|

市場調査レポート

商品コード

1433013

倉庫用燻蒸剤:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Warehouse Fumigants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 倉庫用燻蒸剤:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 132 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

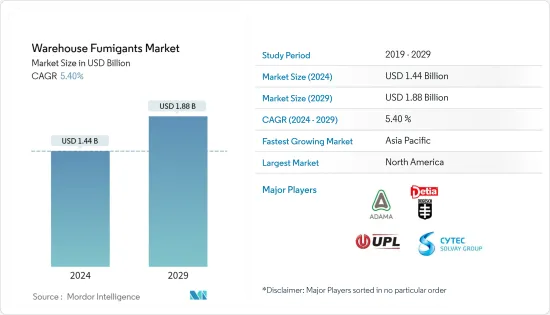

倉庫用燻蒸剤の市場規模は、2024年に14億4,000万米ドルと推定され、2029年までには18億8,000万米ドルに達すると予測され、予測期間中(2024年~2029年)にCAGR5.40%で成長する見込みです。

2018年、北米は調査対象市場の最大の地域セグメントであり、世界市場の約33.8%のシェアを占めました。タイプ別では、ホスフィンベースの燻蒸剤製品セグメントが2018年に26.3%の最大市場シェアを占め、予測期間中も最も急成長するセグメントであり続けると予測されています。

アジア太平洋は、倉庫用燻蒸剤市場においてまだ最大の潜在力を発揮していない地域とされています。この市場を牽引しているのは、この分野における急速な技術進歩、ポストハーベスト・ロスに対する懸念の高まり、収穫量の増加につながった先進的農法の転換など、いくつかの要因です。植物への燻蒸剤の導入は、病害を根から遠ざけ、より良い収量を生み出すのに役立ちます。

倉庫用燻蒸剤の市場動向

害虫駆除のニーズの増加

害虫駆除業界では、穀物の安全な貯蔵と流通に対する最大の自然脅威は昆虫の侵入です。しかし、害虫駆除には、構造物や倉庫の燻蒸に比べ、燻蒸のようなツールが効果的であり、より効果的です。気温の上昇などの気候変動により、昆虫の個体数は今後増加し、燻蒸剤の使用への依存度が高まることが予想されます。日用品や輸出資材の害虫を駆除するために、燻蒸は一般的な方法のひとつであり、新興国全体で広く採用されています。世界的には、ホスフィンと臭化メチルの2つが一般的な燻蒸剤であり、貯蔵製品の保護に使用されています。

北米が世界市場を独占

北米は、2018年に33.8%のシェアで世界の倉庫用燻蒸剤消費に大きく貢献しており、米国とカナダが地域市場の約80%を占めています。北米は農業用燻蒸剤の主要市場であり、米国とカナダの主要国では250以上の認可製品が販売されています。この地域で燻蒸剤を倉庫と土壌の両方に使用している主な品目は、トウモロコシ、米、大麦、ジャガイモ、トマト、小麦、イチゴ、キャベツなどです。キューバ、ドミニカ共和国、コスタリカ、ジャマイカなどの輸出と貯蔵能力が非常に低いため、倉庫用燻蒸剤の使用に関する規制禁止または厳しい規制が発効するまで、成長率と市場シェアは一定に保たれると予想されます。

倉庫用燻蒸剤産業の概要

2016年以降、世界の倉庫用燻蒸剤市場は細分化された形になってきており、このプロセスは今後も続くと思われます。大手企業が採用した戦略のうち、買収、提携、拡大がシェアの半分以上を占めています。このような活発なM&A活動の背景にある主な理由は、市場向けに技術的に先進的で使いやすい燻蒸剤を開発するために、両社の新技術を連携させることです。主な買収や産業提携は、市場への浸透とポジショニングを深めるための前方および後方統合を目的としています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

市場セグメンテーション

- タイプ

- 臭化メチル

- フッ化スルフリル

- ホスフィン

- リン酸マグネシウム

- リン化アルミニウム

- その他

- 用途

- 商品貯蔵保護

- 形状

- 固体

- 液体

- ガス

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- オランダ

- ポーランド

- イタリア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- その他アジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他南米

- アフリカ

- 南アフリカ

- その他のアフリカ

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- ADAMA Agricultural Solutions Ltd

- UPL Group

- Cytec Solvay Group

- Degesch America Inc.

- Douglas Products and Packaging Products LLC

- BASF SE

- Corteva Agriscience

- Reddick Fumigants, LLC

- Ikeda Kogyo Co., Ltd.

- Industrial Fumigation Company LLC

- Lanxess

- Nippon Chemical Industrial Co. Ltd

- Vietnam Fumigation Joint Stock Company

- Fumigation Services Pvt. Ltd

第7章 市場機会と今後の動向

The Warehouse Fumigants Market size is estimated at USD 1.44 billion in 2024, and is expected to reach USD 1.88 billion by 2029, growing at a CAGR of 5.40% during the forecast period (2024-2029).

In 2018, North America was the largest geographical segment of the market studied and accounted for a share of around 33.8% of the global market.By type, the phosphine-based fumigant product segment had the largest market share of 26.3% in 2018 and is expected to remain the fastest-growing segment during the forecast period.

Asia-Pacific has been identified as the region, which is yet to reach its maximum potential in the warehouse fumigant market. The market is driven by several factors, like rapid technological advancement in the sector, growing concerns over the post-harvest loss, and the shift in advance farming practices that led to increased yield. The introduction of fumigants to plants helps them keep the diseases away from their roots and to produce a better yield.

Warehouse Fumigants Market Trends

Increased Need for Pest Control

The largest natural threat to the safe storage and distribution of grains is insect infestation in the pest control industry. However, tools like fumigation are more effective in controlling pest infestations and are more effective, as compared to structural and warehouse fumigation. It is anticipated that due to climate changes, like an increase in temperature, the insect population is going to increase in the future, leading to increased dependence on the usage of fumigants. In order to control insects in commodities and export materials, fumigation is one of the general methods, which is adopted widely across emerging countries. Globally, phosphine and methyl bromide are the two common fumigants, which are used for stored product protection.

North America Dominates the Global Market

North America contributes a significant share of global warehouse fumigant consumption with a 33.8% share in 2018, with the United States and Canada accounting for around 80% of the regional market. North America is a major market for agriculture fumigants, with over 250 authorized products available in the main countries of the United States and Canada. The major commodities using fumigants for both warehouse and soil applications in the region are, corn, rice, barley, potato, tomato, wheat, strawberry, cabbage, etc. Due to very low export and storage capacities of countries like including Cuba, the Dominican Republic, Costa Rica, Jamaica and others, the growth rate, and market share are expected to remain constant until regulatory ban or stringent regulations on the usage of warehouse fumigants are brought into effect.

Warehouse Fumigants Industry Overview

The global warehouse fumigantsmarket has been getting into a fragmented shape since 2016, and this process is likely to continue in the future as well. Acquisitions, partnerships, and expansions account for more than half of the share among the strategies adopted by leading players. The main reason behind such intensive M&A activities, is the collaboration of new technology of the two companies, in order to develop technologically advanced and user-friendly fumigants for the market. The major acquisitions and industrial collaborations taking place are targeted toward forward and backward integration for deeper penetration and positioning in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Force Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Methyl Bromide

- 5.1.2 Sulfuryl Fluoride

- 5.1.3 Phosphine

- 5.1.4 Magnesium Phosphide

- 5.1.5 Aluminium Phosphide

- 5.1.6 Others

- 5.2 Application

- 5.2.1 Structural Fumigation

- 5.2.2 Commodity Storage Protection

- 5.3 Form

- 5.3.1 Solid

- 5.3.2 Liquid

- 5.3.3 Gas

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 US

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 UK

- 5.4.2.3 France

- 5.4.2.4 Russia

- 5.4.2.5 Spain

- 5.4.2.6 Netherlands

- 5.4.2.7 Poland

- 5.4.2.8 Italy

- 5.4.2.9 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 ADAMA Agricultural Solutions Ltd

- 6.3.2 UPL Group

- 6.3.3 Cytec Solvay Group

- 6.3.4 Degesch America Inc.

- 6.3.5 Douglas Products and Packaging Products LLC

- 6.3.6 BASF SE

- 6.3.7 Corteva Agriscience

- 6.3.8 Reddick Fumigants, LLC

- 6.3.9 Ikeda Kogyo Co., Ltd.

- 6.3.10 Industrial Fumigation Company LLC

- 6.3.11 Lanxess

- 6.3.12 Nippon Chemical Industrial Co. Ltd

- 6.3.13 Vietnam Fumigation Joint Stock Company

- 6.3.14 Fumigation Services Pvt. Ltd