|

市場調査レポート

商品コード

1431742

キャプティブ発電所:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Captive Power Plant - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| キャプティブ発電所:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 105 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

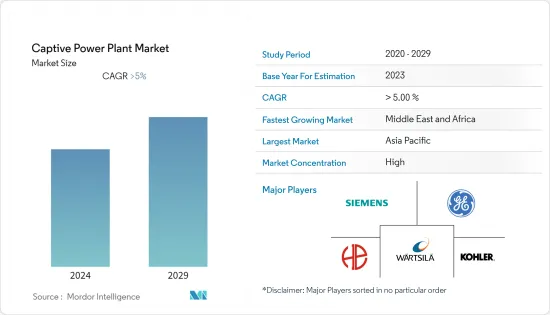

Equal-6.41に換算したキャプティブ発電所市場規模は、予測期間中(2024-2029年)にCAGR 6.41%で、2024年の2,141億2,000万米ドルから2029年には2,921億4,000万米ドルに成長すると予測されます。

主なハイライト

- 中期的には、発電産業はほとんどの国で確立されているが、電力会社が24時間体制で高品質の電力を産業用ユーザーに供給するには限界があるため、産業界は自家発電所を設立せざるを得ないです。さらに、これらの産業のいくつかは遠隔地にあり、電力供給の信頼性が低い(特に発展途上国や低開発諸国)ことが、自家発電所の設置を促進する要因となっています。

- その一方で、高い資本支出と運転経費が、世界中の低開発地域におけるキャプティブ発電所の成長を制限しています。

- とはいえ、ナイジェリア、アンゴラ、ガーナといったアフリカ諸国におけるエネルギー集約型産業の拡大は、近い将来、キャプティブ発電所の設備メーカーや開発者に大きな機会を提供すると期待されています。

- アジア太平洋地域がキャプティブ発電所市場を独占しており、需要の大半は中国、インド、日本によるものです。

キャプティブ発電所市場の動向

市場で大きなシェアを占める鉄鋼業界

- 大規模な製鉄所を運営する上で、信頼できる電源を確保することは非常に重要です。鉄鋼プラントの配電システムは、負荷の性質とその大きさから、他の産業プラントの配電システムとは異なります。大規模な総合鉄鋼プラントは、様々な加工プラント、非加工プラント、サービス、ユーティリティで構成されていることは常識です。

- 鉄鋼プラントは、高額の資本支出を必要とする連続プロセスプラントであるため、電力網の設計は、電力品質の低下による系統停電、電力機器の故障、電力系統の内部障害などのあらゆる事態に適切に対処できるよう、クリティカリティの観点から検討されるべきです。機器や付属品の選定やサイジングに制約があると、生産が失われる結果、経済的損失に伴う莫大な資本的損害が発生することになり、結果として莫大な資本的損害を被ることになりかねないです。

- さらに、現代生活の大部分は鉄鋼で構成されています。インフラ、建物、機械、電気機器、自動車、調理器具から家具に至るまで、さまざまな製品が大量の鉄鋼を必要とします。鉄鋼需要は2050年までに5倍になると推定されています。

- 世界は近代化の過程で膨大な鉄鋼生産能力を構築してきました。世界鉄鋼協会によると、2022年の鉄鋼生産量は約18億8,500万トン(MT)で、2012年から約20.6%増加しました。

- 様々な政策の結果、多国間協力プロセスを通じた製造基盤の拡大、ノウハウの共有、製品開発、技術移転により、国産化が促進されます。

- 例えば、2022年10月、ArcelorMittal傘下のAMNS Indiaは、インドのハジラ製鉄所への76億2,000万米ドルの投資を発表しました。この投資により、同工場の生産能力は現在の900万トンから1,500万トンに増加する見込みです。さらに、この投資には新しい製鉄技術の導入、新時代の機械の設置、製品提供の拡大も含まれます。

- 2022年7月、インドネシアのKrakatau Steelと韓国のPOSCO Holdingsは、インドネシアにおける鉄鋼生産能力の拡大に35億米ドルを投資することで合意しました。この合意により、クラカタウ・ポスコの川上・川下製品の生産能力は年間1,000万トンに拡大されます。2023年からの拡張には、電気自動車用の自動車用鋼の製造も含まれます。

- 同地域における鉄鋼・鉄鋼産業の発展と投資を考慮すると、容量発電所の需要は予測期間中に大幅な成長が見込まれます。

アジア太平洋が市場を独占する

- アジア太平洋地域は、2022年にキャプティブ発電所市場を独占すると予想され、今後数年間もその支配力を維持すると予想されます。人口増加、急速な都市化、工業化などの要因がこの地域の電力需要を牽引し、容量拡大の大きな機会を生み出しています。

- GDPでは、中国は世界第2位の経済大国です。2022年、同国のGDPは約0.8%成長し、17兆9,600億米ドルに達しました。高齢化が進み、製造業からサービス業へ、外需から内需へ、投資から消費へと経済のリバランスが進む中、同国の成長は徐々に衰えています。

- 中国は、化学、石油・ガス、金属加工、その他の分野の著しい成長により、キャプティブ発電所の最大かつ急成長市場のひとつになると予想されます。さらに、キャプティブ発電所はこれらの産業で重要な役割を果たしているため、予測期間中も同様の成長が見込まれています。

- 鉄鋼業界は、キャプティブ発電所の重要な市場です。世界鉄鋼協会によると、2022年の中国の鉄鋼生産量は約10億1,800万トンで、世界の鉄鋼生産量の約54%を占めています。

- さらに、石油化学産業は中国経済に大きく貢献しており、製造業の高品質な発展を支える主な分野でもあります。最近、中国は石油化学部門の発展を目の当たりにしています。例えば、2023年3月、アラムコと合弁パートナーである磐金新城実業集団とNORINCOグループは、中国北東部で大規模な石油精製と石油化学の統合コンプレックスの建設を開始する計画を発表しました。このコンプレックスは、日産30万バレルの製油所と年産165万トンのエチレンと200万トンのパラキシレンを生産する石油化学プラントを併せ持つ予定です。建設は、プロジェクトが行政認可を確保した後、2023年第2四半期に開始される予定です。2026年までにフル稼働する予定です。

- 韓国も石油化学事業に投資しており、キャプティブ発電所の需要増加が見込まれています。2022年11月、サウジアラムコは、より高価値の石油化学製品を生産するため、港湾都市ウルサンにある韓国の関連会社の工場に約70億米ドルの投資計画を発表しました。同社によると、シャヒーン・プロジェクトは、世界最大級の石油精製統合型石油化学スチームクラッカーを開発するための、アジア諸国におけるサウジ最大の投資です。

- したがって、鉄鋼、石油化学産業からのこれらの動向により、キャプティブ発電所の需要は予測期間中に大幅に増加すると予想されます。

キャプティブ発電所産業の概要

キャプティブ発電所市場は統合されています。この市場の主要企業(順不同)には、Kohler Co.、General Electric Company、Wartsila Oyj Abp、Bharat Heavy Electricals Limited、Siemens AGなどが含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2028年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と展開

- 政府の規制と政策

- 市場力学

- 促進要因

- 産業分野における電力需要の増加

- 複数の産業の遠隔地と電力供給の不安定性

- 抑制要因

- 高い設備投資と運用費

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 燃料源

- 石炭

- ガス

- ディーゼル

- 再生可能

- その他の燃料

- 産業

- セメント

- 鉄鋼

- 金属・鉱物

- 石油化学

- その他

- 地域

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- ドイツ

- フランス

- 英国

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Kohler Co.

- General Electric Company

- Wartsila Oyj Abp

- Siemens AG

- Bharat Heavy Electricals Limited

- Tata Power Renewable Energy

- AMP Solar Group Inc.

第7章 市場機会と今後の動向

目次

Product Code: 47683

The Captive Power Plant Market size in terms of Equal-6.41 is expected to grow from USD 214.12 billion in 2024 to USD 292.14 billion by 2029, at a CAGR of 6.41% during the forecast period (2024-2029).

Key Highlights

- Over the medium term, though the power generation industry is well-established in most countries, the limitations that the utilities have to provide high-quality power round the clock to the industrial users force the industries to establish captive power plants. Moreover, the remote location of some of these industries and the unreliability of the power supply (especially in developing and underdeveloped countries) are the factors promoting the installation of captive power plants.

- On the other hand, high capital and operational expenditures are limiting the growth of captive power plants in underdeveloped regions across the world.

- Nevertheless, the expansion of energy-intensive industries in African countries such as Nigeria, Angola, and Ghana is expected to provide a significant opportunity for captive power plant equipment manufacturers and developers in the near future.

- Asia-Pacific has dominated the captive power plant market, with the majority of the demand coming from China, India, and Japan.

Captive Power Plant Market Trends

Steel Industry to Have Significant Share in the Market

- It is very important to have a reliable power source when operating a large-scale steel plant. The distribution system for power in a steel plant is different from that of any other industrial plant because of the nature of the load and its magnitude. It is common knowledge that large-scale integrated steel plants consist of a variety of processing plants, nonprocessing plants, services, and utilities.

- Since steel plants are continuous process plants requiring high capital expenditure, power network design should be viewed from a criticality perspective to ensure that any eventuality such as grid power failure, power equipment failure and internal power system disturbances due to poor power quality is adequately addressed. A constraint in selection and sizing of equipment and accessories cannot result in a massive capital damage associated with financial loss as a result of lost production, resulting in huge capital damage.

- Further, a large portion of modern life is comprised of steel. Infrastructure, buildings, machinery, electrical equipment, automobiles, and various products, from cookware to furniture, require large amounts of iron and steel. It is estimated that the steel demand will increase by five times by 2050.

- The world has built an enormous capacity for iron and steel during its modernization process. According to World Steel Association, in 2022, the steel production was around 1,885 million tons (MT), with an increase of around 20.6% from 2012.

- As a result of various policy, indigenous manufacturing will be encouraged by widening the manufacturing base, sharing know-how, product development, and technological transfer through a multilateral collaboration process.

- For instance, in October 2022, AMNS India, an arm of ArcelorMittal, announced an investment of USD 7.62 billion in its Hazira steel plant in India. This investment is expected to increase the plant's capacity to 15 million tons, which is currently 9 million tons. Additionally, the investment will include the installation of new steel-making technologies, the setting up of new-age machinery, and the expansion of product offerings.

- In July 2022, Indonesia's Krakatau Steel and South Korea's POSCO Holdings agreed to invest USD 3.5 billion in expanding their steel production capacity in Indonesia. KRAKATAU POSCO's production capacity for upstream and downstream products will be increased to 10 million tonnes per year under the agreement. Starting in 2023, the expansion includes manufacturing automotive steel for electric vehicles.

- Considering the developments and investments in the steel and iron industry in the region, the demand for capative power plants is expected to witness significant growth during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is expected to dominat the captive power plant market in 2022, and is expected to continue its dominance in the coming years as well. Factors such as growing population, rapid urbanization, and industrialization are driving the power demand in the region, creating significant opportunities for capacity expansion.

- In terms of GDP, China is the second-largest economy in the world. In 2022, the country's GDP grew by about 0.8%, reaching USD 17.96 trillion. The growth in the country is gradually diminishing as the aging population, manufacturing to services, and external to internal demand, and the economy is rebalancing from investment to consumption.

- China is expected to be one of the largest and fastest-growing markets for captive power plants, owing to the significant growth in its chemical, oil & gas, metals processing, and other sectors. Further, it is expected to continue to witness similar growth during the forecast period, as captive power plants play a crucial role in these industries.

- The iron and Steel industry is a significant market for captive power plants. According to World Steel Association, in 2022, the steel production in China was approximately 1,018 million tons, around 54% of the global steel production.

- Further, the petrochemical industry is a significant contributor to China's economy and a key field for supporting the high-quality development of the manufacturing sector. Recently, China is witnessing developments in the petrochemical sector. For instance, in March 2023, Aramco and joint venture partners Panjin Xincheng Industrial Group and NORINCO Group announced plans to start the construction of a significant integrated refinery and petrochemical complex in northeast China. The complex is going to have combination of a 300,000 barrels per day refinery and a petrochemical plant with an annual production capacity of 1.65 million tons of ethylene and 2 million metric tons of paraxylene. Construction is expected to start in the second quarter of 2023 after the project has secured administrative approvals. It is expected to be fully operational by 2026.

- South Korea is also investing in its petrochemical business which is anticipated to create a rising demand for captive power plants. In November 2022, Saudi Aramco announced investment plans for about USD 7 billion at a South Korean affiliate's factory in the port city of Ulsan to produce more high-value petrochemical products. According to the company, the Shaheen project is Saudi's biggest investment in the Asian nation to develop one of the world's largest refinery-integrated petrochemical steam crackers.

- Hence, with these trends from the steel, and petrochemical industries, the demand for captive power plants is anticipated to increase significantly during the forecast period.

Captive Power Plant Industry Overview

The captive power plant market is consolidated. Some of key players in this market (not in particular order) include Kohler Co., General Electric Company, Wartsila Oyj Abp, Bharat Heavy Electricals Limited, and Siemens AG., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Power Demand across Industrial Sector

- 4.5.1.2 Remote Location of Several Industries and the Unreliability of the Power Supply

- 4.5.2 Restraints

- 4.5.2.1 High Capital and Operational Expenditures

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Fuel Source

- 5.1.1 Coal

- 5.1.2 Gas

- 5.1.3 Diesel

- 5.1.4 Renewable

- 5.1.5 Other Fuel Sources

- 5.2 Industry

- 5.2.1 Cement

- 5.2.2 Steel

- 5.2.3 Metal & Minerals

- 5.2.4 Petrochemicals

- 5.2.5 Others

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Kohler Co.

- 6.3.2 General Electric Company

- 6.3.3 Wartsila Oyj Abp

- 6.3.4 Siemens AG

- 6.3.5 Bharat Heavy Electricals Limited

- 6.3.6 Tata Power Renewable Energy

- 6.3.7 AMP Solar Group Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Expansion of Energy Intensive Industries in African Countries such as Nigeria, Angola, And Ghana