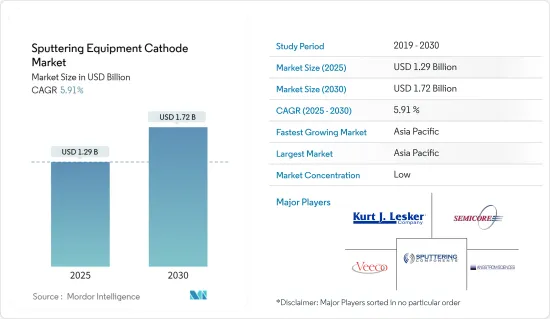

スパッタリング装置カソード市場規模は、2025年に12億9,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは5.91%で、2030年には17億2,000万米ドルに達すると予測されています。

急成長する半導体産業での部品コーティングにおけるスパッタリングの用途拡大が、予測期間中にこの種の装置の需要を押し上げる主要因の1つになると見られています。

主要ハイライト

- 航空宇宙やエレクトロニクスなど様々なエンドユーザー産業における人工知能の出現は、半導体需要を増加させ、市場の成長を促進すると予想されます。さらに、ゲームにおける仮想現実の実装に半導体が使用されるケースが増加していることも、市場成長をさらに促進すると予想されます。

- 企業が次世代製造方法の活用に向かうにつれ、マグネトロンスパッタリング技術などのプロセスは、半導体の効率と品質を高めるために半導体製造企業によってますます採用されるようになっています。

- マグネトロンスパッタリング技術には、高い成膜速度、高純度膜、極めて高い膜密着性、段差や小さな特徴の優れた被覆性、熱に敏感な基板へのコーティング能力、自動化の容易さ、大面積基板での高い均一性、あらゆる金属、合金、化合物へのスパッタリングの容易さなどの利点があります。このような利点から、半導体のスパッタリングにマグネトロンスパッタリング技術の利用が増加しています。

- 技術の進歩や、半導体製造における新しい代替技術の研究開発への投資の増加は、性能の向上、生産速度の向上など多くの利点をもたらし、物理蒸着(PVD)法の使用を減少させています。これは調査した市場に影響を与えます。

- 世界中でCOVID-19パンデミックが発生し、2020年の初期段階において市場におけるサプライチェーンと製品の生産が大きく混乱しました。労働力不足のため、各地域の包装工場や検査工場の多くが操業を縮小、あるいは停止しました。これはまた、そうしたバックエンドの包装や検査能力に依存している企業にとってボトルネックとなりました。

- さらに、新しい製造プロセスを開発するための研究開発への継続的な投資など、大手企業による取り組みが増加したことで、プロセスの生産量がさらに高まると予想されます。

スパッタリング装置カソード市場動向

半導体用途の増加が市場を牽引する展望

- 半導体の需要は、民生用電子機器、産業用工具・機器、自動車製品、ネットワーキング、通信製品などの需要の増加が牽引しています。その他多数。これらの産業は、ワイヤレス技術(5G)、人工知能、自動化などの技術の変遷に触発されています。

- モノのインターネット(IoT)機器の増加傾向は、半導体産業に生産能力強化のための設備投資を強いるものと予想されます。

- 例えば、SEMI(Semiconductor Equipment and Materials International)の最近の予測によると、半導体用途のシリコンウエハー出荷量は2019年の118億1,000平方インチ(MSI)から2025年には176億MSIを超えると予想されています。

- 自動車産業では、1台当たりの半導体製品数が増加し、自律走行車や電気自動車などの動向が半導体製造の需要を高めています。

- モノのインターネットの用途の増加は、半導体需要を押し上げると予想されます。さらに、無線通信セグメントは、5Gネットワークの成長とともに成長すると予想されます。第5世代ネットワークはまた、世界的に半導体のアプリケーションを促進するために、消費者が携帯電話/デバイスをアップグレードする可能性を示しています。

- 世界中の様々なデバイスで半導体の生産が増加しており、市場は予測期間中にプラス成長を示すことになります。

アジア太平洋が最も高い市場シェアを占める見込み

- 主に中国、韓国、インド、台湾などの国々で半導体生産が増加していることから、アジア太平洋はスパッタリング装置の最大市場になると予想されます。さらに、太陽電池や医療機器産業からのPVDコーティング需要の増加も、予測期間中の市場成長をプラスに押し上げると予想されます。

- 世界の製造拠点である中国は、予測期間中にエレクトロニクスや自動車など様々な製品の生産増加が見込まれ、市場の牽引役となることが期待されます。また、自動車産業はスパッタリング装置を使用した様々なコーティング部品で構成されています。また、電気自動車/ハイブリッド車の生産台数の増加が市場に影響を与えると予想されます。

- 日本は、重要なICチップセットメーカーやエレクトロニクス産業の本拠地であるため、半導体産業において重要な地位を占めています。WSTSによると、2021年の日本の半導体産業の売上高は436億9,000万米ドルで、2022年には479億3,000万米ドルに達し、今後も安定的に成長すると予想されています。

- さらに、中国や日本のような国のロボット産業における技術革新は、半導体コーティングの需要を押し上げると予測されています。半導体チップの需要増は、ロボット産業からの需要増によって支えられると予想されます。

- インドの半導体エコシステムは強固で、世界の大手半導体メーカーのほとんどがインドに研究開発センターを置いています。しかし、政府の支援施策もあり、半導体製造施設はあまり発展していないです。調査された市場には大きな機会があります。

- インド電子半導体協会は、同地域の半導体部品市場は2025年までに323億5,000万米ドル規模になると予想され、CAGRは10.1%(2018~2025年)であると述べています。これは、同国のエレクトロニクスセグメントにおける潜在的な活動が高いことを示しており、調査対象市場にとっていくつかの機会につながります。

- 2021年1月、通商産業エネルギー省は、2020年の韓国のICT輸出額は3.8%増の1,836億米ドル、輸入額は3.9%増の1,126億米ドルに達したと発表しました。また、2020年の半導体輸出は1,002億5,000万米ドルになると発表しました。2020年上半期は1.5%減少したが、下半期は約12.3%増加しました。特にシステムオンチップの輸出は17.8%増の303億米ドルと過去最高を記録しました。メモリーチップの輸出は1.5%増の639億米ドルとなりました。

スパッタリング装置カソード産業概要

スパッタリング装置カソード市場は、国内外市場に装置を供給する様々な大手企業が存在するため、競争が激しくなっています。現在、市場を独占している参入企業は少数であるため、市場は統合されているように見えます。市場の主要企業は、製品革新やパートナーシップのような戦略を採用し、リーチを拡大し、競争をリードしています。同市場の主要企業には、Semicore Equipment, Inc.、Sputtering Components, Inc.、Angstrom Sciences Inc.、Veeco Instruments, Inc.などがあります。

- 2022年1月-Kurt J. Lesker Company(KJLC)は、資産売買契約によりKDF Electronics & Vacuum Services(KDF Technologies)の全資産を実質的に買収したと発表しました。2022年初頭より、KDF Electronics & Vacuum ServicesはKDF Technologiesとして知られるようになります。KDFはKJLCから独立して事業を継続するが、一部の共有サービスは活用します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- 半導体の用途拡大

- マグネトロンスパッタリング技術などの技術の進歩

- 市場抑制要因

- 熱蒸着などの代替技術の台頭

第6章 市場セグメンテーション

- 製品別

- 線形

- 円形

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- その他のアジア太平洋

- その他

- ラテンアメリカ

- 中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Kurt J. Lesker Company

- Veeco Instruments, Inc.

- Semicore Equipment Inc.

- Impact Coatings AB

- AJA International Inc.

- Soleras Advanced Coatings

- Sputtering Components, Inc.

- KDF Technologies

- Angstrom Sciences, Inc.

- Angstrom Engineering Inc.

第8章 投資分析

第9章 市場機会と今後の動向

The Sputtering Equipment Cathode Market size is estimated at USD 1.29 billion in 2025, and is expected to reach USD 1.72 billion by 2030, at a CAGR of 5.91% during the forecast period (2025-2030).

The increasing applications of sputtering in the coating of components in the rapidly growing semiconductor industry is expected to be one of the primary factors that will drive the demand for these types of equipment over the forecast period.

Key Highlights

- The emergence of Artificial Intelligence across various end-user industries, such as aerospace and electronics, is expected to increase the demand for semiconductors, which will drive the market's growth. Moreover, the increasing use of semiconductors for implementing virtual reality in gaming is further expected to drive market growth.

- As companies move toward leveraging next-generation manufacturing methods, the processes such as magnetron sputtering technology are increasingly adopted by semiconductor manufacturing companies for enhanced efficiency and quality of semiconductors.

- Magnetron sputtering technology offers advantages such as high deposition rates, high purity films, extremely high adhesion of films, excellent coverage of steps and small features, ability to coat heat-sensitive substrates, ease of automation, high uniformity on large-area substrates, ease of sputtering any metal, alloy, or compound, and many more. These advantages lead to increased use of magnetron sputtering technology in the sputtering of semiconductors.

- The advancement in technology and increased investment in the research and development of new and alternate techniques in the manufacturing of semiconductors provide advantages such as enhanced performance, increased production rate, and many more, reducing the use of physical vapor deposition (PVD) methods. This impacts the market studied.

- The outbreak of the COVID-19 pandemic across the world significantly disrupted the supply chain and production of products in the market during the initial phase of 2020. Due to labor shortages, many of the package and testing plants in the various region reduced or even suspended operations. This also created a bottleneck for companies that depend on such back-end packages and testing capacity.

- Furthermore, the increased number of initiatives taken by major players, such as continuous investments in R&D to develop new manufacturing processes, is further expected to enhance the volume output of the process.

Sputtering Equipment Cathode Market Trends

Rise in the Application of Semiconductors is Expected to Drive the Market

- The demand for semiconductors is being driven by the increase in demand for consumer electronics, industrial tools & equipment, automotive products, networking, and communication products. And many more. These industries have been inspired by technology transitions such as wireless technologies (5G), Artificial intelligence, automation, etc.

- The trend of increasing numbers of Internet of Things (IoT) devices is expected to force the semiconductor industry to invest in this equipment for enhanced production capabilities.

- For instance, according to the recent forecasts of Semiconductor Equipment and Materials International (SEMI), silicon wafer shipments for semiconductor applications are expected to exceed 17,600 million square inches (MSI) by 2025 from 11,810 MSI in 2019.

- In the automotive industry increasing number of semiconductor products per vehicle and trends like autonomous and electric vehicles are increasing the demand for semiconductor manufacturing.

- The increase in applications of the Internet of Things is expected to boost the demand for semiconductors. Moreover, the wireless communications sector is expected to grow with the growth in 5G networks. Fifth-generation networks also indicate the likelihood of consumers upgrading their handsets/devices to drive applications of semiconductors globally.

- With the increasing production of semiconductors in various devices worldwide, the market will witness positive growth over the forecast period.

Asia-Pacific is Expected to Occupy Highest Market Share

- The Asia-Pacific region is expected to be the largest market for sputtering equipment, primarily owing to the increased semiconductor production in countries like China, South Korea, India, and Taiwan. Moreover, the increasing demand for PVD coatings from solar photovoltaic cells and the medical equipment industry is also expected to positively push the market growth during the forecast period.

- China, a global manufacturing hub, is expected to witness an increase in the production of various products such as electronics and automotive, among others, over the forecast period, which is expected to drive the market. Also, the automotive industry comprises various coated components using sputtering equipment. Also, the growth in the production of electric/hybrid vehicles is expected to impact the market.

- Japan holds a significant position in the semiconductor industry as it is home to some of the important IC chipset manufacturers and the electronics industry. According to WSTS, the semiconductor industry revenue in Japan for 2021 stood at USD 43.69 billion, and it is expected to reach USD 47.93 billion in 2022 and grow steadily in the future.

- Furthermore, technological innovations in the robotics industry in countries like China and Japan are projected to boost the demand for semiconductor coatings. The increasing demand for semiconductor chips is expected to be supported by the increased demand from the robotics industry.

- The Indian semiconductor ecosystem is robust, with most major global semiconductor players having their R&D centers in India. However, with supportive government policies, semiconductor manufacturing facilities are not significantly developed in the country. There are massive opportunities for the studied market.

- The India Electronics and Semiconductor Association stated that the semiconductor component market in the region is expected to be worth USD 32.35 billion by 2025 while witnessing a CAGR of 10.1% (2018 -2025). This indicates high potential activity in the country's electronics sector, leading to several opportunities for the market studied.

- In January 2021, the Ministry of Trade, Industry, and Energy announced that South Korea's ICT exports and imports increased by 3.8% and 3.9% to USD 183.6 billion and USD 112.6 billion, respectively, in 2020. The government also reported that in 2020, the country's semiconductor exports totaled USD 100.25 billion. The exports decreased by 1.5% in the first half of 2020; however, they increased by around 12.3% in the second half. Especially, system-on-chip exports increased by 17.8% to an all-time high of USD 30.3 billion. Memory chip exports increased by 1.5% to USD 63.9 billion.

Sputtering Equipment Cathode Industry Overview

The Sputtering Equipment Cathode Market is highly competitive owing to the presence of various large players supplying equipment in domestic and international markets. The market appears to be consolidated as few of the players currently dominate the market. Major players in the market are adopting strategies like product innovation and partnerships to expand their reach and stay ahead of the competition. Some of the major players in the market are Semicore Equipment, Inc., Sputtering Components, Inc., Angstrom Sciences Inc., and Veeco Instruments, Inc., among others.

- January 2022 - Kurt J. Lesker Company (KJLC) has announced that it has substantially acquired all of the KDF Electronics & Vacuum Services (KDF Technologies) assets through an asset purchase agreement. From the beginning of 2022, KDF Electronics & Vacuum Services will become known as KDF Technologies. KDF will continue to operate independently of KJLC while leveraging some shared services.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assesment of Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise in the Applications of Semiconductors

- 5.1.2 Advancement in Technology Such as Magnetron Sputtering Technology

- 5.2 Market Restraints

- 5.2.1 Rise of Alternative Technologies Such as Thermal Evaporation

6 MARKET SEGMENTATION

- 6.1 By Product

- 6.1.1 Linear

- 6.1.2 Circular

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 Germany

- 6.2.2.2 United Kingdom

- 6.2.2.3 France

- 6.2.2.4 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 China

- 6.2.3.2 Japan

- 6.2.3.3 India

- 6.2.3.4 Rest of Asia-Pacific

- 6.2.4 Rest of the World

- 6.2.4.1 Latin America

- 6.2.4.2 Middle-East and Africa

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Kurt J. Lesker Company

- 7.1.2 Veeco Instruments, Inc.

- 7.1.3 Semicore Equipment Inc.

- 7.1.4 Impact Coatings AB

- 7.1.5 AJA International Inc.

- 7.1.6 Soleras Advanced Coatings

- 7.1.7 Sputtering Components, Inc.

- 7.1.8 KDF Technologies

- 7.1.9 Angstrom Sciences, Inc.

- 7.1.10 Angstrom Engineering Inc.