|

市場調査レポート

商品コード

1939614

臨床データ分析:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Clinical Data Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 臨床データ分析:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

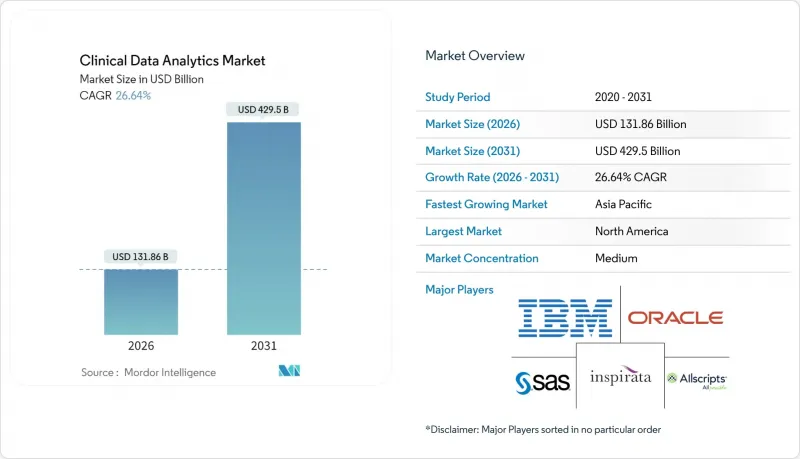

臨床データ分析市場は、2025年の1,041億2,000万米ドルから2026年には1,318億6,000万米ドルへ成長し、2026年から2031年にかけてCAGR26.64%で推移し、2031年には4,295億米ドルに達すると予測されています。

この著しい成長軌道は、実世界エビデンスに関する規制要件と、大規模な精密医療を可能にするAI搭載予測モデルの普及に牽引された、医療業界の加速するデジタル変革を反映しています。

市場の拡大は、医療の利害関係者が膨大な臨床データセットから実用的な知見を抽出する方法を根本的に変革しています。2024年時点ではクラウド導入モデルが61.54%の市場シェアを占めていますが、ジェネレーティブAI対応ソフトウェアが2030年までにCAGR23.67%で最も急速に成長するコンポーネント分野として台頭しています。このインテリジェントオートメーションへの移行は、データサイエンティスト不足という重大なボトルネックへの対応策であり、スタンフォード・ヘルスケアのChatEHRは、自然言語インターフェースが臨床データへのアクセスを現場の医療提供者に民主化する方法を実証しています。

北米は2024年に47.24%のシェアで市場をリードし続けていますが、アジア太平洋地域の19.78%という成長率は、政府主導のデジタル化施策と拡大する製薬分野の研究開発投資に牽引された地理的再均衡を示しています。競合情勢においては、HEALWELL AIによるOrion Healthの買収といった大規模な統合が進んでおり、デジタルヘルス企業におけるFHIR導入率が現在の73%からさらに加速する中、相互運用性のプレミアムを獲得する企業群が形成されつつあります。

価値に基づく医療報酬モデルとマルチオミクスデータ生成の融合により、高度な分析プラットフォームへの需要がかつてないほど高まっています。2024年には医療提供者が市場の46.78%を占め、製薬・バイオテクノロジー分野の16.56%のCAGRは年間2,500億米ドルの研究開発費と、AIによる臨床知見を活用した医薬品開発期間短縮の推進を反映しています。しかしながら、ソースシステム間のデータ品質のばらつきや、レガシーEHRシステムとの統合コストの高さは、コスト重視の医療環境における導入率を制約する可能性のある重大な障壁として残っています。

世界の臨床データ分析市場の動向と洞察

AI駆動型予測モデルの採用拡大

医療提供者、保険者、ライフサイエンス企業は、臨床および業務ワークフローに生成AIを組み込んでいます。Epic社は、記録作成やリスクスコアリングを自動化する100以上のAIプロジェクトの展開を開始し、複数の大規模医療システムはMicrosoft社と提携し、電子カルテ内にリアルタイム予測を表示しています。FDAは適応型アルゴリズムの審査サイクルを迅速化し続けており、早期敗血症警報や再入院防止ツールの導入期間を短縮しています。ベラダイムなどのベンダーは、2億件以上の縦断的患者記録を活用し、文書作成時間を削減し臨床医の満足度を向上させる環境記録機能の商用化を実現しています。

医薬品承認における実世界データの規制推進

FDAが2025年に発表した「規制申請における実世界データ(RWE)活用に関するガイダンス」は、製薬業界における縦断的データプラットフォームの需要を加速させています。RWEは、従来の臨床試験が実施困難な希少疾患や市販後調査において特に価値が高いものです。製薬アナリティクスへの支出は、企業が保険請求データ、電子健康記録(EHR)、ゲノムデータセットを統合し、日常診療における薬剤の有効性を検証する動きに伴い、2025年までに30億米ドルに達すると予測されています。CDCとTruvetaの提携のようなパートナーシップは、官民のデータ連携が安全性監視やパンデミック対応をいかに迅速化できるかを示しています。FHIRベースのAPIに対する規制当局の選好は、臨床データ分析市場全体で、広範な実世界コホートをオンデマンドで構築できる相互運用可能なインフラへの投資をさらに促進しています。

ソースシステム間におけるデータ品質のばらつき

異なるコーディング方式、不一致なタイムスタンプ、自由記述形式の入力は分析の信頼性を低下させます。買収により拡大した医療システムでは、複数のEHRを同時に運用しているケースが多く、それぞれが独自のデータモデルを有しています。不十分なデータ管理はAIパイプライン開発に要する時間を膨張させ、コストのかかる手動によるデータ整備を強いることになります。マスターデータ管理プラットフォームや自動化されたデータプロファイリングツールが、リアルタイムで異常を検知するために導入されつつあります。進歩はあるもの、普遍的なデータ品質基準の欠如は組織間の連携を妨げ、臨床データ分析市場における分析プログラムの拡大を遅らせています。

セグメント分析

クラウドベースの導入は2025年に収益の60.88%を占め、医療分野がスケーラブルな従量課金型アーキテクチャへ移行していることを反映しています。クラウドセグメントは15.70%のCAGRを記録すると予測され、オンプレミス型を大きく上回ります。マイクロソフトのAzureを活用したプロビデンスおよびノースウェスタン・メディシンとの連携事例は、弾力的なコンピューティングががん治療経路の最適化から環境記録に至るAIプロジェクトをいかに加速させるかを実証しています。一方、オンプレミス導入は主に、厳格なデータ居住要件やプライベートデータセンターへの既得投資を抱える機関に支持されています。こうした二重の圧力により、調達方針はローカル管理とクラウドの俊敏性を融合したハイブリッドモデルへ移行しつつあり、臨床データ分析市場の主要な成長エンジンとしてのクラウドの役割を強化しています。

地域固有の医療データ保護法の台頭は、ローカルクラウドリージョンの促進につながり、多国籍企業が主権規則に抵触することなく分析サービスの拡大を可能にしております。自動化されたコンプライアンス報告とゼロトラストセキュリティアーキテクチャを提供するベンダーのシェアが拡大中です。ワークロードの移行が進むにつれ、プラットフォームロックインのリスクが買い手にコンテナベースのデプロイメントとオープンスタンダードAPIを要求させる要因となっており、これらの動向が相まって臨床データ分析市場全体でイノベーションと価格競争を促進しております。

サービス分野が依然として支出の51.60%を占める一方、生成AIソフトウェアは最も急速に拡大する構成要素であり、2031年まで年率22.35%の成長が見込まれます。電子健康記録(EHR)に組み込まれたチャットインターフェースにより、臨床医はコーディングスキルなしで診療記録の要約や指示書の作成が可能となります。SASのViya Workbenchは開発者がセキュアなサンドボックス内でAIモデルの構築・検証・展開を可能にし、クラウド収益を前年比30%増加させています。ソフトウェアの直感的な操作性向上に伴い、サービスプロバイダーは基本的な導入支援から、モデルガバナンスや変更管理に関する高付加価値のコンサルティングへと業務をシフトしています。この再配置により、ライセンス収益がサブスクリプション型AIプラットフォームに依存する傾向が強まる中で利益率が守られ、臨床データ分析市場の進化する構造を支えています。

地域別分析

北米地域は、電子健康記録(EHR)の高い普及率、大規模な研究開発予算、実世界データ(RWE)を重視する積極的な規制ガイダンスにより、2025年に収益の46.70%を生み出しました。主導的立場にあるにもかかわらず、相互運用性は依然として課題であり、米国のクロスプラットフォーム接続性はわずか59.8%と測定されています。スタンフォード大学やマサチューセッツ総合病院ブリガムなどの学術医療センターでは、生成AI放射線診断ツールや対話型EHRインターフェースの試験運用が進められており、導入速度のベンチマークを確立しています。政府資金プログラムは地方病院の設備更新を継続的に促進しており、同地域の臨床データ分析市場におけるユニット需要を支えています。

アジア太平洋地域は2031年までにCAGR19.05%を記録し、最も急速な拡大が見込まれます。中国、インド、日本における政府主導のデジタル化推進、大規模な人口基盤、成長するバイオテックエコシステムが成長の原動力となっています。クラウド優先政策により参入障壁が低下し、小規模病院でも従来型段階を飛び越えることが可能となりました。多国籍企業は遺伝的多様性に富むコホートへのアクセスを目的に、同地域で分散型臨床試験を増加させており、分析ツールの導入をさらに後押ししています。しかしながら、プライバシー規制の差異や人材スキルのギャップといった運用上の複雑性が存在し、ベンダーはこれらを克服することで初めて、アジア太平洋地域の臨床データ分析市場における役割を最大限に活用できるでしょう。

欧州、南米、中東・アフリカでは、10%台半ばの着実な成長が見込まれます。EUの厳格なGDPR要件は、高度な匿名化ツールとプライバシー保護分析を促進し、それが輸出志向のプラットフォームベンダーに利益をもたらしています。ラテンアメリカでは、ブラジルとコロンビアの国家的なe-ヘルスプログラムが、資金面の制約はあるもの、新たな需要の創出につながっています。湾岸協力会議(GCC)加盟国は、サウジアラビアの「ビジョン2030」に代表されるように、AIを活用したスマート病院プロジェクトに多額の投資を行っており、臨床データ分析市場において、世界規模で高度な分析プラットフォームへの需要が高まっていることを示しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3か月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- AI駆動型予測モデルの採用拡大

- 医薬品承認における実世界データの規制推進

- 価値に基づく医療報酬モデルへの移行

- クラウドネイティブ医療ITインフラの拡大

- マルチオミクスおよびゲノムデータ生成の急増

- FHIRベースの相互運用可能なデータ交換の出現

- 市場抑制要因

- ソースシステム間のデータ品質のばらつき

- レガシーEHR統合の高コスト

- 二次データ利用に関する倫理的・法的懸念

- 特定分野のデータサイエンティストの不足

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 展開モデル別

- クラウドベース

- オンプレミス

- コンポーネント別

- ソフトウェア

- サービス

- 用途別

- 品質改善と臨床ベンチマーキング

- 臨床意思決定支援

- 規制報告およびコンプライアンス

- 比較有効性分析

- 精密医療/集団健康

- エンドユーザー業界別

- プロバイダー

- 支払機関

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 中東

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Oracle Corporation

- Optum Inc.

- IBM Corporation

- Philips Healthcare

- SAS Institute Inc.

- Health Catalyst Inc.

- Allscripts Healthcare LLC

- McKesson Corporation

- IQVIA Inc.

- Veradigm Inc.

- Epic Systems Corporation

- GE HealthCare Technologies Inc.

- Amazon Web Services(AWS)HealthLake

- Google Cloud Healthcare Data Engine

- Microsoft Azure Health Data Services

- Medidata Solutions(Dassault Systemes)

- Flatiron Health Inc.

- Evidation Health

- TriNetX LLC

- Inspirata Inc.

- CareEvolution Inc.