超音波診断装置:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

Ultrasound Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日

- 商品コード

- 1849929

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

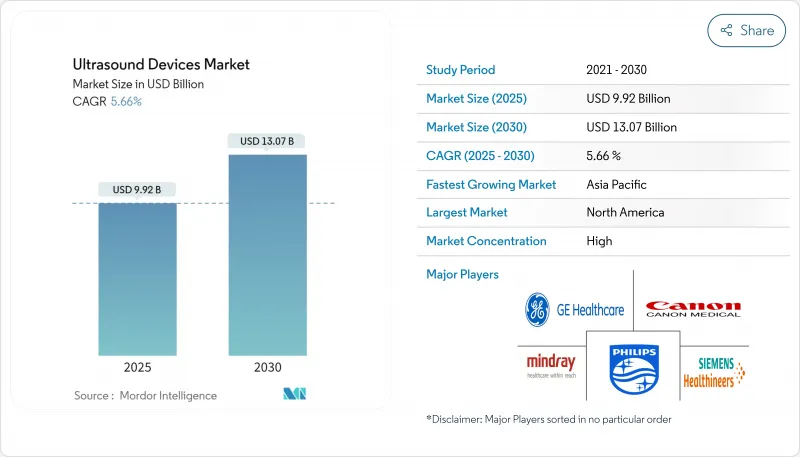

超音波診断装置市場規模は2025年に91億2,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは3.77%で、2030年には109億8,000万米ドルに達すると予測されます。

リアルタイムで放射線を使用しない画像診断に対する一貫した需要、画像取得と解釈における人工知能(AI)の急速な普及、プライマリケアにおけるハンドヘルドプローブの普及がこの成長を支えています。臨床的エビデンスによれば、AIガイダンスにより、専門家以外が実施したスキャンの診断品質は98.3%まで向上し、専門医のパフォーマンスに匹敵します。成熟市場がプレミアム3D&4Dシステムの買い替え需要を牽引し続ける一方、新興国が公衆衛生プログラムを通じて初回購入を後押しします。CTやMRIにリアルタイムの超音波をオーバーレイするマルチモーダルフュージョンプラットフォームと組み合わせた低侵襲手技への軸足が、この技術の手技的役割を広げています。同時に、米国ではポイントオブケア機器に対する償還の格差が根強く、世界的な品質システム規制の強化により、その勢いは弱まっています。

世界の超音波診断装置市場動向と洞察

慢性疾患の増加

心血管疾患、腫瘍性疾患、呼吸器疾患が超音波検査紹介の大半を占めており、慢性疾患管理が構造的な需要促進要因となっています。卵巣腫瘍検出のためのAIモデルは、F1スコア83.5%を達成し、専門放射線科医を上回りました。同様に、ディープラーニングツールは、手根管スキャンで正中神経を高い精度で特定します。米国がん協会は、2025年に米国で新たに発生するがん患者数を2024年の200万人から204万人に増加させると予測しており、長期的な画像診断需要を強化しています。AIはワークフローを加速し精度を高めるため、訓練された超音波検査士の不足を補い、ユーザーベースを広げ、超音波診断装置市場を維持します。

増大する低侵襲診断と画像診断施設

針誘導生検、局所麻酔、筋骨格系注射への世界的な軸足は、超音波の手技的関連性を深めています。ライブ超音波とCT、MRI、PETスキャンを融合させたフュージョン・プラットフォームは、複雑な症例における病変ターゲティングを向上させています。施設の成長は、インストールベースを強化する:インドは2024年2月に5,200のNABL認定ラボを数え、その44%が放射線科でした。オーストラリアでは、2023年12月までに4,462の認定画像診療所がリストアップされ、その81%が人口の多い3つの州に集中していました。コロンビアドクターズ/NYプレスビテリアンのマンハッタンサイトのような新しいセンターが2025年1月にオープンし、高密度の都市部にサービスを提供しています。このような地理的な広がりは、高級機と中級機の両方に対する安定した需要につながり、超音波診断装置市場を強化しています。

ハンドヘルドスキャナーの償還制限

ポイントオブケア超音波(POCUS)には、プライマリケアの多くの適応症に対する専用の請求コードがないです。診療報酬モデルは、外来や在宅での超音波診断装置市場の抑制要因となり、幅広い普及を妨げています。最近のCMSの提案は前進を示唆するものであるが、民間支払者間の政策の分断は続いており、医療提供者の投資対効果を遅らせています。

セグメント分析

2024年の超音波診断装置市場売上高の23.3%は放射線学アプリケーションが占め、多臓器画像診断のニーズがその原動力となっています。卵巣悪性腫瘍にフラグを立てるAIモジュールは今や人間の専門知識を凌駕し、病院は放射線科ワークステーションのアップグレードを迫られています。また、エラストグラフィの改良により肝線維症の病期分類がより鮮明になり、非侵襲的スクリーニング・ライブラリの幅が広がっています。

手技誘導麻酔学は、規模は小さいがCAGR4.9%で拡大しています。神経ブロックの採用は、ScanNav Anatomy PNBのようなカラーオーバーレイの補助器具の恩恵を受けています。麻酔薬の使用量と術後痛の軽減に熱心な病院は、専用のリニアプローブを購入し、周術期の超音波診断装置市場を拡大しています。

ポイント・オブ・ケア・スキャナーに対する病院予算の増加は、オピオイド温存鎮痛を奨励する国家レベルのガイダンスとともに、麻酔科における2桁台の機器更新率を維持する可能性が高いです。AIがプリセットの画像プロトコルを作成するようになると、臨床医は超音波ガイド下ブロックを整形外科だけでなく、救急や集中治療環境にも拡大できると確信するようになります。このような部門横断的な波及効果により、利用率が向上し、スキャン1回あたりのコストが削減され、より広範な超音波診断装置市場において先進的プラットフォームへの投資の経済的根拠が強化されます。

3Dおよび4Dシステムは、2024年の超音波診断装置市場シェアの45.6%を占める。3Dおよび4Dシステムは、産科、小児科、循環器科などの体積可視化が必要な症例に使用されています。これらは、胎児の顔の特徴をリアルタイムで自動レンダリングする機械学習アルゴリズムによってサポートされています。このような自動化により、臨床医はノボロジーよりもカウンセリングに集中することができます。

HIFUは子宮筋腫から膵腫瘍まで、ニッチではあるが急速に拡大している治療領域に対応しており、CAGR 5.1%で成長すると予測されています。学術試験は、最小限の回復時間で有意義な症状緩和を示すものであり、中国と欧州の支払者が償還の枠組みを評価するよう促しています。外科部門がHIFUを腫瘍板に統合するにつれて、放射線科の予算内に収まる一方で収益源が多様化し、超音波診断装置市場の軌道が強化されます。

切除ゾーンを瞬時に定量化する統合AIダッシュボードは、術中の不確実性を低減します。この精度は、迅速なターンオーバーと感染リスクの低減が重視される外来デイケアモデルへの腫瘍学のシフトを補完します。その結果、高フレームレートイメージングと治療ビームを融合させるテクノロジーベンダーは、超音波診断装置市場において資本支出増の圧倒的シェアを獲得する可能性が高いです。

地域分析

北米は2024年に38.1%の売上シェアを維持したが、これは強力なペイヤーカバレッジ、高い慢性疾患負担、着実な技術更新サイクルによるものです。Vave Healthの全身ワイヤレス機器やGEヘルスケアの自動乳房超音波プレミアムなどの発売は、AIを組み込んだイノベーションに対する国内の意欲を示しています。規制の明確化と乳房密度スクリーニングのCPTコードが、これらのソリューションの迅速な導入を支えています。病院では救急部門にハンドヘルド・プローブを装備するケースが増えており、トリアージ時間を短縮してベッドフローを改善することで、超音波診断装置市場の活性化につながっています。

アジア太平洋地域はCAGR 4.8%で最も急成長している地域です。中国は、MindrayのConsonaシリーズのような国産コンソールを好む調達プログラムを通じて、この地域の台数を独占しています。ウィプロGEのVersana Premier R3は、ベンガルールで組み立てられたAI対応システムです。過密なプライマリケアセンターでのポイントオブケア超音波の採用により、初回購入が加速しているが、PCPNDT法により産科の台数は抑制されています。とはいえ、公的保険会社による肝臓検査や心臓検査の払い戻しが増加しており、超音波診断装置市場の地域的な上昇を支えています。

欧州は依然として技術重視の市場です。欧州医薬品庁(European Medicines Agency)のような機関は確かな臨床データを要求しており、ベンダーは無線量画像や電子カルテとの相互運用性に関するエビデンスを提示するよう求められています。本態性振戦に対するInsightecのMRgFUSはドイツでNUBステータスを獲得し、償還を受ける。WONCA欧州は、一般開業医を対象とした体系的な超音波トレーニングを展開し、地域医療の裾野を広げています。これらの力学を総合すると、欧州は超音波診断装置市場への重要な貢献者であり続けています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 慢性疾患の発生率の増加

- 低侵襲診断の拡大と画像診断施設の増加

- 在宅妊娠モニタリングの普及

- 遠隔超音波ネットワークの拡大

- ポイントオブケア超音波の導入拡大

- AI強化画像再構成の需要

- 市場抑制要因

- ハンドヘルドスキャナの限定的な償還

- 承認のための厳格な規制

- ポータブルデバイスのバッテリー寿命の疲労

- 肥満患者の画像診断における音響減衰

- 規制の見通し

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測(金額は米ドル、数量は単位)

- 用途別

- 麻酔科

- 心臓病学

- 婦人科・産科

- 筋骨格

- 放射線科

- 集中治療

- 泌尿器科

- 血管

- その他の用途

- 技術別

- 2D超音波画像

- 3Dおよび4D超音波画像

- ドップラー画像

- 造影超音波

- エラストグラフィー

- 高強度焦点式超音波

- ポータビリティ

- 据置型システム

- ポータブルカートベースシステム

- ハンドヘルド/ポケットデバイス

- エンドユーザー別

- 病院

- 診断画像センター

- 外来手術センター

- 産科・不妊治療クリニック

- 在宅ケアの設定

- 動物病院

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- GE HealthCare Technologies Inc.

- Siemens Healthineers AG

- Canon Medical Systems Corp.

- Koninklijke Philips N.V.

- Fujifilm Sonosite Inc.

- Samsung Electronics Co. Ltd

- Shenzhen Mindray Bio-medical Electronics Co., Ltd.

- Hologic Inc.

- Esaote SpA

- Butterfly Network Inc.

- Clarius Mobile Health Corp.

- Terason Division

- Carestream Health

- Shantou Institute of Ultrasonic Instruments

- Sonoscape Medical Corp.

- Chison Medical Imaging Co.

- DRAMINSKI S.A.

- Holisto Veterinary Ultrasound

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日