|

市場調査レポート

商品コード

1687981

データセンタースイッチ:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Data Center Switch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| データセンタースイッチ:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 165 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

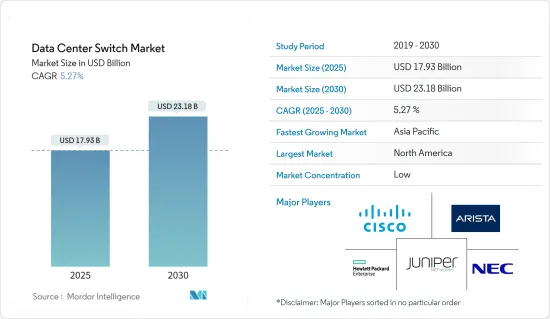

データセンタースイッチ市場規模は2025年に179億3,000万米ドルと推計され、2030年には231億8,000万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは5.27%です。

クラウドコンピューティング、データローカライゼーション、5GやIoTなどの新技術の採用により、世界のデータセンター投資は増加しています。データセンターが急速に普及している背景には、あらゆる規模の企業のニーズの変化、何百万台ものリンクされたデバイスの継続的な創出、インターネット経由で日々生成される大量のデータがあります。

主なハイライト

- AI技術の潜在能力を十分に引き出すには、さらなるコンピューター処理と意思決定プロセスが必要です。性能、容量、コストなどの側面に応じて、AI処理とデータ保存の場所は、クラウドからオンプレミスのデータセンター、ネットワークの周辺部まで、さまざまな可能性があります。コネクテッドデバイス、革新的産業、コネクテッドカーから多大な恩恵を受けると予測されるエッジコンピューティングは、検討中の市場に大きな影響を与えると思われます。

- コアスイッチは、トラフィック管理の拡大により新たな成長の可能性を秘めています。COVID-19の大流行で人々が自宅待機を余儀なくされたとき、多くの人が外食や映画ではなく、NetflixのようなOTTサービスに娯楽を求めました。COVID-19の最初の3ヶ月で、ネットフリックス・アジア太平洋は360万人の新規加入者を増やしました。ネットフリックスは、ストリーミングサービスの品質を維持しながら大量の受信トラフィックを処理するため、帯域幅の高いストリームを削除し、トラフィックをtorで削減することを決定しました。

- COVID-19の発生により、データセンター建設のサプライチェーンが混乱しました。ロックダウンに関連したプロジェクト完了の遅れや、ホスピタリティやエンターテイメントなど、特に被害の大きかった業界からの収益の減少が、建設活動やデータセンターの立地に影響を与えました。

- クラウドベースのビジネス・プロセスの急速な導入により、企業はこれらのシステムから生成される大量のデータを処理するためのデータ管理ソリューションに多大な投資を行ってきました。マルチクラウド・コンピューティングの成長により、仮想ネットワークベースのサーバーが従来のオンプレミスの物理サーバーに取って代わりつつあり、これがデータセンターの世界の拡大を促し、データセンターのスイッチング機器に対する需要を高めています。

- しかし、データセンターにとって最も大きな出費のひとつは、やはり電力です。国際エネルギー機関(IEA)によると、データセンターは世界の全電力の1%を消費しています。今後5年間で、その消費量はさらに増えると思われます。このエネルギー消費の大半は、サーバーを稼動させるために必要なもので、暖房と冷房が発生します。ここでも、冷却プロセスに多くのエネルギーが使われています。

データセンタースイッチ市場の動向

最大の市場シェアを占めるコアスイッチ

- コアスイッチは、他の2つのスイッチよりも優先されなければならないです。アマゾンやマイクロソフトのような市場シェアの大きい企業は、データセンターの増設を進めています。データセンターが拡大しているため、コアスイッチの必要性は飛躍的に高まると思われます。

- 増大するトラフィックを効率的かつ確実に処理し、レイテンシーを低く予測できなければならないです。しかし、vPC(仮想ポート・チャネル)は2つのアクティブな並列アップリンクしか供給できないため、3層データセンター・アーキテクチャでは帯域幅が制約となります。3層設計のもう1つの問題は、使用するトラフィック経路によってサーバー間のレイテンシが変化することです。インスタンスでは、シスコがこれらの制約に対処するため、クロス・ネットワークベースのスパイン&リーフ・アーキテクチャとして知られる新しいデータセンター設計を導入しました。この設計は、高帯域幅、低レイテンシ、ノンブロッキングのサーバー間接続を提供することが実証されています。

- Croreスイッチは、さまざまなデータセンターの要件を満たす包括的なデバイスの選択肢を提供します。Croreのスイッチは、トップ・オブ・ラック(ToR)、スパイン、およびリーフ・アーキテクチャ向けに、効果的でスケーラブルなネットワーク・インフラを構築することができます。さらに、SANやハイパフォーマンス・コンピューティング(HPC)用クラスタなど、特定の使用事例に特化した制御も提供しています。

- 北米では、クラウド・コンピューティング技術の利用が広まりつつあります。例えば、フェイスブック社のメタ・プラットフォームズ社は昨年、米国アイダホ州の大規模キャンパスに8億米ドルを投じ、データセンターの市場シェアを拡大する計画を発表しました。

- データセンター機能の拡大により、多くのIT機器の複雑さと相互接続性が改善されることが予想され、スイッチやルーターなどのデータセンター・ネットワーキング・コンポーネントの需要は、ハイパースケールインフラの重要な一部となると思われます。ハイパースケールITインフラプロバイダーによる迅速なデータ転送のための高性能コアスイッチの使用は、データセンタースイッチ市場の成長を促進すると思われます。

北米が著しい成長を遂げる見込み

- 不動産の専門家であるCBREによると、米国の上位7市場におけるデータセンター・リースは、過去数年に比べて31%増加し、パンデミックの影響で若干減少した昨年と比べても50%増加しました。バージニア州北部は、全米の新規データセンター容量の60%以上を占める主要市場でした。

- コロケーション・データセンターの需要の大半は、クラウド・サービス・プロバイダーとソーシャルメディア企業が占めています。また、ブロックチェーン技術、5Gインフラ、バーチャルリアリティコミュニティ、自律走行車技術などの新技術の採用も市場を牽引しています。

- 企業向けプロバイダーの新規プロジェクトにより、アトランタは最近、データセンター開拓のもうひとつの重要な市場となっています。アトランタに110万平方フィートのデータセンターを開発するため、QTSデータセンターは一昨年、提案書を提出しました。Project Granite」に掲載された設計図によると、QTSは約36エーカーの土地に、データセンタースペースと商業、小売、住宅用地を含む230万平方フィートの複合施設を建設する予定です。このような進歩により、これらの地域ではデータセンターのスイッチング機器の必要性が高まっています。

- ハイパーコンバージェンスは、ストレージ、プロセッシング、ネットワークを1つのシステムに統合することで、データセンターの複雑さを軽減し、拡張性を向上させる。ハイパーコンバージド・インフラストラクチャ・プラットフォームの利用増加が、データセンター市場を牽引しています。

- Patrinely Groupとその資金調達パートナーであるUSAA Real Estateは昨年、新しいデータセンター開発プラットフォームであるCorscaleをバージニア北部市場に導入しました。同社の最初のプロジェクトはゲインズビル・クロッシングで、プリンス・ウィリアム郡にある300メガワットの複合施設で、超大規模顧客向けに設計された5つのデータセンターがあります。

- 近年、この地域では200GbEと400GbEのスイッチポートも広く採用されています。例えば、ヒューレット・パッカード・エンタープライズ(HPE)は、昨年と今年、最新のデータセンター向けに特別に設計された32ポートの200GbE SN3700Mスイッチを発表しました。このスイッチは、画期的な8.33Bppsのパケット処理速度と、50G PAM-4ベースのSpectrum-2 ASICを搭載した場合に最大12.8Tb/秒の双方向スイッチング能力を備えています。

データセンタースイッチ業界の概要

データセンタースイッチ市場は競争が激しく、複数の大手企業が存在します。しかし、現在、市場シェアで市場を独占しているのは少数の大手企業です。これらの企業は、事業拡大、M&A、ジョイントベンチャー、提携、パートナーシップなど、いくつかの戦略に従っており、これらの市場プレーヤーは事業における地位を強化しています。本レポートで取り上げている主な市場プレイヤーは、Cisco、Jupiter Networks、Dell EMC、Arista Networks、ZTE、Hewlett Packard Enterprise、Mellanox、Huawei、Extreme Networksなどです。

- 2023年9月- ハイパースケーラはデータセンタースイッチにCiscoではなくAristaを選択。Aristaはクラウドサービスプロバイダーに注力しており、売上高の半分以上を占める。近年はエンタープライズ市場にも足を踏み入れ、「事業の多角化」を図っています。

- 2023年4月- 次世代のデータセンター・ネットワーク・アーキテクチャを提供するため、Edgecoreは超大容量400Gスイッチを発表。次世代のデータセンターとクラウド・コンピューティング環境の要求を満たし、基本的なネットワーク・アーキテクチャに新たなレベルをもたらすために、エッジコアは超大容量400GスイッチであるDCS520の発売を発表しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

- 技術スナップショット

- 帯域幅

- 技術(イーサネット、ファイバーチャネル、インフィニバンド)

第5章 市場力学

- 市場促進要因

- クラウド&エッジコンピューティングサービスの需要拡大

- データセンターの現地化に関する政府規制

- 市場抑制要因

- 高いデータセンター運用コスト

第6章 市場セグメンテーション

- スイッチタイプ

- コアスイッチ

- ディストリビューションスイッチ

- アクセススイッチ

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 世界のその他の地域

- 北米

第7章 競合情勢

- 企業プロファイル

- Cisco Systems, Inc.

- Arista Networks, Inc.

- Juniper Networks, Inc.

- Hewlett Packard Enterprise Development LP

- NEC Corporation

- Huawei Technologies Co., Ltd.

- H3C Holding Limited

- Lenovo Group Limited

- Extreme Networks Inc.

- Dell EMC

- Mellanox Technologies.

- Fortinet, Inc.

- ZTE Corporation

- Quanta Cloud Technology(QCT)

- D-Link Corporation

- Silicom Ltd. Connectivity Solutions

第8章 投資分析

第9章 今後の市場展望

The Data Center Switch Market size is estimated at USD 17.93 billion in 2025, and is expected to reach USD 23.18 billion by 2030, at a CAGR of 5.27% during the forecast period (2025-2030).

Global data center investments are rising because of adopting cloud computing, data localization, and emerging technologies like 5G and IoT. Data centers are fast gaining popularity because of the shifting needs of businesses of all sizes, the ongoing creation of millions of linked devices, and the daily volume of data generated via the Internet.

Key Highlights

- Additional computer processing and decision-making processes are needed to exploit AI technology's potential fully. Depending on aspects like performance, capacity, and cost, the location of AI processing and data storage may range from the cloud to on-premises data centers to the network's periphery. Edge computing, projected to tremendously benefit from connected devices, innovative industries, and connected cars, would significantly impact the market under examination.

- Core switches are experiencing new growth potential because of expanding traffic management. When the COVID-19 outbreak forced people to stay home, many turned to OTT services like Netflix for entertainment instead of going out to eat or to the movies. In the first three months of COVID-19, Netflix Asia-Pacific added 3.6 million new subscribers. Netflix decided to delete the highest bandwidth streams and cut traffic by tor to handle the high volume of incoming traffic while retaining the streaming service's quality.

- The COVID-19 outbreak messed up the supply chain for building the data center. Lockdown-related delays in project completion and a decline in revenue from particularly hard-hit industries, like hospitality and entertainment, impacted construction activity and data center entry locations.

- Due to the rapid adoption of cloud-based business processes, businesses have made significant investments in data management solutions to handle the massive volume of data produced by these systems. Virtual network-based servers are replacing conventional on-premises physical servers due to the growth of multi-cloud computing, which drives the global expansion of data centers and increases the demand for data center switching equipment.

- However, one of the most significant expenses for data centers is still electricity. According to the International Energy Agency, data centers consume 1% of all electricity worldwide. They will use it in the next five years. Most of this energy consumption is required to run the servers, which generate heating and cooling. Again, a lot of energy is used in the cooling process.

Data Center Switch Market Trends

Core Switches Holding the Largest Market Share

- Core switches must be given more priority than the other two switches. Companies with larger market shares, such as Amazon and Microsoft, are building additional data centers. The need for core switches will rise dramatically since data centers are expanding.

- The growing traffic must be handled effectively and reliably, with low and predictable latency. However, because vPC (virtual-port-channel) can only supply two active parallel uplinks, bandwidth becomes a constraint in a three-tier data center architecture. Another issue with a three-tier design is that server-to-server latency changes depending on the traffic path used. For Instance, Cisco introduced a new data center design known as the Clos network-based spine-and-leaf architecture to address these restrictions. This design has been demonstrated to provide a high-bandwidth, low-latency, nonblocking server-to-server connection.

- Crore Switches offer a comprehensive selection of devices to satisfy different data center requirements. Switches from their range allow clients to create effective and scalable network infrastructures for top-of-rack (ToR), spine, and leaf architectures. Additionally, offer specialized controls for particular use cases, including SANs or clusters for high-performance computing (HPC).

- In North America, cloud computing technology is becoming more widely used. For instance, Facebook Inc.'s Meta Platforms Inc. announced plans to increase its data center market share by investing USD 800 million in large-scale campuses in Idaho, United States, last year.

- The complexity and interconnectedness of many IT devices are expected to be improved by expanding data center capabilities, and the demand for data center networking components like switches and routers will be a crucial part of hyper-scale infrastructures. The use of high-performance core switches for quick data transfer by hyper-scale IT infrastructure providers will drive the growth of the data center switch market.

North America Expected to Register Significant Growth

- According to real estate expert CBRE, data center leasing in the top seven US markets was 31% greater than in the previous several years and 50% higher than the last year, which had slightly decreased owing to the pandemic. Northern Virginia was the leading market, with over 60% of the country's new data center capacity.

- Cloud service providers and social media firms account for most of the demand for colocation data centers. The market is also driven by adopting new technologies, including blockchain technology, 5G infrastructure, virtual reality communities, and autonomous car technology.

- With new projects from providers aiming at the enterprise sector, Atlanta has recently become another important market for data center development. To develop a 1.1 million square foot data center in Atlanta, QTS Data Centers submitted proposals the year before the current year. According to the designs in "Project Granite," QTS would create 2.3 million square feet of mixed-use space on around 36 acres of land, including data center space and commercial, retail, and residential land uses. These advances increase the need for data center switching devices in these areas.

- By fusing storage, processing, and networking into a single system, hyper-convergence reduces the complexity of data centers and improves scalability, which has begun to gain the attention of businesses in the North American region. An increase in the usage of a hyper-converged infrastructure platform is driving the market for data centers.

- The Patrinely Group and its financing partner, USAA Real Estate, introduced Corscale, a new data center development platform, to the Northern Virginia market last year. The company's first project is Gainesville Crossing, a 300-megawatt complex in Prince William County with five data centers designed for hyper-scale clients.

- In recent years, the region has also widely adopted the 200GbE and 400GbE switch ports. Hewlett Packard Enterprise (HPE), for instance, in the previous and current year, introduced the 32-port 200GbE SN3700M switch, which is designed specifically for the modern data center. The switch has a groundbreaking 8.33Bpps packet processing rate and a bidirectional switching capacity of up to 12.8Tb/s when powered by the 50G PAM-4-based Spectrum-2 ASIC.

Data Center Switch Industry Overview

The Data Centre Switch market is highly competitive and has several major players. However, few significant companies currently dominate the market regarding market share. The companies follow several strategies, including expansions, mergers & acquisitions, joint ventures, collaborations, partnerships, and others; these market players have strengthened their position in the business. The major market players interpreted in the report include Cisco, Jupiter Networks, Dell EMC, Arista Networks, ZTE, Hewlett Packard Enterprise, Mellanox, Huawei, Extreme Networks, etc.

- September 2023 - Hyperscalers have chosen Arista over Cisco for data center switches. Arista focuses on cloud service providers, representing over half of the vendor's revenue. In recent years, the networking company has also attempted to "diversify its business" by dipping its feet into the enterprise market.

- April 2023 - Edgecore launched the Ultra High-Capacity 400G Switch to provide the next-generation data center network architectures. To satisfy the demands of the next-generation data center and cloud computing environments and to bring a new level of basic network architecture, Edgecore announced the launch of the DCS520, an ultra-high capacity 400G switch.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Market

- 4.4 Technology Snapshot

- 4.4.1 Bandwidth

- 4.4.2 Technology (Ethernet, Fiber Channel, and InfiniBand)

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Augmented Demand for Cloud & Edge Computing Services

- 5.1.2 Government Regulations Regarding Localization of Data Centers

- 5.2 Market Restraints

- 5.2.1 High Data Center Operational Cost

6 MARKET SEGMENTATION

- 6.1 Switch Type

- 6.1.1 Core Switches

- 6.1.2 Distribution Switches

- 6.1.3 Access Switches

- 6.2 Geography

- 6.2.1 North America

- 6.2.1.1 Unites States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Germany

- 6.2.2.3 France

- 6.2.2.4 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 China

- 6.2.3.2 Japan

- 6.2.3.3 India

- 6.2.3.4 South Korea

- 6.2.3.5 Rest of Asia-Pacific

- 6.2.4 Rest of the World

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Cisco Systems, Inc.

- 7.1.2 Arista Networks, Inc.

- 7.1.3 Juniper Networks, Inc.

- 7.1.4 Hewlett Packard Enterprise Development LP

- 7.1.5 NEC Corporation

- 7.1.6 Huawei Technologies Co., Ltd.

- 7.1.7 H3C Holding Limited

- 7.1.8 Lenovo Group Limited

- 7.1.9 Extreme Networks Inc.

- 7.1.10 Dell EMC

- 7.1.11 Mellanox Technologies.

- 7.1.12 Fortinet, Inc.

- 7.1.13 ZTE Corporation

- 7.1.14 Quanta Cloud Technology (QCT)

- 7.1.15 D-Link Corporation

- 7.1.16 Silicom Ltd. Connectivity Solutions