|

市場調査レポート

商品コード

1431572

航空におけるGPSおよびGNSS受信機- 市場シェア分析、産業動向と統計、成長予測(2024年~2029年)GPS And GNSS Receivers In Aviation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空におけるGPSおよびGNSS受信機- 市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

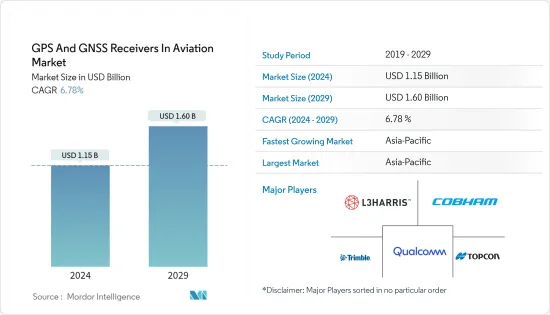

航空におけるGPSおよびGNSS受信機市場規模は、2024年に11億5,000万米ドルと推定され、2029年には16億米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは6.78%で成長すると予測されます。

主なハイライト

- 航空市場の全地球測位システム(GPS)および全地球航法衛星システム(GNSS)受信機は、COVID-19の大流行によりかつてない課題を目の当たりにしました。低成長、航空旅客数の減少、航空業務の減少により、民間機と軍用機の需要が低迷しました。

- さらに、ボーイング737 MAX型機の着陸により、ワイドボディ機とナローボディ機の受注成長率が低下していました。とはいえ、この低迷は一時的なものであり、航空機の相手先商標製品メーカー(OEM)や整備・修理・オーバーホール(MRO)サービス・プロバイダーの両方からこのような機器に対する需要があるため、市場は力強い成長を示すと予想されました。

- 民間航空機で使用するために設計されたGPS機器のほとんどは、試験済みで承認された場所に適切な電源とともに恒久的に設置され、他のフライト・システムと統合されています。航空ナビゲーション・システムは通常、移動地図ディスプレイを備えており、多くの場合、エンルート航法用の自動操縦装置に接続されています。航空産業の成長と新しい航空機のイントロダクション伴い、迅速で手間のかからない航空機ナビゲーションに対する需要が、予測期間中に航空市場におけるGPSおよびGNSSレシーバーの需要を押し上げるでしょう。

航空におけるGPSおよびGNSS受信機の市場動向

軍事航空セグメントは予測期間中に最も高いCAGRで成長すると予測される

- 軍事航空セグメントは、予測期間中に大きな成長を示すと予想されます。この成長は、すべての地域の政府による軍事費の増加、新しい軍用機に対する需要の高まり、軍事近代化プログラムの増加によるものです。衛星ナビゲーションは、敵地でのナビゲーション目的の軍事任務遂行に非常に重要であり、夜間任務で光がない場合には特に重要です。軍隊は、自軍の部隊の正確な位置と敵軍の位置を把握するために、GNSSとGPSに大きく依存しています。

- 軍隊が効率的に任務を遂行するのに役立つため、いくつかの防衛機関もGPSとGNSS技術に依存しています。米国、中国、インド、英国、ロシア、フランスは現在、それぞれ世界最大の軍事支出国です。2021年8月、BAE Systems plcは、妨害やなりすましに強い次世代Mコード軍用GPSと互換性のある超小型MicroGRAM-M全地球測位システム・レシーバーを発表しました。MicroGRAM-Mは、サイズに制約のあるその他のマイクロ・アプリケーション向けの世界最小、最軽量、最も電力効率の高いGPSレシーバーです。

- 各国は、軍用機の近代化のために軍事予算を増やしています。軍用機の増加に伴い、GPSおよびGNSSレシーバーの需要も予測期間中に増加するでしょう。

アジア太平洋地域は予測期間中に著しい成長を示す

- アジア太平洋地域は、予測期間中に最も高い成長を示すと予測されています。航空分野への支出の増加と、特に中国とインドからの新しい航空機に対する需要の増加が、この地域の市場成長を後押ししています。国際航空運送協会(IATA)によると、中国は2022年に米国を抜いて世界最大の航空市場になります。さらに、中国は2036年までに航空旅客数が15億人に達すると予想されています。

- また、インド民間航空省は、インドが2021年に国内航空市場第3位になると発表しました。さらに、インド、中国、日本からの次世代戦闘機の調達は、市場の成長を促進すると思われます。民間および軍用航空機の増加に伴い、ナビゲーション・デバイス、特にGPSとGNSSの需要も増加し、市場の成長につながります。

- 例えば、2021年12月、ロシアの宇宙機関ロスコスモスと中国の衛星航法システム委員会は、ロシアのGLONASSと中国のBeiDouというナビゲーションシステムの開発と、両国の領土に地上ベースの測定サイトを設置するための協定に調印しました。このように、アジア諸国からの民間機や軍用機の需要の高まりが、市場の成長を後押ししています。

航空におけるGPSおよびGNSS受信機の概要

航空市場におけるGPSおよびGNSSレシーバは、少数のプレイヤーが市場で重要なシェアを保持している性質上、適度に統合されています。著名な市場プレイヤーには、Cobham Limited、Trimble Inc.、Qualcomm Technologies, Inc.、L3Harris Technologies, Inc.、Topcon Positioning Systems, Inc.などがいます。この市場に参入しているこれらの大手企業は、M&A、研究開発投資、提携、パートナーシップ、地域事業拡大、新製品投入など、さまざまな戦略を採用しています。

例えば、2020年11月、Cobham Aerospace Connectivity社は、MQ-1C ER Gray Eagle Extended Range(GE-ER)無人航空機システム(UAS)プラットフォームにアンチジャムGPSシステムを提供するため、General Atomics Aeronautical Systems, Inc.(GA-ASI)と米国陸軍に選定されました。さらに、L3 Harrisは、高度なナビゲーションおよびタイミングペイロード技術の開発と統合により、次世代GPS III衛星コンステレーションを構築しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 用途別

- 民間航空

- 軍用機

- タイプ別

- 有線レシーバー

- 無線レシーバー

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- 企業プロファイル

- Trimble Inc.

- Topcon Positioning Systems, Inc.

- Broadcom, Inc.

- Hexagon AB

- Garmin Ltd.

- Tallysman

- NavtechGPS

- L3 Harris Technologies, Inc.

- Cobham Limited

- Qualcomm Technologies, Inc.

第7章 市場機会と今後の動向

The GPS And GNSS Receivers In Aviation Market size is estimated at USD 1.15 billion in 2024, and is expected to reach USD 1.60 billion by 2029, growing at a CAGR of 6.78% during the forecast period (2024-2029).

Key Highlights

- The global positioning system (GPS) and global navigation satellite system (GNSS) receivers in the aviation market witnessed unprecedented challenges due to the COVID-19 pandemic. The demand for commercial and military aircraft slumped due to low economic growth, a decrease in air traffic passengers, and a decline in aviation operations.

- Moreover, there had been a decrease in the growth rate of wide-body aircraft and narrow-body aircraft orders owing to the grounding of the Boeing 737 MAX aircraft. Nevertheless, the slump was temporary, and the market was anticipated to witness robust growth due to the demand for such equipment both from aircraft original equipment manufacturers (OEMs) and maintenance, repair, and overhaul (MRO) service providers.

- Most of the GPS equipment designed for use in commercial aircraft is permanently installed in tested and approved locations with appropriate power supplies and is integrated with other flight systems. Air navigation systems usually have a moving map display and are often connected to the autopilot for en-route navigation. With the growth of the aviation industry and the introduction of new aircraft to the fleet, the demand for quick and hassle-free aircraft navigation will boost the demand for GPS and GNSS Receivers in the Aviation market during the forecast period.

GPS And GNSS Receivers In Aviation Market Trends

Military Aviation Segment is Anticipated to Grow with the Highest CAGR During the Forecast Period

- The military aviation segment is expected to show significant growth during the forecast period. The growth can be attributed to the increasing military expenditure by governments of all regions, rising demand for new military aircraft, and growing military modernization programs. Satellite navigation is very crucial for carrying out military missions for navigation purposes in enemy territories and is especially important in the absence of light in night missions. The military forces heavily rely on GNSS and GPS in order to obtain an accurate positioning of their own units, as well as the enemy force's positions.

- Several defense bodies also depend on GPS and GNSS technologies as it helps the forces to efficiently conduct their missions. The United States, China, India, the UK, Russia, and France are currently the world's largest military spenders, respectively. In August 2021, BAE Systems plc unveiled its ultra-small MicroGRAM-M global positioning system receiver compatible with next-generation M-Code military GPS that is resistant to jamming and spoofing. MicroGRAM-M is the world's smallest, lightest, and most power-efficient GPS receiver for size-constrained and other micro-applications.

- Countries are increasing their military budgets in order to modernize their military aircraft fleet. With the rise in military aircraft, the demand for GPS and GNSS receivers will also increase during the forecast period.

Asia Pacific Will Showcase Remarkable Growth During the Forecast Period

- Asia-Pacific is projected to show the highest growth during the forecast period. Growing expenditure on the aviation sector and growing demand for new aircraft, especially from China and India, boost the market growth across the region. According to the International Air Transport Association (IATA), China surpassed the United States and became the largest aviation market in the world in 2022. Furthermore, China is expected to reach a total of 1.5 billion aviation passengers by 2036.

- Also, the Indian civil aviation ministry announced that India would become the third-largest domestic aviation market in 2021. Furthermore, the procurement of next-generation fighter jets from India, China, and Japan will propel the growth of the market. As the aircraft fleet commercial and military increases, the demand for navigation devices, particularly GPS and GNSS, will also increase, leading to the growth of the market.

- For instance, in December 2021, Russian space agency Roscosmos and the Chinese Satellite Navigation System Commission signed an agreement for the development of navigation systems, Russia's GLONASS and China's BeiDou, and installing ground-based measuring sites on the territory of both states. Thus, the growing demand for commercial and military aircraft from Asian countries drives the growth of the market.

GPS And GNSS Receivers In Aviation Industry Overview

The GPS and GNSS Receivers in the Aviation Market are moderately consolidated in nature, with few players holding significant shares in the market. Some prominent market players are Cobham Limited, Trimble Inc., Qualcomm Technologies, Inc., L3Harris Technologies, Inc., and Topcon Positioning Systems, Inc. These major players operating in this market have adopted various strategies comprising mergers and acquisitions, investment in R&D, collaborations, partnerships, regional business expansion, and new product launches.

For instance, in November 2020, Cobham Aerospace Connectivity was selected by the General Atomics Aeronautical Systems, Inc. (GA-ASI) and the U.S. Army to provide the anti-jam GPS systems for the MQ-1C ER Gray Eagle Extended Range (GE-ER) Unmanned Aircraft System (UAS) platform. In addition, L3 Harris is building the next-generation GPS III satellite constellation by developing and integrating advanced navigation and timing payload technologies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 End-Use

- 5.1.1 Commercial Aviation

- 5.1.2 Military Aviation

- 5.2 Type

- 5.2.1 Wired Receivers

- 5.2.2 Wireless Receivers

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Trimble Inc.

- 6.1.2 Topcon Positioning Systems, Inc.

- 6.1.3 Broadcom, Inc.

- 6.1.4 Hexagon AB

- 6.1.5 Garmin Ltd.

- 6.1.6 Tallysman

- 6.1.7 NavtechGPS

- 6.1.8 L3 Harris Technologies, Inc.

- 6.1.9 Cobham Limited

- 6.1.10 Qualcomm Technologies, Inc.