|

市場調査レポート

商品コード

1437595

航空機用タービンエンジン:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Aircraft Turbine Engine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空機用タービンエンジン:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

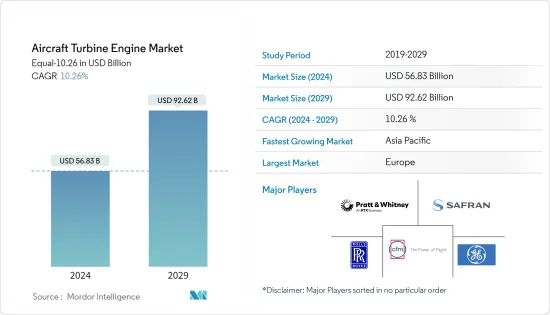

航空機用タービンエンジンの市場規模は、2024年に568億3,000万米ドルと推定され、2029年までに926億2,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に10.26%のCAGRで成長します。

航空機エンジンの需要は、主に航空機(ビジネスジェット、商用機、または軍用機)の注文件数の増加、または既存の航空機のエンジンの代替によって促進されます。航空機OEMとエンジンメーカーは、航空機の性能を向上させ、航続距離を延長するために広範な統合の取り組みに取り組んでいます。このような技術の研究開発への投資は、予測期間中に市場の見通しを強化すると予想されます。

現在の航空会社は統合収益モデルに基づいて運営されているため、利益率は比較的低くなります。このシナリオでは、通信事業者が新しいフリートを調達し、取引を完了するために多額の現金を支払うことが困難になります。しかし、航空機およびエンジンのリース事業の新たな動向により、航空会社は航空機金融機関からのリース契約を選択するという安心感を得ることができ、航空会社に財政的救済を提供し、供給能力の増加に対する一時的なアクセスを許可しています。

航空機エンジンの重要なコンポーネントを構築するために3Dプリンティングとセラミックマトリックス複合材料の使用が増加しているため、航空機エンジンOEMの製造サイクルは急速に変化すると予想されます。さらに、ハイブリッド電気ジェットエンジンなどの新興技術は、市場参加者にとって現在のビジネスチャンスを高めると予想されます。

航空機用タービンエンジン市場動向

商業セグメントが予測期間中に市場シェアを支配する

商業セグメントは、いくつかの魅力的な要因により、航空機用タービンエンジン市場で最大の市場シェアを保持しています。所得の増加、中流階級の成長、都市化などの要因により、世界の航空旅客旅行の増加は、商用航空機用エンジン産業の強力な基盤となっています。この成長傾向は今後も続くと予想されており、特にインドや中国などの国々からかなりの数の人々が世界の中流階級に加わることになります。業界の視点では、コストと航空旅行者にとっての利便性の要因によってナローボディ機の台頭が強調されています。この変化は、世界のジェット旅客機の大部分を占めるエアバスのA320やボーイングのB737などの航空機の使用量の増加に反映されています。単通路機は引き続き市場を独占すると予想されており、商用航空機用タービンメーカーにとってはチャンスとなります。さらに、商用タービンエンジンに課せられる厳しい規制およびコンプライアンス基準により、他のセグメントにとって独特の参入障壁が生じます。これらの要件を満たすには、調査、開発、製造に多額の投資が必要ですが、多くの場合、確立された商用エンジンメーカーのみがこれを行うことができます。軍用エンジンは、過酷な戦闘や広範な使用に耐え、数十年にわたって使用できるように設計されています。その結果、政府はメンテナンス、修理、アップグレードに多額の投資を行っており、その結果、メーカーやサービスプロバイダーに継続的な収入源が生まれています。たとえば、ロールス・ロイス plcは2022年 7月に、世界最大の航空エンジン技術実証機「UltraFan」の最終構築段階に入り、将来の持続可能な航空旅行をサポートする技術を提供しました。デモンストレーターのエンジンはファン直径 140インチで、100%持続可能な航空燃料で動作します。新しいエンジンは、第1世代のトレントエンジンと比較して燃料効率が25%向上しました。長期的には、UltraFanエンジンの25,000ポンドから100,000ポンドの推力まで拡張可能なテクノロジーは、新しいワイドボディおよびナローボディの民間航空機に動力を供給する可能性をもたらします。

アジア太平洋が予測期間中に市場シェアを独占する

LCCモデルの継続的な成功は、アジア太平洋地域の旅客輸送量の着実な増加に貢献しています。また、さまざまな企業の航空機製造活動への投資を刺激することで、この地域の航空機およびエンジン製造業者の成長に大きな機会を生み出しました。より新しく改良されたバージョンの航空機に対する需要の高まりにより、航空機用ガスタービンエンジンも同時に必要になりました。多くの航空会社は、優れたMROおよびアフターサービスを受けるためにエンジンOEMと協力しようとしています。例えば、エアバスはすでにMRO市場の可能性を認識しており、買収、合弁事業(JV)、パートナーシップを通じてアジア太平洋での存在感を加速することに注力しています。

他の国際的なエンジンサプライヤーは、これらの開発が予測期間中に地域市場を促進するため、エンジンと関連コンポーネントの適切な供給を維持する必要があるでしょう。たとえば、2023年6月、インドと米国は、インド空軍(IAF)向けの戦闘機エンジンを製造するためのヒンドゥスタン・エアロノーティクス・リミテッド(HAL)とGEエアロスペースとの間の合意を発表しました。この取引は、IAFの能力と能力を向上させる取り組みの一環として行われました。 IAFは、軽戦闘機(LCA)Mk1A、続いてLCA Mk2を追加で取得するとともに、114機の多用途戦闘機(MRFA)を調達中です。 GEのF404エンジンは、インド唯一の国産戦闘機LCA Tejasの動力源として使用されています。現在、75基のF404エンジンがGEによって製造され、さらに99基がLCA Mk1Aで発注されています。 LCA Mk2の進行中の開発プログラムでは、8基のF414エンジンが供給されています。

航空機用タービンエンジン業界の概要

航空機用タービンエンジン市場は半統合化されており、多くの世界的ベンダーが存在することが特徴です。 CFM International、General Electric Company、Pratt & Whitney(RTX Corporation)、Rolls-Royce plc、Safranは市場の5つの主要企業であり、入手可能性、品質、価格、および技術の点で競争しています。市場は非常に競争が激しく、すべてのプレーヤーが最大の市場シェアを獲得しようと競い合っています。技術的問題による航空機の運航停止、高い生産コスト、エンジン納入の遅れ、関税や輸入関税の変動などが、市場の成長を脅かす主な要因となっています。ベンダーは、熾烈な競争市場環境で生き残り、成功するために、先進的で高品質のガスタービンエンジンを提供する必要があります。

社内の製造能力、世界の拠点ネットワーク、提供する製品、研究開発投資、強力な顧客ベースが、競合他社に対して優位性を持つための重要な領域です。世界経済状況の改善により、予測期間中の市場の成長が促進されると予想され、それにより新世代の航空機やエンジンを導入するのに理想的な時期となります。製品やサービスの拡張、技術革新、合併・買収の増加により、市場の競合環境はさらに激化すると思われます。たとえば、2021年 11月に、MaterializeとProponentは、航空宇宙のアフターマーケットサプライチェーンにおける3Dプリンティングのプロファイルを拡大するための提携を発表しました。 Proponentは、航空会社、MRO、OEM、革新的な製品ポートフォリオに従来の流通サービスを提供しています。同社は世界の事業展開を通じて、100か国以上の約6,000機の航空機顧客に年間5,400万個の部品を納入しています。これらの企業は、エンジン、機体、客室内装、コックピットなどのアフターマーケット部品を提供しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- エンドユーザー

- 民間・商用航空

- 軍用航空

- 航空機の種類

- 固定翼

- 回転翼

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- シンガポール

- その他アジア太平洋

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東とアフリカ

- サウジアラビア

- エジプト

- イスラエル

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- Safran

- Rolls-Royce plc

- General Electric Company

- Pratt &Whitney(RTX Corporation)

- Rostec State Corporation

- CFM international

- MTU Aero Engines AG

- Honeywell International Inc.

- Lycoming Engines(Avco Corporation)

第7章 市場機会と将来の動向

The Aircraft Turbine Engine Market size is estimated at USD 56.83 billion in 2024, and is expected to reach USD 92.62 billion by 2029, growing at a CAGR of 10.26% during the forecast period (2024-2029).

The demand for aircraft engines is driven primarily by either an increase in the order book of aircraft (business jet, commercial, or military aircraft) or a replacement for the engines for the existing aircraft fleet. Aircraft OEMs and engine manufacturers are engaging in extensive integration efforts to enhance performance and extend the range of aircraft. The investments towards the R&D of such technologies are anticipated to bolster the market prospects during the forecast period.

Since modern-day airlines operate on a merged profit model, the profit margins are relatively low. This scenario makes it challenging for operators to procure a new fleet and pay significant amounts of cash to complete the transaction. However, due to the emerging dynamics of the aircraft and engine leasing business, airlines have access to the comfort of opting for lease agreements from aircraft financing entities, providing financial relief to airlines and granting them temporary access to increased capacity.

The manufacturing cycle of aircraft engine OEMs is expected to undergo rapid transformation due to the increasing use of 3D printing and ceramic matrix composites to construct critical components of an aircraft engine. Furthermore, emerging technologies such as a hybrid-electric jet engine are anticipated to enhance the current business opportunities for the market players.

Aircraft Turbine Engine Market Trends

Commercial Segment to Dominate Market Share During the Forecast Period

The commercial segment holds the largest market share in the aircraft turbine engine market due to several compelling drivers. The rise in global air passenger travel, attributed to factors such as rising incomes, the growth of the middle class, and urbanization, provides a strong foundation for the commercial aircraft engine industry. This growth trend is expected to continue, with a significant number of people joining the global middle class, especially from countries like India and China. The industry perspective emphasizes the rise of single-aisle aircraft, driven by cost and convenience factors for air travelers. This shift is reflected in the increasing usage of aircraft like Airbus' A320 and Boeing's B737, comprising a significant portion of the global passenger jet fleet. Single-aisle aircraft are expected to continue dominating the market, presenting opportunities for commercial aircraft turbine manufacturers. Additionally, the stringent regulatory and compliance standards imposed on commercial turbine engines create a unique barrier to entry for other segments. Meeting these requirements necessitates substantial investments in research, development, and manufacturing, which often only established commercial engine manufacturers can undertake. Military engines are designed to last for decades, withstanding the rigors of combat and extensive use. Consequently, governments are heavily invested in their maintenance, repair, and upgrade, resulting in a continuous revenue stream for manufacturers and service providers. For instance, in July 2022, Rolls-Royce plc entered the final build stage for the world's largest aero-engine technology demonstrator "UltraFan", offering technologies to support sustainable air travel for future. The demonstrator engine has a fan diameter of 140 inches and runs on 100% Sustainable Aviation Fuel. The new engine offers a 25% fuel efficiency improvement compared with the first generation of Trent engine. In the longer term, the UltraFan engine's scalable technology from 25,000 to 100,000 lb. thrust offers the potential to power new wide-body and narrow-body commercial aircraft.

Asia-Pacific to Dominate the Market Share During the Forecast Period

The ongoing success of the LCC model has contributed to steady growth in passenger traffic in Asia-Pacific. It has also created significant opportunities for the growth of aircraft and engine manufacturers in the region by stimulating various companies to invest in aircraft manufacturing activities. The rise in demand for newer and improved versions of aircraft has resulted in a simultaneous requirement for aircraft gas turbine engines. Numerous airline operators are trying to collaborate with engine OEMs to receive superior MRO and after-services. For instance, Airbus has already realized the potential of the MRO market and has put in efforts to accelerate its presence in Asia-Pacific through acquisitions, joint ventures (JVs), and partnerships.

Other international engine suppliers will be required to maintain an adequate supply of engines and associated components as these developments will promote the regional market during the forecast period. For instance, In June 2023, India and the US announced the agreement between Hindustan Aeronautics Limited (HAL) and GE Aerospace to produce fighter jet engines for the Indian Air Force (IAF). The deal takes place in the context of efforts by the IAF to improve its capabilities and capacities. The IAF is in the process of procuring 114 multi-role fighter jets (MRFA), along with acquiring additional numbers of Light Combat Aircraft (LCA) Mk1A, followed by LCA Mk2. GE's F404 engines are the engine used to power India's only indigenous fighter jet LCA Tejas. As of now, 75 F404 engines have been manufactured by GE and another 99 are on order with LCA Mk1A. In the ongoing development programme for LCA Mk2, 8 F414 engines have been supplied.

Aircraft Turbine Engine Industry Overview

The aircraft turbine engine market is semi-consolidated and characterized by the presence of many global vendors. CFM International, General Electric Company, Pratt & Whitney (RTX Corporation), Rolls-Royce plc, and Safran are five major companies in the market, which compete in terms of availability, quality, price, and technology. The market is highly competitive with all the players competing to gain the largest market share. Grounding of fleets due to technical issues, high production costs, delays in engine deliveries, and fluctuations in customs and import duties are the key factors posing a threat to the growth of the market. Vendors must provide advanced and high-quality gas turbine engines to survive and succeed in the intensely competitive market environment.

In-house manufacturing capabilities, a global footprint network, product offerings, R&D investments, and a strong client base are the key areas to have the edge over competitors. Improving global economic conditions is expected to fuel market growth during the forecast period, thereby making it an ideal time to adopt new-generation aircraft and engines. The competitive environment in the market is likely to intensify further due to an increase in product and service extensions, technological innovations, and mergers and acquisitions. For instance, In November 2021, Materialize and Proponent announced a partnership to expand the profile of 3D printing in aerospace aftermarket supply chains. Proponent offers traditional distribution services to airlines, MROs, Original Equipment Manufacturers, and Innovative Product Portfolios. Through its global coverage, the firm delivers 54 million parts a year to approximately 6,000 aircraft clients in more than 100 countries. These companies offer aftermarket parts, such as engines, airframes, cabin interiors, and cockpits.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 End-user

- 5.1.1 Civil and Commercial Aviation

- 5.1.2 Military Aviation

- 5.2 Aircraft Type

- 5.2.1 Fixed-wing

- 5.2.2 Rotorcraft

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Singapore

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Egypt

- 5.3.5.3 Israel

- 5.3.5.4 South Africa

- 5.3.5.5 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Safran

- 6.2.2 Rolls-Royce plc

- 6.2.3 General Electric Company

- 6.2.4 Pratt & Whitney (RTX Corporation)

- 6.2.5 Rostec State Corporation

- 6.2.6 CFM international

- 6.2.7 MTU Aero Engines AG

- 6.2.8 Honeywell International Inc.

- 6.2.9 Lycoming Engines (Avco Corporation)