|

|

市場調査レポート

商品コード

1431449

プラスチックフィルムコンデンサの世界市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Plastic Film Capacitors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| プラスチックフィルムコンデンサの世界市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

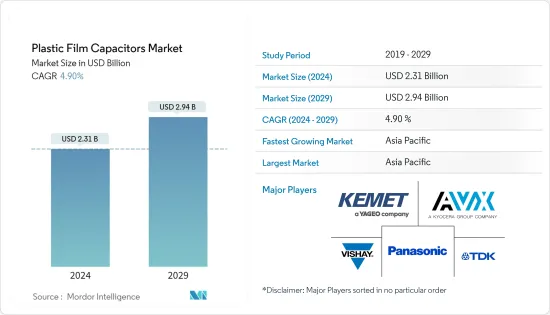

世界のプラスチックフィルムコンデンサの市場規模は、2024年に23億1,000万米ドルと推定され、2029年には29億4,000万米ドルに達し、予測期間中(2024年~2029年)にCAGR4.90%で成長すると予測されています。

プラスチックフィルムコンデンサは、主に誘電体材料として異なるプラスチックを使用する複数のコンデンサファミリーを含みます。オーディオ、ラジオ回路、低電圧から中電圧で動作する回路などの用途で、紙タイプのコンデンサを大幅に置き換えています。コンデンサによく使われるプラスチックには、ポリカーボネート、ポリプロピレン(PP)、ポリエステル(PET)、ポリスチレン、ポリスルホン、カプトン・ポリイミド、テフロン(PTFEフッ素樹脂)、金属化ポリエステル(金属化プラスチック)などがあります。

主なハイライト

- プラスチックフィルムコンデンサを使用する大きな利点は、低歪率で卓越した周波数特性を持つことです。また、これらのコンデンサに使用されるプラスチックフィルムの範囲が広いため、汎用性が高いです。これらのコンデンサはすぐに磨耗しないため、カップリング回路やデカップリング回路、オーディオ回路のADCなど、高電圧・高周波用途に適しています。

- 様々な産業で持続可能な発電ソリューションへの注目が高まる中、太陽光発電や風力発電のインバーター需要が増加しています。これに対応するため、ベンダーは新しいプラスチックフィルムコンデンサを投入しています。例えば、2021年5月、ニューヨーカー・エレクトロニクスは、薄型の金属化ポリプロピレンフィルムで製造され、高い静電容量を提供するCDE-Illinoisコンデンサ(33~220uF、最大1,440WVDC、-40ツーC~+85ツーC)を発表しました。この製品は、DCリンク、電気ヒーター、モーター駆動、誘導ヒーター、UPSシステム、太陽光・風力発電インバーターなどの用途向けに設計されています。

- さらに、ヘルスケア分野でのウェアラブルの採用は、ここ数年牽引力を増しており、これは、調査市場に影響を与える重要な要因の1つとなっています。ウェアラブル接続デバイスの主な動向としては、疼痛管理ウェアラブルデバイスの需要増加、心血管疾患管理のためのウェアラブル使用の増加などが挙げられます。

- さらに、2022年4月、エレクトロニンクス社は、同社独自の有機金属分解(MOD)導電性金属インクソリューションのフルスイートが生産規模で利用可能になったことを発表しました。エレクトロニンクスは、単体のインク製品を市場に投入するだけでなく、CircuitJetと呼ばれるオンデマンドのプリント基板(PCB)印刷・修理のための独自の小型デスクトップ試作アディティブ・マニュファクチャリング・ソリューションなど、インク製品群によるトータルソリューションを顧客に提供しています。こうした発展もまた、研究市場を牽引すると思われます。

- COVID-19の大流行は、世界の産業全体のサプライチェーンに甚大な混乱をもたらしました。ウイルスの蔓延に対抗するため、世界的に多くの企業が業務を停止または縮小しました。しかし、パンデミック後のシナリオでは、電子部品市場は、原材料と部品生産レベルのサプライチェーン全体で動作レベルの増加につながりました。これにより、さまざまな地域や国での売上が増加しました。

- さらに、電子部品は資源集約型です。表面実装型電子部品の大量生産で消費される材料は、通常、設計された粉末やペーストの形で提供され、コンデンサのような受動部品の生産に関連する最大の「変動費」を構成しています。

プラスチックフィルムコンデンサ市場動向

家電が大きな市場シェアを占める見込み

- 家電製品に対する需要の急増が市場を押し上げています。スマートフォンやタブレット端末などのデバイスは、高性能を発揮できる小型アンテナを必要としています。これらのアンテナシステムには、特定の性能特性を持つコンデンサが必要です。コンデンサはアンテナシステムにおいて重要な部品です。アンテナシステムにおけるコンデンサの最も一般的な用途には、周波数調整、インピーダンス整合、フィルタリングなどがあります。これらの用途に使用されるコンデンサには、低リーク電流、高品質係数、高直線性などの優れた性能特性が求められます。

- スマートフォンアンテナシステムの厳しい性能要件を満たすコンデンサを製造するために、コンデンサ技術の数多くの進歩がなされてきました。例えば、コンデンサ・メーカーは微小電気機械システム(MEMS)技術を利用して、スマートフォンのアンテナ・システム用の超小型・薄型コンデンサを製造しています。

- コンシューマー・テクノロジー協会によると、米国の家電市場の小売売上高は、2012年~2021年に絶えず増加しています。2023年の小売売上高予測に基づくと、米国の家電小売売上高は4,850億米ドルに達する見込みです。

- さらに、コンデンサは一般的にカメラのフラッシュモジュールに組み込まれています。カメラのフラッシュコンデンサは、低抵抗でインダクタンスが著しく低い構造になっており、フラッシュ管にエネルギーを可能な限り速く供給し、電流パルスの速い立ち上がり時間を実現しています。また、大電流による局所的な発熱を避けるため、内部接続はより堅牢に作られています。フラッシュコンデンサがなければ、デジタルカメラ内のバッテリーはすぐに消耗してしまいます。

- さらに、スマートウォッチ、ヘッドマウントディスプレイ、ボディ装着型カメラ、耳かけ型デバイス、フィットネストラッカーなどのウェアラブルエレクトロニクスの発展が、プラスチックフィルムコンデンサの技術革新と採用を後押ししています。例えば、コンデンサは、10,000サイクルの充放電後にエネルギー性能が数%ポイント低下するという耐摩耗性により、ウェアラブル家電製品に広く使用されています。

アジア太平洋が大きな市場シェアを占める見込み

- アジア太平洋は、コンデンサにとって最も重要な市場のひとつです。中国では自動車産業が増加しており、世界の自動車市場でますます重要な役割を果たしています。政府は、自動車部品部門を含む自動車産業を国の柱となる産業のひとつと見なしています。中国政府は、中国の自動車生産台数が2020年までに3,000万台、2025年までに3,500万台に達すると予測しています。これが研究用コンデンサ需要を牽引すると予想されます。

- EVの人気は高まっており、中国は電気自動車を採用する主要国のひとつと見なされています。同国の第13次5ヵ年計画では、ハイブリッド車や電気自動車など、環境に配慮した輸送ソリューションの開発が推進されており、同国の輸送セクターの発展が期待されています。

- 中国乗用車協会(CPCA)のデータによると、こうした新エネルギー自動車(NEV)の販売台数は2021年11月と12月で2倍以上に増加し、通年では169%増の299万台、世界最大の自動車市場である中国での新車販売台数の14.8%を記録しました。これは同国のプラスチックフィルムコンデンサ採用を後押しすると予想されます。

- IEAによると、中国は再生可能エネルギーの成長において文句なしのリーダーであり、2022年までにクリーン・エネルギー・ミックス全体の約40%を占めると推定されています。また、同国は2020年のソーラーパネル目標を上回りました。

- さらに、ゼロ・エミッション車の導入を促進するため、オーストラリアのニューサウスウェールズ(NSW)州政府は2021年に電気自動車戦略を導入し、総額約5億豪ドルの資金を提供しました。オーストラリアでは2021年上半期に8,688台の電気自動車が販売されました。同国では、電気自動車支援インフラも拡大しています。オーストラリアには電気自動車用の公共充電器が3,000基以上あります。同国のEV市場には31の電気自動車モデルがあり、2022年末には58の電気自動車モデルが存在すると推定されています。

プラスチックフィルムコンデンサ業界の概要

プラスチックフィルムコンデンサ市場は細分化されており、複数の大手企業が存在します。市場で大きなシェアを持つこれらの大手企業は、海外における顧客基盤の拡大に注力しています。同市場には、パナソニック株式会社、Vishay Intertechnology Inc.、TDK株式会社、AVX Corporation、KEMET Corporation、その他多数の企業が参入しています。これらの企業は、戦略的協業イニシアティブを活用して市場シェアと収益性を高めています。

- 2023年11月エレクトロキューブは、さまざまな軍事、商業、陸上、海上用途で使用されるハイパワーインバータ向けに特別に調整された金属化ポリプロピレンフィルムコンデンサを開発しました。これらのコンデンサは、AC信号やパルス信号による高温・大電流環境下でも優れた機能を発揮するよう、入念に設計・最適化されています。さらに、劣化することなく高サージ電流に耐える顕著な能力により、電解コンデンサに代わる優れた選択肢となっています。

- 2023年5月サビックのエルクレスは、ポリカーボネートコポリマーをベースとしたHTV150Aフィルムを発表しました。このフィルムは、150℃までの温度と100kHzまでの周波数にさらされた場合、散逸損失を最大40%低減できる可能性があります。この材料は、薄肉キャパシタフィルムですでにその有効性を実証しています。散逸損失の低いElcres HTV150A誘電体フィルムを利用することで、エンジニアは、動作効率の向上、内部発熱の低減、ホットスポット温度の安定化などの恩恵を受けることができ、その結果、コンデンサを設計する際の柔軟性が向上します。このフィルムは、コンデンサの損失低減につながると期待されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

- マクロ経済動向の業界への影響評価

第5章 市場力学

- 市場促進要因

- EVの登場による自動車業界の需要拡大

- エレクトロニクスの複雑化

- 市場抑制要因

- 金属価格の上昇が部品製造コストに影響

第6章 市場セグメンテーション

- タイプ

- ポリプロピレン

- ポリエチレン

- その他のタイプ(PTFE、PPSなど)

- 用途

- 自動車

- 通信

- 産業用

- 航空宇宙・防衛

- 家電

- 医療

- その他の用途

- 地域

- 南北アメリカ

- 欧州、中東・アフリカ

- アジア太平洋(日本と韓国を除く)

- 日本と韓国

第7章 競合情勢

- 企業プロファイル

- KEMET Corporation(Yageo company)

- Panasonic Corporation

- Vishay Intertechnology Inc.

- TDK Corporation

- AVX Corporation(Kyocera Corp)

- Murata Manufacturing Co. Ltd.

- Cornell Dubilier Electronics Inc.

- Desai Electronics

- Shanghai Yinyan Electronic

- Rubycon Corporation

- Nantong Jianghai Capacitor Co. Ltd.

- Nichicon Corporation

- Wima GmBH & Co. KG

第8章 投資分析

第9章 市場の将来展望

The Plastic Film Capacitors Market size is estimated at USD 2.31 billion in 2024, and is expected to reach USD 2.94 billion by 2029, growing at a CAGR of 4.90% during the forecast period (2024-2029).

Plastic Film capacitors primarily include multiple families of capacitors that use different plastics as dielectric materials. They significantly replace paper-type capacitors in applications such as audio, radio circuits, and circuits operating at low to moderate voltages. Some of the commonly used plastics in these capacitors include polycarbonate, polypropylene (PP), polyester (PET), polystyrene, polysulfone, Kapton polyimide, Teflon (PTFE fluorocarbon), and metalized polyester (metalized plastic).

Key Highlights

- The significant advantage of using a plastic film capacitor is that it has a low distortion factor and exceptional frequency characteristics. Also, the wide range of plastic films that are used for these capacitors makes them versatile. These capacitors do not wear off quickly and are suited for high-voltage and high-frequency applications such as coupling and decoupling circuits and audio circuit ADCs.

- With a rising focus on sustainable solutions across various industries for power generation, the demand for solar and wind power inverters has increased. To cater to this, vendors are introducing new plastic-film capacitors. For instance, in May 2021, New Yorker Electronics introduced CDE-Illinois capacitors (33 to 220 uF and up to 1,440 WVDC, -40°C to +85°C) that are manufactured with low-profile metalized polypropylene film and offer high capacitance. The product is designed for applications such as DC links, electric heaters, motor drives, induction heaters, UPS systems, and solar and wind power inverters.

- Moreover, the adoption of wearables in the healthcare sector has been gaining traction in recent times, which, in turn, has been one of the significant factors influencing the market studied. The major trends in wearable connected devices include the increasing demand for pain management wearable devices and the increased use of wearables for cardiovascular disease management, among others.

- Further, in April 2022, Electroninks, Inc. announced the production-scale availability of its full suite of proprietary metal-organic decomposition (MOD) conductive metal ink solutions. In addition to bringing standalone ink products to market, Electroninks is also bringing total solutions to the customer with its line of ink products, including its own small desktop prototype additive manufacturing solution for rapid on-demand printed circuit board (PCB) printing and repair, called CircuitJet. These developments will also drive the study market.

- The COVID-19 pandemic led to immense disruptions in supply chains across industries globally. Many businesses globally halted or reduced operations to help combat the spread of the virus. However, in post pandemic scenario, the electronic components market, leading to increased operation levels across the supply chain for raw materials and component production levels. This denoted a rise in sales among a range of regions and countries.

- Moreover, electronic components are resource-intensive. The materials consumed in the mass production of surface-mount electronic components usually come in the form of engineered powders and pastes, making up the largest "variable cost" associated with producing passive components like capacitors.

Plastic Film Capacitors Market Trends

Consumer Electronics is Expected to Hold Significant Market Share

- The rapid surge in demand for consumer electronics products has boosted the market. Devices such as smartphones and tablets need small antennas capable of delivering high performance. These antenna systems demand capacitors with specific performance characteristics. Capacitors are critical components in antenna systems. The most general applications of capacitors in antenna systems include frequency tuning, impedance matching, and filtering. Capacitors for use in these applications must have prominent performance characteristics, including low leakage current, a high quality factor, and high linearity.

- Numerous advancements in capacitor technology have been made to produce capacitors that meet the strict performance requirements of smartphone antenna systems. For instance, capacitor manufacturers use microelectromechanical systems (MEMS) technology to make ultra-small and thin capacitors for smartphone antenna systems.

- According to the Consumer Technology Association, the retail revenue of the consumer electronics market in the United States constantly increased during the period from 2012 to 2021. Based on the projected retail sales for 2023, consumer electronics retail sales in the United States is expected to reach USD 485 billion.

- Moreover, capacitors are commonly incorporated in the flash module of cameras. Camera flash capacitors are constructed to have low resistance and significantly low inductance to deliver their energy to the flash tube as fast as possible, achieving a fast rise time on the pulse of current. The internal connections are also made more robust to avoid localized heating due to the high current. Without the flash capacitor, the batteries located inside the digital cameras would drain quickly.

- Furthermore, developments in wearable electronics, such as smartwatches, head-mounted displays, body-worn cameras, ear-worn devices, and fitness trackers, among others, drive innovations and the adoption of plastic film capacitors. For instance, capacitors are being widely used in wearable consumer electronics due to their wear and tear capability, which exhibits a loss of a few percentage points of energy performance after 10,000 cycles of charging and discharging.

Asia-Pacific is Expected to Hold Significant Market Share

- The Asia-Pacific region is one of the most important markets for capacitors. The automotive industry is increasing in China, and the country plays an increasingly important role in the global automotive market. The government views its automotive industry, including the auto parts sector, as one of the country's pillar industries. The government of China estimates that China's automobile output is expected to reach 30 million units by 2020 and 35 million units by 2025. This is expected to drive the studied capacitors' demand.

- The popularity of EVs is growing, and China is regarded as one of the dominant adopters of electric vehicles. The country's 13th Five-Year Plan promotes the development of green transportation solutions, such as hybrid and electric vehicles, for advancements in the country's transportation sector.

- According to data by the China Passenger Car Association (CPCA), sales of these new energy vehicles (NEVs) more than doubled in November and December of 2021, increasing full-year deliveries by 169% to a record 2.99 million units, or 14.8% of new sales in China, the world's largest vehicle market. This is anticipated to boost the country's adoption of plastic film capacitors.

- According to the IEA, China was the undisputed leader in renewable growth, estimated to account for around 40% of its total clean energy mix by 2022. The country also surpassed its 2020 solar panel target.

- Additionally, to promote the adoption of zero-emission vehicles, the New South Wales (NSW) state government in Australia introduced an Electric Vehicle Strategy in 2021 with funding totaling almost AUD 500 million. 8,688 electric vehicles were sold during the first half of 2021 in Australia. The country is witnessing a growing electric vehicle support infrastructure as well. Australia has more than 3,000 public chargers for electric vehicles. The country's EV market had 31 electric vehicle models, and by the end of 2022, it was estimated that there would be 58 electric vehicle models in the country.

Plastic Film Capacitors Industry Overview

The plastic film capacitors market is fragmented and has several major players. These major players with prominent shares in the market are focusing on expanding their customer base across foreign countries. The market comprises Panasonic Corporation, Vishay Intertechnology Inc., TDK Corporation, AVX Corporation, KEMET Corporation, and many others. These companies leverage strategic collaborative initiatives to increase their market shares and profitability.

- November 2023: Electrocube has developed a range of metalized polypropylene film capacitors specifically tailored for high-power inverters used in various military, commercial, land, and sea applications. These capacitors have been carefully designed and optimized to function exceptionally well in high temperature and high current scenarios with AC and pulsing signals. Furthermore, their remarkable capability to withstand high surge currents without deterioration makes them an outstanding alternative to electrolytic capacitors.

- May 2023: Sabic's Elcres introduced its polycarbonate copolymer-based HTV150A films, which can potentially decrease dissipation losses by up to 40% when exposed to temperatures up to 150°C and frequencies up to 100 kHz. This material has already demonstrated its effectiveness in thin-wall capacitor films. By utilizing Elcres HTV150A dielectric films with lower dissipation losses, engineers can benefit from improved operating efficiency, reduced internal heat generation, and more stable hot spot temperatures, resulting in increased flexibility when designing capacitors. It is anticipated that these films will lead to reduced dissipation losses in capacitors.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of Substitute Products

- 4.2.4 Threat of New Entrants

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of Macro Economic Trends on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand from the Automotive Industry due to the Advent of EVs

- 5.1.2 Increasing Complexity of Electronics

- 5.2 Market Restraints

- 5.2.1 Rising Metal Prices Impacting Component Production Costs

6 MARKET SEGMENTATION

- 6.1 Type

- 6.1.1 Polypropylene

- 6.1.2 Polyethylene

- 6.1.3 Other Types (PTFE, PPS, etc.)

- 6.2 Applications

- 6.2.1 Automotive

- 6.2.2 Telecommunications

- 6.2.3 Industrial

- 6.2.4 Aerospace & Defense

- 6.2.5 Consumer Electronics

- 6.2.6 Medical

- 6.2.7 Other Applications

- 6.3 Geography

- 6.3.1 Americas

- 6.3.2 Europe, Middle East & Africa

- 6.3.3 Asia-Pacific (Excl. Japan and Korea)

- 6.3.4 Japan and Korea

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 KEMET Corporation (Yageo company)

- 7.1.2 Panasonic Corporation

- 7.1.3 Vishay Intertechnology Inc.

- 7.1.4 TDK Corporation

- 7.1.5 AVX Corporation (Kyocera Corp)

- 7.1.6 Murata Manufacturing Co. Ltd.

- 7.1.7 Cornell Dubilier Electronics Inc.

- 7.1.8 Desai Electronics

- 7.1.9 Shanghai Yinyan Electronic

- 7.1.10 Rubycon Corporation

- 7.1.11 Nantong Jianghai Capacitor Co. Ltd.

- 7.1.12 Nichicon Corporation

- 7.1.13 Wima GmBH & Co. KG