|

|

市場調査レポート

商品コード

1644865

マスターデータ管理:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Master Data Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| マスターデータ管理:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

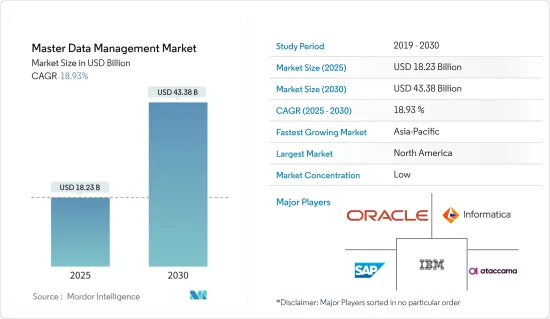

マスターデータ管理の市場規模は2025年に182億3,000万米ドルと推計され、予測期間(2025~2030年)のCAGRは18.93%で、2030年には433億8,000万米ドルに達すると予測されます。

データコンプライアンスの需要や、業務改善のために著名企業でマスターデータ管理ソリューションの利用が拡大していることが、収益成長の原動力となりそうです。

主なハイライト

- 意思決定や消費者への働きかけに信頼できる情報を提供するためには、マスターデータ管理とデータガバナンスのためのツールが不可欠です。これは、企業やパートナー組織のより広範なシステム、ITスペシャリスト、ユーザーがデータを作成し、データにアクセスするためです。

- 近年、組織は、組織の最も重要な事業活動の成否を左右するデータに対する意識を高めています。モノのインターネット(IoT)、相互接続されたコネクテッド・デバイス、クラウド・コンピューティング、モビリティ、デジタル化によって、データの流量と量が増加し、安価なストレージが利用できるようになったことも相まって、組織は実質的にあらゆるものを保存するようになりました。残念なことに、この戦略は、機密、重要、ミッションクリティカルなデータポイントのパラメータを変化させ、一般的にダークデータ沼を作り出す原因となっています。

- 分離されたデータ環境から統合されたマスターデータセットへの切り替えは、現在多くの企業で調査され、試みられています。マスターデータ管理(MDM)プロジェクトとしても知られるこのようなマスターデータ構想の目的は、重要な企業データのゴールデンコピーを生成して利用し、可能な限りソース付近でデータエラーを発見、検証、対処することです。MDMプログラムが成功すれば、データの一貫性、完全性、正確性が実現します。しかし、MDMプログラムを導入して成功を保証できるのは、ビジネスがサポートするデータ管理イニシアチブが同時に実施されている場合に限られます。

- 最近の機械学習(ML)、ビッグデータ、人工知能(AI)の革新により、市場は拡大しています。この技術は、膨大なデータセットへのアクセスを提供するだけでなく、データ処理とストレージに新たな技術的可能性をもたらしています。複数の領域や視点からデータを扱う新技術の能力が高まるにつれて、顧客はさまざまな期待を抱くようになった。最も多い要望は、マスターデータ管理システムをビッグデータ、アナリティクス、ビジネスインテリジェンス技術と組み合わせることです。

- しかし、実装、データ・セキュリティ、プライバシーの問題が市場の収益を制約しています。厳格な法律や広範なビジネス要件により、MDMの導入は課題となっています。さらに、企業はテクノロジーの統合を進めているため、セキュリティ上の欠陥や攻撃を受けやすくなっています。ユーザーは、重要な個人データを失うことを懸念し、MDMソリューションに抵抗しています。こうした問題がMDMソリューションの採用を阻害し、市場の収益成長を制限しています。

マスターデータ管理市場の動向

クラウドMDMセグメントが大きなシェアを占める

- マスターデータ管理(MDM)が企業の成功に不可欠になるにつれ、マスターデータの取得、保存、活用のための新しいテクノロジーやアプローチの分析が不可欠になっています。次世代のMDMシステムは、AI/ML、クラウド、連携アーキテクチャ、企業間共有、世界展開、データプラットフォームソリューション、その他の最新のMDM機能によって推進されます。

- ベンダーや顧客は世界中に分散しており、バーチャルなコミュニケーションを行っているため、企業部門はスピードと柔軟性を求めてクラウド上のMDMテクノロジーを利用してきました。企業はMDMクラウド・サービスをカスタマイズし、オンショアではクラウド・ソースとのマスター・データ統合とデータ品質に一層注力することになります。

- より多くのアプリケーションとデータがクラウドに移行するにつれて、データ専門家は、複数のクラウド、1つのクラウド内、オンプレミスのソースにまたがる、より複雑な量のデータを管理できるようになります。このような様々なトポロジーを実現するためには、マルチクラウドとクラウド間のデータ管理が不可欠です。

- クラウドベースのサービスは、MDM(その他の重要な企業アプリケーションも同様)に広く利用されるようになってきています。クラウドMDMのようなクラウドネイティブ・ソリューションは、データの重心がファイアウォールを越えて移動し続ける中、クラウドソースデータやアプリケーションとの統合に関して、おそらくオンプレミス・ソリューションよりも優位性を提供すると思われます。

北米が主要市場シェアを占める

- マスターデータ管理業界は、北米で最大の市場シェアを持つと推定されます。この地域におけるテクノロジーの利用拡大が、北米のMDM市場の成長を促進する主な理由の1つです。IBM、オラクル、インフォマティカ・インクなど、各地域のMDMプレーヤーの拡大は、市場のさらなる拡大を促進すると予測されます。

- 一方、重要な地域経済諸国による研究開発費の伸びは、北米のマスターデータ管理市場における新技術の開拓を後押ししています。

- 例えば、2022年6月、統合データ管理とガバナンス・ソリューションのプロバイダーであるAtaccamaは、成長資本投資ラウンドで1億5,000万米ドルを確保しました。

- 米国ではデータ保護とセキュリティに関する規則が厳しいため、銀行やヘルスケアなど特定の業界で働く組織はMDMの導入を求められています。また、業務効率を高め、データの冗長性を減らしたいという要望が高まっていることも、市場を牽引しています。

マスターデータ管理業界の概要

マスターデータ管理市場は非常に細分化されており、重要なプレーヤーが複数存在します。現在市場の大部分を占めているのは、IBM、オラクル、Informatica Inc.、SAP SE、Ataccamaなど、一部の主要企業のみです。同市場のプレーヤーは、市場シェアと収益性を高めるため、国際的に消費者基盤を拡大しています。

- 2022年10月- 統合データ管理プラットフォームのトッププロバイダーであるAtaccama社は、Ataccama ONEプラットフォームの次期大幅アップデートの早期配布を発表しました。このバージョンでAtaccamaは、世界中の企業にエンドツーエンドのデータ管理を提供し、データの民主化を可能にするという同社の目標をサポートする新機能を導入します。このプラットフォーム・アップグレードにより、Ataccamaは、現代のデータ・ガバナンス・プログラムは、単一目的のテクノロジーでは不可能な方法でデータ・ガバナンス機能を収束させる必要があるという、業界の高まる合意の最前線に位置することになります。

- 2022年2月-IBMは、Microsoft Azureプラットフォームとマルチクラウドの専門知識に特化した米国のクラウドサービスコンサルタントであるNeudesicを買収したと発表しました。この買収により、IBMが提供するハイブリッド・マルチクラウド・サービスのポートフォリオは大幅に増加し、同社のハイブリッド・クラウドとAI戦略をさらに推進することになります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3カ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- 検証とコンプライアンスに対する需要の高まり

- データ管理におけるデータ品質ツールの利用拡大

- 市場抑制要因

- 高価な統合と保守作業

- データセキュリティとプライバシーに関する懸念

- 各地域で課される厳しいデータ規制

第6章 市場セグメンテーション

- コンポーネント別

- ソフトウェア

- サービス

- 展開モデル別

- オンプレミス

- クラウド

- 企業規模別

- 大企業

- 中小企業

- 用途別

- サプライヤー

- 製品別

- 顧客

- その他の用途

- 業界別

- IT・通信

- BFSI

- ヘルスケア

- 政府機関

- 小売

- 製造業

- 教育

- その他業界別

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- IBM

- Oracle

- Informatica Inc.

- SAP SE

- Ataccama

- SAS Institute Inc.

- TIBCO Software Inc.

- Teradata Corporation

- Syndigo LLC

- Profisee

第8章 投資分析

第9章 市場の将来

The Master Data Management Market size is estimated at USD 18.23 billion in 2025, and is expected to reach USD 43.38 billion by 2030, at a CAGR of 18.93% during the forecast period (2025-2030).

The demand for data compliance and the growing usage of master data management solutions in prominent companies to improve business operations would likely fuel revenue growth.

Key Highlights

- To deliver information that can be relied upon for decision-making and consumer outreach, tools for master data management and data governance are essential. This is because a broader range of systems, IT specialists, and users from businesses and partner organizations create and access data.

- In recent years, organizations have become more aware of their data, which is crucial to the success or failure of an organization's most important business activities. The Internet of Things (IoT), interconnected, connected devices, cloud computing, mobility, and digitalization have all boosted data flow and volume, combined with the availability of less expensive storage, pushing organizations to preserve practically everything. Unfortunately, this strategy has caused sensitive, critical, and mission-critical data points to have varying parameters, commonly creating dark data swamps.

- The switch from segregated data environments to a consolidated master data set is now being investigated and tried by many businesses. The purpose of such master data initiatives, also known as master data management (MDM) projects, is to generate a golden copy of crucial company data for consumption and to discover, validate, and address data errors near the source as feasible. A successful MDM program enables data consistency, completeness, and correctness. However, installing an MDM program can only guarantee success if business-supported data management initiatives are implemented concurrently.

- The market is growing due to recent innovations in machine learning (ML), big data, and artificial intelligence (AI). In addition to offering access to enormous datasets, this technology offers new technological possibilities for data processing and storage. As new technologies' capacity for handling data from several domains and perspectives has increased, customers have a wide range of expectations. The most frequent request has been to combine master data management systems with big data, analytics, and business intelligence technologies.

- However, implementation, data security, and privacy issues constrain market revenue. Due to strict laws and extensive business requirements, MDM implementation might be challenging. Furthermore, firms are progressively integrating technologies, which makes them prone to security flaws and assaults. Users resist MDM solutions because they are concerned about losing critical personal data. These issues are inhibiting MDM solution adoption and limiting the market's revenue growth.

Master Data Management Market Trends

Cloud MDM Segment to Hold a Significant Share

- Analyzing new technologies and approaches for acquiring, storing, and utilizing master data is becoming vital as master data management (MDM) becomes essential for fostering company success. The next generation of MDM systems is driven by AI/ML, cloud, federated architectures, inter-enterprise sharing, global deployment, data platform solutions, and other contemporary MDM features.

- Enterprise sectors have used MDM technologies on the cloud for speed and flexibility since vendors and customers are dispersed worldwide and communicate virtually. Businesses will customize their MDM cloud services, while those onshore will result in a stronger focus on master data integration and data quality to and from cloud sources.

- As more apps and data migrate to the cloud, data professionals can manage more complicated amounts of data across several clouds, inside one cloud, and on-premises sources. To enable these various topologies, multi-cloud and inter-cloud data management is essential.

- Cloud-based services are becoming more widely used for MDM (as well as other essential corporate applications). A cloud-native solution, such as cloud MDM, will probably offer advantages over on-premise solutions concerning integration with cloud-sourced data and apps as the center of gravity for data continues to move beyond the firewall.

North America to Hold Major Market Share

- The master data management industry is estimated to have the largest market share in North America. The expanding use of technology in the area is one of the main reasons promoting the growth of the MDM market in North America. The expansion of MDM players across regions, such as IBM, Oracle, and Informatica Inc., is anticipated to drive market expansion further.

- On the other hand, the growth of R&D spending by significant regional economies is helping the development of new technologies in the North American master data management market.

- For instance, in June 2022, Ataccama, a unified data management and governance solutions provider, secured USD 150 million in a growth capital investment round, money that will be used to finance the company's efforts to develop new products and expand its market presence.

- Organizations working in specific industries, including banking and healthcare, are required to adopt MDM because of the strict data protection and security rules in the United States. The increasing desire to enhance operational effectiveness and lessen data redundancy also drives the market.

Master Data Management Industry Overview

The master data management market is highly fragmented and has several significant players. Only some key companies currently hold a large portion of the market, such as IBM, Oracle, Informatica Inc., SAP SE, and Ataccama. The players in the market are growing their consumer bases internationally to raise their market share and profitability.

- October 2022 - Ataccama, a top provider of unified data management platforms, announced the early distribution of the upcoming significant update to its Ataccama ONE platform. With this version, Ataccama will introduce new features that support its objective of giving businesses worldwide end-to-end data management and allowing data democratization. The platform upgrade places Ataccama at the forefront of a growing industry agreement that contemporary data governance programs must converge data governance capabilities in ways that single-purpose technologies cannot.

- February 2022 - IBM announced that it had acquired Neudesic, a US cloud services consultant focused on the Microsoft Azure platform and multi-cloud expertise. The portfolio of hybrid multi-cloud services offered by IBM will be significantly increased due to this purchase, further advancing the company's hybrid cloud and AI strategy.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Verification and Compliance

- 5.1.2 Growing Usage of Data Quality Tools for Data Management

- 5.2 Market Restraints

- 5.2.1 Expensive Integration and Maintenance activities

- 5.2.2 Concerns on Data Security and Privacy

- 5.2.3 Stringent Data Regulations Imposed in Various Regions

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Software

- 6.1.2 Service

- 6.2 By Deployment Model

- 6.2.1 On-premise

- 6.2.2 Cloud

- 6.3 By Enterprise Size

- 6.3.1 Large Enterprises

- 6.3.2 Small and Medium Enterprises

- 6.4 By Application

- 6.4.1 Supplier

- 6.4.2 Product

- 6.4.3 Customer

- 6.4.4 Other Applications

- 6.5 By Industry Vertical

- 6.5.1 IT and Telecommunication

- 6.5.2 BFSI

- 6.5.3 Healthcare

- 6.5.4 Government

- 6.5.5 Retail

- 6.5.6 Manufacturing

- 6.5.7 Education

- 6.5.8 Other Industry Verticals

- 6.6 By Geography

- 6.6.1 North America

- 6.6.2 Europe

- 6.6.3 Asia

- 6.6.4 Australia and New Zealand

- 6.6.5 Latin America

- 6.6.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM

- 7.1.2 Oracle

- 7.1.3 Informatica Inc.

- 7.1.4 SAP SE

- 7.1.5 Ataccama

- 7.1.6 SAS Institute Inc.

- 7.1.7 TIBCO Software Inc.

- 7.1.8 Teradata Corporation

- 7.1.9 Syndigo LLC

- 7.1.10 Profisee