|

市場調査レポート

商品コード

1432327

建築用コーティング:市場シェア分析、産業動向、成長予測(2024~2029年)Architectural Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 建築用コーティング:市場シェア分析、産業動向、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

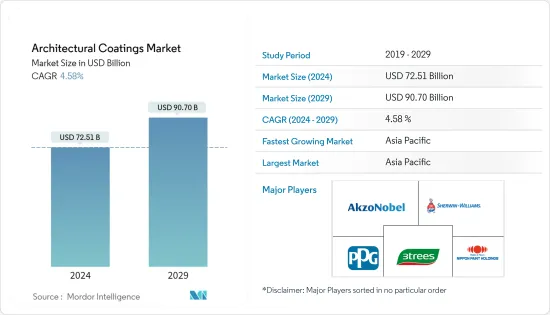

建築用コーティング市場規模は2024年に725億1,000万米ドルと推定され、2029年には907億米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは4.58%で成長する見込みです。

建築分野は建築用コーティング市場の主要促進要因です。これらのコーティングには、耐食性、紫外線防止など、いくつかの利点があります。酢酸ビニルは一般的に使用されている建築用コーティングの一種です。建築用インフラの需要増加が期待されます。

主なハイライト

- 低VOCコーティングへの需要の高まりが、同市場に様々な機会を生み出しています。

- 世界中で地球温暖化への懸念が高まり、オフィスビルや住宅などに安全で省エネルギーなコーティングが求められています。

- 予測期間中、アジア太平洋地域が世界市場を独占すると予想されます。

建築用コーティング市場の動向

住宅分野からの需要の増加

- エンドユーザーセグメントのうち、住宅セグメントが2021年の建設セクターを支配し、世界市場で建築用コーティングの最も高い需要を生み出しています。

- 中国では近年、住宅需要が大幅に増加しています。住宅価格が過去最低水準にあるため、住宅需要が大幅に増加し、建築用コーティングの需要が増加しています。

- 同様に米国でも、住宅用塗料の消費量は2022年に高い伸びを示しました。United States Cnesus BoardとUnited States Department of Housing and Urban Developmentによると、2022年8月の個人の住宅建設戸数は2022年7月の165万5,000戸から1.1%増加しました。

- 今後1年間は、ロシアとウクライナにおける最近の戦争勃発により、住宅や商業用建物の需要が高まると予測されています。

- 以上のような要因が、予測期間中の建築用塗料・コーティングの需要を押し上げると予想されます。

アジア太平洋地域を支配する中国

- 中国における建築用コーティングの消費量は近年増加傾向にあります。住宅の床面積は2022年6月の6,642万3,470㎡から2022年7月には7,606万6,760㎡へと増加しています。これは国内における建築用コーティングの消費増加に直接的な影響を与えます。

- 2022年3月以降、輸入用塗料・コーティングの申請や試験義務の撤廃といった政府のイニシアチブは、国内における建築用コーティングのポジティブな将来性に対するコーティング企業の自信を高めているため、消費と売上の増加は予測期間中に拡大すると予想されます。

- 水性コーティングは、中国政府が定めたVOC規制を長期にわたって採用してきたため、同国で消費される建築用コーティング全体の約79%という最大シェアを占めています。さらに、2050年までにカーボンニュートラルを実現するという中国のコミットメントが、水性コーティングのような環境に優しい製品をさらに後押ししています。

- 中国では、2016~2021年の建築用コーティングの総消費量において、外壁の主要部分の塗装に使用されるアクリルコーティングが樹脂タイプの中で大きなシェアを占めています。

- アクリルコーティングは、この期間に消費された建築用コーティング全体の約半分以上を占めています。中国政府の規制が低VOC建築用コーティングの採用を促進しており、建築用コーティングメーカーはコーティングのVOC含有量を減らし、安全な製品として販売することを余儀なくされています。

建築用コーティング業界の概要

建築用コーティング市場は細分化されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 東欧諸国の床面積中央値の伸び

- 住宅および商業インフラの増加

- 抑制要因

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 規制

第5章 市場セグメンテーション

- 技術

- 水性

- 溶剤系

- 樹脂タイプ

- アクリル

- アルキド

- ポリウレタン

- エポキシ

- ポリエステル

- その他

- 最終用途サブセグメント

- 商業用

- 住宅用

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- タイ

- インドネシア

- マレーシア

- フィリピン

- シンガポール

- ベトナム

- オーストラリア・ニュージーランド

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- ポーランド

- 北欧諸国

- ロシア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア分析

- 主要企業の採用戦略

- 企業プロファイル

- 3 Trees

- AkzoNobel N.V.

- Asian paints

- BASF SE

- Benjamin Moore

- Berger Paints India

- Brillux GmbH & Co. KG

- CIN, S.A.

- Cloverdale Paint Inc.

- DAW SE

- Flugger group A S

- Hempel A/S

- Kansai Paint Co.,Ltd.

- Masco Coporation

- Nippon Paint

- PPG

- RPM International

- Sniezka SA

- The Sherwin-Williams Company

第7章 市場機会と今後の動向

The Architectural Coatings Market size is estimated at USD 72.51 billion in 2024, and is expected to reach USD 90.70 billion by 2029, growing at a CAGR of 4.58% during the forecast period (2024-2029).

The construction sector is a major driver of the Architecture Coatings Market. These coatings have several advantages including corrosion resistance, UV rays protection, etc. Vinyl Acetate is the common type of Architecture coating in use. Architecture Infrastructure is expected to see a rise in demand for Market Studied.

Key Highlights

- Increasing demand for Low VOC Coatings is creating various opportunities in this Market.

- Increasing Global Warming Concern across the globe is demanding safe and energy-saving coatings for office buildings, residential homes, etc.

- Asia-Pacific is expected to dominate the global market, during the forecast period.

Architectural Coatings Market Trends

Increasing Demand from Residential Sector

- Among the end-user segments, the residential segment dominated the construction sector in 2021, generating the highest demand for architectural coatings in the global market.

- In China, there has been a significant increase in demand for residential houses in the recent past. With the prices of the residential houses at an all time low when compared to the previous years the demand for the residential houses has increased to a greater extent there by increasing the demand for architectural coatings.

- Similarly, in the United States, residential paint consumption saw high growth in 2022. According to the United States Cnesus Board and United States Department of Housing and Urban Development the number of private houses construction increased by 1.1% in August 2022 compared to 1,655,000 houses in July 2022.

- In the coming year it is projected that there would be a high demand of residential and commercial buildings in Russia and Ukraine due to the recent outbreak of the war.

- All the above mentioned factors are expected to drive the demand for the architectural paints and coatings in the forecast period.

China to Dominate the Asia-Pacific Region

- Architectural coating consumption in China has been on rising in the recent past. There has been an increase in the floor space of the residential houses from 66,423.47 thousand Square metres in June 2022 to 76,066.76 thousand Square metres in July 2022. This has a direct impact on the increase in the consumption of Architectural coatings in the country.

- The increase in consumption and sales is expected to grow in the forecasted period due to the government initiatives such as revoking filing and mandatory testing requirements of imported paint and coatings in the country from march, 2022 grows the confidence of coating companies in the positive future of architectural coating in the country.

- The waterborne coating holds the largest share of around 79% of the total architectural coating consumed in the country due to the long adoption of VOC regulations set by the Chinese government. Furthermore, the country's commitment toward carbon neutrality by 2050, will further drive the eco-friendly product like waterborne coatings in the country.

- In China, acrylic coatings holds the major share amongst resin type, in terms of the total consumption volume of architectural coatings during 2016-2021, as it is used to coat the major part of the exterior walls.

- Acrylic coatings accounted for about ore than half of the total architectural coatings consumed during this period. The Chinese government regulations are majorly driving the adoption of low VOC architectural coatings and forces architectural coating manufacturers to reduce the VOC content in their coatings and market it as a safe product.

Architectural Coatings Industry Overview

The architectural coatings market is fragmented in nature. Some of the major players of the market studied include (not in particular order) Akzo Nobel N.V., The Sherwin-Williams Company, PPG Industries, Inc., 3 Trees and Nippon Paint Holdings Co., Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMEREY

4 MARKET DNAMICS

- 4.1 Drivers

- 4.1.1 Growth in Median Floor Area of Eastern European Countries

- 4.1.2 Increasing Residential and Commertial Infrastructure

- 4.2 Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Force Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Regulations

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Water-borne

- 5.1.2 Solvent-borne

- 5.2 Resin Type

- 5.2.1 Acrylic

- 5.2.2 Alkyd

- 5.2.3 Polyurethane

- 5.2.4 Epoxy

- 5.2.5 Polyester

- 5.2.6 Other Resin Types

- 5.3 End-use sub segment

- 5.3.1 Commercial

- 5.3.2 Residential

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Thailand

- 5.4.1.6 Indonesia

- 5.4.1.7 Malaysia

- 5.4.1.8 Philippines

- 5.4.1.9 Singapore

- 5.4.1.10 Vietnam

- 5.4.1.11 Australia & Newzealand

- 5.4.1.12 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.2.4 Rest of North America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 France

- 5.4.3.3 United Kingdom

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Poland

- 5.4.3.7 Nordic Countries

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis

- 6.3 Stratergies Adopted by Leading players

- 6.4 Company Profiles

- 6.4.1 3 Trees

- 6.4.2 AkzoNobel N.V.

- 6.4.3 Asian paints

- 6.4.4 BASF SE

- 6.4.5 Benjamin Moore

- 6.4.6 Berger Paints India

- 6.4.7 Brillux GmbH & Co. KG

- 6.4.8 CIN, S.A.

- 6.4.9 Cloverdale Paint Inc.

- 6.4.10 DAW SE

- 6.4.11 Flugger group A S

- 6.4.12 Hempel A/S

- 6.4.13 Kansai Paint Co.,Ltd.

- 6.4.14 Masco Coporation

- 6.4.15 Nippon Paint

- 6.4.16 PPG

- 6.4.17 RPM International

- 6.4.18 Sniezka SA

- 6.4.19 The Sherwin-Williams Company