|

市場調査レポート

商品コード

1431571

航空宇宙用フッ素樹脂:市場シェア分析、産業動向、成長予測(2024~2029年)Aerospace Fluoropolymers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空宇宙用フッ素樹脂:市場シェア分析、産業動向、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

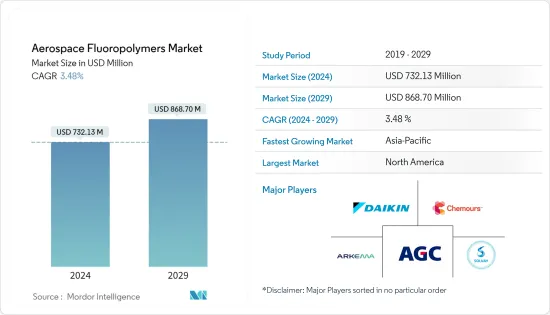

航空宇宙用フッ素樹脂市場規模は、2024年に7億3,213万米ドルと推定され、2029年には8億6,870万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは3.48%で成長する見込みです。

主なハイライト

- 2020年のCOVID-19パンデミック時に生じたサプライチェーンの混乱と航空機の受注残は、航空宇宙用フッ素樹脂市場に大きな影響を与えました。大手フッ素樹脂メーカー(OEM)は、エンドユーザーからの需要が減少したため生産量を減らさざるを得ず、収益源が細り、小規模な市場企業にとっては持続可能性の問題が浮上しました。しかし、COVID以後は、航空セクターの回復により需要が急拡大し、航空宇宙用途でのふっ素樹脂の使用増加が予想されるため、今後も堅調に推移するとみられます。

- フッ素樹脂は、航空機のようなエンドユーザー・プラットフォームをより安全で燃費の良いものにするユニークな特性を持っているため、航空宇宙産業から高い需要があります。高い耐久性と、熱、特殊燃料、湿度、エンジン振動に対する効果的な保護は、航空宇宙および航空宇宙部品メーカーの目を引いているフッ素樹脂の特性の一部です。また、フッ素樹脂が他の材料に比べて軽量であることも、航空宇宙分野でフッ素樹脂の採用が進んでいる理由です。しかし、フッ素樹脂の中にはコストが高いものもあり、これが市場成長の妨げになる可能性があります。

航空宇宙用フッ素樹脂市場の動向

予測期間中、民間航空セグメントが市場をリードする見込み

- 今後数年間は、民間航空プラットフォームが市場をリードすると予想されます。2020年には、COVID-19パンデミックにより民間航空機の納入が減少しました。しかし、2021年には航空機納入が改善し、エアバスやボーイングなどの主要民間航空機OEMは航空機の生産と納入率を向上させました。渡航制限の解除に伴い、航空旅客輸送量は改善し始めました。

- 航空旅客数の増加に伴い、航空会社はすべての主要路線で運航を開始し、新規路線も追加しました。ユナイテッド航空は新路線の就航を発表し、"最大規模の大西洋横断路線の拡大"と表現しました。すべてが平常に戻り、新しい航空会社も運航を開始しました。インドの新しい航空会社アカサ航空は2022年8月に運航を開始し、週28便の1路線からスタートし、徐々に2路線を追加しました。

- 2022年10月、アラスカ航空はボーイングB737 MAXを52機発注し、機材拡大を計画しています。同航空は、2023年末までに全機ボーイング製のメインライン機材を導入する計画を発表しました。民間航空機の増産に伴い、フッ素樹脂の需要も増加し、市場の成長が見込まれます。

予測期間中に最も高いCAGRで推移するのはアジア太平洋地域

- アジア太平洋地域は、フッ素樹脂市場の評価期間中に著しい成長を遂げると予想されます。アジア太平洋は、長年にわたって航空産業の重要な拠点となっています。インドや中国のようなこの地域の新興国は、航空需要の増加により、それぞれの民間航空市場で大きな躍進を経験しています。中国は、大きな内需によって世界の民間航空市場の回復をリードしており、航空会社の財政回復に貢献しています。

- ボーイング社によると、中国は国内航空旅客輸送量の増加により航空業界最大の市場となっており、北米地域を上回り、2040年までに4.4%の急成長が見込まれています。近隣諸国間の緊張に起因する域内諸国の軍事費の増加や、オーストラリアのような国に軍事基地局を配置するために投資する諸外国に伴い、アジア太平洋地域の軍事航空も増加しています。

- 中国は軍事航空能力を高めており、2022年10月には世界初の双座ステルス戦闘機であるJ-20の新型ステルス戦闘機が発表されました。また、アジア太平洋諸国は人件費が安いためコスト面で優れ、製造能力を整えるための投資も少なくて済みます。このように、アジア太平洋地域では航空宇宙産業が急速に発展しているため、航空宇宙用フッ素樹脂市場は今後も成長を続けると思われます。

航空宇宙用フッ素樹脂産業の概要

航空宇宙用フッ素樹脂市場は元来、統合型です。Daikin Industries、The Chemours Company、AGC Group、Arkema S.A.、Solvay S.A.が、この市場における有力な企業です。これらの大手企業は、この市場での地位を強化するために、M&A、新製品の発売、事業拡大、契約、合弁事業、パートナーシップなど、さまざまな有機的・無機的成長戦略を採用しています。

しかし、航空宇宙用フッ素樹脂市場で機能する中小企業もいくつか存在します。各社は顧客基盤を増やすため、あらゆる地域で存在感を高めようとしています。例えば、2021年3月、アルケマは常熟(中国)のフッ素樹脂生産能力をさらに35%増強するために投資を増やすと発表しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- プラットフォーム

- 民間航空

- 一般航空

- 軍用機

- 樹脂タイプ

- PTFE

- ETFE

- PFA

- FKM

- その他の樹脂タイプ

- タイプ

- パウダー

- ペレット

- 分散液

- 成分タイプ

- シール

- ワイヤー&ケーブル

- ホース&チューブ

- フィルム

- コーティング

- その他の部品

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- 企業プロファイル

- Daikin Industries, Ltd.

- The Chemours Company

- AGC Group

- Arkema S.A.

- Solvay S.A.

- Fluorotherm

- Plastics Europe

- Dongyue Group

- The 3M Company

- HaloPolymer, OJSC

- Saint-Gobain Group

第7章 市場機会と今後の動向

The Aerospace Fluoropolymers Market size is estimated at USD 732.13 million in 2024, and is expected to reach USD 868.70 million by 2029, growing at a CAGR of 3.48% during the forecast period (2024-2029).

Key Highlights

- The supply chain disruption and aircraft order backlogs caused during the COVID-19 pandemic in 2020 greatly affected the aerospace fluoropolymers market. Major fluoropolymer original equipment manufacturers (OEMs) had to reduce their production rate due to less demand from the end-users, leading to trickling revenue streams and raising sustainability issues for small market players. However, post-COVID, the demand witnessed rapid growth due to the recovery demonstrated by the aviation sector and was likely to remain robust as the use of fluoropolymers is expected to increase in aerospace applications.

- Fluoropolymers have been witnessing high demand from the aerospace industry due to their unique properties that make end-user platforms such as aircraft safer and more fuel-efficient. High durability and effective protection against heat, specialty fuels, humidity, and engine vibrations, are a few of those characteristics of fluoropolymers that are catching the eyes of aerospace and aerospace component manufacturers. In addition, the lightweight nature of fluoropolymers in comparison to other materials is another reason leading to the greater adoption of fluoropolymers in aerospace. However, the costs of some of the fluoropolymer resins are at the higher end, which can act as a hindrance to market growth.

Aerospace Fluoropolymers Market Trends

Commercial Aviation Segment is Expected to Lead the Market During the Forecast Period

- The commercial aviation platform is expected to lead the market in the years to come. In 2020, there was a decline in commercial aircraft deliveries due to the COVID-19 pandemic. However, aircraft deliveries improved in 2021, and the major commercial aircraft OEMs, like Airbus and Boeing, increased their aircraft production and delivery rates. With the lifting of travel restrictions, air passenger traffic started to improve.

- With the increase in air passenger traffic, airlines have started operating on all major routes and have also added new routes. United Airlines has announced that it has started operating on new routes, describing it as its "largest transatlantic expansion." With everything returning to normal, new airlines have started operations. Akasa Air, a new Indian airline, started its operations in August 2022, starting with one route with 28 flights a week and gradually adding two more routes.

- In October 2022, Alaska Airlines placed an order for 52 Boeing B737 MAX aircraft with a plan to expand its fleet. The airline announced plans to have an all-Boeing mainline fleet by the end of 2023. With the increase in the production of commercial aircraft, the demand for fluoropolymers will also increase, resulting in the growth of the market.

Asia Pacific to Register the Highest CAGR During the Forecast Period

- Asia-Pacific is anticipated to witness tremendous growth over the assessment period in the fluoropolymers market. Asia-Pacific has become a significant hub for the aviation industry over the years. The emerging economies in the region, like India and China, are experiencing a massive surge in their respective commercial aviation markets due to an increased demand for air travel. China is leading the recovery of global commercial aviation due to great domestic demand, helping the airlines witness financial recovery.

- China is the largest market in aviation due to an increase in domestic air passenger traffic, which has surpassed the North American region and is expected to grow rapidly at a rate of 4.4% by 2040, according to Boeing. With the increase in military spending of the countries in the region due to tensions between neighboring countries and with foreign nations investing in arranging military base stations in countries like Australia, military aviation in the Asia-Pacific region is also increasing.

- China is increasing its military airborne capabilities, and a new stealth fighter aircraft, the new version of the J-20, which is the world's first twin-seat stealth fighter aircraft, was unveiled in October 2022. In addition, countries in the Asia-Pacific are cost-friendly due to the low cost of labor and require low investments to set up manufacturing capabilities. Thus, due to the rapidization of the aerospace industry in Asia Pacific, the aerospace fluoropolymers market will continue to experience growth in the region.

Aerospace Fluoropolymers Industry Overview

The aerospace fluoropolymers market is consolidated in nature. Daikin Industries, Ltd., The Chemours Company, AGC Group, Arkema S.A., and Solvay S.A. are the prominent players in the market. These major players have adopted various organic as well as inorganic growth strategies such as mergers & acquisitions, new product launches, expansions, agreements, joint ventures, partnerships, and others to strengthen their position in this market.

However, there are several smaller players that function in the aerospace fluoropolymers market. The companies are trying to increase their presence across all regions to increase their customer base. For example, in March 2021, Arkema announced to increase its investment to further increase its fluoropolymer production capacities in Changshu (China) by 35%.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Platform

- 5.1.1 Commercial Aviation

- 5.1.2 General Aviation

- 5.1.3 Military Aviation

- 5.2 Resin Type

- 5.2.1 PTFE

- 5.2.2 ETFE

- 5.2.3 PFA

- 5.2.4 FKM

- 5.2.5 Other Resin Types

- 5.3 Type

- 5.3.1 Powder

- 5.3.2 Pellets

- 5.3.3 Dispersions

- 5.4 Component Type

- 5.4.1 Seals

- 5.4.2 Wires & Cables

- 5.4.3 Hoses & Tubes

- 5.4.4 Films

- 5.4.5 Coatings

- 5.4.6 Other Component Types

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia Pacific

- 5.5.4 Latin America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of Latin America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Daikin Industries, Ltd.

- 6.1.2 The Chemours Company

- 6.1.3 AGC Group

- 6.1.4 Arkema S.A.

- 6.1.5 Solvay S.A.

- 6.1.6 Fluorotherm

- 6.1.7 Plastics Europe

- 6.1.8 Dongyue Group

- 6.1.9 The 3M Company

- 6.1.10 HaloPolymer, OJSC

- 6.1.11 Saint-Gobain Group