|

市場調査レポート

商品コード

1683513

家庭用コーヒーマシン:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Household Coffee Machine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 家庭用コーヒーマシン:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

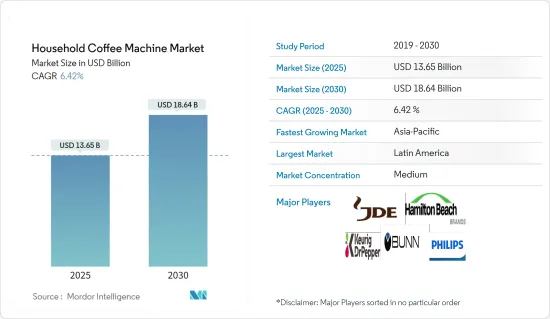

家庭用コーヒーマシン市場規模は2025年に136億5,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは6.42%で、2030年には186億4,000万米ドルに達すると予測されます。

コーヒー市場には、アジア太平洋、北米、ラテンアメリカ、欧州、中東・アフリカが含まれます。ブラジル(ラテンアメリカ)は世界最大のコーヒー生産国です。Yahoo Financeによると、2021年のコーヒー市場最大手は、Keurig Dr. Pepper Inc所有のTully's Coffee、The Coffee Bean & Tea Leaf、SSP Group所有のCaffe Ritazza、Coffee Beanery、Caffe Nero、McDonald's Corporation所有のMcCafeです。

COVID-19は世界の家庭用コーヒーマシン市場に大きな影響を与え、コーヒーとコーヒーマシンの両市場でサプライチェーンに混乱が生じた。労働環境はオフィスから家庭へと変化しました。その結果、家庭用コーヒーマシン市場に活路が生まれました。厳しい締め付けが強まり、必要な環境にしかお金を使わない環境が生まれ、コーヒー業界の投資環境が変化しました。原料価格はCOVID-19や現在進行中のロシア・ウクライナ戦争の影響で上昇の一途をたどり、豊作でもガス代が高く、コーヒーマシンの価格だけでなく、私たちが飲むコーヒーの価格も上昇しています。

コヴィードが減少し続け、コヴィードで職を失った人々が復職し、収入が増加しているため、家庭や企業のコーヒーマシン市場にとって良い環境となっています。供給の変化と原料価格の上昇の混乱は安定しており、消費者と生産者にとってポジティブな環境を作り出しています。家庭内消費に比べ、家庭外消費は大きなシェアを占めると予想されるため、企業、カフェ、店舗が求める自動コーヒーマシン市場に焦点を移す必要があります。

家庭用コーヒーマシン市場動向

コーヒー生産国におけるコーヒー消費量の減少がコーヒーマシン市場を牽引し、新たなビジネスチャンスを見出します。

レディ・トゥ・ドリンク(RTD)コーヒーは市場で増加傾向を示しており、ソーダに代わる健康的な最適飲料として認識されています。アイスコーヒーやコールドコーヒーはプレミアム飲料になりつつあり、新しい機能を備えたコーヒーマシン市場の機会を高めています。淹れ方も、従来のドリップ式コーヒーマシンから、一度に一定量を抽出するシングルカップ式に変わりつつあります。

コーヒー生産国におけるコーヒーの消費はあまり注目されていないが、その潜在的な影響は、その地域が植民地化され、コーヒーが輸出目的でのみ移植されたためかもしれないです。生産国における国内消費の可能性は、生産国が生み出す市場価値の増加や、コーヒーマシーン市場の拡大につながっていく可能性があります。

インドでは、アラビカ種とロブスタ種が主に生産されています。両品種とも増加傾向にあり、現在の生産量は(2022年)時点で103100MTと350400MTです。インドのコーヒー市場価格は継続的に変動しており、家庭用コーヒーの消費に負担を与えています。そのため、コーヒーマシン各社は家庭用コーヒーマシンの価格を引き下げて売り上げを伸ばし、パンデミックによる混乱後の市場をリードする必要があります。

COVID-19が世界のコーヒーマシン市場に与えた影響により、コーヒーマシンメーカーの事業戦略が変更されました。

COVID-19パンデミックは、コーヒーポッドマシン市場の成長にマイナスの影響を与えました。これは、超常利潤を維持するために、企業間で大規模な合併や買収が発生するときです。市場は142万台以上で、このcovidの影響の後に成長すると予想されます。ベンダー間の戦略的パートナーシップは、Bunn-O-Matic Corp、Hamilton Beach Brand Holding Co、Jacob Douwe Egberts BV、Keurig Dr. Pepper Inc、Koninklijke Philips NV、Luigi Lavazza、Masimo Zanetti Beverage Group Spa、Melitta Group、Nestleなどの主要市場参入企業との絶大な成長機会を提供します。

開発途上国でも先進国でも、コーヒーの人気はますます高まっています。もはや伝統的な飲み物ではなく、若々しくトレンディな飲み物となっています。インドでは、コーヒーの消費量が最も多いのは東部で、北部と西部はその後に続きます。

コーヒー市場を牽引しているのは、コーヒーを摂取する消費者層であり、コーヒー消費の主要国は世界の西側地域です。コーヒーマシンを自動化し、新たな先進機能を追加することが、コーヒーマシン・メーカー全体の競争の場です。オフィスがオープンし、人々が仕事に戻ることで、家庭やオフィスでのコーヒーマシンの需要が増加します。

家庭用コーヒーマシン産業概要

米国は自動コーヒーマシン市場の主要国です。全生産量のうち50%近くが北米産で、約70%が米国産です。ガジェットの電気使用量に革命的な時代が訪れ、星評価が適用される中、ドイツのコーヒーマシン市場は(GHG)削減に焦点を当てたエネルギー効率の高い製品を提供しています。コーヒー消費量の増加に伴い、中国とインドは有利な自動コーヒーマシンの販売機会を提供しています。コーヒーマシン内の自動化は時代とともに増加し、市場で先進的な製品の発売競争を引き起こしています。

2022年中の世界最大のコーヒー会社は、スターバック、ダンキン、ティム・ホートン、ダッチ・ブラザーズ・コーヒーです。世界最大のコーヒー会社であるスターバックは、2021年には33,000店舗近く、つまり最も近い競合であるダンキンの3倍の店舗数を持っています。いくつかの調査によると、コヴィッド以降もコーヒーの消費量は変わらないが、自宅で淹れることが増え、カフェで淹れることが減っているため、コーヒーマシンがより多くの家庭に浸透しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 市場概要

- 市場促進要因

- 市場抑制要因

- コーヒーマシン市場における技術革新の影響に関する洞察

- 製品技術に関する洞察

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19の市場への影響

第5章 市場セグメンテーション

- 流通チャネル別

- マルチブランドストア

- 専門店

- オンラインストア

- その他の流通チャネル

- 製品タイプ別

- フィルター式コーヒーマシン

- カプセル/ポッド式コーヒーマシン

- 従来のエスプレッソコーヒーマシン

- Bean to Cupコーヒーマシン

- 操作カテゴリー

- 半自動

- 自動

- 地域別

- 北米

- 欧州

- アジア太平洋

- 南米

- 中東・アフリカ

第6章 競合情勢

- 市場集中の概要

- 企業プロファイル

- S&D coffee makers.Inc

- National Presto Industry.Inc

- Lavazza

- Regal Ware

- Quench

- Dynamo Aviation US

- Lancaster Commercial Product

- Espresso Supply

- Simpli Press

- Starbucks

第7章 市場機会と今後の動向

第8章 免責事項と出版社について

The Household Coffee Machine Market size is estimated at USD 13.65 billion in 2025, and is expected to reach USD 18.64 billion by 2030, at a CAGR of 6.42% during the forecast period (2025-2030).

The coffee market includes Asia Pacific, North America, Latin America, Europe, the Middle East, and Africa. Brazil (Latin America) is the world's largest producer of coffee. As per Yahoo Finance, the largest coffee market in 2021 is Tully's Coffee, Owned by Keurig Dr. Pepper Inc, The Coffee Bean & Tea Leaf, and Caffe Ritazza, Owned by SSP Group, Coffee Beanery, Caffe Nero, McCafe; Owned by McDonald's Corporation.

Covid-19 had a major impact on the global household coffee machine market, with disruption in the supply chain occurring for both the coffee and coffee machine markets. The working environment changed from office to home. As a result, it created a scope for the coffee machine market in households. It changes the investment environment in the coffee industry with strict lockdowns increasing, creating an environment where people only spend on the necessary environment. Price of raw materials saw a continuous increase because of Covid-19 and the Russia-Ukraine war going on at present, even with good harvest high cost of gas increase price of coffee machines as well as the coffee we drink.

As Covid cases are continuously reducing and those who lost employment during covid are returning to work with an increase in income, creating a positive environment for the coffee machine market in households and firms. Disruption in supply change and increasing price of raw material has been stabilized, creating a positive environment for consumers and producers. The out-of-house coffee market is expected to have a large share compared to in-house consumption, so focus must be shifted towards automated coffee machine markets that firms, cafes, and shops demand.

Household Coffee Machine Market Trends

Low Coffee consumption in Coffee producing nation driving coffee machine market to find new business opportunity.

Ready-to-drink (RTD) coffee is showing an increasing trend in the market and is being perceived as a healthier optimal substitute to soda; iced and cold coffee is becoming a premium beverage and raising opportunities for the coffee machine market with new features. The brewing method is also changing from a traditional drip coffee machine to a single cup brewer with a fixed amount being dispensed at a point.

Consumption of coffee in coffee-producing nations is not highlighted, the potential impact might be because of colonialization of the region, and coffee was transplanted only for export purposes. There exist the potential for domestic consumption in producing nations which can lead to an increase in total market value created by producing nation and leading more opportunity for market expansion in the coffee machine market.

In India, Arabica and Robusta are the varieties of coffee which are mostly produced. An increase in both varieties is observed with the current production level during (2022) existing at (103100 MT and 350400 MT). Continuous fluctuation is observed in India's coffee market price, creating a burden on household coffee consumption with which a need arises for coffee machine makers to reduce the price of household coffee machines to increase their sales and lead the market after disruptions caused by the pandemic.

Effect of Covid-19 on global coffee machine market leading to change in Coffee machine makers business strategy.

COVID 19 pandemic negatively impacted the growth of the coffee pod machine market. This is when major mergers and acquisitions occur between firms to maintain their supernormal profit. The market is expected to grow after this covid impact with over 1.42 million units. A strategic partnership among vendors will offer immense growth opportunities with major market participants such as Bunn-O-Matic Corp, Hamilton Beach Brand Holding Co, Jacob Douwe Egberts BV, Keurig Dr. Pepper Inc, Koninklijke Philips NV, Luigi Lavazza, Masimo Zanetti Beverage Group Spa, Melitta Group, Nestle.

Coffee in developing and developed nations are becoming increasingly popular. With no longer now a traditional beverage but a youthful and trendy beverage. In India, the maximum consumption of coffee is in the east zone, with the North and west zone coming afterward.

The coffee market is driven by the consumer base of those who intake coffee, and the leading nations in coffee consumption are the western part of the globe. Automating coffee machines and adding new advanced features is where whole coffee machine makers compete. Offices opening and people returning to work will increase demand for coffee machines in households and offices.

Household Coffee Machine Industry Overview

The United States is the leading Automated Coffee machine market. Nearly 50% of the automated coffee machine demand out of total production comes from North America, with approximately 70 % originating from the United States. With a revolutionary period for electricity use in gadgets and star ratings applied to them, the German coffee machine market offers energy-efficient products focusing on reduction in (GHG). With increasing coffee consumption, China and India offer lucrative automated automatic coffee machine sales opportunities. Automation within coffee machines is increasing with time, causing competition for launching advanced products in the market.

The largest coffee companies in the world during 2022 are Starbuck, Dunkin, Tim Horton, and Dutch Bros Coffee. Starbux, the largest coffee company in the world, has nearly 33,000 stores in 2021, i.e., three times more than its nearest competitor, Dunkin. From some studies, it was observed that even after covid, the level of coffee consumption is the same, but people are brewing more at home and less in cafes, allowing coffee machine makers to penetrate more households.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Insights on impact of technology and innovation in Coffee Machine Market

- 4.5 Insights on Product Technology

- 4.6 Industry Attractiveness - Porters' Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Distribution Channel

- 5.1.1 Multibrand Store

- 5.1.2 Speciality Store

- 5.1.3 Online Store

- 5.1.4 Other Distribution Channel

- 5.2 By Product Type

- 5.2.1 Filter coffee machine

- 5.2.2 Capsule or Pod coffee machine

- 5.2.3 Traditional Espresso coffee machine

- 5.2.4 Bean to Cup coffee machine

- 5.3 Operational Cateogry

- 5.3.1 Semi Automated

- 5.3.2 Automated

- 5.4 By Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concetration Overview

- 6.2 Company Profiles

- 6.2.1 S&D coffee makers.Inc

- 6.2.2 National Presto Industry.Inc

- 6.2.3 Lavazza

- 6.2.4 Regal Ware

- 6.2.5 Quench

- 6.2.6 Dynamo Aviation US

- 6.2.7 Lancaster Commercial Product

- 6.2.8 Espresso Supply

- 6.2.9 Simpli Press

- 6.2.10 Starbucks