|

市場調査レポート

商品コード

1432864

飼料用固化防止剤:市場シェア分析、産業動向・統計、成長予測(2024~2029年)Feed Anti-Caking Agents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 飼料用固化防止剤:市場シェア分析、産業動向・統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

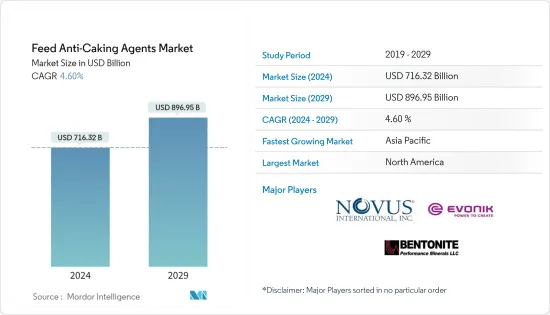

飼料用固化防止剤の市場規模は2024年に7,163億2,000万米ドルと推定され、2029年には8,969億5,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは4.60%で成長する見込みです。

動物飼料市場の拡大が、調査対象市場の成長を牽引しています。さらに、高品質の飼料に対するニーズの高まりと、特に配合飼料業界における飼料添加物の増加が、調査した市場の主な成長促進要因です。

飼料用固化防止剤の市場動向

配合飼料産業の拡大が市場成長の原動力

調査対象市場は主に動物飼料市場の拡大が牽引しています。畜産業が低成長を記録したため、動物用飼料のニーズが高まっています。このため、飼料添加物、特に飼料の固結防止剤の需要が増加すると予想されます。さらに、ケイ酸塩は水と油の両方を吸収することができるため、固結防止剤として広く使用されています。フェロシアン化ナトリウムやリン酸三カルシウムなどのナトリウムやカルシウム製品は、飼料の個体付着を減らすため、高い需要を目の当たりにしています。

北米と欧州が市場の主要地域

北米地域は世界の飼料用固化防止剤市場において最大の地域セグメントであり、僅差で欧州が続いています。鶏肉と豚肉がそれぞれ市場シェアの40%と25%を占めています。米国は地域別市場シェアのほぼ70%を占めているが、これは主に畜産業が確立されているためです。さらに、高品質の飼料に対するニーズが、この市場の成長を牽引しています。

飼料用固化防止剤産業の概要

飼料用固化防止剤市場は非常に断片化されており、様々な中小企業と少数の大手企業が存在しています。したがって、調査した市場では高い競合が存在します。さらに、調査した市場では、各社は設備やプロモーションの質で競争しているだけでなく、最大の市場シェアを占めるために戦略的な動きにも注力しています。新製品の発売、パートナーシップ、買収は、世界の飼料用固化防止剤市場の主要企業が採用する主要戦略です。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因と市場抑制要因のイントロダクション

- 市場促進要因

- 市場抑制要因

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 化学タイプ

- シリコン系

- ナトリウムベース

- カルシウム系

- カリウム系

- その他の化学タイプ

- 動物タイプ

- 反芻動物

- 家禽

- 豚

- 水産養殖

- その他の動物

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- スペイン

- 英国

- フランス

- ドイツ

- ロシア

- イタリア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- タイ

- ベトナム

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- Novus International

- BASF SE

- Archer Daniels Midland Company

- Evonik Industries

- Bentonite Performance Minerals LLC

第7章 市場機会と今後の動向

The Feed Anti-Caking Agents Market size is estimated at USD 716.32 billion in 2024, and is expected to reach USD 896.95 billion by 2029, growing at a CAGR of 4.60% during the forecast period (2024-2029).

The expansion of the animal feed market is driving the growth of the market studied. Moreover, the rising need for a high-quality feed and an increase in the number of feed additives, especially in the compound feed industry, are the major growth drivers of the market studied.

Feed Anti-Caking Agents Market Trends

Expansion of the Compound Feed Industry is Driving the Market's Growth

The market studied is primarily driven by the expansion of the animal feed market. As the livestock industry registered a low growth rate, there is an increasing need for animal feed. This is expected to drive the demand for feed additives, particularly feed anti-caking agents. Moreover, silicates are widely used as anti-caking agents, as silicates can absorb, both, water and oil. Sodium and calcium products, such as sodium ferrocyanide and tricalcium phosphate are witnessing high demand, as they reduce individual adhesion of feed.

North America and Europe are the Major Regions in the Market

The North American region is the largest geographical segment in the global feed anti-caking agents market, closely followed by Europe. Poultry and swine accounted for 40% and 25% of the market share, respectively. The United States accounted for almost 70% of the regional market share, mainly due to its well-established livestock production industry. Additionally, the need for high-quality feed is driving the growth of the market studied.

Feed Anti-Caking Agents Industry Overview

The feed anti-caking agent market is highly fragmented, with the presence of various small and medium-sized companies and a few major players. Thus, there is high competition in the market studied. Furthermore, in the market studied, companies are not only competing on the basis of the quality of equipment and promotion but also are focusing on strategic moves, in order to account for the largest market share. New product launches, partnerships, and acquisitions are the major strategies adopted by the leading companies in the feed anti-caking agents market, globally.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.4 Market Restraints

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Chemical Type

- 5.1.1 Silicon-based

- 5.1.2 Sodium-based

- 5.1.3 Calcium-based

- 5.1.4 Potassium-based

- 5.1.5 Other Chemical Types

- 5.2 Animal Type

- 5.2.1 Ruminant

- 5.2.2 Poultry

- 5.2.3 Swine

- 5.2.4 Aquaculture

- 5.2.5 Other Animal Types

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Spain

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Germany

- 5.3.2.5 Russia

- 5.3.2.6 Italy

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Thailand

- 5.3.3.5 Vietnam

- 5.3.3.6 Australia

- 5.3.3.7 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East & Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Novus International

- 6.3.2 BASF SE

- 6.3.3 Archer Daniels Midland Company

- 6.3.4 Evonik Industries

- 6.3.5 Bentonite Performance Minerals LLC