|

市場調査レポート

商品コード

1437427

PHR(Personal Health Record)ソフトウェア:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年)Global Personal Health Records Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| PHR(Personal Health Record)ソフトウェア:世界市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 116 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

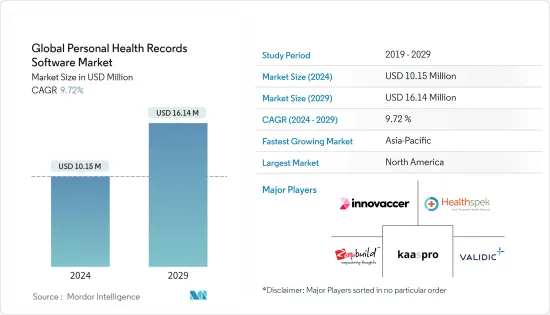

世界のPHR(Personal Health Record)ソフトウェア市場規模は、2024年に1,015万米ドルと推定され、2029年までに1,614万米ドルに達すると予測されており、予測期間(2024年から2029年)中に9.72%のCAGRで成長します。

COVID-19のパンデミックは、PHRソフトウェア市場に大きな影響を与えています。COVID-19の蔓延を遅らせることを目的とした厳格なロックダウンと政府の規制により、医療活動が減少し、PHRソフトウェアの使用にも悪影響を及ぼしました。例えば、2021年2月にBMJジャーナルに掲載された「COVID-19のパンデミックが医療サービスの利用に及ぼす影響:系統的レビュー」というタイトルの記事によると、医療サービスの利用における変化の範囲と性質を判断するために体系的な研究が実施されたといいます。COVID-19のパンデミック中に医療医療とサービスの利用率が約3分の1に減少したことがわかりました。さらに、2022年1月に国立医学図書館ジャーナルに掲載された「デジタルヘルスのCOVID-19の影響評価:得られた教訓と説得力のあるニーズ」というタイトルの記事にあるように、調査が実施され、患者にとってデジタル格差はさらに深刻化していることが示されました。この傾向はパンデミックの最中に顕著であり、重要なテクノロジーと信頼できるインターネットへのアクセスにより、PHRソフトウェアに新たな機会が生まれました。したがって、COVID-19の発生は、その準備段階で市場の成長に悪影響を及ぼしました。ただし、PHRソフトウェアがパンデミック中に個人の医療データ管理に新たな機会を提供したため、市場は牽引力を増すことが予想されます。

さらに、合理化された医療情報に対するニーズの高まり、患者中心のパーソナルケアを促進する取り組みの高まり、オンラインデータ統合に対する政府の取り組みの高まりなどが、調査対象市場の成長を促進する主な要因となっています。がん、糖尿病、呼吸器疾患などの慢性疾患の有病率の上昇も市場の成長を促進すると予想されています。

さらに、2022年 8月に公開されたBreaking Media, Inc.のブログによると、ワークフローの合理化により相互運用性が最大化され、患者の転帰が改善され、これによりPHRソフトウェアを含むクラウドベースのソフトウェアの機会が生まれるとのことです。したがって、合理化された医療情報に対するニーズの高まりにより、世界的にPHRソフトウェア市場が加速する傾向にあり、将来的にも増加すると予想され、それによって予測期間中に調査対象市場の成長を推進します。

さらに、新興企業の数の増加と市場の主要企業による戦略的活動は、調査対象市場の成長にプラスの影響を与えています。たとえば、2020年 12月にEka Careが設立され、同社はPHRアプリを提供し、医療提供者と患者の間にデジタル対応で接続された医療エコシステムを構築することを目指しています。さらに、2022年5月に国家保健局(NHA)は、インド政府がその主力スキームであるアユシュマン・バーラト・デジタル・ミッション(ABDM)の下で、PHR管理のための改良されたアユシュマン・バーラト・ヘルス・アカウント(ABHA)モバイル・アプリケーションを開始したと発表しました。したがって、製品の発売とパートナーシップにより、調査対象の市場は予測期間中に大幅な成長を遂げると予想されます。

したがって、前述の要因により、調査対象の市場は分析期間中に成長すると予想されます。ただし、ソフトウェアに関するセキュリティ上の懸念と地方の患者の認識不足により、市場の成長が妨げられる可能性があります。

PHRソフトウェア市場動向

モバイルアプリとソフトウェアセグメントは予測期間中に成長すると予想される

モバイルアプリとソフトウェアは扱いが簡単なので、それらにPHRシステムを実装すると、患者がすべての健康記録を効果的に処理および管理するための非常に使いやすいインターフェースが作成されます。使いやすいインターフェイスと高速なデータ管理は、近年人気が高まっているモバイルアプリやソフトウェアの利点の一部です。さらに、2021年4月にSeventh Sense Research Group(SSRG)International Journal of Mobile Computing and Applicationに掲載された「医療業界におけるモバイルアプリに関する研究」というタイトルの記事によると、最近の研究では、医療アプリの個人使用が臨月の妊娠を予測することが示されているといいます。以前は標準であった紙の車輪よりも正確に日付を取得できます。したがって、PHRモバイルアプリとソフトウェアが提供する利点により、これらの製品の採用は対象人口の間で増加し、最終的に市場の成長を促進する可能性があります。

さらに、2021年8月に医療 Information and Management Systems Society, Inc.(HIMSS)が発行した「医療の将来レポート:医療ケア利害関係者の探求「次章への期待」」と題した記事によると、医療提供者の80%が投資の増加を計画しているとのことです。今後5年間でテクノロジーとデジタルソリューションの分野での成長が期待されており、主催者は人工知能(AI)、クラウドコンピューティング、XR、IoTを活用して、新しい治療法やサービスを開発、提供します。したがって、医療システムのデジタル化の進展により、技術的に高度なモバイルアプリとソフトウェアの需要が生まれ、将来的にこの分野が成長する機会が生まれます。

さらに、市場の主要企業による継続的な製品発売は、この部門の成長にプラスの影響を与えています。たとえば、インドの医療サービスへのアクセスとその質を改善するスタートアップであるHealth Safeは、2021年 12月に、すべての医療記録を安全なデジタル形式で保管し、医師や家族とすぐに共有できるアプリ「Keypr」を立ち上げました。テクノロジー業界のリーダーから非公開の金額を調達した後、他の医療サービスプロバイダーと協力しました。さらに、2021年11月、オーストラリアデジタルヘルス庁(ADHA)は、アカウント所有者向けのPHRモバイルアプリ「My Health Record」を構築するためにシャモニーITマネジメントコンサルティングと契約を結んだと発表しました。

したがって、モバイルアプリとソフトウェアセグメントは、上記の要因により、予測期間中に大幅な成長を遂げると予想されます。

北米がPHRソフトウェア市場を独占している

北米は、技術的に進んだ製品が容易に入手できること、およびこの地域におけるPHR管理に対する消費者の意識が高いことなどの要因により、市場を独占しています。米国におけるさまざまな慢性疾患の有病率の増加は、北米での調査対象市場の成長に貢献する重要な要因の1つです。

たとえば、2022年 1月の疾病管理予防センター(CDC)のデータによると、米国には約3,730万人が糖尿病を患っており、これは米国総人口の11.3パーセントを占めています。さらに、2020年の米国国立がん研究所のデータによると、米国では推定1,806,590人が新たにがんと診断され、606,520人ががんにより死亡しました。この地域におけるこれらの慢性疾患の有病率の上昇により、PHRソフトウェアとアプリの必要性が生じ、この要因がこの国の市場の成長を促進すると予想されます。

したがって、前述の要因により、調査対象市場の成長は北米地域で予想されます。

PHRソフトウェア業界の概要

PHRソフトウェア市場は、世界的および地域的に事業を展開する複数の企業が存在するため、本質的に細分化されています。競合情勢には、市場シェアを保持し、よく知られている数社の国際企業と地元企業の分析が含まれています。これには、Patient Ally、Health Companion、Healthspeck、NoMoreClipboard、Records For Living, Inc.、Health Safe、Knapsack Health、Kaaspro、Zapbuild、Validicなどが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 合理化された医療情報のニーズの高まりと患者中心のパーソナルケアを促進する取り組みの高まり

- オンラインデータ統合に対する政府の取り組みの高まり

- 市場抑制要因

- ソフトウェアに関するセキュリティ上の懸念

- 農村部の患者における認識の欠如

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- コンポーネントの種類別

- モバイルアプリとソフトウェア

- サービス

- 展開モード別

- クラウドベース

- ウェブベース

- アーキテクチャ別

- ペイヤー

- プロバイダー

- スタンドアロン

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋

- 世界のその他の地域

- 北米

第6章 競合情勢

- 企業プロファイル

- Patient Ally

- Health Companion

- Healthspek

- NoMoreClipboard

- Records For Living, Inc.

- Health Safe

- Knapsack Health

- kaaspro

- Zapbuild

- Validic

- Innovaccer, Inc.

第7章 市場機会と将来の動向

The Global Personal Health Records Software Market size is estimated at USD 10.15 million in 2024, and is expected to reach USD 16.14 million by 2029, growing at a CAGR of 9.72% during the forecast period (2024-2029).

COVID-19 pandemic has had a substantial impact on the personal health records software market. The strict lockdowns and government regulations intended to slow down the spread of COVID-19 resulted in a decrease in healthcare activities and it adversely affected the usage of personal health records software as well. For instance, according to an article titled 'Impact of COVID-19 pandemic on utilization of healthcare services: a systematic review' published in the BMJ Journals in February 2021 a systemic study was performed to determine the extent and nature of changes in the utilization of healthcare software and services during COVID-19 pandemic and it was found that healthcare software and services utilization decreased by about a third during the pandemic. Furthermore, as per an article titled 'Digital Health COVID-19 Impact Assessment: Lessons Learned and Compelling Needs' published in the journal of National Library of Medicine in January 2022 a survey was performed which showed that for the patients the deepening digital divide became more pronounced during the pandemic and access to essential technology and reliable internet created new opportunities for personal health records software. Thus, the COVID-19 outbreak affected the market's growth adversely in its preliminary phase; however, the market is expected to gain traction as personal health records software provided new opportunities for personal healthcare data management during the pandemic.

Further, increasing need for streamlined healthcare information and rising initiatives to encourage patient centric personal care, and rising government initiatives for online data integration are among the major factors driving the growth of the studied market. The rising prevalence of chronic diseases like cancer, diabetes and respiratory disorders is also expected to drive the growth of the market.

Moreover, according to a blog by Breaking Media, Inc. published in August 2022 streamlined workflow maximizes interoperability and improves patient outcomes, and this will create an opportunity for cloud-based software which includes personal health records software as well. Therefore, the increasing need for streamlined healthcare information is poised to accelerate the personal health records software market globally and is expected to increase in the future, thereby driving the growth of the studied market over the forecast period.

In addition, growing number of startup companies and strategic activities by major players in the market are positively affecting the growth of the studied market. For instance, in December 2020 Eka Care was founded, the company provided personal health records app and they aim to build a digitally-enabled and connected healthcare ecosystem between healthcare providers and patient. Additionally, in May 2022, National Health Authority (NHA) announced that the government of India has launched a revamped Ayushman Bharat Health Account (ABHA) mobile application for personal health records management under its flagship scheme of Ayushman Bharat Digital Mission (ABDM). Thus, owing to the product launches and partnerships the studied market is expected to have significant growth over the forecast period.

Therefore, owing to the aforementioned factors the studied market is anticipated to witness growth over the analysis period. However, the security concerns regarding the software and lack of awareness among rural patients are likely to impede market growth.

Personal Health Records Software Market Trends

Mobile Apps and Software Segment is Expected to Witness Growth Over the Forecast Period

Mobile apps and software are easy to handle and thus implementing personal health records systems in those will create a very easy-to-use interface for the patients to effectively handle and manage all their health records. Easy-to-use interface and fast data management are some of the advantages of mobile apps and software for which it has gained popularity in recent years. Moreover, according to an article titled 'A study on Mobile apps in the Healthcare Industry' published in the Seventh Sense Research Group (SSRG) International Journal of Mobile Computing and Application in April 2021 recent studies showed that personal use of health apps predicts pregnancy due dates more accurately than the paper wheels that had previously been the standard. Hence, owing to the advantages offered by personal health records mobile apps, and software, the adoption of these products is likely to increase among the target population, ultimately driving the market growth.

In addition, according to an article titled 'Future of Healthcare Report: Exploring Healthcare Stakeholders' Expectations for the Next Chapter' published by Healthcare Information and Management Systems Society, Inc. (HIMSS) in August 2021 80 percent of healthcare providers plan to increase investment in technology and digital solutions over the next five years and it is also expected to see growth in areas including telemedicine, personalized medicine, genomics, and wearables, with organizers leveraging artificial intelligence (AI), cloud computing, extender reality (XR), and the internet of things (IoT) to develop and deliver new treatments and service. Thus, the increasing digitalization of healthcare systems will create demand for technically advanced mobile apps and software and is creating opportunities for the growth of the segment in the future.

Furthermore, continuous product launches by major players in the market are positively affecting the growth of the segment. For instance, in December 2021, Health Safe a startup improving access to and quality of healthcare services in India, launched "Keypr," an app that helps in keeping all medical records in a secure digital format, ready for sharing with doctors, family members and other health service providers, after raising an undisclosed amount from technology industry leaders. Moreover, in November 2021 The Australian Digital Health Agency (ADHA) announced that they have signed a contract with Chamonix IT Management Consulting for the company to build out a 'My Health Record' personal health records mobile app for accountholders

Therefore, the mobile apps and software segment is expected to witness significant growth over the forecast period due to the abovementioned factors.

North America is Dominating the Personal Health Records Software Market

North America is dominating the market owing to factors such as the easy availability of technologically advanced products, and high awareness among consumers about personal health records management in the region. An increase in the prevalence of various chronic diseases in the United States is among the key factors which contribute to the growth of the studied market in North America.

For instance, as per the data by Centers for Disease Control and Prevention (CDC) in January 2022 there are almost 37.3 million people in the United States who have diabetes and this comprises 11.3 percent of the total United States population. Furthermore, as per the data by National Cancer Institute of the United States in 2020, an estimated 1,806,590 new cases of cancer were diagnosed in the United States and 606,520 people died from the disease. The rising prevalence of these chronic diseases in the region will create a need for personal health records software and apps and this factor is anticipated to drive the growth of the market in the country.

Therefore, owing to the aforesaid factors the growth of the studied market is anticipated in the North America Region.

Personal Health Records Software Industry Overview

The personal health records software market is fragmented in nature due to the presence of several companies operating globally as well as regionally. The competitive landscape includes an analysis of a few international as well as local companies which hold the market shares and are well known. include Patient Ally, Health Companion, Healthspek, NoMoreClipboard, Records For Living, Inc., Health Safe, Knapsack Health, Kaaspro, Zapbuild, and Validic among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Need for Streamlined Healthcare Information and Rising Initiatives to Encourage Patient Centric Personal Care

- 4.2.2 Rising Government Initiatives for Online Data Integration

- 4.3 Market Restraints

- 4.3.1 Security Concerns Regarding the Software

- 4.3.2 Lack of Awareness Among Rural Patients

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Component Type

- 5.1.1 Mobile Apps and Softwares

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 Web-Based

- 5.3 By Architecture

- 5.3.1 Payer Tethered

- 5.3.2 Provider Tethered

- 5.3.3 Standalone

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Patient Ally

- 6.1.2 Health Companion

- 6.1.3 Healthspek

- 6.1.4 NoMoreClipboard

- 6.1.5 Records For Living, Inc.

- 6.1.6 Health Safe

- 6.1.7 Knapsack Health

- 6.1.8 kaaspro

- 6.1.9 Zapbuild

- 6.1.10 Validic

- 6.1.11 Innovaccer, Inc.