|

市場調査レポート

商品コード

1431448

セラミックコンデンサの世界市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Ceramic Capacitors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| セラミックコンデンサの世界市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

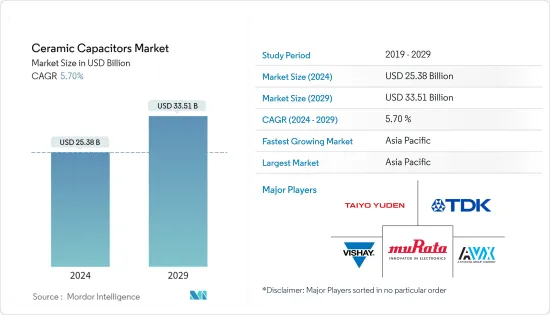

世界のセラミックコンデンサの市場規模は、2024年に253億8,000万米ドルと推定され、2029年には335億1,000万米ドルに達し、予測期間中(2024年~2029年)にCAGR5.70%で成長すると予測されています。

セラミックコンデンサは、信頼性が高く製造コストが安いため、ほとんどの電気機器で最も一般的に使用されています。これらのコンデンサは複数の産業で使用されており、主に無極性で存在するセラミックまたは磁器ディスクで構成されています。セラミック材料は、導電性が低く、静電界を効率的にサポートするため、優れた誘電体でもあります。

主なハイライト

- セラミックコンデンサには、主に3つのタイプがあります。スルーホール実装用のリード付きディスクセラミックコンデンサ、樹脂コーティングされた表面実装用積層セラミックコンデンサ(MLCC)、および主にPCB上のスロットに装着することを目的とした特殊タイプのマイクロ波用裸リードレスディスクセラミックコンデンサです。

- 中でもMLCCは多くの電子機器に不可欠な部品であり、ウェアラブル機器やスマートフォン(スマートフォンには約900~1,100個の積層セラミックコンデンサが搭載されている)などに広く使用されています。

- また、エレクトロニクスの嗜好が家電からコンピューティングへとシフトしています。AI、IoT、クラウド、デジタル化の出現により、メーカーはこの分野に集中しています。これらの新技術は消費財に比べて利益率が高く、必要な台数も少ないため、メーカーの生産ライン管理も成り立ちます。

- 5Gスマートフォンの普及と高機能化は、さらなる小型化と電子回路の高密度化への需要を刺激しています。例えば、クアルコムやメディアテックを含む多くの企業が5Gをサポートするチップセットをリリースしており、多くのスマートフォンメーカーがそれらを使用しています。以前は、5Gのサポートはフラッグシップモバイルのみに限られていましたが、現在ではミッドレベルのスマートフォンも5Gをサポートし、より安価なチップセットを市場に投入しています。こうした取り組みがセラミックコンデンサの必要性を高めています。

- その反面、セラミックコンデンサの生産にはいくつかの課題があります。大きな課題のひとつは、高容量の積層セラミックコンデンサ(MLCC)の製造であり、これには多数の単層コンデンサをひとつのパッケージに積層する必要があります。このようなコンデンサの製造には、機械的な影響を受けやすい、回路基板への表面実装はんだ付け時にクラックが入りやすい、層全体で高い静電容量の均一性を得るのが難しい、などの問題がつきまといます。もう一つの課題は、キャパシタンスの温度依存性と周波数依存性であり、これは高性能用途で問題を引き起こす可能性があります。

- COVID-19パンデミックはセラミックコンデンサ市場に影響を与えました。パンデミックはサプライチェーンと製造工程に混乱を引き起こし、セラミックコンデンサの需要と供給に変動をもたらしました。

- しかし、ワクチン接種の推進や規制の緩和が進み、状況が正常化するにつれて市場は回復すると予想されました。一方、セラミックコンデンサ部品は、世界の在宅勤務の増加により、ノートパソコンやパソコンなどの家電製品やモバイル機器の需要が増加しているため、他の産業からの需要が増加すると予想されます。また、パンデミックの間にオンラインゲームの傾向が強まり、ゲームやホームシアターエレクトロニクスの需要が増加したことも、大きな需要につながりました。

セラミックコンデンサ市場動向

自動車セグメントが市場の成長を牽引する見込み

- セラミックコンデンサは、そのコンパクトなサイズ、高い信頼性、高温や振動に耐える能力から、通常自動車用用途に採用されています。エンジン制御ユニット、インフォテインメント・システム、照明システムなど、さまざまな自動車システムの電源から高周波ノイズをフィルタリングします。また、スイッチング回路の電圧スパイクやリンギングを抑制するスナバ回路や、回路間の高周波信号を通過させるカップリング回路にも採用されています。さらに、センサーやアクチュエーターの共振回路、各種車載システムのクロックジェネレーターなど、タイミング回路や発振回路にも使用されています。

- 自律走行車技術、車車間通信、ADAS(先進運転支援システム)、バックアップカメラや車線逸脱検知器などの安全・検知システムによる新しい自動車機能や特徴が、自動車用電子部品の需要を押し上げています。セラミックコンデンサのような受動部品は、安定性と干渉のない設計を保証するために必要です。

- 世界経済フォーラムによると、完全自律走行車は2035年までに年間1,200万台以上販売され、世界の自動車市場の25%をカバーすると予想されています。さらに新法は、そのような車は"現在の乗用車と同じレベルの乗員保護を提供し続けなければならない"と強調しています。運輸長官が述べたように、ピート・バッティギーグの新ルールは、ADS搭載車の強固な安全基準を確立するために不可欠です。このような発展は、同地域におけるコネクテッドカー市場の普及を促進することで、研究市場の成長を支援します。これにより、国内外のエッジコンピューティング企業が市場シェアを拡大する機会が生まれる可能性があります。

- 自動運転車やADAS(先進運転支援システム)などの高度な自動車へのシフトは、自動車当たりのMLCCの使用を促進しています。そのため、こうした動向に対応するため、各メーカーはセラミックコンデンサの高容量化に関連した製品革新に取り組んでいます。例えば、村田製作所は2021年12月、MLCCとしては最高の静電容量22µF、定格電圧16VのGCM31CC71C226ME36 MLCCの開発を発表しました。このMLCCは、車載用途や安全用途に最適です。さらに、このコンデンサは薄層シート成形技術で設計されており、より高い信頼性と効率を実現しています。

- 同様に2022年2月、同社は3端子で4.3µFの静電容量を提供するよう設計されたNFM15HC435D0E3 MLCCを発売しました。このコンデンサは、ADAS(先進運転支援システム)や自律走行機能などに搭載される高性能プロセッサに求められるノイズ除去や優れたデカップリングなどの効果を発揮する車載用途向けに設計されています。このことは、自動車産業におけるセラミックコンデンサの需要が拡大していることを示しています。しかし、COVID-19の恒常的な流行の影響により、サプライチェーンは小規模ながら混乱すると予想されます。

- さらに、電気自動車におけるMLCCの需要も増加しています。運転支援機能や完全自律走行システムなどの機能の増加により、ほとんどのEVが10~1万5,000個近いMLCCを使用しているためです。IEAによると、EVの販売台数は2022年に増加し、102万台を占めました。このような事例は、自動車セクターにおけるMLCCの需要が拡大していることを示しています。さらに、EVの高い普及率と、様々な政府によって設定されたICEエンジンの完全な段階的廃止時期が、自動車セクターにおけるMLCCの成長を促進すると思われます。

アジア太平洋は高い市場成長が見込まれる

- アジア太平洋はセラミックコンデンサにとって最も重要な市場の一つです。中国では自動車産業が拡大しており、世界の自動車市場で重要な役割を果たしています。政府は、自動車部品部門を含む自動車産業を国の主要産業のひとつと見なしています。中国政府は、中国の自動車生産台数が2025年までに3,500万台に達すると予想しています。これがコンデンサ需要を牽引すると予想されます。

- EVの人気は高まっており、中国は電気自動車を採用する主要国のひとつとみなされています。同国の第13次5ヵ年計画は、同国の交通セクターの進歩のため、ハイブリッド車や電気自動車などのグリーン交通ソリューションの開発を推進しています。中国の電気自動車は、数十社の競合他社による新モデルが新規購入者を引きつけ、所有者に電気自動車への乗り換えを促したため、中国政府の2025年予測を大幅に上回る2022年に全国普及率20%という目標を達成する勢いでした。

- さらに日本政府は、2050年までに日本で販売されるすべての新車を、電気自動車であれハイブリッド車であれ普及させることを目指しています。また、民間企業による電気自動車用のバッテリーやモーターの開発を加速させるため、補助金を提供する計画もあります。日本は、10年以上前に日産リーフや三菱i-MIEVが発売され、電気自動車をいち早く導入した国のひとつです。

- セラミックコンデンサは、その高い静電容量、高い耐電圧、低コストにより、通信業界で一般的に使用されています。フィルタリング、デカップリング、電圧調整など、さまざまな用途に採用されています。特に、積層セラミックコンデンサ(MLCC)は、そのコンパクトなサイズと高い静電容量値により、通信業界で人気があります。MLCCは、スマートフォン、基地局、その他の通信機器など、さまざまな用途で使用されています。

- 京セラやKEMETといったアジア太平洋のメーカーは、通信用途向けに設計されたセラミックコンデンサを生産しています。同地域における電気通信需要の増加は、同地域のセラミックコンデンサ需要を押し上げると予想されています。例えば、チャイナテレコムによると、2022年の売上高は約4,750億人民元で、前年の4,400億人民元から大幅に増加しました。

- 中国はアジア太平洋におけるAGVの成長に大きく貢献しています。製造業、自動車、Eコマースなど、あらゆる産業でAGV製品に対する需要が高まっていることが、市場の成長を積極的に後押ししています。AGVは、ダンプやリフティングのための高出力のバーストと、ステーション間の移動のための継続的なエネルギーを必要とします。これらのバーストパワーはバッテリー寿命を著しく低下させるため、メーカーはバッテリーを頻繁に交換する必要があります。また、作業シフト中にバッテリーを交換する必要もあります。バッテリーとは異なり、キャパシタはメンテナンスがほとんど必要なく、床面誘導充電を使用して数秒で充電できるため、メーカーはバッテリーの交換や交換から解放されます。アジア太平洋では工場の自動化が進んでおり、予測期間中、セラミックコンデンサ需要を牽引すると予想されます。

- さらに、同地域の企業は幅広い顧客ニーズに対応するため、さまざまな製品を提供しています。例えば、村田製作所は自動車パワートレイン向けに積層セラミックコンデンサ(MLCC)、高実効容量チップMLCC、高リップル電流チップMLCC、家電・産業機器向けに安全チップMLCCなど、さまざまなセラミックコンデンサを提供しています。村田製作所のセラミックコンデンサは、小型で大きな静電容量値で知られています。また、MLCCとしては世界初となる静電容量1μF/25VのGCM033D70E105ME36を開発し、量産を開始しています。

セラミックコンデンサ業界の概要

セラミックコンデンサ市場は、世界市場のベンダーが限られているため、半ば固まっています。主要企業は、市場シェアを向上させ、市場での収益性を高めるために、買収やパートナーシップなどの様々な戦略に関与しています。村田製作所、TDK Corporation、太陽誘電、AVX Corporation、Vishay Intertechnology, Inc.などの大手企業が参入しています。

- 2023年11月京セラAVXは、クラスX1/Y2規格に準拠したコンデンサKGKシリーズとクラスX2規格に準拠したコンデンサKGHシリーズを発表しました。これらのコンデンサの定格電圧は250VACで、EN 60384-14、IEC 60384-14、UL 60384-14規格の要件を満たすように設計されています。サージ保護、過渡保護、EMIフィルタリング機能を備えており、モデムやFAXなど様々な家電や産業機器での使用に適しています。

- 2023年9月TDK株式会社(社長:上釜健宏)は、積層セラミックコンデンサ(MLCC)CNシリーズに、革新的で特徴的なデザインを採用した強化バージョンを発表しました。従来のソフトターミネーション型MLCCは端子電極全体を樹脂層で被覆していたが、本製品は基板に実装する片面のみに樹脂層を形成しました。さらに、TDK株式会社は、より大容量のMLCCに対する需要の高まりに対応するため、CNAシリーズ(車載グレード)およびCNCシリーズ(商用グレード)を発表し、製品ラインアップを拡充しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- バリューチェーン分析

- COVID-19以後の分析を含むマクロ経済評価

第5章 市場力学

- 市場促進要因

- デジタル化と5G技術の普及拡大

- ファクトリーオートメーションとロボティクスの採用

- 市場抑制要因

- セラミックコンデンサ開発に必要な高度なマイクロレベルの技術力

第6章 市場セグメンテーション

- タイプ別

- MLCC

- セラミックディスクコンデンサ

- 貫通型セラミックコンデンサ

- セラミックパワーコンデンサ

- エンドユーザー別

- 家電

- 自動車

- 通信

- 産業用

- エネルギー・電力

- その他エンドユーザー

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Murata Manufacturing Co., Ltd.

- TDK Corporation

- Taiyo Yuden Co., Ltd.

- Vishay Intertechnology, Inc.

- AVX Corporation

- Johanson Dielectrics, Inc.

- AFM Microelectronics

- Kemet Corporation

- Walsin Technology Corporation

- TE Connectivity

第8章 投資分析

第9章 市場の将来展望

The Ceramic Capacitors Market size is estimated at USD 25.38 billion in 2024, and is expected to reach USD 33.51 billion by 2029, growing at a CAGR of 5.70% during the forecast period (2024-2029).

Ceramic capacitors are one of the most commonly used in most electrical instruments, as they offer reliability and are cheaper to manufacture. These capacitors are used in multiple industries and primarily consist of ceramic or porcelain discs that exist in a non-polarized form. The ceramic material is also an excellent dielectric due to its poor conductivity and its efficient support of electrostatic fields.

Key Highlights

- Ceramic capacitors are mostly available in three types. However, other styles are also available: leaded disc ceramic capacitors for through-hole mounting, resin-coated surface mount multilayer ceramic capacitors (MLCC), and special type microwave bare lead-less disc ceramic capacitors, which are primarily intended to sit in a slot on the PCBs.

- Among the applications, MLCCs are essential components of many electronic devices and are widely used in such devices as wearable devices and smartphones (approximately 900 to 1100 multilayer ceramic capacitors are installed in a smartphone).

- Also, there has been a shift in preference in electronics from consumer electronics to computing. The emergence of AI, IoT, cloud, and digitalization has led manufacturers to concentrate on this segment. These new technologies have a high profit margin compared to consumer goods, and the units needed are also fewer, making it viable for manufacturers to manage their production lines.

- The widespread adoption of 5G smartphones and their increasing functionality are stoking demand for further miniaturization and higher electronic circuitry density. For instance, a number of companies, including Qualcomm and MediaTek, are releasing chipsets that support 5G, and numerous smartphone manufacturers are using them. Previously, 5G support was confined to only flagship mobiles; now, mid-level smartphones also support 5G to introduce cheaper chipsets in the market. Such initiatives are increasing the need for ceramic capacitors.

- On the flip side, the production of ceramic capacitors presents several challenges. One major challenge is manufacturing high-capacitance multilayer ceramic capacitors (MLCCs), which involves stacking many single-layer capacitors into a single package. The manufacture of these capacitors is fraught with problems, including mechanical susceptibility, cracking during surface-mount soldering to a circuit board, and difficulty achieving high uniformity of capacitance across the layers. Another challenge is capacitance's temperature and frequency dependence, which can cause issues in high-performance applications.

- The COVID-19 pandemic impacted the ceramic capacitor market. The pandemic caused disruptions in the supply chain and manufacturing processes, leading to fluctuations in the demand and supply of ceramic capacitors.

- However, the market was anticipated to recover as the situation normalized with the ongoing vaccination drives and relaxed regulations. Meanwhile, ceramic capacitor components were expected to witness a growing demand from other industries due to an increasing demand for consumer electronics and mobile devices, such as laptops and computers, due to the work-from-home scenario across the world. Also, significant demand was witnessed from the increasing trend of online gaming during the pandemic, which subsequently increased the demand for gaming and home theater electronics.

Ceramic Capacitors Market Trends

Automotive Segment is Expected to Drive the Market's Growth

- Ceramic capacitors are usually employed in automotive applications due to their compact size, high reliability, and ability to withstand high temperatures and vibrations. They filter out high-frequency noise from power supplies in various automotive systems, such as engine control units, infotainment systems, and lighting systems. They are also employed in snubber circuits to suppress voltage spikes and ringing in switching circuits and in coupling circuits to pass high-frequency signals between circuits. Further, they are used in timing and oscillation circuits, such as in resonant circuits for sensors and actuators, as well as in clock generators for various automotive systems.

- The new automotive features and functionality due to autonomous vehicle technologies, vehicle-to-vehicle communications, advanced driver-assistance systems, and other safety and sensing systems, like backup cameras and lane-departure detectors, are driving the demand for electronic components in automotive applications. Passive components, like ceramic capacitors, are required to ensure stability and interference-free designs.

- According to the World Economic Forum, over 12 million fully autonomous cars are expected to be sold annually by 2035, covering 25% of the global automotive market. Further, the new law emphasizes that such cars "must continue to offer the same high levels of occupant protection as current passenger vehicles." As the Transportation Secretary said, Pete Buttigieg's new rule is essential to establishing robust safety standards for ADS-equipped vehicles. Such developments aid the growth of the studied market by propelling the proliferation of the connected car market in the region. This may create opportunities for local and international edge computing players to expand their market share.

- The shift towards sophisticated vehicles, such as self-driving vehicles, ADAS (Advanced Driver Assistance Systems), is driving the use of MLCCs per vehicle. Therefore, to cater to such a trend, manufacturers are involved in product innovation related to higher capacitance for ceramic capacitors. For instance, in December 2021, Murata announced the development of a GCM31CC71C226ME36 MLCC that features the highest capacitance of 22 µF for MLCCs and has a voltage rating of 16V. The application of this MLCC is streamlined for automotive and safety applications. In addition, the capacitors are designed with thin-layer sheet forming technology to achieve greater reliability and efficiency.

- Similarly, in February 2022, the company launched the NFM15HC435D0E3 MLCC, designed with three terminals to provide a capacitance of 4.3 µF. The capacitors are designed for automotive applications to attain results on noise removal and superior decoupling that are required for high-performance processors employed in advanced driver assistance systems and autonomous driving functions. This indicates the growing demand for ceramic capacitors in the automotive industry. However, with the impact of the constant COVID-19 pandemic, the supply chain is expected to be disrupted on a small scale.

- Moreover, the demand for MLCC in electric vehicles is also increasing, as most of the EVs use close to 10-15,000 MLCC due to increased features like driver assistance functions and fully autonomous systems. The sales of EVs increased in 2022, according to the IEA, and accounted for 1.02 million electric vehicles. Such instances indicate the growing demand for MLCC in the automotive sector. Further, the high adoption of EVs and the complete phase-out dates of ICE engines set by various governments will drive the growth of MLCC in the automotive sector.

Asia-Pacific Region is Expected to Witness a High Market Growth

- The Asia-Pacific region is one of the most important markets for ceramic capacitors. The automotive industry is expanding in China, and the country plays an important role in the worldwide automotive market. The government sees its automotive industry, including the auto parts sector, as one of the country's primary industries. The government of China anticipates that China's automobile output is expected to reach 35 million units by 2025. This is expected to drive the capacitors' demand.

- The popularity of EVs is growing, and China is regarded as one of the dominant adopters of electric vehicles. The country's 13th Five-Year Plan promotes the development of green transportation solutions, such as hybrid and electric vehicles, for advancements in the country's transportation sector. China's electric cars were on track to reach the 20% nationwide penetration goal in 2022, well ahead of the Chinese government's 2025 forecast, due to new models by dozens of competitors attracting new buyers and encouraging owners to switch to electric vehicles.

- Further, the Japanese government aims to have all the new cars sold in Japan, whether electric or hybrid, by the year 2050. The country plans to also offer subsidies to accelerate the private sector's development of batteries and motors for electricity-powered vehicles. Japan is one of the countries that were early adopters of electric vehicles, with the launch of the Nissan LEAF and Mitsubishi i-MIEV more than a decade ago.

- Ceramic capacitors are commonly used in the telecommunications industry due to their high capacitance, high voltage tolerance, and low cost. They are employed in various applications, such as filtering, decoupling, and voltage regulation. In particular, multilayer ceramic capacitors (MLCCs) are popular in the telecommunications industry due to their compact size and high capacitance values. MLCCs are used in various applications, including smartphones, base stations, and other telecommunications equipment.

- Manufacturers in the Asia-Pacific region, such as Kyocera and KEMET, produce ceramic capacitors designed for telecommunications applications. The increasing telecom demand in the region is anticipated to boost the demand for ceramic capacitors in the region. For instance, according to China Telecom, in 2022, it generated revenue of approximately CNY 475 billion, a significant increase from CNY 440 billion in the previous year.

- China has been a significant contributor to the growth of the AGVs in the Asia-Pacific region. The growing demand for AGV products across industries, such as manufacturing, automotive, and e-commerce, among others, is boosting the market's growth positively. An AGV requires high power bursts for dumping or lifting, as well as continuous energy for traveling between stations. These bursts of power significantly reduce battery life, requiring manufacturers to replace batteries frequently. There is also the need to exchange batteries during working shifts. Unlike batteries, capacitors require little maintenance and can be charged in seconds using in-floor inductive charging, freeing manufacturers from constant battery swaps and replacements. The increasing factory automation in the Asia-Pacific region is anticipated to drive the demand for ceramic capacitors during the forecast period.

- Additionally, the players in the region are offering various products to cater to a wide range of customers' needs. For example, Murata Manufacturing Co., Ltd. offers various ceramic capacitors, including multilayer ceramic capacitors (MLCCs), high effective capacitance, and high ripple current chip MLCCs for automotive powertrains, and safety chip MLCCs for consumer electronics and industrial equipment. Murata's ceramic capacitors are renowned for their small size and large capacitance values. They have also developed and started mass production of the GCM033D70E105ME36, the world's first MLCC capacitance of 1 µF/25 V.

Ceramic Capacitors Industry Overview

The ceramic capacitor market is Semi-consolidated due to limited vendors in the global market. The key players are involved in various strategies, such as acquisitions and partnerships, to improve their market share and enhance their profitability in the market. Some of the leading players are there in the market are Murata Manufacturing Co., Ltd., TDK Corporation, Taiyo Yuden Co., Ltd., AVX Corporation, Vishay Intertechnology, Inc., and many others.

- November 2023: Kyocera AVX has introduced the KGK series of capacitors that comply with Class X1/Y2 standards and the KGH series of capacitors that comply with Class X2 standards. These capacitors, with a voltage rating of 250 VAC, are designed to meet the requirements set by EN 60384-14, IEC 60384-14, and UL 60384-14 standards. They offer surge and transient protection and EMI filtering, making them suitable for use in various consumer and industrial devices such as modems and fax machines.

- September 2023: TDK Corporation has introduced an enhanced version of its CN series of multilayer ceramic capacitors (MLCCs) that boasts an innovative and distinctive design. In contrast to conventional soft termination MLCCs, where the entire terminal electrodes are coated with resin layers, this new design incorporates resin layers only on one side that is mounted on a board. Moreover, TDK Corporation has also expanded its product range by introducing the CNA series (automotive grade) and CNC series (commercial grade) to cater to the growing demand for MLCCs with larger capacitances.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Value Chain Analysis

- 4.4 Macro-economic Assessment Including Post-COVID-19 Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Penetration of Digitalization and 5G technology

- 5.1.2 Adoption of Factory Automation and Robotics

- 5.2 Market Restraints

- 5.2.1 Requirement of Advanced Micro level Technical Competence for Developing Ceramic Capacitors

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 MLCC

- 6.1.2 Ceramic Disc Capacitor

- 6.1.3 Feedthrough Ceramic Capacitor

- 6.1.4 Ceramic Power Capacitor

- 6.2 By End-User

- 6.2.1 Consumer Electronics

- 6.2.2 Automotive

- 6.2.3 Telecommunication

- 6.2.4 Industrial

- 6.2.5 Energy & Power

- 6.2.6 Other End-Users

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Murata Manufacturing Co., Ltd.

- 7.1.2 TDK Corporation

- 7.1.3 Taiyo Yuden Co., Ltd.

- 7.1.4 Vishay Intertechnology, Inc.

- 7.1.5 AVX Corporation

- 7.1.6 Johanson Dielectrics, Inc.

- 7.1.7 AFM Microelectronics

- 7.1.8 Kemet Corporation

- 7.1.9 Walsin Technology Corporation

- 7.1.10 TE Connectivity