|

市場調査レポート

商品コード

1639355

精製触媒-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Refining Catalysts - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 精製触媒-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

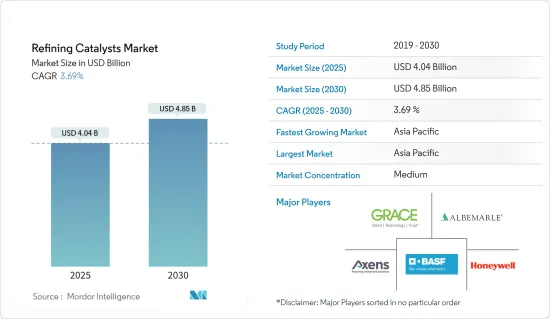

精製触媒市場規模は2025年に40億4,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは3.69%で、2030年には48億5,000万米ドルに達すると予測されます。

COVID-19の発生は、石油精製製品の消費減少により市場にマイナスの影響を与えました。しかし、2021年には産業は回復し、市場の需要は回復しました。

主要ハイライト

- 短期的には、製油所への投資の増加と高オクタン価燃料への需要の加速が市場を牽引する主要要因です。

- 反面、貴金属価格の変動は市場成長の妨げになると予想されます。

- ナノ触媒への関心のシフトは、将来的には好機となると考えられます。

- アジア太平洋は石油精製触媒の最大市場であり、世界シェアのほぼ半分を占めています。

精製触媒マーケット動向

流動接触分解(FCC)触媒がマーケットを支配する

- 流動接触分解(FCC)プロセスは、原油から軽い製品を生産する製油所で重要な役割を果たしています。

- FCC装置は、分解ガス油、軽油、脱アスファルトガス油、真空/大気圧樹脂など、さまざまなタイプの原料を、軽油、ジェット燃料、LPG、灯油、ガソリンなど、より軽量で高価値の製品に変換するのに役立ちます。

- 原料はFCC装置内で高温・中圧で加熱されます。これとともに、原料は触媒と接触させられ、高沸点炭化水素液体の長鎖分子を低分子に分解し、さらに蒸気として回収されます。

- FCCプロセスでは、触媒は微粉末として使用されます。以前は、アモルファスシリカ・アルミナなどの触媒が、FCC装置で真空ガス油を分解するために使用されていました。しかし、1960年代初頭にゼオライトがFCC触媒として商業的に導入され、接触分解の歴史において大きな進歩を遂げました。例えば、Indian Oil Corp(IOC)は、ハリヤナ州パニパットにある製油所の拡大に43億9,000万米ドルを投じる予定です。この拡大計画は2024年9月までに完了する予定で、製油所の生産量を年間1,500万トンから2,500万トンに拡大します。

- 上記のような要因から、FCC触媒は予測期間において精製触媒の市場需要を促進する上で重要です。

アジア太平洋が市場を独占する

- アジア太平洋は石油精製用触媒の最大市場であり、世界シェアのほぼ半分を占めています。

- 中国が主要な市場ホルダーであり、同地域の40%以上を占めています。中国の石油精製能力は世界の精製能力の14%以上を占めています。

- さらに、インドのトップ石油精製会社のひとつであるIndian Oil Corpは、今後5~7年間に既存のブラウンフィールド製油所を拡大するため、76億4,000万米ドルを含む229億1,000万米ドルの投資を計画しています。

- 韓国では、エチレンプラントの能力増強とアジアにおけるプラスチック需要の増加により、ナフサの使用量は引き続き拡大するとみられます。例えば、2022年の韓国の燃料油生産量は約13億6,000万リットルで、2021年比で28.55%の増加を示しました。韓国の燃料油生産量は近年増加しています。そのため、同国における燃料の生産量の増加は、精製触媒市場の需要増につながると予想されます。

- さらにインドネシアは、輸入石油製品への依存度を最小限に抑えるため、石油精製能力をほぼ増強する計画を加速させています。政府は2030年までに、国内の石油生産量を100万B/Dまで増加させたいと考えています。そのためには、老朽化した油田の回収方法を改善するための追加調査と投資を促進する必要があります。

- 以上のような要因が、予測期間中、同国の石油精製触媒市場を牽引すると予想されます。

精製触媒産業概要

精製触媒市場は、その性質上、部分的に統合されています。この市場の主要企業には、W. R. Grace &Co.-Conn、Albemarle Corporation、BASF SE、Axens、Honeywell Internationalなどが含まれます(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 高オクタン価燃料の需要加速

- 石油・ガス活動の拡大

- その他の促進要因

- 抑制要因

- 貴金属価格の変動

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模(金額・数量))

- 製品

- CoMo

- ニッケルモリブデン

- アルミナ系貴金属

- NiW

- ゼオライト

- その他

- プロセス

- 水素化処理

- ガソリン

- 灯油

- ディーゼル

- 真空ガスオイル

- 接触分解ガソリン

- 残留フィード

- 流動接触分解(FCC)

- 残留流体接触分解(RFCC)

- 水素化分解

- 水素化処理

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ASEAN諸国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Albemarle Corporation

- Axens

- BASF SE

- China Petrochemical Corporation

- Exxon Mobil Corporation

- Topsoe

- Honeywell International

- JGC C & C

- Johnson Matthey

- Royal Dutch Shell PLC

- W. R. Grace & Co.-Conn

- Chevron Lummus Global(CLG)

- KNT Group

第7章 市場機会と今後の動向

- OPEC諸国における今後の投資と生産能力増強

- その他の機会

The Refining Catalysts Market size is estimated at USD 4.04 billion in 2025, and is expected to reach USD 4.85 billion by 2030, at a CAGR of 3.69% during the forecast period (2025-2030).

The COVID-19 outbreak negatively impacted the market due to reduced consumption of oil-refined products. However, the industry witnessed a recovery in 2021, thus rebounding the demand for the market studied.

Key Highlights

- Over the short term, increasing investment in refineries and the accelerating demand for higher octane fuel are the major factors driving the market studied.

- On the flip side, the volatility in precious metal prices is expected to hinder market growth.

- The shifting focus toward nanocatalysts will likely act as an opportunity in the future.

- Asia-Pacific region accounted for the largest market for refining catalysts, with almost half of the global share, and is also expected to be the fastest-growing market.

Refining Catalysts Market Trends

Fluid Catalytic Cracking (FCC) Catalysts to Dominate the Market

- The fluid catalytic cracking (FCC) process plays a crucial role in refineries while producing lighter products from crude oil.

- FCC unit helps in converting a variety of feed types, such as cracked gas oil, gas oil, deasphalted gas oils, vacuum/atmospheric resins, and others, into lighter and high-value products, such as diesel oil, jet fuel, LPG, kerosene, and gasoline.

- The feedstock is heated at high temperatures and moderate pressure in the FCC unit. Along with this, the feedstock is brought in contact with a catalyst which helps break the long-chain molecules of the high-boiling hydrocarbon liquids into small molecules, which are further collected as vapors.

- In the FCC process, the catalysts are used as fine powders. Previously, catalysts, such as amorphous silica-alumina, were used for cracking vacuum gas oils in the FCC unit. However, in the early 1960s, zeolite was commercially introduced as an FCC catalyst, a significant advancement in the history of catalytic cracking. For instance, the Indian Oil Corporation (IOC) intends to spend USD 4.39 billion on expanding its oil refinery in Panipat, Haryana. The extension scheme, which is expected to be completed by September 2024, will expand the refinery's production from 15 million tons annually to 25 million tons annually.

- Due to the abovementioned factors, FCC catalysts are important in propelling the market demand for refining catalysts in the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific region accounted for the largest market for refining catalysts, with almost half of the global share, and is also expected to be the fastest-growing market.

- China is the primary market holder, accounting for more than 40% of the region. China's refinery capacity accounts for over 14% of the world's refining capacity.

- Additionally, one of the top oil refiners in India, Indian Oil Corp, plans to invest USD 22.91 billion, including USD 7.64 billion, for expanding its existing brownfield refineries in the next 5 to 7 years.

- Naphtha use will likely continue expanding in South Korea due to capacity additions at ethylene plants and the rising demand for plastics in Asia. For instance, in 2022, the production volume of fuel oil in South Korea amounted to around 1.36 billion liters, which shows an increase of 28.55% compared to 2021. Fuel oil production in South Korea has risen in recent years. Therefore, increasing the production volume of fuel in the country is expected to create an upside demand for the refining catalysts market.

- Moreover, Indonesia is speeding up plans to nearly increase its oil refining capacity to minimize its reliance on imported petroleum products. By 2030, the government wants to increase domestic petroleum output to 1 million bpd. It seeks to do this by stimulating additional research and investment in improved recovery procedures for aging fields.

- All the factors above, in turn, are expected to drive the market for refining catalysts in the country during the forecast period.

Refining Catalysts Industry Overview

The refining catalysts market is partially consolidated in nature. The major players in this market include (not in any particular order) W. R. Grace & Co.-Conn, Albemarle Corporation, BASF SE, Axens, and Honeywell International, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Accelerating Demand for Higher-Octane Fuel

- 4.1.2 Expansion of Oil and Gas Activities

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Volatility in Precious Metal Prices

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value and Volume)

- 5.1 Product

- 5.1.1 CoMo

- 5.1.2 NiMo

- 5.1.3 Alumina-based Noble Metal

- 5.1.4 NiW

- 5.1.5 Zeolites

- 5.1.6 Other Products

- 5.2 Process

- 5.2.1 Hydrotreating

- 5.2.1.1 Gasoline

- 5.2.1.2 Kerosene

- 5.2.1.3 Diesel

- 5.2.1.4 Vacuum Gas Oil

- 5.2.1.5 Catalytic Cracking Gasoline

- 5.2.1.6 Residual Feed

- 5.2.2 Fluid Catalytic Cracking (FCC)

- 5.2.3 Residue Fluid Catalytic Cracking (RFCC)

- 5.2.4 Hydrocracking

- 5.2.1 Hydrotreating

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Albemarle Corporation

- 6.4.2 Axens

- 6.4.3 BASF SE

- 6.4.4 China Petrochemical Corporation

- 6.4.5 Exxon Mobil Corporation

- 6.4.6 Topsoe

- 6.4.7 Honeywell International

- 6.4.8 JGC C & C

- 6.4.9 Johnson Matthey

- 6.4.10 Royal Dutch Shell PLC

- 6.4.11 W. R. Grace & Co.-Conn

- 6.4.12 Chevron Lummus Global (CLG)

- 6.4.13 KNT Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Upcoming Investments and Capacity Additions in OPEC Countries

- 7.2 Other Opportunities