|

|

市場調査レポート

商品コード

1430578

家畜用ワクチンの世界市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Global Livestock Vaccines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 家畜用ワクチンの世界市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

家畜用ワクチンの世界市場規模は2024年に58億8,000万米ドルと推定され、2029年には72億3,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは4.21%で成長する見込みです。

COVID-19パンデミックは、家畜用ワクチンを含むすべての産業に影響を与えています。主に製造拠点の一時閉鎖、輸出禁止、COVID-19医薬品の需要増加により、いくつかの国で動物用医薬品の供給途絶と不足が観察されています。各国政府は医薬品の供給を緩和するための対策を講じています。2020年7月、疾病管理予防センターにより、COVID-19パンデミック時にコンパニオンアニマルを治療するための特定の予防的ガイドラインが獣医専門家に示されました。さらに、疾病管理予防センターのような多くの政府当局は、動物病院や診療所に対し、緊急かつ緊急の診察や処置を優先するよう推奨しています。このような国家機関によるイニシアチブは、動物ヘルスケア管理における診断機器への依存度と使用率を低下させる可能性があります。従って、コンパニオンアニマル用ワクチン市場には、主にCOVID-19発生時の獣医師による診察の減少により、短期的に若干のマイナスの影響が見られます。

世界的に、畜産部門では肉や乳製品などの畜産物に対する需要が増加しています。この動向は従来、北米や欧州の先進諸国で顕著であったが、過去10年間にアジア太平洋やラテンアメリカの新興諸国で畜産物需要が大幅に増加しています。

これは主に、急速な都市化と経済成長と相まって、これらの地域で人口が増加していることに起因しています。畜産動物で特定の疾病が繰り返し発生することで、畜産セクターの利害関係者の間で動物の健康や予防的な動物ヘルスケアアプローチへの関心が高まり、動物用ワクチン市場の成長を支えるものと期待されています。

コロナウイルスは、接触感染やエアロゾル感染によって動物から動物へと広がり、他の動物に感染します。COVID-19に感染した養殖ミンクなどの事件は、2020年後半に米国やデンマークなど多くの国で報告されました。それにより、このような事件はCOVID-19動物ワクチンの必要性を引き起こしました。その結果、市場関係者はCOVID-19に対する動物用ワクチンの製造に乗り出しています。例えば、Zoetis社は、動物園の動物の健康と福祉を守るために、実験的なCOVID-19ワクチンを11,000回分以上寄贈しようとしています。一方、2021年4月、ロシアは動物用のCarnivac-Covと呼ばれる世界初のCOVID-19ワクチンを登録しました。このように、家畜および野生動物におけるCOVID-19感染症例の増加は、予防的な動物の健康を守るための動物ワクチンの受け入れを促進し、その結果、業界の成長を急上昇させています。

2021年6月、英国政府は英国に動物ワクチン製造イノベーションセンターを設立すると発表しました。家畜用ワクチンの開発を加速させ、コロナウイルスを含むウイルス性疾患の蔓延を抑制することを目的としています。このセンターの設立には、英国政府が2,479万米ドル、Bill & Melinda Gates Foundationが1,943万米ドルを拠出しています。このように、市場各社が採用する研究イニシアティブ、動物におけるCOVID-19感染事例の増加、政府の支援は、家畜用ワクチン産業の大幅な拡大を可能にします。

さらに、シェア維持と製品ポートフォリオの多様化を図るため、大手企業はM&A、提携、新製品発売など様々な戦略を頻繁に選択しています。例えば、2021年2月、Cevaは動物由来の感染症予防と動物の健康増進の研究開発のため、フランス国立農業・食品・環境研究所(INRAE)と提携しました。同様に2021年1月、ゾエティスは感染性滑液包病(IBD)から家禽を守るためのPoulvac Procerta HVT-IBDワクチンを発売しました。

しかし、ワクチンの保管コストが高く、ワクチンを投与する獣医師や熟練した農場労働者の不足が、家畜用ワクチン市場の成長を抑制すると予想されています。

家畜用ワクチン市場動向

家禽用ワクチンが家畜用ワクチン市場で大きなシェアを占める見込み

家禽には、卵、肉、羽毛を目的として人間に飼われている家禽が含まれます。家禽は世界で最も生産量の多い家畜です。国連食糧農業機関の統計によれば、世界の鶏の平均飼育数は10億羽近く、1人当たり3羽です。さらに、家禽類の生産は今後も増加すると予想されています。

2020年12月、インドの9つの州で鳥インフルエンザの発生が報告されました。このため、鶏肉製品の価格が下がり、畜産業全体に深刻な影響を及ぼしています。インド家禽連盟によると、2020年12月現在、鶏肉の消費量は50%に減少し、価格は30%下落しています。ほとんどのアジア諸国がワクチン政策を採用しているのに対し、インドは主に鳥の淘汰に頼っています。パンジャブ州とハリヤナ州政府はワクチン接種の合法化を間近に控えており、同分野の成長にプラスに働くと期待されています。

米国農務省対外農業庁の2022年1月報告書「家畜と家禽」によると、世界の家畜市場と貿易は、家畜の淘汰に頼っている:世界市場と貿易'によると、2022年の世界の鶏肉生産量は1億80万トンと予測され、10月からほぼ横ばいです。同様に、2022年の世界の鶏肉輸出量は1%増の1,340万トンです。

したがって、鶏肉生産量の増加に伴い、疾病に罹患する家禽の数も増加すると予想されます。この対策として、農家は将来の経済的損失を防ぐために予防ワクチンを選ぶと予想されます。これは家畜用ワクチン市場の成長に貢献すると予想されます。

北米が市場を独占する見込み

北米は、高品質な食品とより良い動物の健康のために、動物用ワクチンの採用が増加していることから、成長が見込まれています。

米国農務省および食糧農業機関による2022年1月の報告書によると、米国の全飼育場における食肉市場向けの牛および子牛の飼料在庫は、2022年1月に1,470万頭となった。この在庫は2021年1月の合計1,470万頭からわずかに増加しています。収容頭数1,000頭以上の肥育場で飼養されている牛は、2022年1月1日時点の飼料牛全体の81.9%を占め、前年よりわずかに増加しました。

さらに米国では、ワクチン開発の進歩として、生ベクターワクチン、非複製組み換え抗原ワクチン、核酸媒介ワクチン、生遺伝子欠失ワクチンの開発が進んでいます。例えば、2020年1月、大手動物医療企業であるZoetisは、ニューカッスル病ウイルスとマレック病ウイルスに対する防御のためのベクター組み換えワクチンであるPoulvac Procerta HVT-NDを導入することにより、家禽ワクチンのポートフォリオをさらに拡大しました。

さらに、北米諸国である米国とカナダは、医療制度が整備され、発達しています。これらの制度は研究開発も奨励しています。こうした政策が、米国やカナダへの世界企業の進出を後押ししています。その結果、これらの国々は多くの世界市場プレーヤーの存在を享受しています。この地域における世界企業の存在によって高い需要が満たされるため、市場はさらに拡大すると予想されます。

家畜用ワクチン産業の概要

家畜用ワクチン市場はかなり競争が激しく、複数の主要企業で構成されています。家畜用ワクチンの大半は、世界の主要企業によって製造されています。より多くの研究資金と優れた流通システムを持つ市場リーダーが、市場での地位を確立しています。さらに、アジア太平洋地域では、畜産業に対する意識の高まりから、小規模プレーヤーが台頭してきています。これも市場の成長を後押ししています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 人獣共通感染症の増加

- 様々な政府機関、動物協会、大手企業による取り組み

- 食品安全への注目の高まり

- 市場抑制要因

- 獣医師の不足と熟練した農場労働者の不足

- ワクチンの高い保管コスト

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 製品タイプ別

- 牛用ワクチン

- 家禽用ワクチン

- 豚ワクチン

- その他の家畜用ワクチン

- 技術別

- 生ワクチン

- 不活化ワクチン

- トキソイドワクチン

- 組み換えワクチン

- その他の技術

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- AniCon Labor GmbH

- Animal Science Products Inc.

- Biovac

- Boehringer Ingelheim International GmbH

- ADL BIONATUR SOLUTIONS, S.A.

- Ceva Sante Animale

- Elanco

- Merck & Co.

- Phibro Animal Health Corporation

- Zoetis Inc

第7章 市場機会と今後の動向

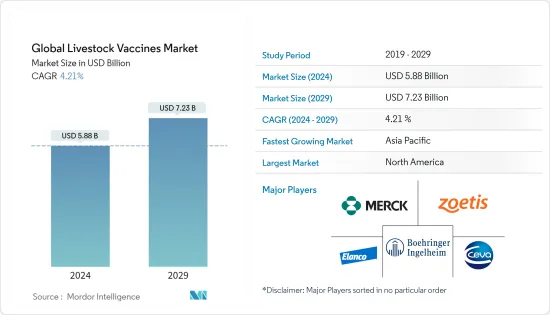

The Global Livestock Vaccines Market size is estimated at USD 5.88 billion in 2024, and is expected to reach USD 7.23 billion by 2029, growing at a CAGR of 4.21% during the forecast period (2024-2029).

The COVID-19 pandemic has impacted all industries, including livestock vaccines. Supply disruption and shortages of veterinary medicines have been observed in several countries, primarily due to the temporary lockdowns of manufacturing sites, export bans, and increased demand for COVID-19 medicines. Governments are taking measures to mitigate the supply of medicines. Certain specific and precautionary guidelines were given to veterinary professionals to treat companion animals during the COVID-19 pandemic by the Centers for Disease Control and Prevention in July 2020. Additionally, many government authorities, such as the Centers for Disease Control and Prevention, recommended veterinary hospitals and clinics prioritize urgent and emergency visits and procedures. This initiative by such national bodies may reduce the dependence on and usage of diagnostic equipment in veterinary healthcare management. Hence, a slight short-term negative impact is witnessed on the companion livestock vaccine market, primarily due to the reduced veterinary visits during the COVID-19 outbreak.

Globally, the livestock sector is witnessing an increased demand for livestock products such as meat and dairy products. Though this trend has traditionally been evident in developed countries across North America and Europe, demand for livestock products has increased significantly in emerging Asia Pacific and Latin American countries over the past decade.

This can primarily be attributed to the growing population in these regions, coupled with the rapid urbanization and economic growth. The repeated outbreaks of certain diseases in livestock animals are expected to support growth of the veterinary vaccines market by increasing the focus on animal health and preventive animal healthcare approaches among stakeholders in the livestock sector.

The coronavirus spreads from animal to animal with contact or aerosol transmission, thus infecting other animals. Incidents such as COVID-19 infected farmed minks were reported in numerous nations such as the U.S. and Denmark during late 2020. Thereby, such incidents have triggered the need for the COVID-19 animal vaccine. As a result, the market players are getting involved to manufacture veterinary vaccines against COVID-19. For instance, Zoetis is in process of donating over 11,000 doses of its experimental COVID-19 vaccine to help protect the health and well-being of Zoo animals. On the other hand, in April 2021, Russia has registered the world's first Covid-19 vaccine called Carnivac-Cov for animals. Thus, the growing cases of COVID-19 infections in domestic and wild animals will promote the acceptance of animal vaccines for safeguarding preventive animal health, thus soaring the industry growth.

In June 2021, the Government of the United Kingdom announced the establishment of a United Kingdom. Animal Vaccine Manufacturing and Innovation Centre in Surrey, intending to accelerate the vaccine development for livestock and to control the spread of viral diseases including coronavirus. The United Kingdom government will contribute USD 24.79 million while the Bill & Melinda Gates Foundation will contribute USD 19.43 million to establish this center. Thereby, the research initiatives adopted by the market players, growing COVID-19 infection cases in animals, and government support will enable the significant expansion of the livestock vaccines industry.

In addition, in an attempt to retain share and diversify the product portfolio, major players are frequently opting for various strategies such as mergers and acquisitions, partnerships, and new product launches. For instance, in February 2021, Ceva partnered with the French National Research Institute for Agriculture, Food, and Environment (INRAE) for R&D in the prevention of infectious diseases from animal origin and improvement of animal health. Similarly, in January 2021, Zoetis launched the Poulvac Procerta HVT-IBD vaccine for the protection of poultry against Infectious Bursal Disease (IBD).

However, high storage cost of vaccines and lack of veterinarians and skilled farm workers to administer vaccines is expected to restrain the Livestock Vaccines market growth.

Livestock Vaccines Market Trends

Poultry Vaccine is Expected to Cover a Large Share of the Livestock Vaccines Market

Poultry includes domesticated birds kept by humans for their eggs, their meat, or their feathers. Poultry is the most produced livestock in the world. The world's average stock of chickens is nearly19 a billion, or three per person, according to statistics from the United Nations Food and Agriculture Organisation. Moreover, the production of poultry is expected to increase in the future.

In December 2020, a bird flu outbreak was reported in 9 Indian states. Due to this, the price of poultry products has gone down, severely affecting the overall livestock industry. According to the Poultry Federation of India, chicken consumption has reduced to 50%, with a drop of 30% in the prices, as of December 2020. While most Asian countries have adopted vaccination policies, India has primarily resorted to the culling of birds. Punjab and Haryana state governments are close to legalizing vaccinations, which is expected to positively impact the segment's growth.

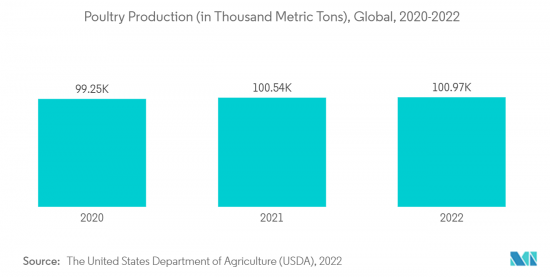

According to the United States Department of Agriculture, Foreign Agricultural Service, January 2022 report 'Livestock and Poultry: World Markets and Trade,' global chicken meat production for 2022 is forecast at 100.8 million tons, virtually unchanged from October. Similarly, global chicken meat exports for 2022 are raised by 1% to 13.4 million tons.

Therefore with the increasing poultry production, the number of poultry affected by the diseases is also expected to increase. To counter this, the farmers are expected to opt for preventive vaccines to prevent future economic loss. This is expected to help the growth of the Livestock Vaccines Market.

North America is Expected to Dominate the Market

North America is expected to grow due to the increasing adoption of veterinary vaccines for quality food products and for better animal health.

As per the January 2022 report by the United States Department of Agriculture and the Food and Agriculture Organization, cattle and calves on feed for the slaughter market in the United States for all feedlots totaled 14.7 million head in January 2022. The inventory is up slightly from the January 2021 total of 14.7 million heads. Cattle on feed in feedlots with a capacity of 1,000 or more head accounted for 81.9 percent of the total cattle on feed on January 1, 2022, up slightly from the previous year.

Additionally, in the United States, advancements in vaccine development include the development of live vector vaccines, non-replicating recombinant antigen vaccines, nucleic acid-mediated vaccines, and live-gene-deleted vaccines. For instance, in January 2020, Zoetis, a leading animal health company, further expanded its poultry vaccine portfolio by introducing Poulvac Procerta HVT-ND, a vectored recombinant vaccine for protection against Newcastle and Marek's disease viruses.

Moreover, the North American countries of the United States and Canada have a developed and well-structured health care system. These systems also encourage research and development. These policies encourage global players to enter the US and Canada. Hence, as a result, these countries enjoy the presence of many global market players. As high demand is met by the presence of global players in the region, the market is further expected to increase.

Livestock Vaccines Industry Overview

The livestock vaccines market is fairly competitive and consists of several major players. The majority of livestock vaccines are being manufactured by the global key players. Market leaders with more funds for research and better distribution system have established their position in the market. Moreover, Asia-pacific is witnessing an emergence of some small players due to the rise of awareness and the livestock industry in the region. This has also helped the market grow.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Incidences of Zoonotic Diseases

- 4.2.2 Initiatives Taken by Various Government Agencies, Animal Associations, and Leading Players

- 4.2.3 Widened Focus on Food Safety

- 4.3 Market Restraints

- 4.3.1 Lack of Veterinarians and Shortage of Skilled Farm Workers

- 4.3.2 High Storage Costs for Vaccines

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Product Type

- 5.1.1 Bovine Vaccine

- 5.1.2 Poultry Vaccine

- 5.1.3 Porcine Vaccine

- 5.1.4 Other Livestock Vaccines

- 5.2 By Technology

- 5.2.1 Live Attenuated Vaccine

- 5.2.2 Inactivated Vaccine

- 5.2.3 Toxoid Vaccine

- 5.2.4 Recombinant Vaccine

- 5.2.5 Other Technologies

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle-East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 AniCon Labor GmbH

- 6.1.2 Animal Science Products Inc.

- 6.1.3 Biovac

- 6.1.4 Boehringer Ingelheim International GmbH

- 6.1.5 ADL BIONATUR SOLUTIONS, S.A.

- 6.1.6 Ceva Sante Animale

- 6.1.7 Elanco

- 6.1.8 Merck & Co.

- 6.1.9 Phibro Animal Health Corporation

- 6.1.10 Zoetis Inc