|

市場調査レポート

商品コード

1849885

装甲材:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Armor Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 装甲材:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月19日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

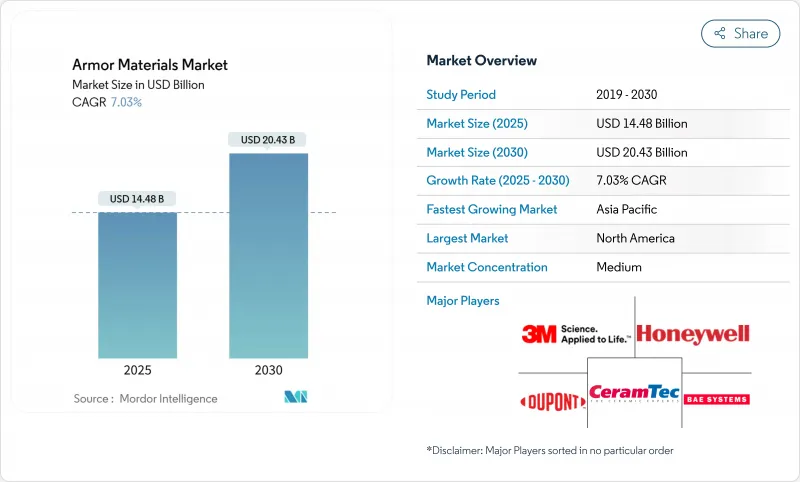

装甲材市場の2024年の市場規模は144億8,000万米ドル、2030年には204億3,000万米ドルに達し、2025年から2030年までのCAGRは7.03%で拡大すると予測されています。

現在の需要は、セラミック、金属基複合材料、超高分子量ポリエチレン(UHMWPE)の急速な進歩に加え、軍事、法執行、重要インフラ環境における脅威レベルの高まりが原動力となっています。軽量ハイブリッド・ソリューションの採用促進、警察官用防護具に補助金を支給する政府プログラム、海軍・宇宙計画の加速化などはすべて、調達予算の増加に寄与しています。一方、チタンや炭化ホウ素のような戦略的鉱物の供給不安は、バイヤーに材料ポートフォリオの再設計と非常用在庫の積み増しを迫り、リサイクル業者や二次加工業者にニッチな機会を開きます。競合の動きは緩やかで、化学や先端材料の大企業が依然として優位を占めているが、ナノ強化セラミックスに特化した新興企業が、特に持続可能性の証明やサーキュラー・エコノミー・サービスが重視される分野で牽引力を増しています。

世界の装甲材市場の動向と洞察

防護服と先端兵器の開発

Angel Armor社の2024 Truth SNAPプレートシステムは、磁気カップリングがモジュール性を実現する一方で、0.65ポンドという軽量プレートがオペレーターの機敏な動きを維持することを実証しました。UHMWPE/炭素繊維強化プラスチック(CFRP)などのハイブリッドレイアップは、レガシーラミネートよりも28%低い背面変形を達成し、マルチマテリアルスタックがより低い質量でレベルIV保護に匹敵することを証明しました。実地試験では、セラミックとUHMWPEのハイブリッドが複数の被弾に耐えることが確認され、アルミニウムとチタンと炭化物の金属マトリックス複合材は、圧延された均質な装甲と比較して弾道限界速度を30%向上させました。これらの技術革新は、装甲材市場の性能上限を高め、生存性を犠牲にすることなく、より軽量な構成に向けて調達を後押しします。

国土安全保障への関心の高まり

連邦政府および州政府の資金は、地方機関に直接流れています。FBIレガシーボディアーマープログラムは、すでに約70万米ドルのプレートとベストを、以前は警官の41%が義務的な着用方針を持っていなかった小規模な部署に譲渡しました。米国国土安全保障省は2025年度予算として1,074億米ドルを要求しており、その中には防護服のアップグレードに10億800万米ドルを充てる補助金も含まれています。欧州とアジアの一部でも同様の制度があり、購入サイクルを加速させ、装甲材市場の数量成長を持続させています。

不安定なチタンと炭化ホウ素の原料価格

米国地質調査所の2025年サマリーは、一握りの生産者に供給が集中することによって引き起こされる、スポンジチタンを含む戦略的金属のスポット価格の頻繁な変動を指摘しています。一方、GAOのデータによると、国防総省は99の材料不足を記録し、2019年比で167%急増し、ホウ素カーバイドは繰り返し「単一供給源」と指摘されています。サプライヤーが課徴金を課す中、装甲メーカーは迅速に調整されることの少ないコストプラス契約と格闘し、装甲材市場全体のマージンを侵食しています。

セグメント分析

2024年には金属と合金が売上高の52%を占めるが、セラミックと複合材料は7.22%のCAGRで装甲材市場全体を牽引しています。炭化ケイ素タイルは現在、3.2g/cm3未満の密度で同程度の耐弾性を実現し、戦闘機の胴体キット1個当たり数キログラムの積載量を削減します。千鳥配置のハーフラップジョイント設計に関する研究結果では、最適化されたセラミック形状が、より低い厚みで米軍のプロトコルに完全に準拠することが確認されています。その結果、調達機関は仕様をより軽量なプレートに再調整し、この動向は装甲材市場内のサプライヤー構成を再構築しています。

構造用セラミックは、UHMWPEの裏打ち材と相性がよく、マルチヒット能力を35%向上させる。Elium熱可塑性樹脂を使用したケブラー/UHMWPEラミネートに関する並行調査では、エネルギー吸収率が25%高く、重量が22.44%減少しました。パラ系アラミド繊維の採用は堅調な伸びを維持しているが、UHMWPE繊維は優れた引張強度と熱老化特性の改善により、現在最も急速に採用が進んでいます。これらの力学が相まって、投資が従来のスチールからハイブリッド・スタックへとシフトし、装甲材市場の先端複合材料への軸足が固まっています。

地域分析

北米は2024年の売上高の38%を占め、米国の国防予算と活発な研究開発によって支えられています。現在進行中の空軍研究所のプログラムにより、高エントロピー合金やナノ加工セラミックスの画期的な技術がそのまま生産に投入され、技術移行のタイムラインが短縮されています。連邦のバイ・アメリカン法は、地域のサプライヤーをさらに孤立させ、装甲材市場を安定させる。

アジア太平洋はCAGR 7.45%で最も急成長しているクラスターです。中国は炭化ケイ素の国産焼結に多大な資源を投入し、インドのDRDOは暑い気候に合わせた繊維強化ポリマー複合材を開発しています。韓国とオーストラリアでは、海軍の並行調達が耐食性装甲鋼と複合船首インサートの需要を押し上げ、この地域の顧客基盤を拡大しています。

欧州は戦略的鉱物アクセスに取り組んでいます。EUの重要原材料法は、2030年までに国内処理率40%、リサイクル率15%を目標としており、炭化ホウ素回収とチタンスクラップ改良への新たな投資を促しています。PESCO(Permanent Structured Cooperation)の枠組みの下での国境を越えた協力が次世代ヘルメット・プログラムを加速させ、厳しい予算にもかかわらず装甲材市場を革新的なものにしています。

中東とアフリカは一桁台半ばの成長を記録。調達の中心は対IED車両キットとエネルギー施設の周辺要塞です。また、UAEなどの国家は、計画中の近宇宙観光のためのマイクロメテオロイド遮蔽調査にも資金を提供しており、装甲材市場を新興の航空宇宙分野にも拡大しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 防弾チョッキと先進兵器の開発

- 国土安全保障への懸念の高まり

- 非対称戦争とIEDの脅威の増加により、耐爆性車両装甲の需要が高まっている

- 微小隕石遮蔽材を必要とする商業宇宙飛行および近宇宙観光の拡大

- 海軍艦隊の近代化の加速により耐腐食性装甲鋼の必要性が高まっている

- 市場抑制要因

- チタンと炭化ホウ素の原料価格の変動が生産コストを押し上げている

- 国境を越えた技術移転を制限する厳格な輸出管理規制

- 複合装甲材料のリサイクルと寿命の課題

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替製品・サービスの脅威

- 競合の程度

第5章 市場規模と成長予測

- 製品タイプ別

- 金属および合金

- セラミックおよび複合材料

- パラアラミド繊維

- 超高分子量ポリエチレン(UHMWPE)

- その他の製品タイプ(例:グラスファイバー、カーボン、ナノ強化)

- 用途別

- ボディアーマー

- 車両用装甲

- 航空用宇宙

- マリーンアーマー

- 民間用装甲

- エンドユーザー別

- 防衛

- 国土安全保障と法執行

- 民事および商業

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動き(合併・買収、合弁事業、契約)

- 市場シェア分析

- 企業プロファイル

- 3M

- Arconic

- ArmorSource, LLC

- ATI Inc.

- BAE Systems

- CeramTec GmbH

- CoorsTek Inc.

- CPS Technologies

- dsm-firmenich

- DuPont

- Honeywell International Inc.

- HS HYOSUNG ADVANCED MATERIALS

- JPS Composite Materials

- Koninklijke Ten Cate BV

- Morgan Advanced Materials

- NP Aerospace

- Plasan

- PPG Industries, Inc.

- Rochling SE & Co. KG

- SafeGuard Armor

- Saint-Gobain

- Schunk Carbon Technology

- Tata Steel

- Teijin Aramid