|

市場調査レポート

商品コード

1430562

ヘリコプター用ブレード:市場シェア分析、産業動向&統計、成長予測(2024~2029年)Helicopter Blades - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ヘリコプター用ブレード:市場シェア分析、産業動向&統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 95 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

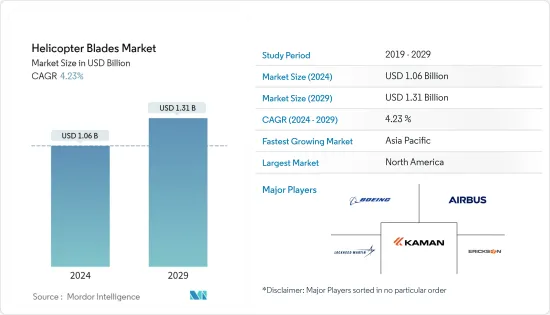

ヘリコプター用ブレード市場規模は2024年に10億6,000万米ドルと推定され、2029年には13億1,000万米ドルに達すると予測され、予測期間(2024年~2029年)のCAGRは4.23%で成長する見込みです。

主なハイライト

- 航空部門はCOVID-19の大流行により比類なき課題に直面。パンデミックの間、ヘリコプターの受注減少と景気減速が市場成長の妨げとなった。世界中のほとんどの国が国境を閉鎖し、数ヶ月間活動を制限しました。これに伴い、2020年の洋上ヘリコプターの輸送量は15%減少し、2019年の4億8,300万旅客マイルから4億1,000万旅客マイルに落ち込みました。しかし、ヘリコプターの需要増加により、2021年から市場は力強い回復を見せた。

- 商用ヘリコプターは、観光、医療・救急救助サービス、輸送、法執行、オフショアヘリコプターサービスなど、さまざまな分野で使用されています。また、攻撃、敵の防空活動の制圧、兵員の空輸や貨物の補給、消火活動、偵察・観測、監視、偵察、重量物輸送、その他の特殊作戦などの用途により、軍用ヘリコプターの需要が増加しています。さらに、3Dプリンティングのような素材や技術の進歩が市場の成長を支えると思われます。3Dプリンティングは、製品開発や既存製品のカスタマイズを加速させることができます。

ヘリコプター用ブレード市場の動向

軍用ヘリコプター分野は予測期間中に大幅な成長が見込まれる

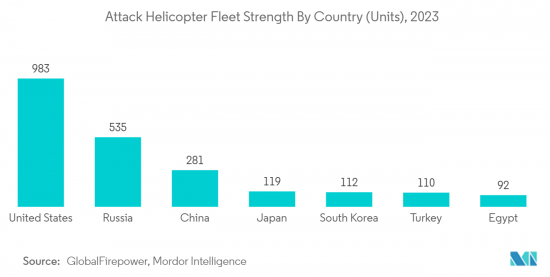

- 軍用ヘリコプターセグメントは、予測期間中にヘリコプター用ブレード市場で大きな成長を示すと思われます。この成長は、先進的な軍用ヘリコプターの調達増加と国防費の増加によるものです。2021年には、世界中の軍用在庫に記載されている戦闘ヘリコプターは19,946機以上でした。

- 戦争の性質の変化と戦術的な機動性の必要性がヘリコプターの需要を高めています。現在進行中のヘリコプター・プロジェクトは、軍用ヘリコプター開発の方向性に前向きな一歩を踏み出したと見ることができます。軍用ヘリコプターは、長年にわたって目覚しい進化を遂げ、戦場で有用であることを証明してきた戦術的プラットフォームです。

- また、老朽化したヘリコプターを置き換える必要性から、新世代のヘリコプターに対する需要が高まっています。例えば、2021年8月、ロッキード・マーチン社の子会社であるシコルスキー社は、米国陸軍契約司令部と、米国陸軍向けブラックホークヘリコプターのメインローターブレードのメンテナンスとオーバーホールを行う5年契約を締結しました。契約金額は1億1,650万米ドル。受注の増加は、メイン・ローター・ブレードやテール・ローター・ブレードを含むヘリコプター部品・コンポーネントの需要をさらに押し上げると思われます。

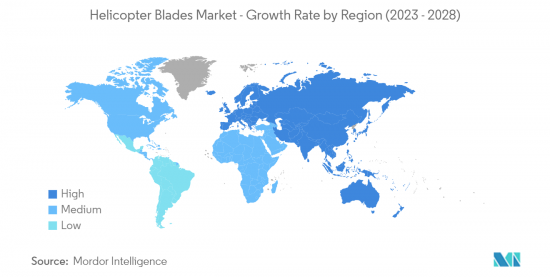

アジア太平洋地域が予測期間中に最も高い成長を遂げる

- アジア太平洋地域は、予測期間中にヘリコプター用ブレード市場で最も高い成長を示すと予測されています。この成長は、空中消火、空中写真撮影、捜索救助、乗員輸送、監視など、様々な商用および軍事用途でのヘリコプターの使用増加によるものです。同地域における回転翼機の主要サプライヤーであるエアバスは、同地域で2,000機以上のエアバス・ヘリコプターが運航していると述べています。また、2022年末時点の地域ヘリコプター保有台数は4,193機となっています。

- ヘリコプターは、特に都市部のシナリオにおいて、ポイント・トゥ・ポイントの移動手段として好まれるようになった。このため、ヘリコプター・チャーター・サービスが急成長しており、複数のチャーター・オペレーターが機体近代化プログラムの一環として新型ヘリコプターの調達を発注しています。

- 中国では、航空医療サービス、緊急対応チーム、捜索救助(SAR)、消防活動などでヘリコプターが重要な役割を果たすため、需要が非常に高いです。この地域のヘリコプターは多様な気候の中で運用される予定であるため、ヘリコプターのブレードはいくつかの天候異変にさらされる可能性があり、その結果、ブレードにひずみや損傷が生じる可能性があります。

- そのため、ヘリコプターの耐空性を確保するためには、アフターマーケットやメンテナンスサービスが必要となります。したがって、ヘリコプターが使用される用途の多様化とそれに伴うメンテナンス活動のために、アジア太平洋地域の市場は予測期間中に高い成長を遂げると予想されます。

ヘリコプター用ブレード産業の概要

ヘリコプター用ブレード市場は、少数の企業が大きなシェアを占めており、適度に統合されています。主な企業は、Kaman Corporation、The Boeing Company、Erickson Incorporated、Airbus SE、Lockheed Martin Corporationなどです。主なOEMは、新しいブレードを開発するだけでなく、生産率を向上させるために、積層造形などの先進技術の導入に注力しています。ヘリコプターOEMはまた、今後数年間で需要をさらに生み出すと予想される新しいヘリコプターモデルを開発しています。

例えば、2023年3月、Leonardo S.p.Iは英国のエンジニアリング会社SFM Technologyおよび3DプリンターメーカーBigRepと協力して、英国海軍のAugustaWestland AW101ヘリコプターの主要部品を3Dプリントしました。同社は、900 x 230 x 160mmの新しいメインローターブレード拘束クレードルを開発しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 用途

- 民間ヘリコプター

- 軍用ヘリコプター

- ブレードタイプ

- メインローターブレード

- テールローターブレード

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ロシア

- イタリア

- その他の欧州

- アジア太平洋

- 中国

- インド

- オーストラリア

- 日本

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- その他のラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Kaman Corporation

- The Boeing Company

- Carson Helicopters, Inc.

- Hindustan Aeronautics Ltd

- Airbus SE

- Lockheed Martin Corporation

- Eagle Aviation Technologies, LLC

- Erickson Incorporated

- Van Horn Aviation, LLC

第7章 市場機会と今後の動向

The Helicopter Blades Market size is estimated at USD 1.06 billion in 2024, and is expected to reach USD 1.31 billion by 2029, growing at a CAGR of 4.23% during the forecast period (2024-2029).

Key Highlights

- The aviation sector faced unmatched challenges due to the COVID-19 pandemic. Decreasing orders for helicopters and an economic slowdown hindered market growth during the pandemic. Most countries across the world have shut down their borders and restricted their activities for several months. On this note, offshore helicopter traffic declined by 15% in 2020, dropping to 410 million passenger miles from 483 million passenger miles in 2019. However, the market showcased a strong recovery from 2021 due to increased demand for helicopters.

- Commercial helicopters are used in different areas, like tourism, medical and emergency rescue services, transportation, law enforcement, and offshore helicopter services. Also, rising demand for military helicopters due to their applications such as attack, suppression of enemy air defense, airlift of troops and cargo resupply, firefighting, reconnaissance and observation, surveillance, scouting, heavy-lift, and other special operations. Moreover, advancements in materials and technologies like 3D printing will support the growth of the market. 3D printing can accelerate product development and customization of existing products.

Helicopter Blades Market Trends

Military Helicopters Segment is Projected to Show Significant Growth During the Forecast Period

- The military helicopters segment will showcase significant growth in the helicopter blades market during the forecast period. The growth is due to increasing procurement of advanced military helicopters and rising defense expenditure. In 2021, there were more than 19,946 combat helicopters listed in military inventories across the globe.

- The changing nature of warfare and the need for tactical mobility have increased the demand for helicopters. The ongoing helicopter projects can be seen as a positive step in the direction of military helicopter development. A military helicopter is a tactical platform that has evolved impressively over the years and has proved itself to be useful on the battlefield.

- Also, the need to replace aging helicopters has propelled the demand for newer-generation helicopters. For instance, in August 2021, Sikorsky, a subsidiary of Lockheed Martin Corporation, signed a five-year contract with the US Army Contracting Command to maintain and overhaul the main rotor blade of Black Hawk helicopters for the US Army. The value of the contract was USD 116.5 million. Increasing orders will further propel the demand for helicopter parts and components, including main and tail rotor blades.

Asia-Pacific to Experience the Highest Growth During the Forecast Period

- Asia-Pacific is anticipated to show the highest growth in the helicopter blades market during the forecast period. The growth is due to the increasing use of helicopters for various commercial and military applications such as aerial firefighting, aerial photography, search and rescue, crew transportation, surveillance, and others. Airbus, a key supplier of rotorcraft in the region, stated that more than 2,000 Airbus helicopters operate across the region. On this note, the regional helicopter fleet stood at 4,193 units at the end of 2022.

- Helicopters have emerged as a preferred mode for point-to-point travel, especially in an urban scenario. This has led to the rapid growth of helicopter charter services, wherein several charter operators have placed orders for procuring new helicopters as part of their fleet modernization programs.

- The demand for helicopters is very high in China due to their critical use in air medical services, emergency response teams, search and rescue (SAR), and firefighting operations. Since helicopters in the region are scheduled to operate in a diversified climate, the helicopter blades may be exposed to several weather anomalies, resulting in potential strain and damage to the blades.

- Hence, aftermarket and maintenance services would be required to ensure the airworthiness of the helicopter fleet. Hence, on account of the diversified plethora of applications that a helicopter can be used for, and the associated maintenance activities, the market in focus in Asia-Pacific is anticipated to witness higher growth during the forecast period.

Helicopter Blades Industry Overview

The helicopter blades market is moderately consolidated in nature, with a presence of few players holding significant shares in the market. Some of the key players in the market are Kaman Corporation, The Boeing Company, Erickson Incorporated, Airbus SE, and Lockheed Martin Corporation. Key OEMs are focused on introducing advanced technologies such as additive manufacturing to develop new blades as well as to increase their production rates. Helicopter OEMs are also developing new helicopter models that are expected to further generate demand in the coming years.

For instance, in March 2023, Leonardo S.p.I collaborated with SFM Technology, a UK-based engineering company, and 3D printer manufacturer BigRep, to 3D print key components for the Royal Navy's AugustaWestland AW101 helicopters. The company developed a new main rotor blade restraint cradle measuring 900 x 230 x 160mm.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Civil Helicopters

- 5.1.2 Military Helicopters

- 5.2 Blade Type

- 5.2.1 Main Rotor Blade

- 5.2.2 Tail Rotor Blade

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Russia

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Australia

- 5.3.3.4 Japan

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Kaman Corporation

- 6.2.2 The Boeing Company

- 6.2.3 Carson Helicopters, Inc.

- 6.2.4 Hindustan Aeronautics Ltd

- 6.2.5 Airbus SE

- 6.2.6 Lockheed Martin Corporation

- 6.2.7 Eagle Aviation Technologies, LLC

- 6.2.8 Erickson Incorporated

- 6.2.9 Van Horn Aviation, LLC