|

市場調査レポート

商品コード

1433942

家禽用飼料:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Poultry Feed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 家禽用飼料:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

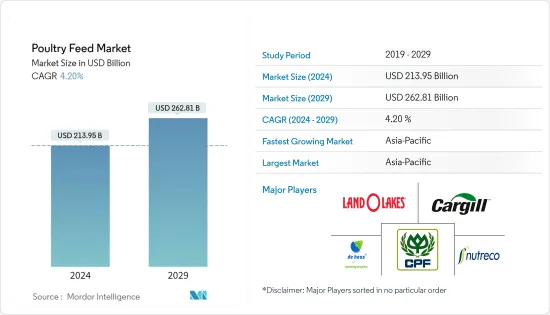

家禽用飼料市場の規模は、2024年に2,139億5,000万米ドルと推定され、2029年までに2,628億1,000万米ドルに達すると予想されており、予測期間(2024年から2029年)中に4.20%のCAGRで成長します。

主なハイライト

- 世界の人口が増加し、ファストフードレストランのさまざまな分野で家禽肉の需要が高まっているため、世界中の家禽生産者は消費者の需要に応えるために生産を強化しています。 EU農業農村開発局の報告書によると、家禽肉の消費量は2030年までに1万2,443トンに達すると推定されています。これは、家禽肉が消費者によって安価で健康的で持続可能な製品の選択肢であると考えられているためです。したがって、健康的で栄養価の高い家禽肉の生産需要の増加が市場の成長を促進すると予想されます。

- 家禽肉製品の需要の急速な増加が市場を牽引する主な要因です。卵や肉などの家禽製品の需要が常に増加しているため、家禽は最も経済的なタンパク質源の1つと考えられています。さらに、アジア太平洋地域における消費者の収入の増加と都市化の進行により、鶏肉製品の需要が増加しています。それはひいては調査対象市場の成長につながります。

- 2021年のオールテック飼料調査によると、動物の種類別の飼料生産のうち、ボイラーが総飼料生産量の28%を占め、層が総飼料生産量の14%を占めました。調査では、家禽種の中でブロイラーが主に成長している分野であることが示されました。したがって、飼料生産の増加は、予測期間中の市場の成長を促進します。

- 家禽拡大プロジェクトの増加により、市場の成長がさらに促進されています。たとえば、2021年4月、アーカンソー州のTyson Poultryグループは、鶏肉の生産能力を増強し、急速に急増する鶏肉の需要に対応するために4,800万米ドルを投資しました。家禽拡大への投資の増加は、家禽用飼料部門の成長の機会としてさらに機能しています。

- 飼料製品の品質と価格は、市場の成長における最も顕著な要因として浮上しています。政府は飼料の重要性を認識し、飼料の品質を維持し、動物の健康を守るためにさまざまな規制を課しています。したがって、家禽肉の需要の増加、消費者所得の増加、都市化、家禽生産投資の増加が、予測期間中の市場の成長を促進しています。

家禽用飼料市場の動向

鶏肉製品の需要の高まり

最近、家禽は農業分野で最も急速に成長している分野の1つです。家禽部門は、現代の集約的生産方法のイントロダクション、遺伝子改良、予防的疾病管理とバイオセキュリティ対策の改善、収入と人口の増加、都市化により、過去20年間に大きな構造変化を経験しました。家禽肉消費量の増加は、東アジア、東南アジア、ラテンアメリカ、特に中国とブラジルで最も顕著です。世界の家禽肉のうち新興諸国で消費される割合は過去10年間で増加しました。新興諸国における家禽肉の生産と消費は、所得の増加、食生活の多様化、市場の拡大により、年間3.6%増加すると推定されています。 OCED農業見通し2020年版によると、世界中の家禽肉の一人当たり消費量は2017年の13.86kgから2020年には13.92kgに増加しました。

スーパーマーケットやショッピングモールの出現が、冷蔵・冷凍鶏肉製品小売業の成長を支えています。さらに、政府の政策により競争力のある価格の製品供給が確保され、家禽部門の成長が促進されています。労働人口と所得の増加により、便利で高品質な鶏肉製品の需要は増え続けています。健康意識の高まりにより、消費者は健康的な肉製品により多くのお金を費やす傾向があり、市場の成長にさらに貢献しています。

さらに、マクドナルド、KFC、ナンドス、マリーブラウン、その他さまざまな店舗などの急速に成長しているファストフードレストランからの家禽肉の需要が家禽部門の成長を促進し、それが市場開拓をもたらしています。たとえば、農務省によると、2018年の鶏肉生産量は9,272万6,000トンで、約7.9%増加し、2020年には10万26トンに達しました。

消費者の需要の増加に対応するには家禽の生産量を増やす必要があり、そのためには生産効率、飼料転換率を改善し、動物の健康を向上させるために高品質の飼料を最適に使用する必要があります。予測期間中に市場を押し上げると予想されます。

アジア太平洋が市場を独占

アジア太平洋は家禽用飼料の最大の市場です。膨大な人口と可処分所得の増加により、アジア太平洋地域で最も速い速度で市場が成長する可能性があります。中国とインドの家禽部門は、過去20年にわたり、家禽の頭数と1羽あたりの生産量の点で急速な成長を遂げました。より高い生産レベルは、食品変換率が高い集約システムの普及に関連しています。

中国では鶏肉に対する強い需要があるため、飼料の使用が増加しています。食糧農業機関(FAO)によると、鶏肉の生産量は2017年の1,437万3,315トンから2020年には1,582万3,712トンまで増加しました。さらに、養鶏業界は回復と再入荷を支援する政府の奨励金からも恩恵を受けています。さらに、中国の大手ブロイラー企業数社が新しいブロイラー建設プロジェクトに投資し、2020年の総投資額は最大74億元(10億米ドル)に達しました。

同様に、一人当たりの収入の増加、インドでのクイックサービスレストランの拡大、高品質の家禽製品に対する需要の高まりが、インドの家禽用飼料の需要の増加に大きく貢献しています。これにより、将来的には国内の家禽用飼料の販売が加速する可能性が高いです。したがって、中国やインドなどのアジア太平洋地域の新興経済国では、家禽用飼料の必要性が引き続き高いです。これは、家禽の個体数を増やすために高品質の飼料の使用を増やすことにつながります。また、世界の家禽肉生産量は増加しており、増加分の3分の2がアジア太平洋で発生しています。

家禽用飼料業界の概要

家禽用飼料市場は非常に細分化されています。 Charoen Pokphand Foods、Cargill Inc.、Nutreco NV、Land O'Lakes Inc.、De Heus BVなどは、市場で活動している主要企業です。プレーヤーは、新製品や即興の製品、提携、拡張、事業拡大のための買収に投資しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 動物タイプ

- レイヤー

- ブロイラー

- ターキー

- その他の動物

- 原料タイプ

- 穀類

- 油糧ミール

- 糖蜜

- 魚油と魚粉

- サプリメント

- その他の原料タイプ

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- スペイン

- 英国

- フランス

- ドイツ

- ロシア

- イタリア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- その他中東とアフリカ

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- Charoen Pokphand Foods

- Cargill Inc.

- Alltech Inc.

- Archer Daniels Midland

- De Heus BV

- Land O Lakes Inc.

- ForFarmers

- Nutreco N.V.

- Kent Nutrition Group

第7章 市場機会と今後の動向

The Poultry Feed Market size is estimated at USD 213.95 billion in 2024, and is expected to reach USD 262.81 billion by 2029, growing at a CAGR of 4.20% during the forecast period (2024-2029).

Key Highlights

- With the increasing global population and rising demand for poultry meat across various sectors of fast-food restaurants, poultry producers across the world are ramping up their production to meet consumer demands. According to a report by the EU Agricultural and Rural Development, the consumption of poultry meat is estimated to reach 12,443.0 metric tons by 2030 because poultry is considered a cheap, healthy, and sustainable product option by consumers. Therefore, the increased production demand for healthy and nutritious poultry meat is anticipated to propel market growth.

- The rapidly increasing demand for poultry meat products is the primary factor driving the market. Poultry is considered one of the most economical sources of protein, owing to which poultry products such as eggs and meat consistently witness growth in demand. Furthermore, the rising incomes of consumers and increasing urbanization in the Asia-Pacific region are leading to increased demand for poultry products. It, in turn, is leading to the growth of the market studied.

- According to the Alltech feed survey in 2021, among feed production by animal type, the boilers accounted for 28% of total feed production, while the layers accounted for 14% of the total feed production. The survey indicated that broilers are a predominantly growing sector in the poultry species. Thus, the growing feed production is bolstering the market's growth during the forecast period.

- The increasing poultry expansion projects are further aiding the growth of the market. For instance, in April 2021, Tyson Poultry group in Arkansas invested USD 48 million to increase the poultry production capacity and meet the rapidly soaring chicken demand. The increasing investment in poultry expansion is further serving as an opportunity for the poultry feed sector growth.

- Quality and the price of feed products are emerging as the most prominent factors in the market growth. The governments are imposing various regulations to maintain the feed quality and safeguard animal health, recognizing its importance. Thus, the increasing demand for poultry meat, growing consumer income, urbanization, and rising poultry production investments are bolstering the market's growth during the forecast period.

Poultry Feed Market Trends

Rising Demand for Poultry Products

Recently, poultry is one of the fastest-growing segments of the agricultural sector. The poultry sector underwent significant structural changes during the past two decades due to modern intensive production methods introduction, genetic improvements, improved preventive disease control and biosecurity measures, increasing income and human population, and urbanization. The increase in poultry meat consumption is most evident in East and Southeast Asia and Latin America, particularly in China and Brazil. The share of the world's poultry meat consumed in developing countries increased over the past decade. It is estimated that poultry meat production and consumption in developing countries will increase by 3.6% per annum due to rising incomes, diet diversification, and expanding markets. According to OCED Agricultural Outlook, 2020, the per capita consumption of poultry meat worldwide increased from 13.86 kg in 2017 to 13.92 kg in 2020.

Supermarkets and shopping malls' emergence support chilled and frozen poultry product retailing growth. In addition, government policies ensure competitively priced product supply, boosting the poultry sector growth. Due to the increasing working population and incomes, the demand for convenient, high-quality chicken products is continually increasing. With increased health awareness, consumers are willing to spend more on healthy meat products, further contributing to the market's growth.

Furthermore, the demand for poultry meat from rapidly growing fast-food restaurants, such as McDonald's, KFC, Nando's, Marrybrown, and various other outlets, is fueling the poultry sector growth, which is, in turn, resulting in market development. For instance, according to USDA, chicken meat production in 2018 was 92,726 thousand metric tons which increased by approximately 7.9% and reached 100,026 metric tons in 2020.

Poultry production must increase to keep up with the increasing consumer demand, which requires optimum use of high-quality feed to improve production efficiency, feed conversion ratios and enhance animal health. It is anticipated to boost the market during the forecast period.

Asia-Pacific Dominates the Market

Asia-Pacific is the largest market for poultry feed. A vast population and growing disposable incomes are likely to trigger market growth at the fastest rate in the Asia Pacific. The poultry sector in China and India experienced vigorous growth over the past two decades in terms of poultry numbers and the level of output per bird. Higher production levels are associated with the spread of intensive systems in which food conversion ratios are high.

Feed use in China is growing due to the country's strong demand for chicken meat. The production of chicken meat increased from 14,373,315 metric tons in 2017 to 15,823,712 metric tons in 2020, according to the Food and Agriculture Organization (FAO). Further, the poultry industry is also benefiting from government incentives to support recovery and restocking. Additionally, several leading broiler enterprises in China invested in new broiler construction projects, with a total investment of up to RMB 7.4 billion (USD 1 billion) in 2020.

Likewise, increasing per capita income, expansion of quick-service restaurants in India, and growing demand for quality poultry products have significantly contributed to the rising demand for poultry feed in India. It will likely accelerate poultry feed sales in the country in the future. Hence, the need for poultry feed continues to be high in emerging economies of Asia-Pacific in countries like China and India. It leads to increasing quality feed use for a higher poultry population. Also, global poultry meat production is growing, with two-thirds of the increase in Asia-Pacific.

Poultry Feed Industry Overview

The Poultry Feed Market is highly fragmented. Charoen Pokphand Foods, Cargill Inc., Nutreco NV, Land O'Lakes Inc., and De Heus BV are some major players operating in the market. The players are investing in new products and improvisation of products, partnerships, expansions, and acquisitions for business expansions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Animal Type

- 5.1.1 Layers

- 5.1.2 Broilers

- 5.1.3 Turkey

- 5.1.4 Other Animal Type

- 5.2 Ingredient Type

- 5.2.1 Cereal

- 5.2.2 Oilseed Meal

- 5.2.3 Molasses

- 5.2.4 Fish Oil and Fish Meal

- 5.2.5 Supplements

- 5.2.6 Other Ingredient Type

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Spain

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Germany

- 5.3.2.5 Russia

- 5.3.2.6 Italy

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle east and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle east and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Charoen Pokphand Foods

- 6.3.2 Cargill Inc.

- 6.3.3 Alltech Inc.

- 6.3.4 Archer Daniels Midland

- 6.3.5 De Heus BV

- 6.3.6 Land O Lakes Inc.

- 6.3.7 ForFarmers

- 6.3.8 Nutreco N.V.

- 6.3.9 Kent Nutrition Group