|

市場調査レポート

商品コード

1431568

衛星ペイロード:市場シェア分析、産業動向、成長予測(2024年~2029年)Satellite Payload - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 衛星ペイロード:市場シェア分析、産業動向、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

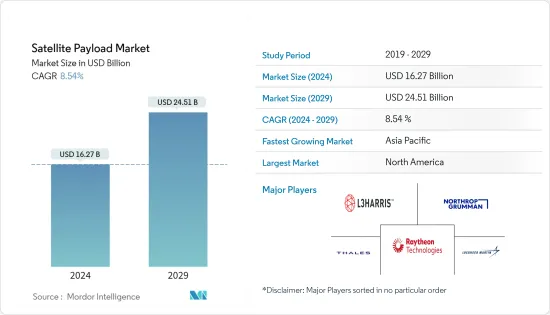

衛星ペイロード市場規模は2024年に162億7,000万米ドルと推定され、2029年には245億1,000万米ドルに達し、予測期間中(2024-2029年)にCAGR 8.54%で成長すると予測されます。

主なハイライト

- 衛星ペイロード市場は、COVID-19パンデミックによる比類なき課題を目の当たりにしました。パンデミックはサプライチェーンの混乱を招き、衛星やその他の宇宙プログラムの打ち上げ遅延につながった。製造業の生産停止は部品不足を引き起こし、物品の輸出入に関連する政府の厳しい規制は衛星の製造と打ち上げをさらに遅らせた。

- さらに、衛星打上げサービスや衛星製造は、中国や韓国などでの製造停止によるコンピュータ・チップ不足の影響も受けました。しかし、COVID後は、衛星打ち上げ数の増加と宇宙分野への支出増により、市場は力強い回復を見せた。

- 商業用や軍事用など、地球観測、通信、画像処理など数多くの用途に向けた小型衛星打ち上げ数の増加が、市場の成長を後押ししています。

- 宇宙分野への支出の増加、宇宙探査活動の増加、衛星打ち上げ数の増加が市場成長を促進します。2022年、宇宙計画のための世界政府支出は過去最高の約1,030億米ドルに達しました。さらに、高速通信サービスのための衛星コンステレーションの採用が増加し、世界中の政府、宇宙機関、研究機関による支出が増加していることが、今後数年間の市場成長を促進します。

衛星ペイロード市場動向

予測期間中、商業セグメントが著しい成長を見せる見込み

- 商用セグメントは予測期間中に著しい成長を示すと思われます。この成長は、商業用途で打ち上げられる衛星の数が増加しているためです。Satellite Industry Association(SIA)は、第26回年次衛星産業状況報告書(SSIR)を発表し、商業衛星産業は5年連続で過去最多の商業衛星を軌道に打ち上げたと述べています。SSIRによると、2022年には合計2,325機の商業衛星が投入され、2021年と比較して35%以上増加しました。

- さらに、いくつかの新興企業は、高速通信、ナビゲーション、画像サービスを提供するために超小型衛星コンステレーションに投資しています。L3Harris TechnologiesのSpaceView画像ペイロードの製品ラインは、農業、林業、鉱業、石油・ガス、地図作成、都市計画など様々なミッションのサポートに使用されています。

- 例えば、2023年5月、宇宙インフラと軌道輸送サービスを提供する米国の商業宇宙企業であるMomentus Inc.は、衛星技術企業のHello Spaceと、SpaceX Transporter-9ミッションでの打ち上げを目標としたVigoride-7ミッションで、4基のpocketqube衛星を搭載したデモデプロイヤーのホストペイロードを運ぶ契約を締結しました。このような動きは、予測期間中の商用セグメントの成長を促進すると思われます。

予測期間中、北米が市場の著しい成長を示す

- 北米は衛星ペイロード市場で最も高いシェアを占めており、予測期間中もその支配を維持します。この成長は、様々なアプリケーションのための衛星ペイロードの需要増加と、SpaceX、NASA、その他が実施したデジタルペイロードの技術進歩によるものです。米国は宇宙開発への投資額が最も高く、2022年の投資額は約620億米ドルでした。

- また、米国は2021年の世界の宇宙飛行活動への支出546億米ドルの半分以上を占めています。総投資額のうち、半分はNASAや商業宇宙支援などの民間宇宙飛行活動に投資され、残りの半分は空軍、宇宙軍、その他の国防総省の防衛活動に使われました。

- 例えば、2022年3月、米国宇宙軍はThe Boeing Companyが開発した衛星通信ペイロードの重要設計審査に合格しました。2020年、The Boeing CompanyとNorthrop Grumman Corporationは、それぞれ1億9,100万米ドルと2億5,300万米ドルの別々の契約を獲得し、米国宇宙軍の保護戦術衛星通信(PTS)プログラムのペイロードを設計しました。このように、宇宙プログラムへの支出の増加、軍事・商業用途の衛星打ち上げ数の増加が、この地域全体の市場成長を牽引しています。

衛星ペイロード産業概要

衛星ペイロード市場は、少数の企業が市場で大きなシェアを占めており、その性質上、適度に統合されています。主なプレイヤーとしては、RTX Corporation、Northrop Grumman Corporation、Lockheed Martin Corporation、THALES、L3Harris Technologies Inc.などが挙げられます。主なOEMは、研究開発と革新的な技術に高度に投資しています。この点に関して、2022年7月、インドの宇宙状況認識企業であるDigantaraは、同社の宇宙気象監視ペイロードROBIが、インドの極衛星ロケットの使用済み上段で運用開始されたと発表しました。同社によると、この実験ペイロードは、2022年6月に打ち上げられたPSLVの軌道実験プラットフォーム(POEM)からのデータの共有に成功しました。主要企業のこうした発展は、今後数年間の市場成長を後押しすると思われます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- ペイロードの種類

- 通信

- ナビゲーション

- イメージング

- その他

- 軌道

- ジオ

- MEO

- LEO

- 用途

- 商業

- 軍事

- 用途

- 気象モニタリング

- 通信

- 監視

- 科学調査

- その他の用途

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- 企業プロファイル

- RTX Corporation

- Lockheed Martin Corporation

- THALES

- Northrop Grumman Corporation

- L3Harris Technologies Inc.

- Honeywell International Inc.

- The Boeing Company

- Airbus SE

- ISRO

- General Dynamics Corporation

- Space Exploration Technologies Corp.

- Sierra Nevada Corporation

第7章 市場機会と今後の動向

The Satellite Payload Market size is estimated at USD 16.27 billion in 2024, and is expected to reach USD 24.51 billion by 2029, growing at a CAGR of 8.54% during the forecast period (2024-2029).

Key Highlights

- The satellite payload market witnessed unparalleled challenges due to the COVID-19 pandemic. The pandemic resulted in supply-chain disruptions, leading to delayed launches of satellites and other space programs. Production halts in manufacturing caused a shortage of components, and stringent government regulations associated with the import and export of goods further delayed the manufacturing and launch of satellites.

- Additionally, satellite launch services and satellite manufacturing were also impacted by computer chip shortages resulting from manufacturing shutdowns in countries like China and South Korea. However, the market showed a strong recovery post-COVID due to a growing number of satellite launches and increased spending on the space sector.

- A growing number of small satellite launches for numerous applications, such as commercial and military applications, which include Earth observation, telecommunication, and imaging, drive the growth of the market.

- Increasing expenditure on the space sector, the rising number of space exploration activities, and a growing number of satellite launches drive the market growth. In 2022, global government expenditure for space programs reached a record high of approximately USD 103 billion. Furthermore, the rising adoption of satellite constellations for high-speed communication services and increasing expenditure by governments, space agencies, and research organizations across the world will drive market growth in the coming years.

Satellite Payload Market Trends

Commercial Segment is Expected to Show Significant Growth During the Forecast Period

- The commercial segment will showcase remarkable growth during the forecast period. The growth is due to the increasing number of satellites launched for commercial applications. The Satellite Industry Association (SIA) has released its 26th annual State of the Satellite Industry Report (SSIR), which stated that the commercial satellite industry launched a record number of commercial satellites into orbit for a fifth consecutive year. According to the SSIR, a total of 2,325 commercial satellites were deployed in 2022, an increase of over 35 percent compared to 2021.

- Furthermore, several startups are investing in nanosatellite constellations to offer high-speed communication, navigation, and imaging services. The L3Harris Technologies' line of SpaceView imaging payloads is used to support various missions, including agriculture, forestry, mining, oil and gas, mapping, and urban planning.

- For instance, in May 2023, Momentus Inc., a US commercial space company that offers in-space infrastructure and orbital transportation services, signed an agreement with Hello Space, a satellite technology company, to carry a hosted payload of a demo deployer carrying four pocketqube satellites on the Vigoride-7 mission targeted to launch on the SpaceX Transporter-9 mission. Such developments will drive the growth of the commercial segment during the forecast period.

North America Will Showcase Significant Growth in the Market During the Forecast Period

- North America holds the highest shares in the satellite payload market and continue its domination during the forecast period. The growth is attributed to the increasing demand for satellite payloads for various applications and technological advancements in digital payloads carried out by SpaceX, NASA, and others. The US was the highest spender on space programs, with an approximate investment of USD 62 billion in 2022.

- Also, the United States accounted for more than half of the global spending of USD 54.6 billion in 2021 on spaceflight activities. Out of the total investment, half of the amount was invested in civil spaceflight activities such as NASA and supporting commercial space, and the other half went to defense programs in the Air Force, Space Force, and other parts of the Department of Defense.

- For instance, in March 2022, the US Space Force passed a critical design review of a satellite communication payload developed by Boeing. In 2020, The Boeing Company and Northrop Grumman Corporation won separate contracts worth USD 191 million and USD 253 million, respectively, to design payloads for the Protected Tactical Satcom (PTS) program of the US space force, a planned network of jam-resistant geostationary satellites for military classified and unclassified communications. Thus, growing expenditure on space programs and a rising number of satellite launches for military and commercial applications drive the growth of the market across the region.

Satellite Payload Industry Overview

The satellite payload market is moderately consolidated in nature, with the presence of a few players holding significant shares in the market. Some of the key players in the market are RTX Corporation, Northrop Grumman Corporation, Lockheed Martin Corporation, THALES, L3Harris Technologies Inc., and others. The key OEMs highly invest in research and development and innovative technologies. On this note, in July 2022, Digantara, an India-based space situational awareness company, announced its space weather monitoring payload ROBI is operational onboard a spent upper stage of India's Polar Satellite Launch Vehicle. The company said that the experimental payload successfully shared data from PSLV's Orbital Experimental Platform (POEM), which was launched in June 2022. Such developments from key players will boost market growth in the coming years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Payload Type

- 5.1.1 Communication

- 5.1.2 Navigation

- 5.1.3 Imaging

- 5.1.4 Others

- 5.2 Orbit

- 5.2.1 GEO

- 5.2.2 MEO

- 5.2.3 LEO

- 5.3 End-Use

- 5.3.1 Commercial

- 5.3.2 Military

- 5.4 Application

- 5.4.1 Weather Monitoring

- 5.4.2 Telecommunication

- 5.4.3 Surveillance

- 5.4.4 Scientific Research

- 5.4.5 Other Applications

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Latin America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of Latin America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 RTX Corporation

- 6.1.2 Lockheed Martin Corporation

- 6.1.3 THALES

- 6.1.4 Northrop Grumman Corporation

- 6.1.5 L3Harris Technologies Inc.

- 6.1.6 Honeywell International Inc.

- 6.1.7 The Boeing Company

- 6.1.8 Airbus SE

- 6.1.9 ISRO

- 6.1.10 General Dynamics Corporation

- 6.1.11 Space Exploration Technologies Corp.

- 6.1.12 Sierra Nevada Corporation