|

市場調査レポート

商品コード

1436022

心臓インプラント:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Cardiac Implants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 心臓インプラント:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

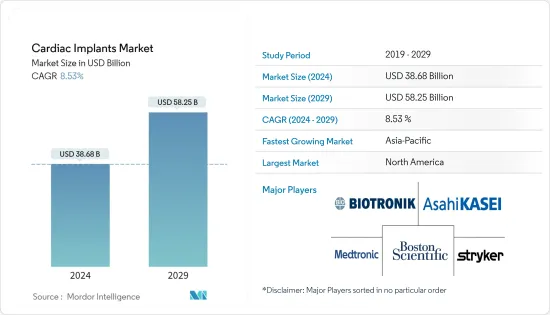

心臓インプラント市場規模は、2024年に386億8,000万米ドルと推定され、2029年までに582億5,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に8.53%のCAGRで成長します。

COVID-19の発生は、心臓インプラント装置市場を含む医療機器業界のあらゆる側面に大きな影響を与えました。パンデミックの間、循環器科で救急治療が受けられるにもかかわらず、患者の来院数は大幅に減少しました。COVID-19患者に近接して治療を行うことさえ、心臓専門医にとっては課題でした。医療従事者がCOVID-19患者の治療に携わっていたため、アクセスは必要不可欠な治療のみに制限され、心臓病センターの一時閉鎖により心臓手術は大幅に減少しました。メドトロニック PLCなどの心臓インプラント業界の主要企業は、2020年第4四半期に60億米ドルの収益減少を報告しました。しかし、2022会計年度の収益は2021会計年度と比較して16億米ドルわずかに増加しました。COVID-19のパンデミックの影響で2021会計年度の第1四半期と第2四半期に経験した低迷から世界の手術件数が回復したため。したがって、COVID-19が市場の成長に及ぼす影響は、流行の初期段階では悪影響を及ぼしたが、世界中で手術や治療が再開されているため、近い将来、市場はパンデミック前の水準まで牽引力を得ることが予想されます。

心血管疾患の発生率と高齢者人口の増加が、心臓インプラント市場の促進要因となっています。たとえば、2022年 2月に発表された米国心臓協会の報告書によると、世界では2020年に2億4,410万人が虚血性心疾患(IHD)を患っていると推定されており、女性よりも男性でより有病率が高くなりました(それぞれ1億4,100万人、1億310万人)。同様に、疾病管理予防センターの2022年 6月の最新情報によると、2020年に米国では20歳以上の成人約2,010万人が冠状動脈性心疾患(CAD)を患っていました。また、冠状動脈性心疾患は米国で最も一般的なタイプの心疾患であるとも述べています。糖尿病、過体重または肥満、不健康な食事、運動不足、過度のアルコール摂取が心臓病の主な原因でした。世界中で心臓病の頻度が増加している結果、心臓病に苦しむ人々が心臓インプラントを含む外科手術を受け入れることが増えており、これが市場の成長を促進しています。

さらに、技術の進歩と新製品の承認および発売により、調査期間中の市場の成長が促進されます。たとえば、2020年10月、アボットは異常な心拍リズムと心不全のための新しい植込み型除細動器(ICD)と心臓再同期療法除細動器(CRT-D)装置をインドで発売しました。

したがって、上記の要因により、市場は将来的に大幅な成長を遂げると予想されます。ただし、心臓インプラントの高コストと心臓インプラントに関連する副作用は、市場の成長を抑制する可能性のある要因の一部です。

心臓インプラント市場動向

植込み型除細動器(ICD)セグメントは、予測期間中により急速に成長し、市場を独占すると予想されます

植込み型除細動器(ICD)は、不規則な心拍(不整脈)を検出して停止するために胸部に設置される、電池駆動の小型装置です。心拍を継続的に監視し、必要に応じて電気ショックを与えて、規則的な心拍リズムを回復します。植込み型除細動器(ICD)セグメントは、心血管疾患の症例増加や技術的に先進的な製品の採用増加などの要因により、大幅な成長が見込まれています。

世界保健機関によると、2020年には毎年1,790万人が心血管疾患で死亡していると推定されており、これは世界全体の死亡者数の32%を占め、そのうち85%は心臓発作と脳卒中によるものです。ただし、個人への影響を最小限に抑えるために、心血管疾患をできるだけ早期に検出することが重要です。

さらに、2022年6月に発表された「中国における心房細動の有病率とリスク:国家横断的疫学研究」と題された2020年から2021年に実施された研究によると、心房細動の有病率は中国成人人口の1.6%であり、その後増加傾向にあります。高齢者人口の増加に伴う心臓病の有病率の増加を考慮すると、心臓手術、特に心臓インプラントの範囲は今後数年間で拡大すると推定されています。さらに、2020年1月、メドトロニック plcは、植込み型除細動器(ICD)のコバルトおよびクロムのポートフォリオに対してCE(Conformite Europeenne)マークを取得しました。

したがって、上記の要因を考慮すると、植込み型除細動器(ICD)セグメントは予測期間中に成長すると予想されます。

北米が市場を独占しており、予測期間にも同様の成長が予想される

心臓インプラント市場では北米が主要な市場シェアを占めています。疾病管理予防センター(CDC)の最新報告書2022年によると、米国で報告された心臓病による死亡者数は2019年に65万9,041人で、2020年には69万882人に増加しました。米国疾病管理予防センター(CDC)は、心臓病と脳卒中の主な危険因子は高血圧、糖尿病、高LDL(悪玉)コレステロール、喫煙であると述べています。また、上記の同じ情報源によると、米国では2030年までに1,210万人が心房細動になると推定されています。

市場で活動している著名なプレーヤーによる新製品の承認と発売により、この地域の市場の成長がさらに促進されると予想されます。たとえば、2022年 2月にアボットは、心不全を抱えて生きるより多くの人々のケアをサポートするために、米国食品医薬品局(FDA)からCardioMEMS HFシステムの適応拡大承認を取得しました。 CardioMEMS HFシステムは、カテーテルを使用して患者の肺動脈に埋め込まれるペーパークリップサイズのセンサーです。また、2022年4月、アボット社は米国食品医薬品局(FDA)から、米国の心拍リズムが遅い患者の治療用のAveir単腔(VR)リードレスペースメーカーの承認を取得しました。

したがって、上記の要因と新たな承認と発売により、北米は予測期間中に市場の大幅な成長を示すと予想されます。

心臓インプラント業界の概要

心臓インプラント市場は、本質的に世界中の著名なプレーヤーによって統合されています。市場シェアの点では、現在、いくつかの大手企業が市場を独占しています。心臓インプラント企業は、技術的に高度なソリューションを患者に提供するための新製品開発にさらに注力しており、主要企業間の競合が激化しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 心血管疾患の発生率の増加

- 退屈なライフスタイルの採用の増加と高齢者人口の増加

- 償還に関する政府の有利な政策

- 市場抑制要因

- 心臓インプラントの高額な費用

- 心臓インプラントによる副作用

- 業界の魅力- ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 製品別

- 植込み型除細動器(ICD)

- ペースメーカー

- 冠動脈ステント

- 植込み型心拍リズムモニター

- 植込み型血行動態モニター

- その他

- 用途別

- 不整脈

- 急性心筋梗塞

- 心筋虚血

- その他

- エンドユーザー別

- 病院

- 循環器センター

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Medtronic

- Boston Scientific Corporation

- Stryker(Physio-Control Inc.)

- Biotronik

- Asahi Kasei Corporation(ZOLL Medical Corporation)

- Pacetronix.com

- Schiller AG

- Koninklijke Philips NV

- LivaNova PLC

- Abbott.

- Impulse Dynamics

- Angel Medical Systems, Inc.

第7章 市場機会と将来の動向

The Cardiac Implants Market size is estimated at USD 38.68 billion in 2024, and is expected to reach USD 58.25 billion by 2029, growing at a CAGR of 8.53% during the forecast period (2024-2029).

The COVID-19 outbreak greatly impacted every aspect of the medical device industry, including the cardiac implants devices market. The number of patient visits during the pandemic was drastically reduced, despite having access to emergency care in the cardiology department. Even the treatment proximity to infected patients with COVID-19 was a challenge for cardiologists. Access was restricted to essential care only, and the temporary closure of cardiology centers considerably reduced cardiac surgeries, as the healthcare providers were engaged with COVID-19 patients. Major players in the cardiac implant industry, such as Medtronic PLC, reported a decline in revenue of 6 billion USD in Q4 2020. But the revenue was slightly increased by 1.6 billion USD in the fiscal year 2022 compared with the fiscal year 2021. This was due to the recovery of global procedure volumes from the downturn experienced in the first and second quarters of the fiscal year 2021 as a result of the COVID-19 pandemic. Hence, the impact of COVID-19 on the market's growth was adverse in the initial phase of the outbreak, however, as surgeries and treatments have resumed worldwide, the market is anticipated to gain traction to its pre-pandemic levels in the near future.

The increase in the incidence of cardiovascular diseases and the geriatric population are the driving factors for the cardiac implants market. For instance, as per the report of the American Heart Association published in February 2022, globally, it was estimated that in 2020, 244.1 million people had ischemic heart disease (IHD), and it was more prevalent in males than in females (141.0 and 103.1 million people, respectively). Likewise, according to the Centers for Disease Control and Prevention, in June 2022 update, about 20.1 million adults aged 20 and older had coronary heart disease (CAD) in 2020 in the United States. It also stated that coronary heart disease is the most common type of heart disease in the United States. Diabetes, overweight or obesity, an unhealthy diet, physical inactivity, and excessive alcohol use were the main causes of heart disease. As a result of the increasing frequency of heart illnesses worldwide, people who are affected by them are increasingly embracing surgical procedures, including cardiac implants, which is fueling the market's growth.

In addition, advancements in technology and new product approvals and launches drive the market's growth during the study period. For instance, in October 2020, Abbott launched its new implantable cardioverter defibrillator (ICD) and cardiac resynchronization therapy defibrillator (CRT-D) devices in India for abnormal heart rhythms and heart failure.

Hence, owing to the factors mentioned above, the market is expected to witness significant growth in the future. However, the high cost of cardiac implants and the side effects associated with cardiac implants are some of the factors that may restrain the market's growth.

Cardiac Implants Market Trends

Implantable Cardioverter-Defibrillators (ICDs) Segment is Expected to Grow Faster and Dominate the Market Over the Forecast Period

An implantable cardioverter-defibrillator (ICD) is a small battery-powered device placed in the chest to detect and stop irregular heartbeats (arrhythmias). It continuously monitors the heartbeat and delivers electric shocks, when needed, to restore a regular heart rhythm. The implantable cardioverter-defibrillators (ICDs) segment is expected to witness significant growth owing to factors such as increasing cases of cardiovascular diseases and increasing adoption of technologically advanced products.

According to the World Health Organization, in 2020, it is estimated that 17.9 million people die from cardiovascular diseases each year, which is 32% of all global deaths, of which 85% were due to heart attack and stroke. However, it is important to detect cardiovascular diseases as early as possible to minimize their effect on individuals.

Furthermore, as per the study conducted from 2020 to 2021 titled "Prevalence and risk of atrial fibrillation in China: A national cross-sectional epidemiological study" published in June 2022, the prevalence of atrial fibrillation was 1.6% in the Chinese adult population and increased with age. By considering the increase in the prevalence of heart diseases with an increase in the geriatric population, the scope for heart procedures, especially cardiac implants, is estimated to grow over the coming years. Moreover, in January 2020, Medtronic plc received the CE (Conformite Europeenne) mark for its Cobalt and Crome portfolio of implantable cardioverter-defibrillators (ICD).

Thus, considering the abovementioned factors, the implantable cardioverter-defibrillators (ICDs) segment is expected to grow over the forecast period.

North America Dominates the Market and is Expected to do Same in the Forecast Period

North America holds the major market share in the cardiac implants market. According to the Centers for Disease Control and Prevention (CDC) updated report 2022, the number of deaths reported due to heart diseases was 659,041 in 2019 and increased to 690,882 in 2020 in the United States. The Centers for Disease Control and Prevention (CDC) stated that the key risk factors for heart disease and stroke are high blood pressure, diabetes, high LDL (bad) cholesterol, and smoking. Also, according to the same above-mentioned source, it is estimated that 12.1 million people in the United States will have atrial fibrillation by 2030. Thus, an increase in the prevalence of cardiovascular diseases will have a positive impact on the usage of cardiac implants and drive the market growth.

New product approvals and launches by the prominent players operating in the market are anticipated to further boost the market's growth in the region. For instance, in February 2022, Abbott received expanded indication approval for the CardioMEMS HF System from the United States Food and Drug Administration (FDA) to support the care of more people living with heart failure. The CardioMEMS HF System is a paperclip-sized sensor implanted in a patient's pulmonary artery using a catheter. Also, in April 2022, Abbott received approval from the United States Food and Drug Administration (FDA) for the Aveir single-chamber (VR) leadless pacemaker for the treatment of patients in the United States with slow heart rhythms.

Hence, due to the factors mentioned above and new approvals and launches, North America is expected to witness significant growth in the market over the forecast period.

Cardiac Implants Industry Overview

The cardiac implants market is consolidated in nature with prominent players across the world. In terms of market share, a few of the major players currently dominate the market. The cardiac implant companies are focusing more on new product development to provide technologically advanced solutions to patients, which is boosting the competition among the key players. Some of the major players in the market are Medtronic, Boston Scientific Corporation, Stryker (Physio-Control Inc.), Biotronik, Asahi Kasei Corporation (ZOLL Medical Corporation), Pacetronix.com, Schiller AG, Koninklijke Philips NV, LivaNova PLC, Abbott, Impulse Dynamics, and Angel Medical Systems, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence of Cardiovascular Diseases

- 4.2.2 Increase in Adoption of Torpid Lifestyle and Rising Incidence of Geriatric Population

- 4.2.3 Favourable Government Policies for Reimbursement

- 4.3 Market Restraints

- 4.3.1 High Cost of Cardiac Implants

- 4.3.2 Side Effects due to Cardiac Implants

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Product

- 5.1.1 Implantable Cardioverter-defibrillators (ICDs)

- 5.1.2 Pacemakers

- 5.1.3 Coronary Stents

- 5.1.4 Implantable Heart Rhythm Monitors

- 5.1.5 Implantable Hemodynamic Monitors

- 5.1.6 Other Products

- 5.2 By Application

- 5.2.1 Arrhythmias

- 5.2.2 Acute Myocardial Infarction

- 5.2.3 Myocardial Ischemia

- 5.2.4 Other Applications

- 5.3 By End Users

- 5.3.1 Hospitals

- 5.3.2 Cardiology Centers

- 5.3.3 Other End Users

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia Pacific

- 5.4.4 Middle-East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Medtronic

- 6.1.2 Boston Scientific Corporation

- 6.1.3 Stryker (Physio-Control Inc.)

- 6.1.4 Biotronik

- 6.1.5 Asahi Kasei Corporation (ZOLL Medical Corporation)

- 6.1.6 Pacetronix.com

- 6.1.7 Schiller AG

- 6.1.8 Koninklijke Philips N.V.

- 6.1.9 LivaNova PLC

- 6.1.10 Abbott.

- 6.1.11 Impulse Dynamics

- 6.1.12 Angel Medical Systems, Inc.