|

市場調査レポート

商品コード

1644307

アプリケーションリリース自動化:市場シェア分析、産業動向、成長予測(2025年~2030年)Application Release Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アプリケーションリリース自動化:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

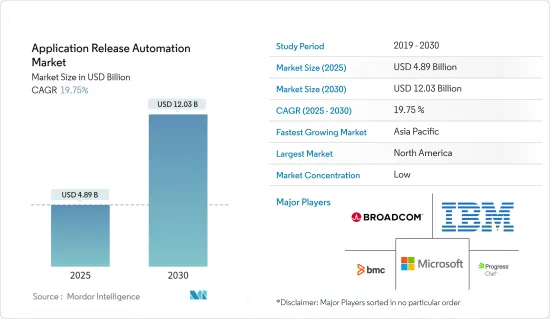

アプリケーションリリース自動化の市場規模は2025年に48億9,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは19.75%で、2030年には120億3,000万米ドルに達すると予測されます。

デジタルインフラは、ビジネスの変化とともに世界的に大きく進化しており、それによって近代化が成功の鍵となっています。さらに、COVID-19パンデミックの出現により、アプリケーションの可視化と管理がさらに注目を集め、自宅や企業で働く従業員が、場所を問わず従業員の生産性を維持できるように環境を急速に変化させました。このことが、予測期間中の市場の成長をさらに押し上げると予想されます。さらに、リモートワーク環境への移行に伴いCOVID-19ロックダウンが実施されたため、これまでにない数の人々が仕事やその他の活動にモバイルアプリケーションを使用するようになり、これらのアプリケーションへのシームレスなセキュリティアクセスのニーズが生まれました。

主なハイライト

- ほとんどの企業でデジタルトランスフォーメーションの導入が進み、人工知能、ビッグデータ、コグニティブオートメーションなど、企業の収益を押し上げる先進技術への投資が増加していることが、アプリケーションリリース自動化市場を押し上げる主な要因の1つとなっています。

- デジタルトランスフォーメーションの拡大により、ほとんどの企業はアプリケーションやツールを導入して市場からのフィードバックに対応し、これまで以上に迅速にエンドユーザーに新しい体験を提供する必要に迫られています。企業は、このような新しい市場環境において競争力を維持し、デリバリーを迅速化するために、アプリケーションリリース自動化ソフトウェアに目を向けています。アプリケーションリリース自動化を活用することで、企業はソフトウェアの迅速な配信とアップデートを容易に処理できるようになり、人的ミスや手順の見落とし、潜在的な生産上の問題を減らすことができます。

- さらに、市場を牽引する主な要因は、ソフトウェア・アプリケーションの新機能を本番環境で迅速にロールアウトしたり、ダウンタイムをほとんど発生させずにセキュリティ・パッチを適用したりして、100%のアップタイムを保証しなければならないというIT部門に対するプレッシャーが高まっていることです。さらに、COVID-19によって、世界中でかつてない数の人々がオフィスから自宅へと職場を変えることを余儀なくされ、通信サービス・プロバイダーには、完璧なデジタル・コミュニケーション能力で機能する社会をサポートしなければならないという大きなプレッシャーがかかっています。

- 2023年2月、エネルギー管理とオートメーションのデジタルトランスフォーメーションのリーダーであるシュナイダーエレクトリックは、フロリダ州オーランドで開催された第27回ARCインダストリー・リーダーシップ・フォーラムにおいて、新しいインダストリアル・デジタルトランスフォーメーション・サービスを発表しました。この専門的な世界・サービスは、産業界の企業が将来対応可能で、革新的、持続可能かつ効果的なエンドツーエンドのデジタル・トランスフォーメーションを実現できるように設計されています。

アプリケーションリリース自動化市場の動向

クラウドが大きな市場シェアを占める見込み

- 世界中の企業が急速にアプリケーションをクラウドに移行しているため、世界市場ではクラウドベースのアプリケーションに対する需要が急増しています。さらに、Apps Run The Worldが実施した調査によると、2021年のクラウドアプリケーション市場シェアでは、マイクロソフトが13%でトップ。セールスフォースとオラクルは、それぞれ11%と7%のシェアを獲得し、僅差で続いた。

- クラウドベースのアプリケーションとウェブサーバーは、クライアントが世界中のどこからでも俊敏にアプリケーションにアクセスできるようにするだけでなく、レガシーシステムを使用しているときに企業のダウンタイムによって発生するコストを削減します。

- 従来のアプリケーションリリース自動化は、アプリケーションサーバーの負荷分散を行い、トラフィックとアプリケーションのデプロイメントを管理するために使用されていました。長年にわたり、SSLオフロード、可視化、アプリケーション分析、マルチクラウド対応、TCP最適化、レートシェーピング、Webアプリケーションファイアウォールなどの新しい機能が統合されてきました。

- 2022年6月、継続的デプロイメント(CD)企業であるArmoryは、開発チームがあらゆる規模でソフトウェアを簡単、確実、安全、継続的にデプロイできるようにするArmory Continuous Deployment-as-a-Serviceの一般提供を発表しました。この製品は、高度なプログレッシブ戦略をサポートする複数の環境に宣言的なデプロイメントを提供し、開発者はデプロイよりも優れたコードの構築に集中し、顧客のエクスペリエンスを向上させ、障害を回避することができます。

- さらに2023年1月、アリババクラウドは、さまざまな開発者向けツールやリソースの提供を強化することで、世界な開発者をサポートする新しいハブ「アプサラ開発者コミュニティ」の立ち上げを発表しました。これは、開発者コミュニティの継続的な成長をサポートすると同時に、新興国市場のデジタル経済のさらなる発展を促進することを目的としています。

アジア太平洋地域が大きな市場シェアを占める見込み

- 予測期間中、アジア太平洋地域が最も高い成長率を示すと予想されます。この地域におけるクラウドコンピューティングの急速な増加は、クラウドベースのアプリケーションデリバリコントローラの重要な推進力になると予想されます。

- さらに、この地域は中小企業の投資により成長が見込まれています。中小企業は、クラウドベースのアプリケーションのために、費用対効果の高いクラウドベースで技術的に高度なソリューションに投資しています。中国やインドなどの国々は、この地域に大きな成長機会をもたらしています。

- 例えば、中小企業省(Ministry of Micro, Small, and Medium Enterprises)の最近のデータによると、インドには5,000万社の中小企業があり、世界最大の中小企業市場のひとつとなっています。政府や中小企業が拡張性のあるITシステムやソリューションに依存していることを考えれば、彼らが機密情報とともにプロセスをクラウドに移行することは理解できます。このことが、アプリケーションリリース自動化市場をさらに大きく牽引しています。

- 最近のCOVID-19の発生を受け、アジア太平洋地域ではクラウドベースのソリューションの採用へと大きくシフトしており、アプリケーションリリース自動化業界は、さまざまなテクノロジー・プロバイダーからの支援を受けて回復力を見せています。コンタクトセンターのアウトソーシング先として重要なインドでは、リモート接続の支援が必要です。このような理由から、さまざまなベンダーが革新的なソリューションを提供し、顧客を惹きつけています。

- 例えば、シンガポールはアジア太平洋地域の医療とヘルスケアのハブと考えられており、地域最高のヘルスケアシステムを提供しています。国際合同委員会(JCI)はシンガポールの23以上の病院やヘルスケア施設を認定しています。毎年35万人以上の患者がシンガポールを訪れ、質の高いヘルスケア・サービスを提供しています。このような潜在力は、クラウド・アプリケーションの利用を増加させ、予測期間中の市場成長を促進すると思われます。

アプリケーションリリース自動化産業の概要

世界のアプリケーションリリース自動化市場は競争が激しく、複数の大手企業が存在します。市場シェアの面では、現在、少数の大手企業が市場を独占しています。市場で高いシェアを誇るこれらの大手企業は、海外における顧客基盤の拡大に注力しています。これらの企業は、市場シェアと収益性を高めるために、戦略的な共同イニシアティブを活用しています。

- 2023年3月-Applitools社は、製品デリバリーのライフサイクル全体でチームをつなぐために設計された新しいツール、Centraの早期アクセスプログラムの開始を発表しました。Centraは、製品デリバリーのライフサイクル全体にわたってチームをつなぎ、デザインから実装まで、あらゆるプロセス段階におけるユーザーインターフェースの追跡、検証、コラボレーションを可能にします。

- 2023年2月- ソフトウェアインテリジェンス企業のDynatraceは、AutomationEngineの発売を発表しました。この新しいDynatraceプラットフォームテクノロジーは、直感的なインターフェイスとノーコードおよびローコードツールセットを特長とし、Davis因果AIを活用して、無限のBizDevSecOpsワークフローにわたって回答駆動型自動化を拡張するチームを支援します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の業界への影響評価

第5章 市場力学

- 市場促進要因

- 運用リスクを低減したソフトウェアの迅速なデリバリーに対する需要の高まり

- 差別化された顧客体験の提供と顧客維持のための企業による急速な採用

- 市場抑制要因

- 製品コストの高さ、ソフトウェアやアプリケーションの導入失敗、設定の複雑さ

第6章 市場セグメンテーション

- コンポーネント別

- ツール

- サービス

- 展開別

- クラウド

- オンプレミス

- エンドユーザー産業別

- BFSI

- IT・通信

- 小売・eコマース

- メディア&エンターテイメント

- その他エンドユーザー産業

- 地域別

- 北米

- 欧州

- アジア太平洋

- 世界のその他の地域

第7章 競合情勢

- 企業プロファイル

- Broadcom Inc.

- IBM Corporation

- Microsoft Corporation

- BMC Software, Inc.

- Chef Software, Inc.

- CloudBees, Inc.

- Micro Focus International Plc

- ARCAD Software

- Attunity Ltd.

- Flexagon LLC

- Datical, Inc.

- Electric Cloud, Inc.

- CollabNet, Inc.

第8章 投資分析

第9章 市場機会と今後の動向

The Application Release Automation Market size is estimated at USD 4.89 billion in 2025, and is expected to reach USD 12.03 billion by 2030, at a CAGR of 19.75% during the forecast period (2025-2030).

Digital infrastructure has been significantly evolving globally along with business change, thereby making modernization the key to success. Moreover, with the emergence of the COVID-19 pandemic, application visibility and management gained even more prominence as employees working from their homes and businesses rapidly transformed their environments to keep their staff productive from any location. This was anticipated to further boost the market's growth over the forecast period. Moreover, due to the COVID-19 lockdowns that were put in place along with the switch to remote working environments, an unprecedented number of people started using mobile applications for work and other activities, creating the need for seamless security access to these applications.

Key Highlights

- Increasing adoption of digital transformation in most enterprises and investment in advanced technologies such as artificial intelligence, big data, and cognitive automation that can boost the company's revenue are some of the primary factors boosting the application release automation market.

- The growing digital transformation has pushed most businesses to adopt applications and tools to respond to market feedback and deliver new experiences to end users faster than ever. Organizations have turned to application release automation software to stay competitive in these new market conditions and speed up delivery. By leveraging application release automation, organizations can easily handle fast software delivery and updates and decrease human error, missed steps, and potential production issues.

- Additionally, the primary factor driving the market is increasing pressure on the IT sector to roll out new features to software applications quickly in production or apply security patches with little to no downtime to guarantee 100% uptime. Moreover, COVID-19 forced an unprecedented number of people worldwide to change their workplace from office to home, creating immense pressure on communications service providers to support a functioning society with flawless digital communication capabilities.

- In February 2023, Schneider Electric, the leader in the digital transformation of energy management and automation, launched its new Industrial Digital Transformation Services during the 27th Annual ARC Industry Leadership Forum in Orlando, Florida. The specialized global service is designed to help industrial enterprises achieve future-ready, innovative, sustainable, and effective end-to-end digital transformation.

Application Release Automation Market Trends

Cloud is Expected to Hold Significant Market Share

- As enterprises across the globe are migrating applications to the cloud at a rapid pace, there is a spike in demand for cloud-based applications in the global market. Moreover, according to a survey conducted by Apps Run The World, in 2021, Microsoft led as the top vendor in the cloud applications market share with 13%. Salesforce and Oracle were close behind, having 11% and 7% of the market share, respectively.

- Cloud-based applications and web servers not only help clients to access the applications with agility from anywhere across the globe, but it reduces the cost incurred due to downtime of businesses while using legacy systems.

- Traditional application release automation was used for load-balancing application servers to manage traffic and application deployment. Over the years, new functions have been integrated, including SSL offloading, visibility, application analytics, multi-cloud support, TCP optimizations, rate shaping, and web application firewalls.

- In June 2022, Armory, the continuous deployment (CD) company empowering development teams to easily, reliably, safely, and continuously deploy software at any scale, announced the general availability of Armory Continuous Deployment-as-a-Service. The product delivers declarative deployments across multiple environments that support advanced progressive strategies, allowing developers to focus on building great code rather than deploying it, enhancing their customers' experience, and avoiding outages.

- Further, in January 2023, Alibaba Cloud announced the launch of the Apsara Developer Community, a new hub created to support global developers through an enhanced provision of various developer tools and resources. It aims to support the developer community's continuous growth while facilitating the digital economy's further progress across markets.

Asia Pacific is Expected to Hold Significant Market Share

- Asia-Pacific is expected to witness the highest growth rate over the forecast period. The rapid increase in cloud computing in this region is expected to be a significant driver for cloud-based application delivery controllers.

- Additionally, the region is expected to witness growth, owing to the investments of small and medium organizations. SMEs are investing in cost-effective cloud-based and technologically advanced solutions for cloud-based applications. Countries such as China and India provide significant growth opportunities in the region.

- For instance, according to recent data from the Ministry of Micro, Small, and Medium Enterprises, India has 50 million MSMEs, which makes it among the world's largest MSME markets. Given that the government and MSMEs rely on scalable IT systems and solutions, it is understandable that they may shift their processes, along with sensitive information, to the cloud. This has further given significant traction to the application release automation market.

- In the wake of the recent outbreak of COVID-19, Asia-pacific is witnessing a significant shift toward adopting cloud-based solutions, and the application release automation industry is showing resiliency with support from various technology providers. India, a vital contact center outsourcing destination, needs help with remote connections, as regional enterprises need more technological capabilities for remote operations. Due to such reasons, various vendors offer innovative solutions to attract customers.

- For instance, Singapore is considered the Asia-Pacific's medical and healthcare hub and offers the region's best healthcare system. The Joint Commission International (JCI) has accredited over 23 hospitals and healthcare facilities in Singapore. Over 350,000 patients visit Singapore to provide high-quality healthcare services each year. Such potential would increase the use of cloud applications and drive market growth during the forecast period.

Application Release Automation Industry Overview

The global application release automation market is highly competitive and has several major players. In terms of market share, few of the major players currently dominate the market. These major players with prominent shares in the market are focusing on expanding their customer base across foreign countries. These companies leverage strategic collaborative initiatives to increase their market shares and profitability.

- March 2023 - Applitools announced the launch of an Early Access Program for Centra, a new tool designed to connect teams across the product delivery lifecycle. It is now available for free access; Centra connects teams across the product delivery lifecycle to track, validate, and collaborate on user interfaces at every process stage, from design to implementation.

- February 2023 - Software intelligence company Dynatrace announced the launch of the AutomationEngine. This new Dynatrace platform technology features an intuitive interface and no-code and low-code toolset and leverages Davis causal AI to empower teams to extend answer-driven automation across boundless BizDevSecOps workflows.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 On Increasing Demand of Faster Delivery of Software with Reduced Operational Risk

- 5.1.2 Rapid Adoption by Enterprise to Deliver Differentiated Customer Experiences and to Retain

- 5.2 Market Restraints

- 5.2.1 High Cost of Product and Failed Deployment of Software or Applications and Complexity in Configurations

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Tool

- 6.1.2 Services

- 6.2 By Deployment

- 6.2.1 Cloud

- 6.2.2 On-Premises

- 6.3 By End-User Industries

- 6.3.1 BFSI

- 6.3.2 IT & Telecommunications

- 6.3.3 Retail & E-commerce

- 6.3.4 Media & Entertainment

- 6.3.5 Others End-User Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Broadcom Inc.

- 7.1.2 IBM Corporation

- 7.1.3 Microsoft Corporation

- 7.1.4 BMC Software, Inc.

- 7.1.5 Chef Software, Inc.

- 7.1.6 CloudBees, Inc.

- 7.1.7 Micro Focus International Plc

- 7.1.8 ARCAD Software

- 7.1.9 Attunity Ltd.

- 7.1.10 Flexagon LLC

- 7.1.11 Datical, Inc.

- 7.1.12 Electric Cloud, Inc.

- 7.1.13 CollabNet, Inc.