|

市場調査レポート

商品コード

1430567

世界のペット糖尿病ケア - 市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Global Pet Diabetes Care - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 世界のペット糖尿病ケア - 市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

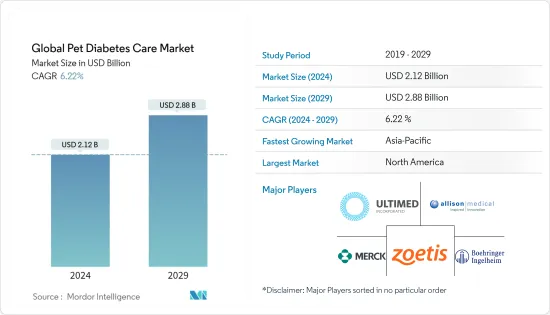

世界のペット糖尿病ケア市場規模は2024年に21億2,000万米ドルと推定され、2029年には28億8,000万米ドルに達すると予測され、予測期間(2024年~2029年)のCAGRは6.22%で成長すると予測されます。

COVID-19はペット用糖尿病市場に大きな影響を与えました。COVID-19の大流行は、マーケティングや販売活動の減少、動物病院を訪れる人の減少、定期的なペット検診の中止、動物病院でのインスリン投与の減少など、世界のペット動物健康分野にハードルと懸念を課しました。2021年に発表された「犬の糖尿病はパンデミックの間に10~20%増加した:COVID-19の間、犬の糖尿病の症例は10-20%増加しました。監禁と規制が強化されたため、定期的な健康診断が不足し、犬の糖尿病の症例が増加しました。したがって、COVID-19はペットの糖尿病ケア市場に顕著な影響を与えました。

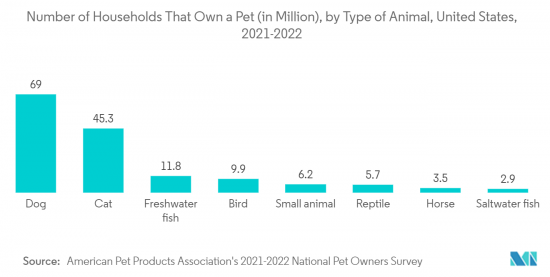

市場成長の主な要因としては、ペット動物の糖尿病有病率の上昇、ペット飼育の増加、ペット人口の増加などが挙げられます。例えば、米国ペット用品協会の2021-2022年全国ペット所有者調査によると、米国では6,900万世帯が犬をペットとして飼っており、4,530万世帯が猫をペットとして飼っています。ここ数年、犬や猫を含む動物を人間のお気に入りのパートナーとして飼う人が大幅に増加しています。犬や猫は最も好まれるペットであるだけでなく、人間の心身の健康を増進させることでも知られています。先進諸国がコンパニオンアニマルの飼育で主導的な地位を占めているのは、とりわけ恵まれた経済状況などのいくつかの要因によるものです。

さらに、American Pet Products Associationの2021-2022年National Pet Owners Surveyによると、犬と猫の外科獣医にかかる基本的な年間費用はそれぞれ458米ドルと201米ドルです。従って、ペット動物の採用の増加は、これらの動物の健康管理の必要性への支出を増加させることが予想され、予測期間中の市場の成長を後押しすることが期待されます。

従って、ペット動物、特に猫と犬の高い人口に支えられて、調査された市場は顕著な規模を持っています。したがって、ペット飼育の増加が予測期間中のペット糖尿病市場の牽引役となっています。しかし、糖尿病治療薬の高コストと薬やインスリンに関する副作用が市場の成長を抑制しています。

ペット糖尿病ケア市場動向

薬剤タイプ別インスリン療法セグメントが最大の市場シェアを占める見込み

糖尿病の犬や猫に対するインスリン治療はケアの基本であり、多くの種類のインスリンが効率的であることが示されています。インスリンは、末梢でのグルコース消費を増加させ、肝グルコースの産生を抑制することで血糖値を低下させる。インスリンは、細胞のグルコースに対する耐性を低下させることで、β細胞の死滅の進展を防ぐ。猫の中でも、インスリンはアミロイドポリペプチド膵島からのアミロイド沈着物の発生を禁止するのに役立ちます。したがって、インスリンはイヌとネコの糖尿病をコントロールするための最も効果的な治療薬であることは間違いないです。

競合他社の存在、糖尿病分野の研究開発、M&Aは市場の成長を後押しします。例えば、2022年に発表された「Ultralongacting recombinant insulin for the treatment of diabetes mellitus in dogs(イヌの糖尿病治療のための超高活性組換えインスリン)」というタイトルの論文によると、この研究では、合成インスリンとイヌFcの組換え融合タンパク質(AKS218d)を週1回皮下投与することで、臨床症状、体重のコントロール、血糖値の維持が達成されたことが示されています。さらに、カニンスリン・ベツリンとプロジンクは動物用医薬品として正式に登録されています。カニンスリン/ベツリンは、犬と猫の両方への使用が承認されている豚レンテインスリンです。作用時間は中程度です。一方、プロジンク(ベーリンガーインゲルハイム)はプロタミン亜鉛インスリン(PZI)の誘導体で、猫への使用が承認されており、糖尿病の犬の管理にも使用できます。

さらに、猫の糖尿病も広く研究されており、市場の成長につながる調査も行われています。例えば、2021年に発表された「An ultra-long-acting recombinant insulin for the treatment of diabetes mellitus in cats(猫の糖尿病治療のための超長時間作用型リコンビナントインスリン)」というタイトルの論文によると、この週1回の新規インスリン治療により、臨床症状のコントロールと血糖値の維持に成功したことが示されています。糖尿病患者の増加とペットの糖尿病に関する調査イニシアチブの増加は、予測期間中に市場プレーヤーに多くの機会を創出すると予想されます。

上記の要因により、インスリンセグメントは予測期間中に成長すると予想されます。

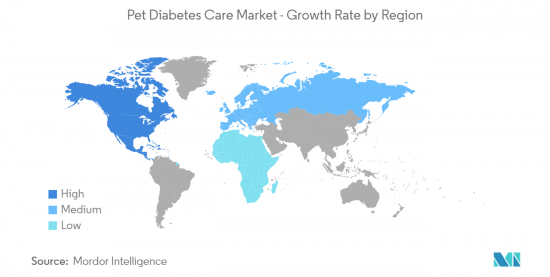

北米が予測期間中に市場を独占する見込み

北米地域では、ペット飼育の増加とペットへの支出の増加が市場全体の成長を押し上げると予想されます。米国ペット用品協会(APPA)が実施した2021年~2022年全国ペット所有者調査によると、北米のペット産業支出総額は1,236億米ドルで、2020年の1,036億米ドルから19%増加しました。

さらに、北米ペット健康保険協会(NAPHIA)の「State of the Industry Report 2022 Highlights」によると、米国におけるペット保険の保険料総額は約26億米ドルでした。2021年末時点で米国で保険に加入しているペットの総数は390万匹で、2020年から28%増加しました。犬の平均傷害・疾病保険料は年583米ドル、月49米ドルでした。保険に加入しているペットはカリフォルニア州、ニューヨーク州、フロリダ州で最も多いです。保険に加入しているペットの最多は犬で82%、対して猫は18%でした。カナダでは77.5%が犬で、猫は22.5%だった。

この市場で事業を展開する主要企業は、より大きな市場シェアを獲得するために、買収、提携、調査、新製品の発売といった新たな戦略に注力しています。例えば、2021年2月にCanine Diabetes Genetics Partnershipが「Genetics of canine diabetes mellitus part 1:研究チームは、遺伝子変異が犬の糖尿病発症リスクと関連する複雑性に寄与する可能性がある方法を研究し、実証しました。

上記の要因から、北米地域は予測期間中に成長すると予想されます。

ペット糖尿病ケア産業の概要

ペット糖尿病ケア市場は統合市場です。市場参入企業には、Allison Medical、Apotex Inc.、Becton, Dickinson and Company、Boehringer Ingelheim Vetmedica Inc.、Henry Schein Animal Health、MED TRUST、Merck &Co.Inc.、UltiMed Inc.、Zoetis Inc.

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- ペット動物における糖尿病と肥満の有病率の上昇

- ペット飼育の増加

- 市場抑制要因

- 糖尿病治療薬の高コスト

- 薬の副作用

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 薬剤タイプ別

- インスリン療法

- 経口薬

- デバイスタイプ別

- グルコースモニタリングデバイス

- インスリン送達デバイス

- 動物タイプ別

- イヌ

- ネコ

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Allison Medical

- Becton, Dickinson and Company

- Boehringer Ingelheim

- Covetrus

- Merck & Co. Inc

- MED TRUST

- Taidoc Technology Corporation

- UltiMed Inc.

- Zoetis Inc

第7章 市場機会と今後の動向

The Global Pet Diabetes Care Market size is estimated at USD 2.12 billion in 2024, and is expected to reach USD 2.88 billion by 2029, growing at a CAGR of 6.22% during the forecast period (2024-2029).

COVID-19 had affected the pet diabetes market significantly. The COVID-19 pandemic imposed hurdles and concerns in the global pet animal health sector, including decreased marketing and sales efforts, reduced people visiting veterinary clinics, cancellation of regular pet check-ups, and fewer instances of insulin administration in veterinary facilities. As per the article published in 2021 under the title 'Diabetes among dogs increased by 10-20% during pandemic: Vets', cases of diabetes in dogs have increased 10-20% during COVID-19. Due to the increased lockdown and restrictions, there was a lack of routine checkups which lead to more cases of diabetes in dogs. Hence COVID-19 had a notable impact in the pet diabetic care market.

The major factors for the growth of the market include the rising prevalence of diabetes in pet animals, an increase in pet adoption, and the growing pet population. For instance, as per the American Pet Products Association's 2021-2022 National Pet Owners Survey, 69 million United States Household has a dog as a pet and 45.3 million households has a cat as a pet. The past few years have observed a significant rise in the adoption of animals, including dogs and cats as the favorite companions of human beings. Dogs and cats are not only the most preferred pets but are also known to improve the physical and mental health of humans. The developed countries have the leading position in companion animal ownership, owing to several factors, like favorable economic conditions, among others.

Furthermore, according to the American Pet Products Association's 2021-2022 National Pet Owners Survey, the basic annual expenses for Dogs and Cats for surgical vets are USD 458 and USD 201 respectively. Thus, the rise in adoption of pet animals is expected to increase the spending on health care needs of these animals which would in turn expected to boost the growth of the market over the forecast period.

Therefore, the market studied has a remarkable size, supported by the high population of pet animals, particularly cats and dogs. Hence, the increase in pet adoption has helped in driving the pet diabetes market over the forecast period. However, the high cost of diabetic medication and side effects relating to medicines and insulin restrain the market growth.

Pet Diabetes Care Market Trends

Insulin Therapy Segment by Drug Type is expected to Hold Largest Market Share

Insulin treatment for diabetic dogs and cats is the foundation of care and many types of insulin were shown to be efficient. Insulin reduces blood glucose levels by increasing peripheral consumption of glucose and by suppressing the production of hepatic glucose. Insulin prevents the development of the death of beta-cells by reducing the cell's tolerance of glucose. Among cats, insulin helps to prohibit amyloid deposits from the amyloid polypeptide islet from developing. Therefore, insulin is undoubtedly the most effective remedy for the control of diabetes in canines and felines.

The presence of competitors, research and development in the field of diabetes, and mergers and acquisitions boost the market growth. For instance, as per the article published in 2022 under the title 'Ultralongacting recombinant insulin for the treatment of diabetes mellitus in dogs', the study showed that control of clinical signs, body weight, and maintenance of glycemia was achieved with a recombinant fusion protein of synthetic insulin and canine Fc (AKS218d) administered subcutaneously onceweekly. Furthermore, Caninsulin / Vetsulin and ProZinc are officially registered for veterinary use. Caninsulin / Vetsulin is porcine Lente insulin approved for use in both dogs and cats. It has a moderate duration of action. While, ProZinc (Boehringer Ingelheim) is a derivative of protamine zinc insulin (PZI), which is approved to be used in cats and can be used in the management of diabetic dogs.

Moreover, diabetes in cats is also being studied widely and research is conducted which leads to market growth. For instance, according to the article published in 2021 under the title 'An ultra-long-acting recombinant insulin for the treatment of diabetes mellitus in cats', the study showed a successful control of clinical signs and maintenance of glycemia was achieved with this once-weekly novel insulin treatment. The rising cases of diabetes and increased research initiatives on pet diabetes are expected to create more opportunities for the market players over the forecast period.

As per the factors mentioned above, the insulin segment is expected to grow over the forecast period.

North America is Expected to Dominate the Market During The Forecast Period

In North America region the rising pet adoption and increasing expenditure on them are expected to boost the overall growth of the market. According to the 2021-2022 National Pet Owners Survey, conducted by the American Pet Products Association (APPA), total pet industry expenditures in the United totaled USD 123.6 billion, up 19% from USD 103.6 billion in 2020.

Furthermore, the North American Pet Health Insurance Association's (NAPHIA) State of the Industry Report 2022 Highlights stated that the total premium volume for pet insurance in the United States was nearly USD 2.6 billion. The total number of pets insured in the United States at year-end 2021 was 3.9 million, a 28% increase since 2020. The average accident and illness premium for dogs was USD 583 a year or USD 49 a month. The largest share of insured pets lives in California, New York, and Florida. The largest number of pets insured were dogs at 82 % versus cats at 18 %. In Canada, 77.5% of insured pets were dogs versus 22.5% of cats.

The key players operating in the market are found focusing on new strategies, such as acquisitions, collaborations, research, and new product launches, to capture larger market shares. For instance, in February 2021, Canine Diabetes Genetics Partnership published an article under the title ' Genetics of canine diabetes mellitus part 1: Phenotypes of disease', the team studied and demonstrated the ways in which genetic variants may contribute to a risk of developing diabetes in dogs and the related complexities.

As per the factors mentioned above the North, America region is expected to witness growth over the forecast period.

Pet Diabetes Care Industry Overview

The pet diabetes care market is consolidated market. Some of the market players in the market are Allison Medical, Apotex Inc., Becton, Dickinson and Company, Boehringer Ingelheim Vetmedica Inc., Henry Schein Animal Health, MED TRUST, Merck & Co. Inc, UltiMed Inc., and Zoetis Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Diabetes and Obesity in Pet Animals

- 4.2.2 Increase in Pet Adoption

- 4.3 Market Restraints

- 4.3.1 High Cost of Diabetes Medications

- 4.3.2 Adverse Reaction of Medications

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Million)

- 5.1 By Drug Type

- 5.1.1 Insulin Therapy

- 5.1.2 Oral Medication

- 5.2 By Device Type

- 5.2.1 Glucose Monitoring Devices

- 5.2.2 Insulin Delivery Devices

- 5.3 By Animal Type

- 5.3.1 Canine

- 5.3.2 Feline

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle-East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Allison Medical

- 6.1.2 Becton, Dickinson and Company

- 6.1.3 Boehringer Ingelheim

- 6.1.4 Covetrus

- 6.1.5 Merck & Co. Inc

- 6.1.6 MED TRUST

- 6.1.7 Taidoc Technology Corporation

- 6.1.8 UltiMed Inc.

- 6.1.9 Zoetis Inc