|

市場調査レポート

商品コード

1433502

STD診断:世界市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Global STD Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| STD診断:世界市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 113 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

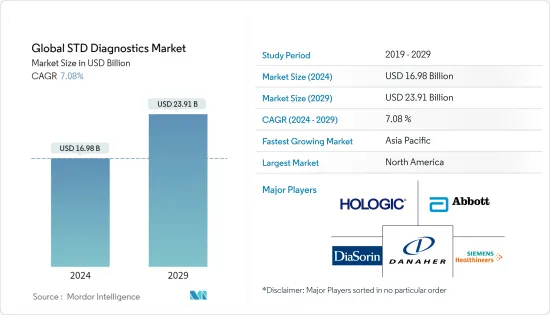

世界のSTD診断の市場規模は、2024年に169億8,000万米ドルと推定され、2029年までに239億1,000万米ドルに達すると予測されており、予測期間(2024年~2029年)中に7.08%のCAGRで成長する見込みです。

COVID-19パンデミックは、性感染症の診断に大きな影響を与えると予想されています。ペンシルベニア州立大学の研究者らが2021年に発表した「Quest Diagnostics 2020 Health動向」によると、COVID-19のパンデミック中に淋病やクラミジアなどの病気のスクリーニング率が低下し、週ごとの陽性率が上昇したといいます。研究者らは、COVID-19パンデミックの初期の数か月間で、性感染症の検査とスクリーニングが男性で63%、女性で59%減少したことを発見しました。研究者らはまた、2020年2月下旬から2020年4月上旬の間にSTI検査が40%も減少したことも発見しました。したがって、ロックダウンや検査施設へのアクセス不足による検査の減少は、STD診断断市場に影響を与える可能性があります。

世界のSTDの蔓延の増加、教育キャンペーンによる患者の意識の向上、政府の取り組みの拡大が市場の成長を促進すると予想されます。世界保健機関が2021年11月に発表した報告書では、世界で100万人以上の性感染症が感染しており、そのほとんどが無症状であると報告しています。また、淋病、クラミジア、トリコモナス症、梅毒という性感染症の4つのうち1つで、毎年推定3億7,400万人が新たに感染していると報告しました。したがって、世界中で性感染症の有病率と発生率がこのように増加しているため、STD診断の需要が増加し、それによって予測期間中に市場の成長が推進されると予想されます。

さらに、HIVは依然として世界的に主要な公衆衛生問題です。スクリーニングの目的は、一見健康に見える集団の中で、健康上の問題や健康状態のリスクが高い人々を特定し、早期の治療や介入を提供して、集団内の発生率と死亡率を減らすことです。たとえば、2022年3月に英国で全国クラミジアスクリーニングプログラム(NCSP)が組織されました。このプログラムの主な目的は、未治療のクラミジア感染のリスクを軽減することです。このプログラムは、検査結果と治療、および治療後の再検査までの時間を短縮することにも重点を置いています。また、このプログラムは、予防と制御から、主に女性と女児を検査することによって未治療のクラミジア感染による害を軽減することに焦点を当てたものに変更されています。さらに、2022年6月、疾病管理予防センターは、性感染症のスクリーニングプログラムと世界中で増大する性感染症の負担に対する意識を高めるために、性感染症のスクリーニングに関するガイドラインを推奨および発行しました。女性、妊婦、女性とセックスする男性、男性とセックスする男性、トランスジェンダーおよび性別の多様性のある人、HIV感染者など、人口のあらゆるグループに対して個別のSTDスクリーニングガイドラインを発行しています。そのため、世界中でスクリーニングプログラムの数が増加すると、性感染症の症例数が増加すると予想され、その結果、STD診断製品の需要が増加すると予想されます。したがって、予測期間中にかなりの市場の成長が予想されます。

さらに、STD診断の進歩と新技術開発の研究開発が市場の成長を促進すると予測されています。また、市場では、従来の技術から性感染症の診断のための分子診断への大きな移行が見られており、市場の成長にとって大きな進歩です。

したがって、前述のすべての要因が調査対象の市場の成長を促進すると予想されます。

STD診断市場の動向

臨床検査部門は予測期間中に成長が見込まれる

臨床検査は、世界中で性感染症(STD)の最も一般的な診断方法です。臨床検査は信頼性が高く、精度が高いため、その使用率は高く、人々は臨床検査をより信頼する傾向があります。

アボット研究所は、クラミジア・トラコマチス、膣トリコモナス、マイコプラズマ・ジェニタリウムによって引き起こされる淋病などのさまざまな性感染症を検出するための、インビトロ逆転写ポリメラーゼ連鎖反応(RT-PCR)アッセイおよびインビトロポリメラーゼ連鎖反応(PCR)アッセイを提供しています。同様に、Qiagen Inc.は、臨床感度と特異性が高く、さまざまな性感染症の検出に使用される、クラミジア・トラコマチス(CT)および淋菌(NG)感染を検出するためのSTI検査など、幅広い診断検査キットを提供しています。

さらに、臨床検査部門の成長を担う主要な要因の1つである分子診断の分野では、継続的な製品の発売が行われています。より多くの製品の発売により、研究室は必要に応じて機器や設備を設置できるようになりました。

たとえば、2022年5月に、Qiagen Inc.は、単純ヘルペスウイルス 1型(HSV-1)DNAおよび/または単純ヘルペスウイルス 2型(HSV-2)の定量と識別のためのNeuMoDxHSV 1/2 Quant Assayを、欧州委員会からの承認を得て発売しました。このアッセイの登場により、同社は臨床検査における製品ポートフォリオを拡大することができ、最終的には革新的な検査による市場の成長に貢献します。さらに、2021年11月にRocheは、新しい分子実験装置であるリアルタイムPCR分子検査ソリューションであるCobas 5800システムをCEマークを受け入れている国で発売しました。この発売は、調査対象市場の成長に貢献すると予想されるSTD診断を含む、同社の診断製品範囲をさまざまな用途に拡大するのに役立っています。

したがって、上記の要因により、臨床検査セグメントは予測期間中に高い成長を遂げると考えられています。

北米は世界のSTD診断市場で最大のシェアを保持

世界のSTD診断断市場は、この地域でのSTDの蔓延率の高さにより、北米が独占しています。米国は、多数の診断会社が存在し、病気に対する意識が高まっているため、北米地域で最大の市場になると予想されています。 2022年4月、疾病管理予防センター(CDC)が発行した「2020年性感染症サーベイランス」と題した報告書では、STDが依然として国内の公衆衛生上の重大な懸念事項であると述べられています。同じ情報源によると、クラミジア・トラコマチス感染症は、2020年に米国で最も蔓延した届出対象の性感染症で、合計157万9,885件の症例がCDCに報告されました。 CDCは2020年に67万7,769件の異なる淋病感染症の報告を受けました。2020年には、最も感染力の強い一次および二次(P&S)期の4万1,655件を含む、全段階を通じて13万3,945件の梅毒が発生しました。このような病気の診断プロセスの需要を高めることにより、STDの蔓延に伴いこの国の市場の成長も拡大すると予想されます。

同様に、CDCは2022年5月、2020年に米国およびその属領の30,635人がHIV診断を受けたと報告しました。この報告書は「2020年米国および属領におけるHIV感染症の診断」と題されていました。 2019年末時点で、HIVとともに生きるアメリカ人の数は118万9,700人と予測されていました。患者が健康で長生きするには早期診断が不可欠であるため、HIVの蔓延により病気の診断の需要が高まると予測されています。

2020年8月、米国保健福祉省は性感染症国家戦略計画(STI計画)を策定しました。このビジョンの横には、STI計画のより正確な目標を構成する5つのハイレベルな目標が示されています。新たな性感染症の予防は、5つの目的および関連する目的の1つです。性感染症の影響を最も受けている地域社会や集団において、スクリーニング、ケア、治療を含む、高品質で安価な性感染症二次予防へのアクセスを増やします。新規および新興疾患の脅威を含む性感染症を特定して治療するために、革新的なSTD診断ツール、治療薬、その他の介入の開発と導入を支援します。したがって、このような措置により市場の拡大が加速すると予想されます。

さらに、2021年5月、ジョンズ・ホプキンス大学率いるチームは、淋病を迅速に診断し、特定の株が最前線の治療に反応するかどうかを評価するための低コストのポータブルデバイスとスマートフォンアプリを開発しました。この技術革新は、病院や診療所で使用されている現在の検査方法を改善したもので、検査結果が判明するまでに最大1週間かかる場合があり、その間に個人が意図せず病気を広めてしまう可能性があります。さらに、2021年3月には、NASTAD(National Alliance of State &Territorial AIDS Director)がBuilding Healthy Online Communitiesと提携し、TakeMeHomeと呼ばれる無料のHIVおよびSTD検査キット宅配プログラムを開始しました。

したがって、上記の要因により、北米のSTD診断市場の成長は予測期間中に急成長すると予想されます。

STD診断業界の概要

STD診断市場は本質的に適度な競争が存在します。 STD診断市場の主要企業は、Abbott Laboratories、MedMira Inc、Qaigen Inc、Cepheid(Danaher Corporation)、F. Hoffmann-La Roche AG、Diasorin SpA、bioMeriuex、Hologic, Inc、Bio-Rad Laboratories, Inc.などです。これらの企業は、STD診断断業界におけるパートナーシップおよび製品/技術ライセンシングの機会に重点を置いています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- STD罹患率と有病率の増加

- 国家スクリーニングプログラムの実施

- STD診断薬の開発における技術革新の進展

- 市場抑制要因

- 患者がSTD専門クリニックを訪れることに伴う社会的不名誉

- 製品承認のための厳しい規制シナリオ

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響

第5章 市場セグメンテーション

- 疾患タイプ別

- クラミジア

- 淋病

- 梅毒

- 性器ヘルペス

- B型肝炎

- HIV/AIDS(ヒト免疫不全ウイルス感染症および後天性免疫不全症候群)

- ヒトパピローマウイルス(HPV)

- その他の疾患

- 診断検査場所別

- ラボ検査

- ポイントオブケア(PoC)検査

- 機器別

- ラボ用機器

- サーマルサイクラー-PCR

- ラテラルフローリーダーイムノクロマトアッセイ

- フローサイトメーター

- 吸光度マイクロプレートリーダー- 酵素結合免疫吸着測定法(ELISA)

- その他の検査機器

- ポイントオブケア(PoC)機器

- フォンチップ(マイクロ流体+ICT)

- ポータブル/ベンチトップ/迅速診断キット

- ラボ用機器

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Siemens Healthcare GmbH

- Abbott Laboratories

- MedMira Inc

- Qiagen Inc

- Danaher Corporation(Cephied)

- F. Hoffmann-La Roche AG

- Diasorin S.p.A

- BioMeriuex

- Hologic, Inc

- Bio-Rad Laboratories, Inc.

- Becton Dickinson and company

- Thermo Fisher Corporation(Affymetrix)

第7章 市場機会と今後の動向

The Global STD Diagnostics Market size is estimated at USD 16.98 billion in 2024, and is expected to reach USD 23.91 billion by 2029, growing at a CAGR of 7.08% during the forecast period (2024-2029).

The COVID-19 pandemic is expected to have a significant impact on sexually transmitted disease diagnostics. According to the Quest Diagnostics 2020 Health Trends, published by researchers from Penn State University in 2021, screening rates for diseases like gonorrhea and chlamydia went down during the COVID-19 pandemic and the weekly positivity rates increased. The researchers found out that testing and screening for sexually transmitted infections had decreased by 63% for men and 59% for women during the early months of the Covid-19 pandemic. The researchers also found out that STI testing decreased between late February 2020 to early April 2020 by as much as 40%. Thus, the decrease in testing, due to lockdowns and lack of access to testing facilities might have an impact on the STD diagnostics market.

The growing prevalence of STDs globally, increase in patient awareness through education campaigns, and growing government initiatives are anticipated to drive market growth. The report published by the World Health Organization in November 2021, reported that more than 1.0 million sexually transmitted infections are acquired globally and most of them are asymptomatic. It also reported that every year there are an estimated 374.0 million new infections with 1 out of 4 sexually transmitted infections: gonorrhea, chlamydia, trichomoniasis, and syphilis. Therefore, such an increasing prevalence and incidence rate of sexually transmitted diseases across the globe is expected to increase the demand for STD diagnostics, thereby propelling the market growth over the forecast period.

Furthermore, HIV continues to be a major public health issue, globally. The purpose of screening is to identify people in an apparently healthy population who are at higher risk of a health problem or a condition so that an early treatment or intervention can be provided and thereby reduce the incidence and mortality rate within the population. For instance, in March 2022, National Chlamydia Screening Program (NCSP) was organized in the United Kingdom. The main aim of the program is to reduce the risk of untreated chlamydia infection. This program also focused on reducing the time to test results and treatment and re-testing after treatment. The program is also changing from prevention and control to focusing on reducing the harms from untreated chlamydia infection by primarily screening women and girls. Additionally, in June 2022, the Centers for Disease Control and Prevention recommended and issued guidelines for screening of sexually transmitted diseases in order to create awareness towards screening programs for STDs and increasing burden of STDs across the globe. It has issued separate STD screening guidelines for every group of the population such as women, pregnant women, men who have sex with women, men who have sex with men, transgender and gender diverse persons, and persons with HIV. Thus, the increase in the number of screening programs across the globe is expected to increase the number of cases of sexually transmitted diseases, which in turn is anticipated to increase the demand for STD diagnostic products. Hence, considerable market growth is expected over the forecast period.

Additionally, advancements in STD diagnostics and research and development in developing new technologies are projected to fuel the market growth. Also, the market is witnessing a major shift from conventional technologies to molecular diagnostics for the diagnosis of STD's is the major breakthrough for the growth of the market.

Hence, all the aforementioned factors are expected to drive the growth of the market studied.

STD Diagnostics Market Trends

Laboratory Testing Segment is Expected to Witness Growth Over the Forecast Period

Laboratory tests are the most common form of diagnosis of Sexually Transmitted Diseases (STDs) across the globe. As laboratory tests are reliable and provide high accuracy, their usage is high and people tend to trust more on laboratory tests.

Abbott laboratories offer an in vitro reverse transcription-polymerase chain reaction (RT-PCR) assay and in vitro polymerase chain reaction (PCR) assay for detection of various sexually transmitted diseases such as gonorrhea and others caused by Chlamydia trachomatis, Trichomonas vaginalis, and Mycoplasma genitalium. Similarly, Qiagen Inc. offers a wide range of diagnostics test kits, including STI tests for detection of Chlamydia trachomatis (CT) and Neisseria gonorrhoeae (NG) infections with high clinical sensitivity and specificity, that are used to detect various sexually transmitted diseases.

Moreover, there have been continuous product launches occurring in the field of molecular diagnostics which is one of the leading factors responsible for the growth of the laboratory testing segment. More product launches are allowing laboratories to install instruments or equipment as per the need.

For instance, in May 2022, Qiagen Inc. launched NeuMoDxHSV 1/2 Quant Assay for the quantification and differentiation of herpes simplex virus type 1 (HSV-1) DNA and/or herpes simplex virus type 2 (HSV-2) with approval from the European Commission. The emergence of this assay is allowing the company to expand its product portfolio in laboratory testing which ultimately helps the market growth owing to the innovative tests. Additionally, in November 2021, Roche launched Cobas 5800 System, a real-time PCR molecular testing solution, a new molecular laboratory instrument, in countries accepting the CE mark. This launch is helping the company in broadening its diagnostics product range for various applications including STD diagnostics which is expected to contribute to the growth of the market studied.

Therefore, owing to the above-mentioned factors, the laboratory testing segment is believed to witness high growth over the forecast period.

North America holds largest share in Global STD Diagnostics Market

The global sexually transmitted diseases diagnostics market is dominated by North America, owing to the high prevalence of STDs in the region. The United States is expected to be the largest market in the North American region due to the presence of a large number of diagnostic companies and greater disease awareness. In April 2022, a report published by the Centers for Disease Control and Prevention (CDC) titled "Sexually Transmitted Disease Surveillance, 2020" stated that STDs remain a significant public health concern in the country. According to the same source, Chlamydia trachomatis infection was the most prevalent notifiable sexually transmitted infection in the United States in 2020 with a total of 1,579,885 cases reported to the CDC. The CDC received reports of 677,769 different gonorrhea infections in 2020. 2020 saw 133,945 cases of syphilis throughout all phases, including 41,655 cases of the disease's primary and secondary (P&S) stages, which are the most contagious. By raising the demand for such diseases' diagnostic processes, the country's market growth is thus anticipated to expand with the prevalence of STDs.

Similarly, the CDC reported in May 2022 that 30,635 people in the United States and dependent territories acquired an HIV diagnosis in 2020. The report was titled "Diagnoses of HIV Infection in the United States and Dependent Areas, 2020." At the end of 2019, the number of Americans living with HIV was predicted to be 1,189,700. Because early diagnosis is essential for the patient to live a long and healthy life, it is therefore projected that the prevalence of HIV will boost the demand for illness diagnostics.

In August 2020, the United States Department of Health and Human Services developed a Sexually Transmitted Infections National Strategic Plan (STI Plan). Five high-level goals that frame the STI Plan's more precise targets are presented beside this vision. The prevention of new STIs is one of the five aims and related objectives. In communities and populations most affected by STIs, increase access to high-quality, inexpensive STI secondary prevention, including screening, care, and treatment. To identify and treat STIs, including novel and emerging disease threats, support the development and adoption of innovative STI diagnostic tools, therapeutic agents, and other interventions. Thus, it is anticipated that such measures will accelerate market expansion.

Moreover, in May 2021, a team led by Johns Hopkins University developed a low-cost portable device and smartphone app to quickly diagnose gonorrhea and evaluate whether a specific strain will respond to frontline treatments. The innovation is an improvement over current testing methods used in hospitals and clinics, which can take up to a week to give findings and during which individuals may unintentionally spread illnesses. Furthermore, in March 2021, NASTAD (National Alliance of State & Territorial AIDS Directors) partnered with Building Healthy Online Communities for a free HIV and STD test kit home delivery program called TakeMeHome.

Therefore, owing to the above factors, the growth of the STD diagnostics market in North America is expected to surge over the forecast period.

STD Diagnostics Industry Overview

The market for STD Diagnostics is moderately competitive in nature. Key players in the STD diagnostics market are Abbott Laboratories, MedMira Inc, Qaigen Inc, Cepheid (Danaher Corporation), F. Hoffmann-La Roche AG, Diasorin S.p.A, bioMeriuex, Hologic, Inc, Bio-Rad Laboratories, Inc., amongst others. These companies focus on partnership and product/technology licensing opportunities in the sexually transmitted diseases diagnostics industry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Incidence and Prevalence Rates of STD

- 4.2.2 Implementation of National Screening Programs

- 4.2.3 Growing Innovations in the Development of STD Diagnostics

- 4.3 Market Restraints

- 4.3.1 Social Stigma Associated With Patients Visiting Specialized STD Clinics.

- 4.3.2 Stringent Regulatory Scenario for product approvals

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Impact Of Covid-19 On The Market

5 MARKET SEGMENTATION

- 5.1 By Type of Disease

- 5.1.1 Chlamydia

- 5.1.2 Gonorrhea

- 5.1.3 Syphilis

- 5.1.4 Genital herpes

- 5.1.5 Hepatitis B

- 5.1.6 HIV/AIDS (Human immunodeficiency virus infection and acquired immune deficiency syndrome)

- 5.1.7 Human papillomavirus (HPV)

- 5.1.8 Other Diseases

- 5.2 By Location of Diagnostic Test

- 5.2.1 Laboratory Testing

- 5.2.2 Point Of Care (PoC) Testing

- 5.3 By Devices

- 5.3.1 Laboratory Devices

- 5.3.1.1 Thermal Cyclers - PCR

- 5.3.1.2 Lateral Flow Readers Immunochromatographic Assays

- 5.3.1.3 Flow Cytometers

- 5.3.1.4 Absorbance Microplate Reader - Enzyme Linked Immunosorbent Assay (ELISA)

- 5.3.1.5 Other Laboratory Devices

- 5.3.2 Point Of Care (PoC) Devices

- 5.3.2.1 Phone Chips (Microfluidics + ICT)

- 5.3.2.2 Portable/Bench Top/Rapid Diagnostic Kits

- 5.3.1 Laboratory Devices

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle-East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle-East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Siemens Healthcare GmbH

- 6.1.2 Abbott Laboratories

- 6.1.3 MedMira Inc

- 6.1.4 Qiagen Inc

- 6.1.5 Danaher Corporation (Cephied)

- 6.1.6 F. Hoffmann-La Roche AG

- 6.1.7 Diasorin S.p.A

- 6.1.8 BioMeriuex

- 6.1.9 Hologic, Inc

- 6.1.10 Bio-Rad Laboratories, Inc.

- 6.1.11 Becton Dickinson and company

- 6.1.12 Thermo Fisher Corporation (Affymetrix )